Accouncements by the government might have substantial impact to the profitability of Sandur in its Iron ore and coke division. However, considering that they were already getting lesser realization for their Iron ore due to export ban (and also poor grade than NMDC’s ore), the impact on realization might be much lesser than faced by NMDC. As per the latest Q4 investor presentation - Sandur’s Iron ore realisation is around Rs. 3,268 per ton. As per GoIndiaStocks.com’s tweet, NMDC’s avg realization might drop from 6,100 per ton to 3,650 due to export duty Sandur might not see such a sharp drop but Company might have already touched its peak earnings. @ayushmit - your take on this entire situation ?

Hi,

Do you gents have an idea of earnings compressions in the coming Quarters due to Levying of this additional duty, kindly share your views on additional revenue generation which can nullify this effect .

Any calculations will greatly help. Thank you.

Hi,

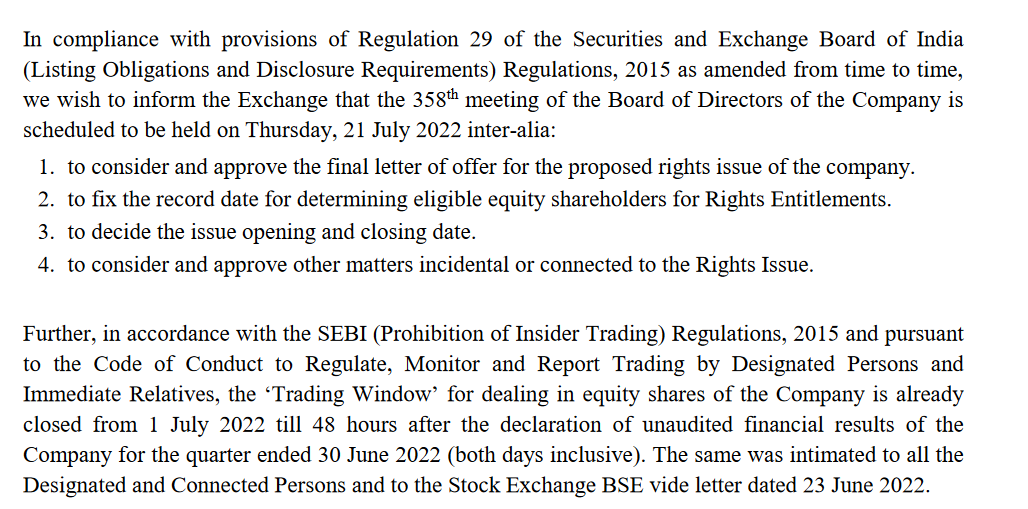

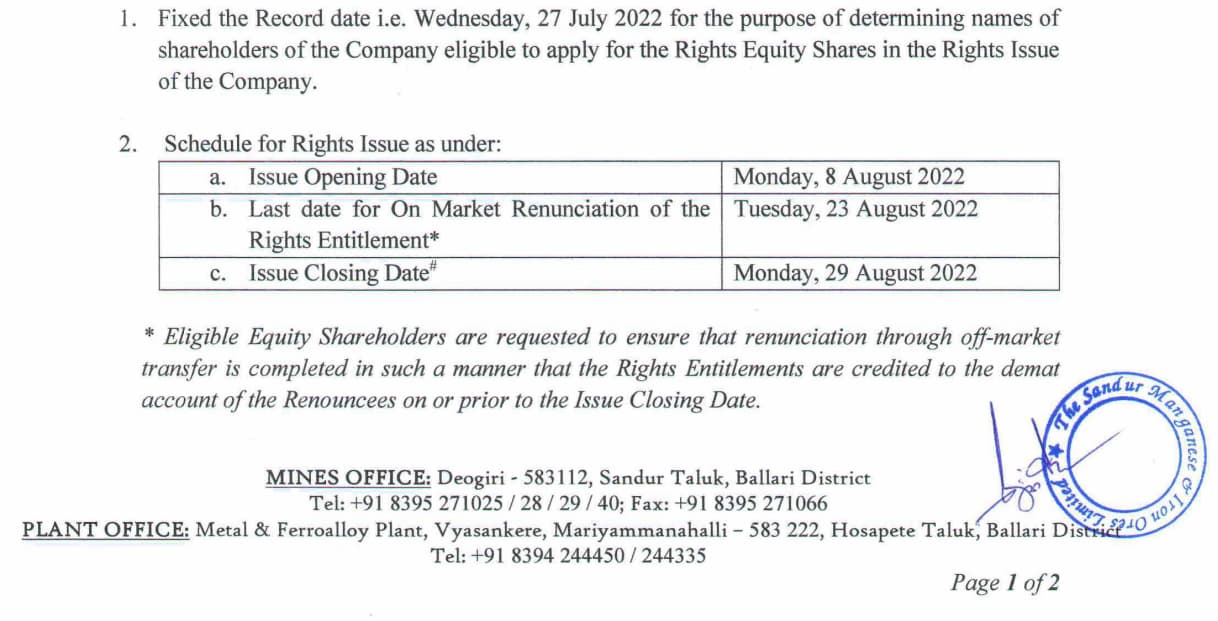

We are in the process of completing the procedural requirements for the right issue. All updates including record date will be provided in due course to the Stock Exchanges and the website.

