In this post I am presenting my investment thesis for SastaSundar Ventures.

Industry structure and Tailwinds

The frost and Sullivan report from 2018 does a good job of explaining the e-pharmacy industry. To summarize the 50 page report in a few points:

- Macro factors: india has a large and aging population. Healthcare Spending as % of GDP will increase. GDP will increase. Indian Pharma market will increase.

-

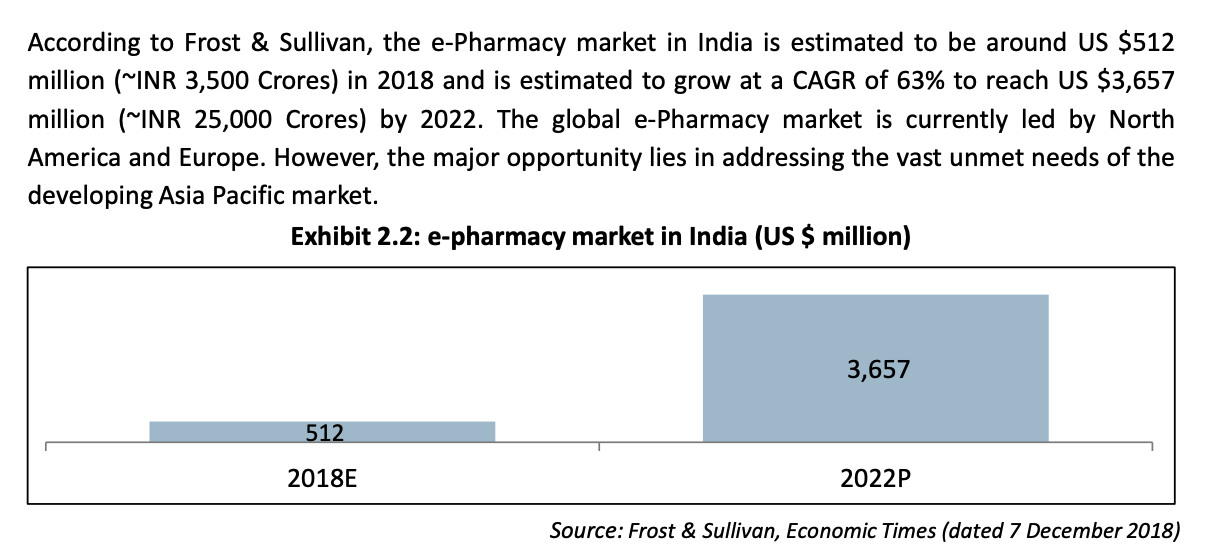

e-Pharmacy Growth: the e-Pharmacy market in India is estimated to be around US $512

million (~INR 3,500 Crores) in 2018 and is estimated to grow at a CAGR of 63% to reach US $3,657 million (~INR 25,000 Crores) by 2022. If you check the YoY growth figures of large e-pharmacies, this won’t seem like a stretch to you. - The e-Pharmacy model could account for 15%-20% of the total pharma sales in India over next 10 years, largely by enhancing adherence and access to medicines for a majority of the under-served population. If the Pharma market becomes 2.5x from 41B$ in 2021 to 100B$ in 2030 (9.5% CAGR), then e-pharmacy would be a 20B$ opportunity in 2030. That would be a CAGR of 24% for 8 years between the 2 estimates of e-pharmacy market size F&S provide to us. 63% growth for 3-4 years, and 24% growth for 8 more years.

- Key drivers for high industry growth: internet penetration, GoI digital india initiative, e-healthcare initiatives by GoI, increase in health insurance penetration, ayushman bharat, changing disease pattern from communication to lifestyle diseases (require frequent medication), growth in indian economy.

- There are 2 business models prevalent in the sector: inventory based and market-place model. In inventory based, company maintains inventory of the medicines and in marketplace based, user is matched to a seller of medicine. In fact this is the case for all ecommerce websites/apps. Most of them like Amazon and Flipkart are hybrid. They keep inventory and serve as a marketplace with inventory maintained by the seller.

