Sandur does have some near term triggers but there is question about lease mining expiring in next 10 years but I also read it somewhere that at the time of renewal, preference is given to the player who has captive consumption.

On the other hand, GPIL has lease till 2060. Moreover, GPIL is more into value added products as compared to Sandur, plus the quality of iron ore in case of GPIL is better than Sandur and hence GPIL enjoys premium over other ore. But the issue with GPIL is, whatever CAPEX they are currently doing is not going to move their top-line (most of the CAPEX is towards captive sourcing of power). In fact management has themselves called out that they are not expecting any significant top-line growth for next couple of years. As per my understanding GPIL story will become interesting if they announce some CAPEX which will be positive for topline as well.

I have prepared my notes on Sandur & GPIL. Sharing those notes here

24 iron ore mines had lease expiry- all of them were auctioned in open market.

This was during 1st/2nd wave of covid.

The mines have been going to highest bidder so far.

There is no preference to anyone- govt has removed the distinction between captive miner and merchant miner.

All miners are allowed to sell iron ore in open market- this is a new clause added recently.

There is no difference between captive and merchant mine anymore- as per the link above.

The mines belong to people of India- it is a national resource.

Sandur doesn’t own any mine, we have given it to Sandur only for a certain period of time.

The govt has made mine auction- very fair and transparent- for everyone’s benefit. No preference is given to anyone.

And, GPIL is doubling mining and pellet capacity in 2/2.5 yrs- very significant increase in both topline and bottomline.

Thank for sharing the details on how mines are auction. About GPIL, as per IP:

Iron Ore capacity expansion:-

EC approval is expected in Q2/Q3 FY24.

Once approval is received it will take 18 months to expand the capacities, that is by Q1/Q2 of FY26.

Pallets Expansion:

Groundwork expected to start in Q3/Q4 FY24.

It will take 24 months to complete the capex. Thus commercialization is expected in Q4 FY26.

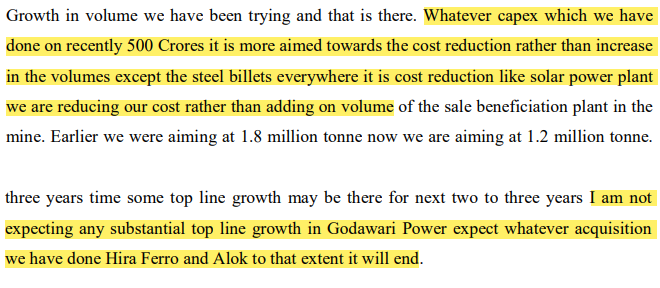

So major capacity is getting expanded in FY26, considering that everything goes as per the plan. But till then whatever CAPEXes that the company has done recently or is doing currently are towards cost reduction.

For such companies, I usually like to keep them on radar and see how plans are getting executed. If they are moving as per the plan and once there is more certainty, I usually take bet. I follow this approach because I have burnt my fingers by betting on the companies where they had a huge expansion plans but failed in execution or faced the challenges in selling their products after expanding their capacities.

Any source that talks about foray into TMT ? Have not come across any recent commentary from the management that talks about entry into TMT.

On TMT- my 2 cents having seen the steel industry very closely

a) It is not a very complex plant/business to manufacture TMT

b) In terms of pricing power- brands usually get a premium but the base price is set by demand and supply ( essentially nobody has a say)

Company sells Iron ore, Manganese ore, Ferro Alloys and Coke. Main decline is in sales of coke due to high fluctuation in price of coking coal, the basic raw material. Coke is highly volatile business and realisations can wary significantly depending upon price of coking coal. sandur results.pdf (709.6 KB)

While QOQ the result looks very bad, with this industry one has to compare YoY (along with other factors):

Ferro alloys are going through a major slump as GPIL itself mentioned.

Coking and thermal coal prices are spiraling down

Earnings driver for Sandur is majorly going to come from how they deliver with the expanded mining capacity, with their mining licenses due for expiry within 7 years (in 2030).

Once 2030 comes they have to participate in the auction and bid for any renewal and it’s pretty sure with the 2020 mining auction rule changes, the royalty and other terms will be drastically non-remunerative compared to their current mining license.