Regards,

The Sandur Manganese & Iron Ores Limited.

‘SATYALAYA’, Door No.266 (Old No.80), Ward No.1,

Behind Taluk Office, Sandur - 583 119

Tel: +91 8395 260301

CIN: L85110KA1954PLC000759

Hi Syed,

There has been two major annoucement back to back that has a direct impact on iron ore pricing. One is relaxation from SC for Karnataka Miners on sale of ores without e-auction and other is the export duty.

Best way to get a direction on pricing for mining products of SMIORE is following pricing declared by NMDC (for Iron Ore), MOIL (for Manganese Ore). In last 4 quarters, avg premium of pricing for NMDC ore is around 158% to Sandur Iron ore prices. Going by this, I could arrive a figure of 2788 per ton for Q4 for Sandur Iron ore. However, its not that simple, since relaxation on selling of ores in Karnataka will lead to better price realization than in past but this is to be seen in light of fresh export duty as well.

Sharing my notes on one part of the thesis which is the DI pipes where Sandur is planning to set up a 2L MTPA plant to be further ramped up to 3L MTPA in the second phase. This is potentially a 1.5k crores in revenue business line when ramped up at full capacity generating EBITDA of about 300 crores with arguably lesser cyclicality. Although this could be a difficult business to scale up for Sandur, which is a new entrant, the industry dynamics are interesting.

Electrosteel castings AR notes:

Industry Outlook:

Water to common people is now getting very high priority from the present Government, the policy makers and the media. The rising concern about future availability of fresh water as well as the deterioration in drinking water quality had prompted the Government of India to already initiate a massive programme termed as “Nal Se Jal” and access to drinking water for all is now a declared priority. As declared by the Prime Minister, an amount of Rs. 3.5 lakh crores will be spent in coming 5 years to achieve this target. The Jal Shakti Ministry has set a target of “Har Ghar Nal se Jal” by 2024 under the Jal Jeevan Mission. The Government is planning an aggressive target of providing piped water to all households by 2024.

This indeed is a massive challenge given the sheer numbers involved – 150mn households across 0.5mn+ villages will have to be brought under the scheme over the next five years. Considering above aspects, time bound completion of schemes is being monitored by Jal Shakti Ministry to achieve the goal of providing tap connection to every rural household. Significant priority to cover water quality affected habitations is also taken up under Jal Jeevan Mission. Apart from the above, the State Governments’ spending on water is expected to increase to fulfill the mission. At the same time, the world demand for DI Pipes are also gradually looking up after the pandemic.

DI Pipe in view of its inherent features, like, high mechanical strength, better pressure bearing ability, higher corrosion & abrasion resistance, easy laying and long service life, is the preferred choice over other types of pipes for water and sewerage transportation.

Notes from credit rating reports:

Leading Industry Player: With the amalgamation of Electrosteel castings and Srikalahasthi Pipes, the combined entity now has a presence in the east and south regions of India with five manufacturing locations across India. The total ductile iron (DI) pipe capacity has increased by 125% to 720,000 metric tonnes per annum (mtpa) by FYE22 (ECL – 320,000mtpa; SPL – 400,000mtpa since August 2021), commanding around 32% at FYE21 of the total market share in terms of operational installed capacity, making ECL India’s single-largest player in the DI pipe segment (existing market share - ECL: 14%; SPL: 18%) and leading to significant economies of scale along with cost efficiency due to operational synergies. While the combined entity does not have captive raw material sources for iron ore and coal, the combined captive power plants (41.5 megawatt) cater to 50% of the overall power requirement. Overall, the combined DI pipe capacities operated at 85% utilisation in 9MFY22 (FY21: 81%; FY20: 104%) with the production volumes impacted in 1QFY22 and FY21 due to COVID-19 led disruptions. The combined entity’s revenue fell 9.8% yoy to INR37,387 million in FY21, as the pandemic led to lower sales realisations.

Post the amalgamation, ECL is likely to increase its volumes in the high-margin export markets as its plants are located near the ports and ECL has all the required approvals in place, while catering to the domestic markets via the growth in SPL’s capacity to 500,000mtpa by 1QFY24. In the domestic markets, ECL has a strong presence in the east and north regions of the country, which account for almost 50% of the overall revenue. Meanwhile, SPL has a strong foothold in the south and west regions which commands 80-85% of its revenue. Thus, the combined entity would have a pan-India presence post the amalgamation.

Healthy Order Book: The combined entity’s order book remained healthy around 0.365 million tonnes (mt) (18% export orders) at end-January 2022, with revenue visibility for the next six-to-seven months. The orders are largely fixed-price in nature and have an exposure to the water departments of the respective states and engineering procurement and construction players. Furthermore, DI pipes remain under the higher focus areas of the state and central governments and thus are part of the critical infrastructure spending. The central government’s Nal se Jal scheme under the Jal Jeevan Mission provides further visibility on the order book and top line for DI pipe players over FY22-FY24.

