Its actually sad that a company with such a good track record had to go through so much of pain, long process and time to get approval. Anyways, hopefully it should be just a matter of time now that they get all the approvals and can ramp up the huge mining potential. They have recently got the approval for manganese ore and hopefully final clearances for iron ore should also come in.

Add to this, there are lots of other expansions too going on - 1. Ferro alloy capacity will double over next 3 months 2. Beneficiation and pellet capacity will be put up over the next 1 year to improve ore quality and move up the value chain 3. DI capacity over next 2-3 years (though people worry about this but based on industry feedback, there is a huge demand in coming years as the govt is spending more on water infra) @tpatel - thanks for sharing about this hiring…shows the intent of the company to hire good talent and yes, they should get benefit of having all the RM inhouse.

Just wanted to quickly check on the Royalty side. Was going through the concalls and ARs of Tata Metaliks to understand Pig Iron and DI Pipes business in a better way and found that there is mention of Royalty in each call and ARs.

Moreover, the royalty for captive consumption of Iron Ore is even more. Below is the snippet from Tata Metalik Q3 FY22 concall.

“The additional royalty which Tata Metaliks had to pay, because of the government regulation, which came in for increasing the royalty on iron ore from 15% to 37.5%, for fines and for lumps, it went up from 15% to 52.5%. So, if you buy from a captive mine owner like Tata Steel, you have to pay that much extra.”

This change in the royalty seem to have direct impact on the bottom line of the company. Can we expect similar type of royalty in case of Sandur when their DI Pipe & Pig Iron production starts? At this point of time I could not find much mention of royalty in the ARs of Sandur.

Royalty gets revised/changed when a mine comes up for re-auction. Will need to see what happened in the case above…probably Tata steel mine would have got renewed on higher royalty

Thanks. I will check Tata Steel concall for the details. However, just wanted to know if Royalty element would be there in case of Sandur as well, right? When they will start DI Pipes and Pig Iron business?

Also, does Sandur have to pay royalty today as well for the excavation of Iron and Manganese Ore?

You will have to go through the Mining Act and the major changes which came in few years back.

In nut shell, no, royalty is not charged due to DI operations. the royalty amount changes when mines come for renewal as there is an auction. The rate depends on the rules and competition at that time.

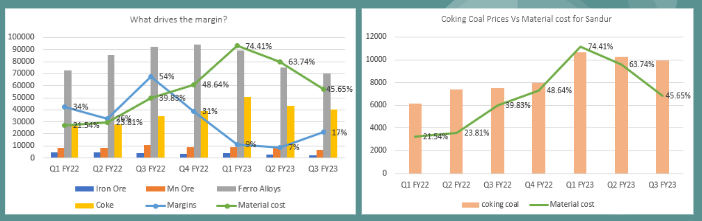

Yes, its mainly because of the coking coal prices, which is main RM for coke & energy division. I was trying to establish this relation and this is what I have found.

From the first graph, the realisations seem to have minimal impact on the margins, on the other hand, material cost is the one which affects the margins.

The second graph is the material cost as % of the expenses for Sandur Vs the coking coal prices (taken from Coal India). It shows good correlation between material cost for Sandur & coking coal prices.

Thus, the margins for Sandur are function of the coking coal prices which is major raw material for the company.

Note: As per my understanding, Sandur imports coal from countries like Australia, but for this exercise, I have taken the prices from Coal India, with the assumption that prices from coal India would be similar to that of international coal prices.

I have been getting several queries about Sandur given that Q4 nos look really good. Few thoughts:

Don’t annualize Q4 nos. these won’t repeat until the next phase of growth happens. The mining segment did very well in this quarter as the co sold around 60% of their annual limit in this quarter. This year was very volatile as there was mining ban etc and prices were very volatile. Co managed this very well.

Finally the much awaited expansion approvals have come for the mining segment. There should be big scale up from Q3FY24.

Good thing is that the most lucrative segment - Mining will see material investments as the co will put up beneficiation and pellet plant and this segment can scale 2.5 to 3x in next 2-3 years.

negatives - there is lot of pressure on the other business segments given the softness/downturn in commodity/steel sector. Coke prices have fallen a lot and probably there maybe some pain due to this in near term.

Biggest issue with Sandur is- the mining lease has only 10 yrs left.

10 yrs from now- mining revenue and profits will be a big zero.

How will you value a company whose majority of profits and revenues will become zero in just another 10 years?

This is a very unique case.

Let us say non-mining revenues and profits go up 4x in 10 yrs.

What’s the net sales/profit growth over 10 yrs in that case? (after accounting for zero mining revenues).