Also, would like to point out a red-flag on corporate governance.

When they did rights issue at Rs. 10, they increased their own shareholding by 1% at zero cost (as many minority shareholders didn’t subscribe to rights issue- as many retail are passive investors/busy in their jobs).

Ideally, such rights issues should not be allowed.

However, would you have faith in such management?

What was the purpose of rights issue at Rs. 10- can someone please explain??

The rights issue was issued @ Rs 10 per share and non participation by passive investors should not be attributed to promoters as they have sufficiently published the Rights issue info in Business newspapers and sent to all individuals thru Emails.You are making a sweeping statement that Rights issue at cheaper prices should not be allowed , which by no stretch of imagination can be construed as NOT monority shareholders friendly.

Your analysis vis-a-vis mining licence changes is timely to let us know about the current position of Sandur.

why was there rights issue at Rs. 10 when share price was Rs. 3000?

why did promoter shareholding increase and retail shareholding reduce?

what was the purpose of rights issue- you can’t do rights issue just for sake of it- please explain the purpose of rights issue.

What was the purpose of rights issue at Rs. 10- can someone please explain?

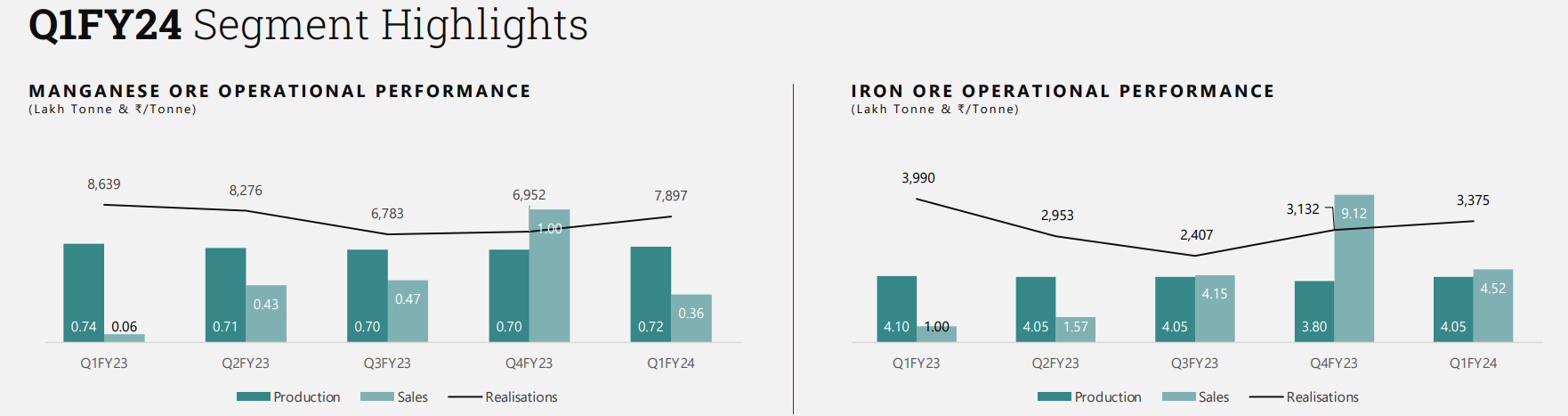

Sandur’s Q1 results have been poor, highlighting a few important excerpts from the Investor PPT below:

Mining segment

Production of both Iron Ore and Manganese Ore mostly in-line with quarterly targets, although have some reserves of Manganese Ore left (broadly both are ~25% of annual capacity, so production seems fine)

Prices of both seem to have rebounded compared to Q3 FY23 (attaching a snippet below for the realizations trend)

Expansion - Based on the remaining approvals, expect to ramp up production for Mn Ore in Sept’23 and Iron Ore in Oct’23 (this is perhaps the most important part, since their effects should be partly visible in Q3FY24 and fully in Q4FY24)

Once production ramps up, focus will shift to downstream operations - pellets and beneficiation