- Key risks to existing e-pharmacy players: B&M chains like Apollo pharmacy can establish online presence, established e-commerce players can enter (already happened with amazon and reliance), risk of consolidation (already happening)

- Healthcare ministry recently (2018) announced some good e-pharmacy rules/guidelines. Key/primary takeaway for me was that e-pharmacies cannot advertise in any way or form on any medium. Need to share data with government for public good. Cannot sell certain classes of drugs like habit forming drugs.

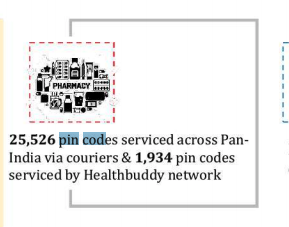

- Why there is a need for e-pharmacies: single retail pharmacies due to their low volume purchase drugs at high prices from distributors. e-pharmacies due to large-scale purchase (from distributors or sometimes pharma companies directly) are able to drive better bargains and thus make the system as a whole more efficient. Quality also goes up since single retail pharmacies cannot control for quality easily. Very hard for single retail pharmacies to stock all drugs forcing customers to visit multiple pharmacies. No such problem for e-pharmacies since inventory and orders are centrally managed. e-Pharmacies have the resource to invest in the latest information technology software. Digitalization of pharmacies enables them to record and track transactions and increase productivity. e-pharmacies due to their centralized approach are also able to deliver to many rural locations in the country, which is a first. Many of these places do not have any proper B&M pharmacies even.

SastaSundar Business Model

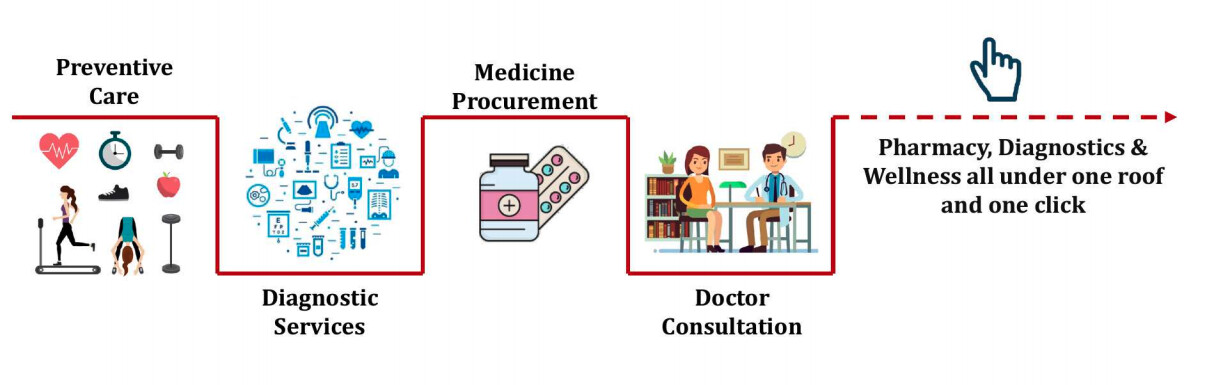

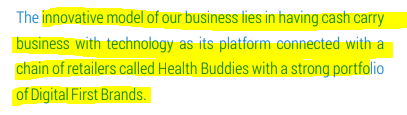

The name of the company is essentially a callback to indian values of Savings and Quality. While some urban indians might find it funny or cringe worthy, I think most indians would appreciate the values it represents. SastaSundar has 3 business verticals. e-Pharmacy, FMCG (Own brands + other brands), diagnostics. Their mission statement is “Providing comprehensive solution for all the healthcare needs- from preventive care to diagnostics to medicine procurement to doctor consultation”.

