One can go to their bank website and apply for the rights through the IPO/Rights issue section. For HDFC its available through Request → IPO/Rights Issue and follow the process and one lands on the following screen

1 Like

Hi,

You could download file from following link for ICICI bank -

Based on your city and area you could visit the branch and submit the form. (not all branches accept the form)

These all instructions are given in application letter sent by Company.

PS: Bhai, if you want to be successful investor, first step is to develop attentive reading habits.

All the Best.

Thanks.

All members are requested to post their basic questions in the appropriate threads. Cluttering the company’s thread is not encouraged.

8 Likes

Announcement under Regulation 30 of SEBI (LODR) Regulations, 2015- Allotment of Equity Shares on Rights Basis

1 Like

Are the shares credited in demat account or any mail communication which has been sent? i have neither received a mail or shares credited in demat?

please enlighten.

Did anyone attend the Sandur AGM?

Any notes from the same would be highly appreciated.

Thanks

Chairman speech is available here - https://www.bseindia.com/xml-data/corpfiling/AttachLive/da479fe1-2d6b-47c0-a521-f628a91c4e9b.pdf

Disc: Invested in family and client acs

16 Likes

Thanks so a ton!

Did anyone ask or did they speak about profitability / margins in Q2 or FY23 full year guidance?

Also, so much talk and focus on expansion makes me tense. I was sure Coke oven is an absolutely good investment. Not sure about DI pipe

There was no discussion/comment on forward-looking nos or guidance.

1 Like

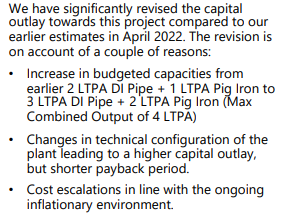

Hi @ayushmit Sandur Manganese has mentioned in a press release that the cost of the DI and Pig Iron Plant has been raised to 2200 cr < combined capacity of 0.4 Million Tons> Any idea why the cost for the plant is so high?

1 Like

Seems like the management has also increased the scope (reproduced in the snippet below), but @ayushmit might be able to share more regarding the cost

Also, 3L TPA DI Pipe might be able to generate 1500-1800cr (50-60k/ton) and 1L TPA Pig Iron might be able to generate 200-300cr (20-30k/ton), given that max combined output is 4L TPA.

For Asset Turn ~1 and ~15% margins, is this a good enough investment?

(Please let me know in case I’m missing anything)

(https://www.bseindia.com/xml-data/corpfiling/AttachHis/aaf3b79c-db62-4377-a0d1-88f1b998fe20.pdf)

6 Likes

Public hearing for Iron ore capacity expansion & benefication plant was completed on 6th Dec, 2022. Proceeding notes from this hearing are now available -

public_hearing_proceedings.pdf (2.5 MB)

Proceedings have very positive testimonials and feedback for Sandur from nearby villagers. All of the testimonials were positive and were in support of the proposal.

Post public hearing, EAC meeting for EC approval was conducted on 17th Jan, 2023. Outcome of the meeting is awaited.

http://environmentclearance.nic.in/DownloadPfdFile.aspx?FileName=mmzGIsGicihafJQG8L3gXthy4tWVwaEJriuDoJT0fwxBTBkcQ0Gs8eCwNhZcOkP9&FilePath=93ZZBm8LWEXfg+HAlQix2fE2t8z/pgnoBhDlYdZCxzUI4D0y0DyH4SbeEYqwvEmbhEpifn7pul6jbKN/D/SJcuZyZWy9WjwNwnz9sEg5AQE=

Outcome of the EAC meetings are generally available in couple of weeks from the meeting date. If the outcome is positive with committee recommending instant EC approval, it generally takes couple of weeks (post meeting outcome) for EC approval to arrive. If this goes well, we might see FY24 with higher volumes along with better iron ore grade.

17 Likes

Good work Tarang (@tpatel) in finding the Proceedings of the Environmental Public Hearing (EPH). Very positive. Pleasure to read views/ opinions/ objections/ suggestions of the public gathered in the Dec 6, 2022 meeting.

The ~3x iron ore capacity expansion and beneficiation plant proposal was considered by the EAC in Jan 17-18, 2023 meeting. The minutes of the meeting (MoM) is available here. The MoM has the long and much awaited green signal for EC grant.

17 Likes

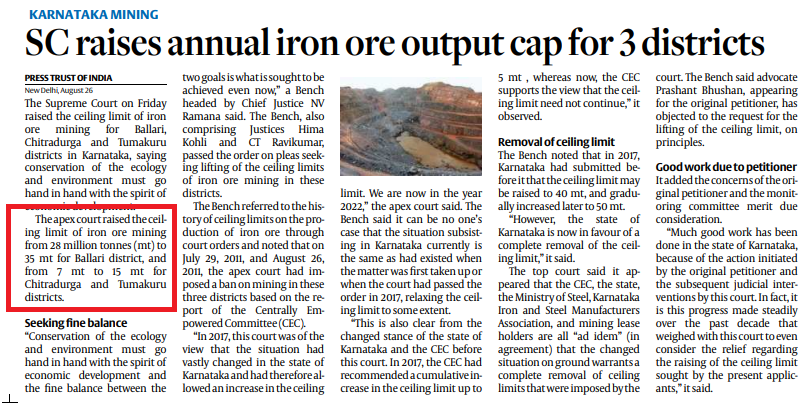

How come the EC is valid only for - year till 31 Dec 23

Sir it is 2033 not 2023.