It shouldn’t be zero. The mine will come up for re-auction. The planning for forward capacity is with an intent to save the mine. From what I understand, as per rules, there is preference for captive mine owners and they have first right of refusal.

Many of these things will depend on circumstances at that time. But yes, the profitability will get impacted if there is lot of competition.

But this is true for almost all the mines in India and this is the reason there is arbitrage/advantage for mine owners whose mines are not to come up for renewal soon enough. Perhaps this is also the reason why iron ore prices are not falling hard in India (when international prices are falling) unlike the moves in past.

Right of first refusal has been taken away in an amendment I guess.

This is how the odisha mine auction happened- and original owners lost the mines- and JSW/Tata acquired them at huge premium.

There is no preference to anyone.

Rules are very transparent.

The highest bidder wins the mine- no preference to anyone.

Auctions happening at 100%+ premium- so the winner makes zero profits from the mines.

So, in that case, whats the total revenue/sales growth over 10 yrs for sandur? even if non-mining business grows many times. I guess it will be less than 8%.

Please correct if I am wrong.

Iron ore will become a scarce resource in another 10 yrs as steel industry demand will jump due to rising GDP per capita.

You can build new steel factories with money, but iron ore is a natural, limited resource.

This is why Tata steel and JSW are bidding for iron ore mines even at 120% premium- they are foreseeing the physical scarcity of iron ore 10 yrs from now.

Based on a few of my discussions with industry people, what I understand is that all of this is very dynamic and differs. What you are saying was correct about a year back or so esp in Orissa. The right to match bid is perhaps available for captive mines. Also in many cases where very high bidding happened, people have not honored and given back the mine.

This is the reason why iron ore mining cos are putting forward capacities…this is the reason why Sandur is investing 2k Cr and will build forward steel capacity to make DI pipe. Once there is a forward integration, these bidding premiums can be absorbed…a merchant miner can’t bid aggressively. I agree with your assessment that mine has become an important resource and hence I have been positive on both Sandur and GPIL.

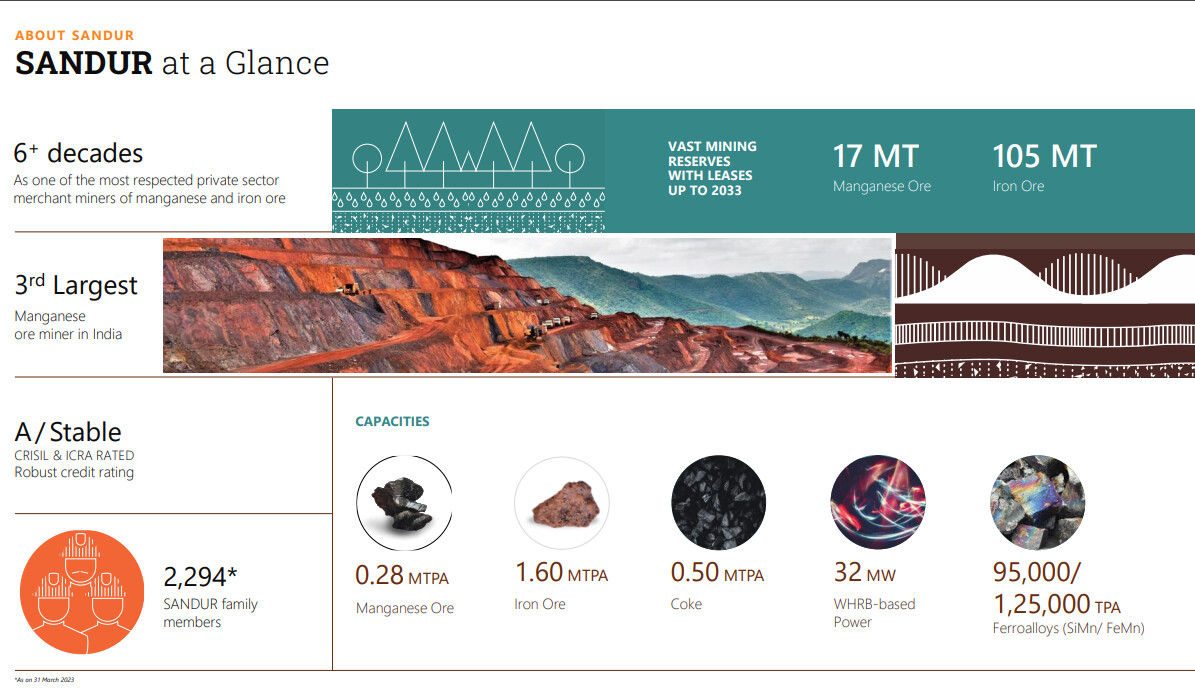

Regarding the question of growth in sandur other than mining - yes, they are expanding in other segments. Have a look at their presentation, lots of details are available. Based on the current expansion plans, they should be over 5000 Cr turnover co within 5 years and I think in past the management shared their aim towards a billion dollar number.