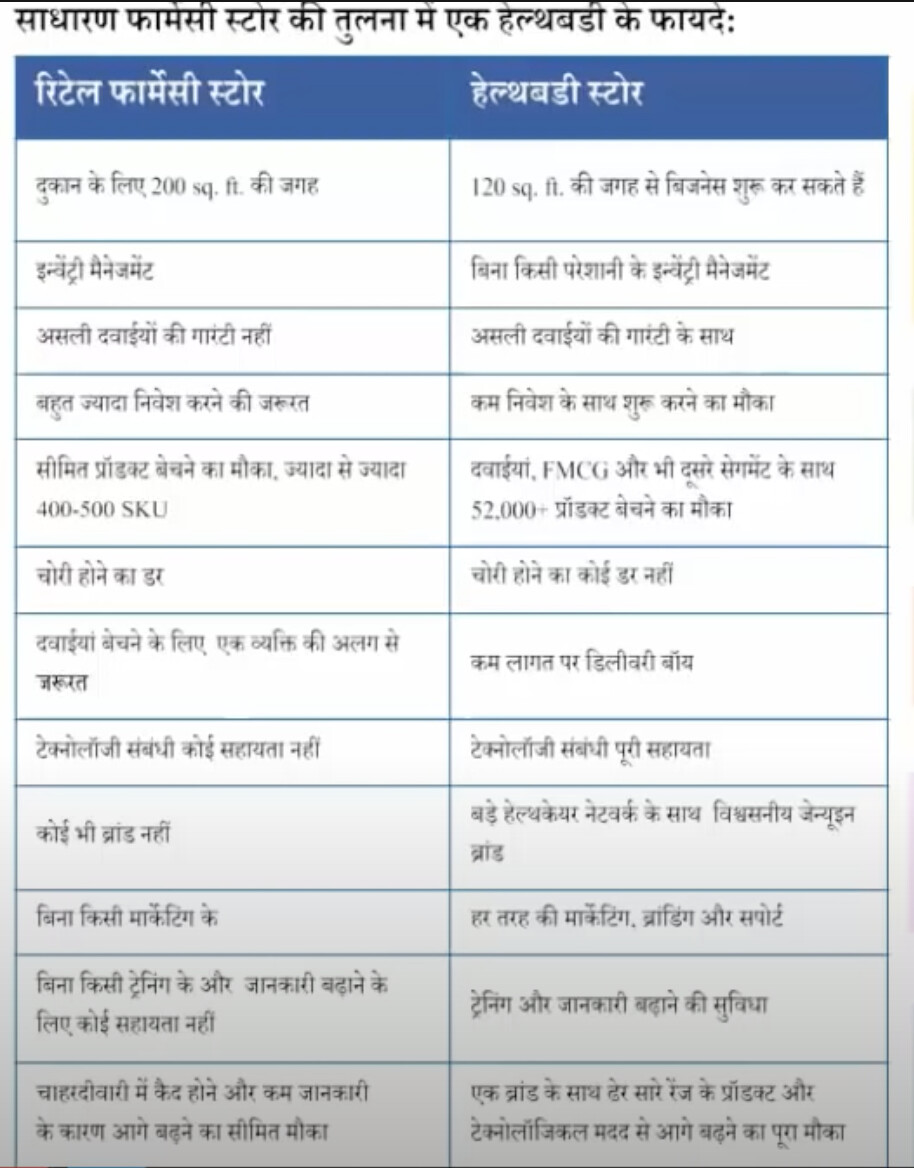

The core business is the e-pharmacy business. They only make 2cr from the diagnostics biz which is why most of the analysis is for the e-pharmacy biz. Sastasundar has an interesting hybrid sort of online-offline business model. They allow users to either place an order online (on the app/website) or to walk into their stores which are asset/inventory light and place orders. Orders are always delivered to your home, even if you place an order inside their store. This is because SS understands the importance of inventory management. Customer experience suffers if pharmacist tells them “I dont have medicine X”. Hence, thanks to their inventory based model they are able to ensure that they always maintain enough stock of all medicine and fulfill all orders. So why do they have the storefronts? I personally find this angle fascinating. It helps in 3 ways:

- A lot of people who require medicine are old and digitally uneducated. Many of them also refrain from trying to learn how to use an app. all such folks can simply walk into the store.