Ferroalloys

This has been one of the main party spoilers due to tepid demand, and while realizations have fallen 20%+ from Q1FY23, the production was quite low too. To put this into context, Sandur produced 11-15K ton each quarter in FY23 ( it has ~1.1L ton of annual capacity or ~25K quarterly capacity at 100% utilization), but only ~8K ton was produced in this quarter

Sandur commissioned the renewable energy project with Renew in Jun’23, which will help in scale up once the demand environment is more conducive

Coke

Prices have fallen ~30% compared to Q1FY23, and 10-20% compared to the previous three quarters. Again, Sandur has optimized volumes here due to lower demand and low prices

Other-

Submitted all necessary applications for listing on NSE, anticipate approval shortly

My personal opinion is that Sandur is not a QoQ or YoY story (and probably Coke and Ferroalloys are not even the most important segments), the key pointer in my thesis is the expansion in mining segment, especially Iron Ore. Just putting things into context, at current Iron Ore Prices of Rs 3.3K/ton, an incremental 2.9M ton (at 100% utilization) can add ~950cr topline with 45-55% margins i.e. 450cr+ EBITDA. The mining segment put together can add incremental 500cr+ EBITDA (even at 90% utilization), given that Sandur’s market cap is ~3300cr, it still looks lucrative.

Also, in my opinion the rights issue was not the best outcome for passive shareholders (and that has to be a key factor under ‘Risks’ in this play; maybe the Market won’t be in a hurry to give good valuations to such a business), but generally these things improve as the size of the company grows. And in no way, does this put a doubt on how good the management is (check what all they do for their employees, these guys are actually one of the good ones out there).

Edit: I’m not sure why the Rights issue took place in the first place, maybe the management considered it as opportunistic or simply wanted to make headlines - but the point is that just because it happened once, I wouldn’t jump off the story (which looks good) since it would be akin to missing forest for the trees.

Having said that, it’s upto the individual to consider these things as red flags or not.

Hi Ansh,

I still did not understand the objective of the rights issue. The amount raised was very small as issue price was Rs. 10 per share.

Other companies don’t go for such a rights issue where rights price is 98% less than main share price. So, my question remains- Why was the rights issue done in the first place?

They may be employee friendly- doesn’t automatically means- they are shareholder friendly!

Vice versa also applies- many companies may be shareholder friendly but not employee friendly.

The best example of the latter is Twitter (X) where 90% of workforce was fired and rest is made to work 120 hours a week.

PSUs and companies with PSU culture like Tata Steel- are very employee friendly but shareholder un-friendly.

Sandur has gone one step ahead and did an obvious shareholder unfriendly move of rights issue at 97% discount with no benefit for the company- but for only increasing the shareholding of promoters at expense of minority shareholders.

Personally, I will stay away from such companies no matter how cheap they are.

P.S- this is not an investment advice. I am not holding sandur shares. No trades in last 15 days. I am not SEBI registered.

Right issue give pro-rata entitlement to all shareholders holding shares on record date, so per se can not be negative minority shareholder in my view. If price is 4000 and right issue is given at 10 (in same proprtion to holding to every shareholding) the ultimate share pattern remained unchanged. It is like Bonus issue which is issue at nil cost to all shareholder pro-rata.

Further, the minority shareholder who do npt have cash/or find inconveniet to subscribe in right, can sell their entitlement in stock market, which are priced normally at differences of current market price less right issue price adjusted with discount factor. So every shareholder (inclduing minority shareholder) has option to benefit from pro-rata allotment in rights.

Coming to last pointsl about increase in promoter stake, there would some shareolder who did not subscribed to right nor did sale their entitlement. In such case, board is authorised to allocate shares to other member in oversubscription ratio in pro-rata basis. So the increase in shareholding by promoter has not directly resulted as loss to minority shareholder. They may have right from open market (in which case kind of purchase at near market price) or got pro-rata allocation for their higher subscription, at same basis, as other shareholder who over-subscribed. You can ot blame managment for non-action of minority shareholder and increasing capital at lower price, at least, in this case in my view.

Discl: No investment in company. Not SEBI registered advisor. Not recommending any investment action.

The company utilised money raised in right issue as in equity contribution in a subsidiary which intends to set up green power capacity. Most likely the power from same would be used by the company in its operations. This is my understanding and it may be wrong.