Hi All,

Wishing you a happy 2017.

Recently I came across an interesting smallcap company – rather a startup – called SastaSundar Ventures Ltd.

Why is it unknown?

There used to be a company called MicroSec Finance that offered multiple financial services with many subsidiaries– some of you have even quoted from research published by them on some good midcaps. Microsec seems to have experimented on a couple of business ideas and has zero-ed in on e-pharmacy business after seeing good initial traction. The listed entity converted itself from an NBFC into a Core Investment Company (holding company) and the main business is that of its subsidiary called SastaSundar HealthBuddy Pvt Ltd

About the Business (model):

SastaSundar operates in primarily the e-pharmacy space (84% of their revenues are from medicines; rest is from OTC/ FMCG products like green tea, sugar free snacks, hebal mouthwash, baby products etc). Their vision is to become a holistic healthcare network (network of doctors, telemedicine/ online consultations, knowledgebase of healthcare etc)

On the core business of epharmacy: They aggregate demand by attracting consumers digitally – primarily mobile app - (by giving a 15% discount (cost) and by home delivering the medicines (convenience). The target segment is the chronic patients (90% of their orders are medicines for chronic diseases like diabetes, blood pressure, cardio etc). This segment gives the best value prop for the consumer/patient since savings of Rs 300 on a Rs 2000 monthly regular purchase is a significant value.

The basic model is an inventory led model (warehouse) where medicines are procured at bulk rates from distributors/ manufacturers (could be 30% to 40% less than the retail prices – pharma margins are high as we know). Of this they share 15% back to the consumer as discount). The rest is divided between the HealthBuddy/Pharmacist and SastaSundar.

Private Labels: On the FMCG products, they seem to be launching their own private label brands – this will give them high margins over the long term.

Current Financials:

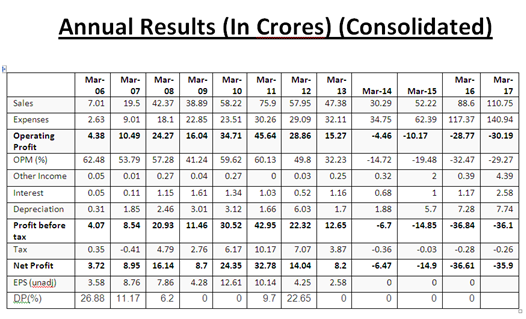

Currently the company is loss making (remember it’s a startup). They did Revenue of 86 Cr in FY16. In H1 of 2017, they have done Revenue of 76 Cr – so the growth has been rapid. Since it’s a startup, we won’t be able to able to do much financial analysis in the traditional sense. What would matter would be unit economics and breakeven timelines – and that they don’t burn money on customer acquisition and discounting.

Competitive landscape:

There are half a dozen well funded startups in the space. In terms of funding, NetMeds has led the pack (has taken $50m) , but in terms of a pure startup 1mg seems to be the leader (Close on their heels are companies like Pharmeasy, LifCare and Myra). All of these are well funded by well known VCs (http://tech.economictimes.indiatimes.com/news/startups/vcs-new-playground-is-online-pharma/55846201)

Risks:

Regulatory risk is very high as epharmacies operate in a grey area. Snapdeal got arrest warrants from FDA for selling medicines without a proper license. But the central government is supporting the epharmacy industry and looks like will come out with some sort of regulation in a few years (lot of news articles can be found regarding the same).

Offline players Lobby risk: The retail pharmacists fear that epharmacy will do to them what Flipkart and Amazon did to their retail counterparts and are heavily lobbying against the epharmacy industry. So this could delay the regulation, though in the long run the regulation will come. Given the political nexus in the pharma distribution business this could be more serious than what meets the eye.

Expansion/ Execution risk: SastaSundar has been able to execute this well in Kolkata. It remains to be seen if they will be able to replicate this model in other states. Especially given the well funded competitors who are strong in their cities/states where they started, this has to be closely watched on a quarterly basis.

Unit economics Sustainability: The company has mentioned that it would be profitable by FY18. This needs to be carefully watched on a quarterly basis. EBITDA has come down from -30% in Sep 15, to -15% in Sep 2016, so the trend is good.

Valuation:

Since the company is yet to breakeven, we cannot value the company using P/E. A more suitable approach would be GMV multiple that’s typically applied to an early stage ecommerce startup. On that basis this is around a multiple of 1 time the Sales, which appears low. Given the good repeat rates (around 80%), which makes it like a subscription business, and high margins of the pharma retail industry (aided by the multiple private label products launched), a valuation of 5 times Revenue looks reasonable at this stage if the growth momentum continues. The potential market size is quite large (Rs 1 lakh crores pharma sales in India in 2016; epharmacy is nascent and has huge headroom for growth). Risks around execution, especially around expansion outside home state of West Bengal; strong competition from multiple well funded players and; regulatory risks remain and could be priced into the stock.

Disclosure: have entered in this quarter with exposure around 10% of portfolio. This is not a recommendation, please do your own research.