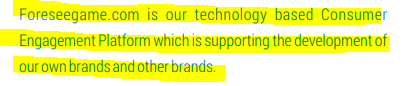

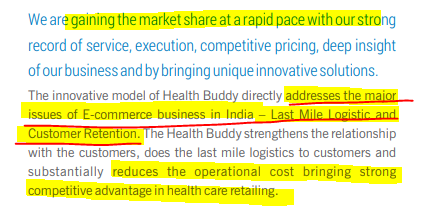

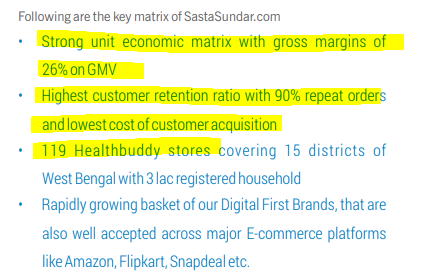

- This enables SS to utilize a key part of their differentiated offering. As highlighted in earlier posts, they have a concept of a health buddy. Think of this as your personal assistant. They’ll help you place an order, create a personalized relationship with you. Ensure you return back. No wonder that SS’s 90% orders come from repeat customers. This kind of customer loyalty is extremely hard to build. SS also ‘sweats’ their healthbuddy assets well by ensuring same person does multiple tasks for the company. This hybrid model ensures that SS has good brand loyalty.

- This hybrid model also ensures that they are able to capture mindspace of the customer. This is extremely important specially for e-pharmacies since they cannot advertise. The assetlight (inventory light) storefronts (which are franchises not owned by SS) also serve as a tool to stay in the mindspace of the customer. Have seen same mental model in other investments: Saregama (carvaan), and Google (Google home, pixel) and Amazon (Echo) etc.

SS also cross-sells FMCG and their own brands. Own brands are of course at a much higher margin and FMCG also, they dont provide much discount. This cross-selling enables convenience for the customer and helps them capture larger pocket share of the customer. If reliance can enter e-pharmacy, then SS can also sell biscuits. ![]()

They seem to have an interesting process in terms of how they select which OTC medicine to sell.

Screenshot 2021-05-22 at 8.03.38 AM|485x101

Their own brands have been created in a thoughtful way after analyzing the needs and wants of the customers and gaps/holes in the marketplace.

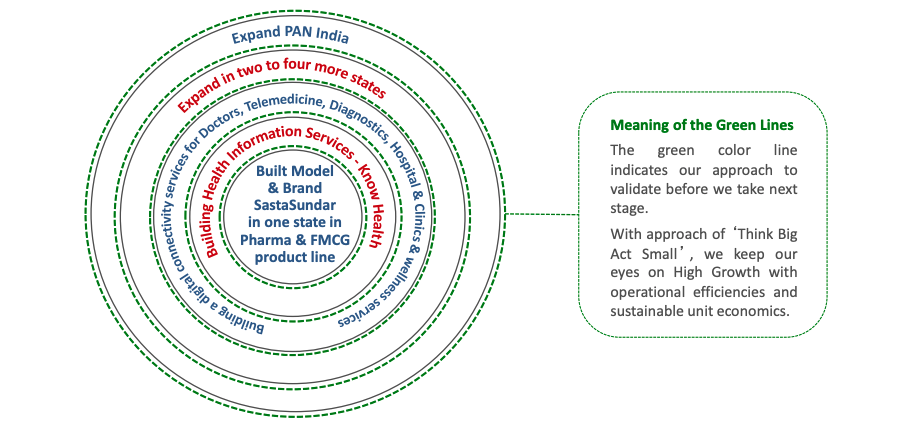

Perhaps the boldest slide one can find about SS is the vision 2024 slide in their FY18 investor presentation which has been removed from subsequent investor presentations. Suffice to say, management must have received feedback not to share 6 year aggressive visions, but the fact that this slide appeared in public domain leads credence to the hypothesis that this is what the management’s vision and targets are. Of course timelines can and will change and are dynamic. Whether this happens in 2024 ot 2026, it would be a great thing if and when management can meet these bold targets:

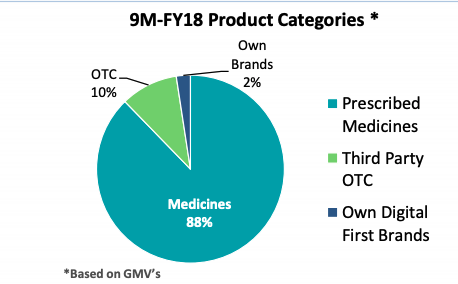

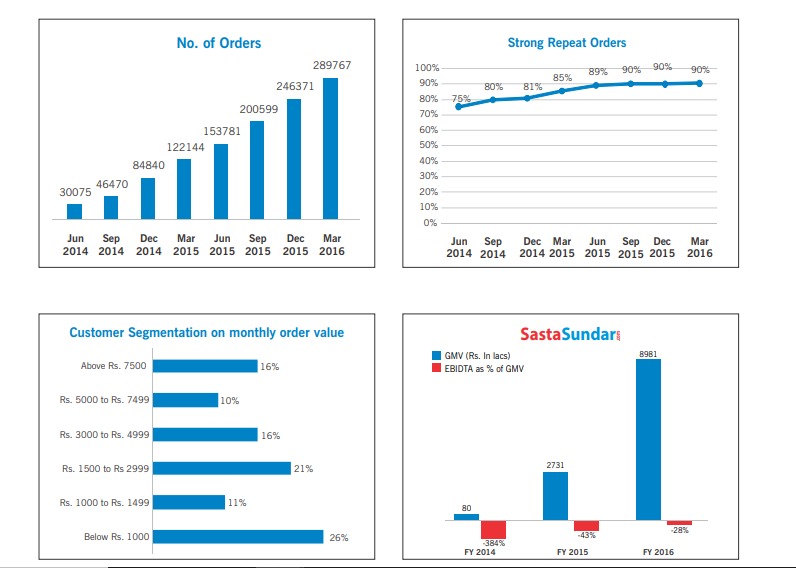

In FY18, the distribution of GMV (gross merchandise value) looked like this:

This sets a clear target of 7000cr of revenue with 15% EBITDA margins. We will analyze both the growth and profitability in subsequent sections.