Yes, they can reach 5000 crore turnover.

However, GPIL has mining license till 2055+. That’s a very big+ over sandur.

Sandur business plans and future turnover pales in comparison to GPIL, as GPIL plans to increase mining capacity 2x in 2 yrs and 4x in 5-6 yrs, and the mining profits will last till 2055.

The iron ore prices will take-off after 2030- when the rest of big mines will have lease expiry- including Tata steel Jamshdepur mines.

Sandur will no longer have old mining rights after that, but GPIL will be the only beneficiary in the entire listed space to have mining lease at old prices till 2055+

The Sandur family has a past decades history of Political ties with Congress. There is also lot of parochial sentiment towards local industries. No way Sandur will be divested of mines if matching offer is given. Also one can see recent Nandini vs Amul narrative on how emotive local issues in Karnataka

Mines allocation is by central ministry, in a very transparent manner.

The mine goes to the highest bidder. There is no other way.

Even if Sandur bids at 120% premium, but JSW bids at 121% premium, the mine will go to JSW.

All companies bid at the same time- you don’t know the bid price of Tata or JSW. The highest bidder wins.

Many steel cos are politically connected. It doesn’t really matter.

Personally, I find it quite hard to form a “10-year picture”, at least I wouldn’t in the case of Sandur. When I started buying at 700 levels, it seemed like a deep value bet trading at <1 Price to sales (most of the other valuation metrics were also close to multi-year lows; it still looks cheap to be honest). The biggest overhang was that of the Mining Expansion approvals, which have been cleared now.

I think it’s fine if we get the picture “roughly right” - with Sandur’s expansion in the mining segment, approvals in place, DI pipes capex with the strategic thinking of getting preference when the mines are up for re-auction, cheap valuations- things look mostly good in the coming 1-2 years given that the management executes well and there are no major screw-ups in the macros

In Q4, it was good to see that the management was able to sell a lot of the pending inventory from FY23, which makes the overall FY23 numbers look decent (not comparable to FY22 due to abnormal margins, but maybe this could be the new base). Additionally, any positive surprise in iron ore prices or that in other segments (ferroalloys, coke, etc.) could be a positive surprise.

As pointed out by Ayush bhai, the scale up in mining segment (~3x in case of iron ore, slightly <2x in case of manganese ore) will add significantly to the bottom line since the PBT margins are >40%

Another interesting thing from this quarter’s investor ppt was that Sandur has partnered to set up a hybrid renewable power plant for ~43MW for its ferroalloys segment (attaching the relevant snippet below)

Had prepared a short note on Sandur a couple of months ago, attaching it here since it might be helpful (has data till Q3 FY23) Sandur Manganese Note_vF.pdf (132.1 KB)

Disc: 10% allocation at cost, holding, probably biased. Please do your own due diligence

The key point is in mining companies- the key profits are from the mines.

But, these mines are not owned by these companies- unlike other sectors.

These mines are on lease- once the lease is over- the mines are gone.

So, the lease expiry metric is a very important metric. One can’t take current year or next year profits and project it forward. Once the lease expires- those profits will go to zero.

I agree this is a unique case but this is what Corporate Finance is all about.

Consider this that you’ve to bid for a mine for the next 10 years, how you do that is you estimate the cashflows from the Iron Ore segment for the next 10 years and discount them at a viable IRR. For Sandur I choose to do this at 15% - 3 MTPA Iron Ore Capacity and 0.28 Mn Ore Capcity. Choose a starting rate, inflate it at rate of Inflation and choose the avg margins for the next 10 years.

I agree this doesn’t give you the best picture but its still better than having nothing and maybe missing out on a good opportunity. Cash flows is what matters, you want to be conservative choose a low starting realisation for the Minerals.

I add the remaining businesses to this value at book value cost because there is a lot of uncertainty in those biz at this point of time.

For me Sandur is starting to look attractive, I’ll start to accumulate below 1150.

The way I see Sandur, the Govt has given it 10 years to grow up & join the big boys. During this period, the Co. sets up forward integrated value added projects, pretty much as a Govt. largesse with these super normal mining profits, which some could say belong to the Govt. as it owns the mines.

It is the shareholders who have the comfort of deciding just how long they want to enjoy this ride!