2 Likes

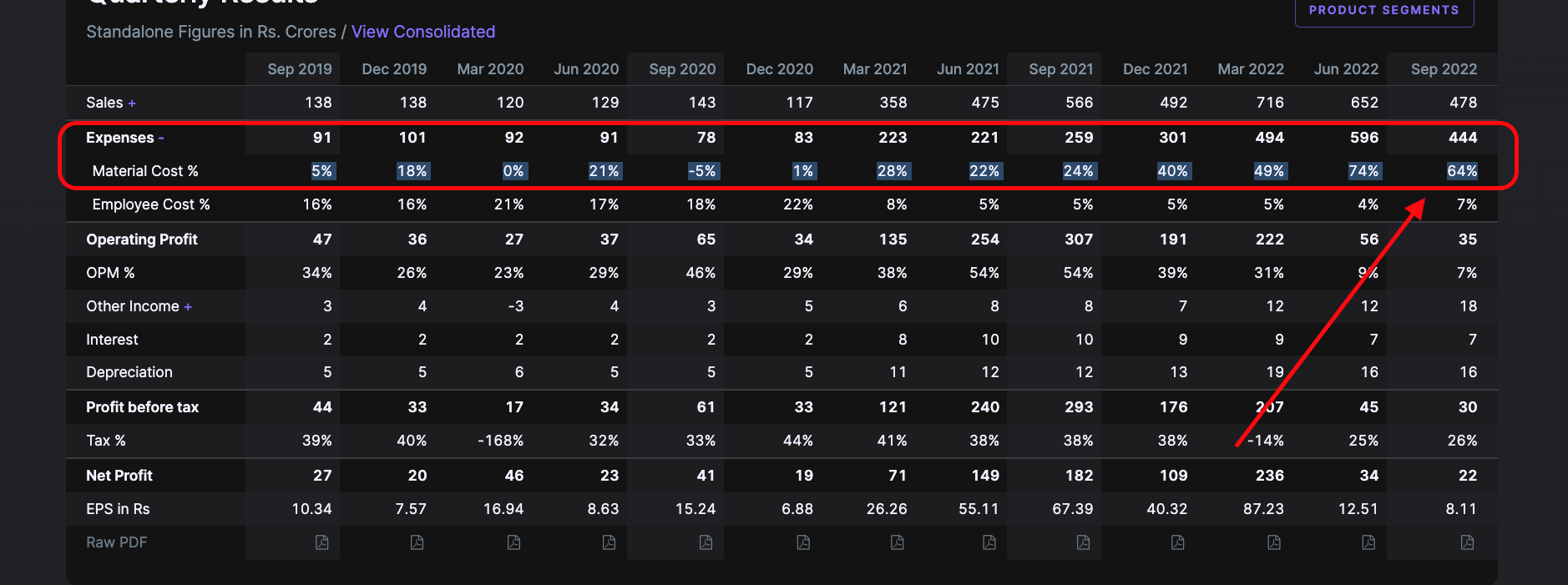

Can some kind soul explain to me what is causing such increase in material cost ?Any site to track the material price every month will be of immense help.

Link to below pic : Sandur Manganese & Iron Ores Ltd financial results and price chart - Screener

Technicals look favourable at this juncture, however its not clear if the material costs will cool off.

From Filings and Investor Presentation at Coffee On Manganese Ore

Filings

Hon’ble Supreme Court of India, has granted approval today, for enhancing the Company’s Mn Ore production from 2.86 lakh tonnes to 5.82 lakh tonnes (5.50 lakh tonnes in Mining Lease No.2678 and 0.32 lakh tonnes in Mining Lease No.2679)

Recent Realization Per Ton from Investor Presentation

₹ 6783/- per ton. Page 15

8 Likes

Steelmint’s team visited Sandur’s mines last month. The mines look quite well maintained. They have shared a few pictures on twitter-

https://twitter.com/SteelMint/status/1617405571719921664

“One of the most systematic mining facilities with a current iron ore capacity of 1.6 mnt, which will be increased to 4.5 mnt”

17 Likes

Thinking about the execution risk with DI plant commissioning and stabilization: -

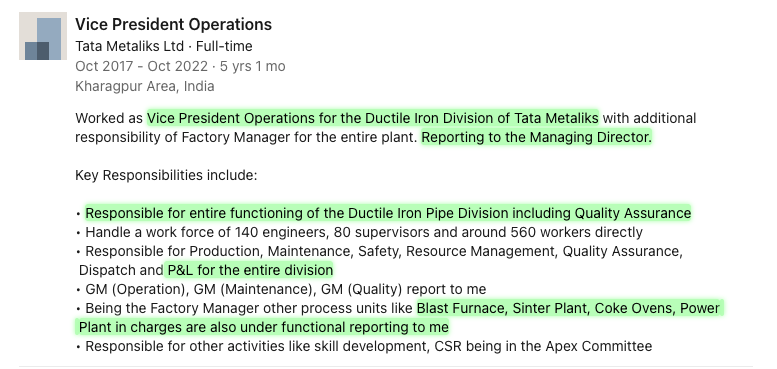

Company recently (Oct 2022) hired a Chief Operating Officer who was with Tata group since 2013 and was VP of operations of Tata Metaliks for last 5 years.

For Tata Metaliks, utilization levels of DI pipe have been 80-90% in FY22. This experience should come handy in stabilizing DI plant for Sandur.

Additionally, Tata Metaliks do not have captive iron ore and buys from Tata Steel. In FY22, Iron ore constituted ~38% of total raw material costs and ~23% of revenue for Tata Metaliks.

Tata Metaliks’ raw material purchase cost includes iron ore, coal & partly coke (~20% of coke is purchased from outside, 80% is internally produced [src - Q1FY23 concall])

Sandur’s raw material purchase would be just coking coal.

In recent TV interview, MD reaffirmed that expansion of DI plant is going as per plan and is expected to be commissioned in FY25/end of FY24.

19 Likes