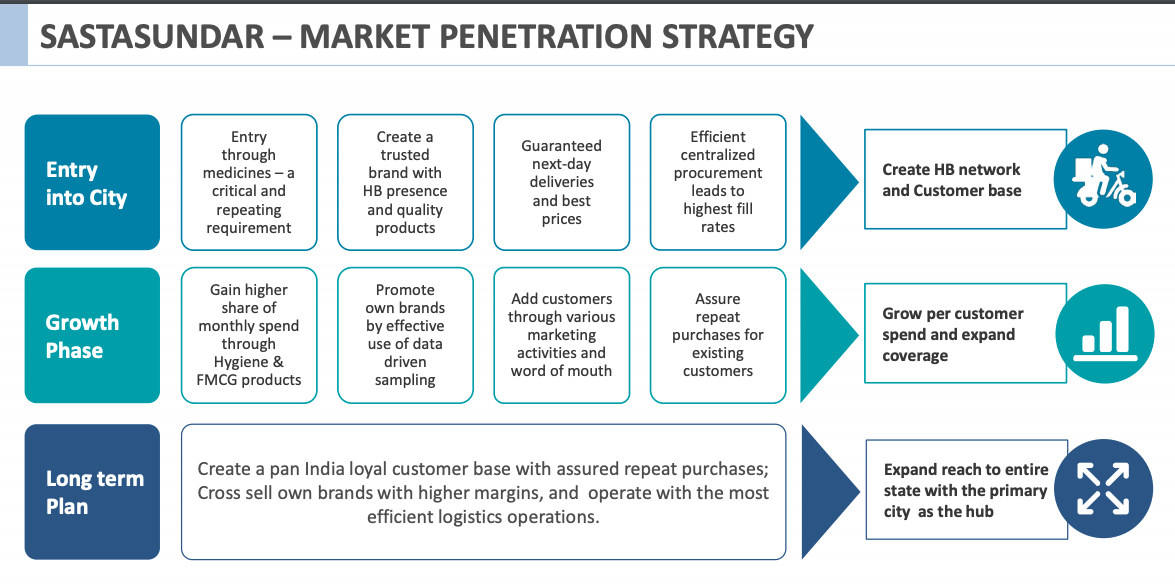

Management strategy for achieving the said growth:

Also to achieve this growth, SS is planning to target top 12 states in India, have 1 warehouse in each of the states, and open 250 micro pharmacies (SS assetlight stores) near each warehouse. They plan to capture 10% of the pharma market in each such region. (I think what they mean is 10% the e-pharmacy market).

SS also has a B2B initiative called ‘Retailershakti’ which would mean, SS would act as distributor for independent retail pharmacies, thus driving more efficiencies and revenues. Retailer Shakti provides competitive advantage to retailers’ customers in terms of wide range of products, price &

experience. It provides the widest assortment of 35000+ products across 120 categories from regional, national & international brands at one place to online retailers & wholesalers at good margins.

Most e-pharmacies allow one to get diagnostics done but they focus on tie-ups with existing brands. SS has taken a different approach by starting their own diagnostics called Genu labs. I like this approach for 2 reasons: industry has very good unit economics and secular growth runway. No need to provide discounts. Scale up here would boost overall business metrics. Genu labs is still very small. Did 2cr revenue in FY20 which was a 100% growth over FY19.

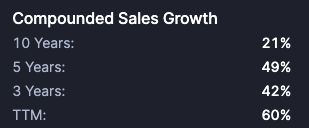

SastaSundar Growth

As far as I can tell, SastaSundar’s strategy is to remain near-profitable and grow in line with or slightly above average industry growth. We can see this in the past data.

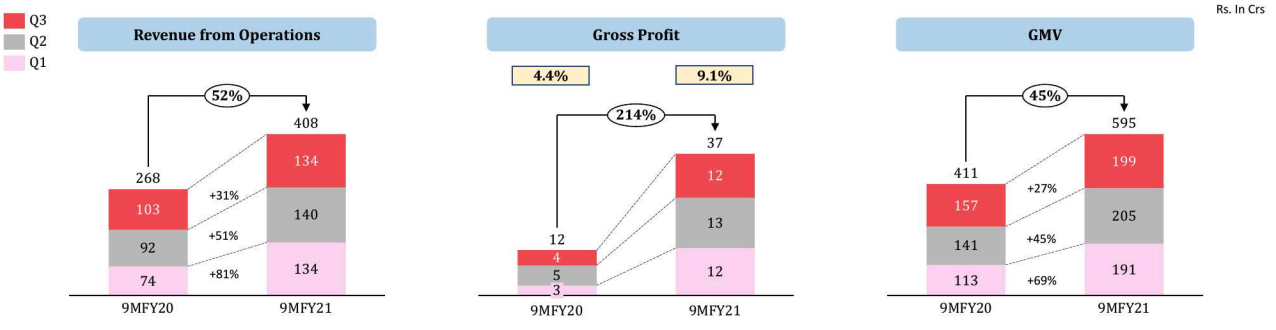

This being a high growth industry, growing in line with industry is perfectly normal in my opinion. We can see similar growth playout in the Q3FY21 and 9MFY21.

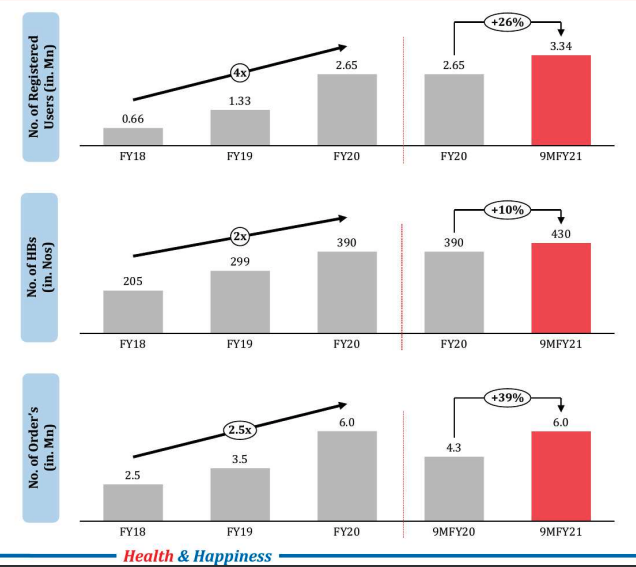

Do note how the number of HBs scales much slower than the number of users and revenue, thereby providing operating leverage.

SastaSundar Profitability

The company is still growing and yet to hit the inflection point wherein it can become profitable. We do know from the 2024 vision that they want to have 15% EBITDA margins. But how will they do it? Let us discuss.

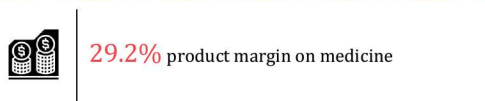

- As we can see from one of the first posts in the thread and also from the F&S report, centralized inventory planning enables the e-pharmacy to place bulk orders at the scale wherein they are able to buy considerably below MRP. How low? See the next point.

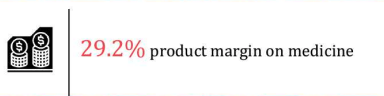

- In the latest Investor presentation, SS has claimed that they make 29% margins on medicines:

. This shows the power of buyer consolidation.

. This shows the power of buyer consolidation. - Then why does SS make losses at EBITDA level? Major driver is the 15% discounts they need to give right now to stay competitive with competition. Right now the industry norm is to provide at least 15% discounts on medicine. The industry is in its hyper-competitive stage. Consolidation is happening. Netmeds got sold out to reliance. Medlife and pharmeasy merged. The offline retailers (which forms the bulk of the market) do not like the 15% discount either. The 15% discount wont remain forever. Same thing played out in Telecom too. Post consolidation, the 15% discount is likely to go away. Then, the EBITDA profitability would emerge.

- Despite giving 15% discounts, SS is very close to breaking even at an EBITDA level: . If one looks closely this is happening both because with scale they are able to buy the medicines cheaply and also because employee costs are going down as they scale up and operating leverage plays out.

- Despite the need for inventory, this is an asset light business. Since the health-buddy centers are operated as franchises, the fixed assets have not growth since 2-3 years. They’re around 112 cr. Co has actually been stocking up on lot of inventory post covid to ensure smooth customer experiences and ensure there is no shortage. Despite that, their total WC is only 63 cr. This gives a total capital deployed of 175 cr. This gives us a capital deployed turnover ratio of 3. Even if co can make a 5% EBITDA margin, ROCE would be 15%. If they can make a moderate 10% EBITDA margin, ROCE would be 20% and if they can make their target EBITDA margins of 15%, ROCE would be 45%. This shows us that this industry (specifically this business model) does have favorable unit economics, once profits are made.

- I checked for international examples and US B&M retailers are able to make 5% EBITDA margins despite strong distributor consolidation. It is not a stretch of imagination to imagine that indian e-pharmacies can make 10% EBITDA margins especially with the asset light nature.

- They have no debt and negligible depreciation and so EBITDA margins would also end up being net margins, approximately.

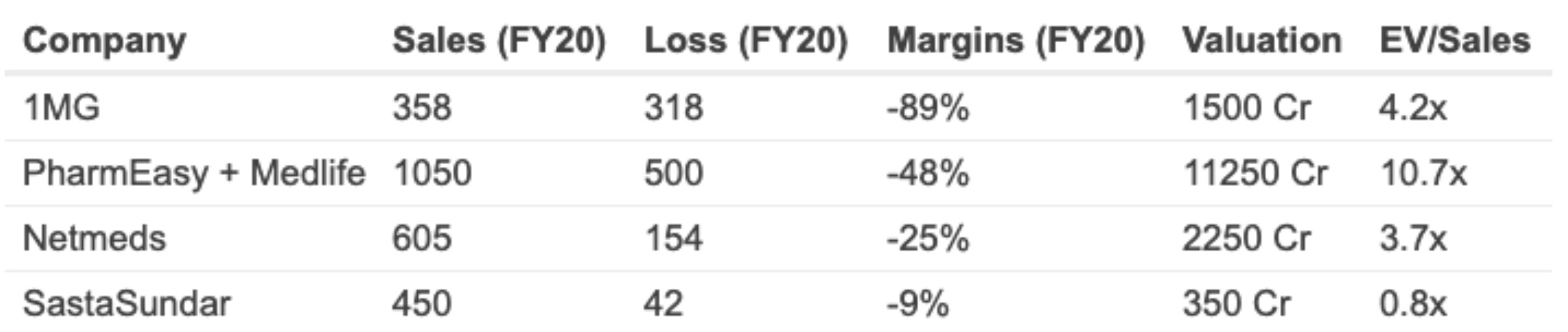

- As per a recent moneycontrol article (shared in this thread), their profitability is actually the best among all the players compared:

Equity Dilution & Fund raising

SS also desires to scale to pan india, which requires up front investments and capital. Public markets are ruthless and give SS a valuation of 1x sales due to its lack of profitability. Thus, company (technically listed company’s subsidiary) raises money from PE firms like its plan to raise 100M$ in the next 2-3 years from existing investors (who are strategic investors): SastaSundar Funding: SastaSundar in talks to raise $100 million - The Economic Times. For the hyper growth and pan-india presence this fundraising is required. It would lead to equity dilution for existing shareholders which is a key negative, but that is what life is like when one invests in a hyper-growth company which needs to raise funds. The good part is that last such fundraise they did was at 3x or 4x valuations of public market cap and so equity dilution is not as much as we fear it would be, plus if company can raise money more efficiently from PE players who are willing to value it higher, it is good for the investor for the long term. This fund raise would also be utilized to scale up Genu Labs which is a very welcome move due to favorable growth and unit economics of the business.

Valuations

As shared in previous section on profitability, SS trades at significant discount to peers who are all unlisted.

Risks

Key risks remain:

- Entire e-pharmacy industry could end up never making money (I place low probability on this event).

- SS could be acquired by a larger player. (Even in this case, i place low probability on loss of capital for public market investor).

- Equity dilution would result in dilution of ownership. (Cannot do anything, need to live with it).

- e-pharmacies could be profitable but SS could go bust/not make profits (Given that they are industry leading in terms of margins, I place low probability on this event).

- SS is a microcap stock and thus liquidity is low. All risks wrt ownership of microcaps apply here.

- Reliance and Amazon could offer deeper discounts (say 30%), and bleed out SS. (Due to their industry leading margins and almost close to breakeven, i place low to medium probability on this. Even SS can and does raise money, can slow their growth and compete on discounts. Would delay profitability for everyone. Still this remains the largest key risk in my books. One key observation is that we have not seen such behavior from amazon when they entered food delivery. Discounts were in line with zomato and swiggy).

Disc: This is not buy or sell advice. I am Invested with ~3% of PF. Most risky investment to date but risk-reward seems favorable to me. Would not advice anyone to invest large parts of PF into this one risky investment.

Sources:

Frost-Sullivan-Outlook-on-e-pharmacy-market-in-India (1).pdf (2.3 MB) Investors_Presentation_February_2018 (1).pdf (2.7 MB)

5697fa8f-66fe-4ec0-8055-f12855d2236c.pdf (4.1 MB)

This VP thread

{kind=link}