Notes from concalls:

The management wants to focus on the exports market as well. They are able to do a blended EBITDA per tonne of 10-11k per tonne. The EBITDA per tonne is higher in the exports market by about 3k per tonne.

In last 15 years there has been capacity addition Tata Metaliks came into picture, Jindal Saw also came into picture in the last 15 years and the capacity enhancement had started happening in last three, four years and last three, four or five years where Kalahasthi had also increased the capacity, Tata Metaliks is also increasing the capacity, Kalahasthi is again increasing the capacity. It is all because there is lot of demand the government push to supply of drinking water to each and every household this creates lot of demand for the DI pipes and DI pipes is one of the most suitable pipe for transportation of water because of its characteristics. So, the expansions and the capacity coming up we do not see any concern in fact it is good for the market and I think and this is also not a fragmented industry there are very limited and renowned players. So, I mean we appreciate this expansion happening.

Sustainability of demand once Nal se jal is fully implemented then what happens to these capacities I mean can the industry absorb incremental capacity of let us say another million ton on a sustainable basis going forward in fact that is what I was trying to understand and how big is this opportunity going forward?

Water is very important for each and everyone. Now you are seeing cities not only in India but everywhere all over the world. So, the market is growing and you will see both I mean in Electrosteel both the units have been increasing the capacities gradually. Whenever we do the capacity increase our production is fully sold there is no question of not selling and the capacity utilization is 100%. So, we do not foresee any gap between production and sales. See a sustainable demand going north of 2 million tons at a country level.

So, most of the orders or per se the entire order has come from government bodies only. Ultimately the buyers of the DI pipes are government bodies so they come out with tenders and either they procure the pipes directly or they do it through the EPC contractors. So, for us the end customers are government bodies only. In terms of margins when the competition comes in see the competition is already there it is just that the capacity is going up slightly maybe by around 10%, 15%. Right now we have a industry capacity of around 2.5 million tons which is expected to go to around 3 million tons and there is ample demand for pipes. So, we do not see any concern on the EBITDA because this is the kind of minimum EBITDA which every player needs to maintain.

I would like to add only one thing to what Mr. Gaurav said the usage of the DI pipe which was hitherto for water and sewage is not extend to even irrigation. So, whatever irrigation projects that are coming up also DI pipes will be used. So, that allocation will come. Now realizing that the water is very important the central government has started a separate department ‘Nal Se Jal’ and the supply of water from the source to the household which initially started in the state of Telangana is now extended to Orissa and is being extended to Andhra, Tamil Nadu like that every state will be doing this. So, we do not foresee any dearth for order of or demand for such a line pipe.

From credit rating reports of Tata Metaliks on industry landscape:

Favourable medium-term demand outlook for DIP in India following Government’s emphasis on ensuring tap water connection for all – The demand outlook for DIP remains favourable over the medium term, given the Government’s focus on ensuring potable drinking water security to every rural household by 2024 under the flagship Jal Jeevan Mission. Around 50% of the households have been covered under this programme till date, so the Central Government’s allocation to this programme has increased by a healthy 33% in FY2023. ICRA expects the funding to remain strong in FY2024 as well. Notwithstanding the new capacity coming in the industry in the current fiscal, ICRA expects the demand-supply dynamics to be evenly balanced over the medium term at least, given the healthy industry order book position and favourable outlook.

Competitively bid fixed-price orders result in range-bound profitability in the DIP division – The major portion of DIP’s sales takes place through tenders, where the lowest bidder is awarded the contract. This results in significant price-based competition, which keeps the profitability under check. Moreover, a rise in input cost adversely impacts the margins of the DIP business due to the fixed-price nature of the contracts. However, healthy medium-term demand outlook is expected to keep the capacity utilisation of the players at a healthy level.

Commentary from Tata Metaliks management on the overall industry landscape:

Q3 FY22

Order load for DI pipe industry -1.3mnt and new inquiries is 1.3mnt i.e. firm demand is 2.6mnt and other projects which has been sanctioned but the demand is not announced yet is 2.2mnt of demand. This takes the total demand to 4.8mnt for the next 2years. Installed capacity of industry is 2.2mnt at 80-85% capacity per year translating into a supply of 4.4mnt for two years. So there is a deficit in supply of 0.4mnt which has led to a 40% rise in prices. The management expects DI pipe demand growth of double digits (10- 12%) over next 5-7years.

DI pipe new contract prices have moved up by 40-45% as compared to prices in last year due to the deficit market scenario. Prices are now at Rs70,000-75,000/tonne – landed cost which was Rs50,000/tonne last year.

TML aspires to be a 1mnt DI pipe player in the longer term. DI pipe business is tough to be mastered by new entrants as there are high entry barriers both on the technical and market side.

Q1 FY22

New capacity addition in industry: Srikalahasthi pipes and Tata Metaliks will add 400ktpa over 2years, Sathavanah Ispat plant has been brought by JC Flower which has a capacity of 200ktpa. New players like Welspun and KIOCL will take at least 2-3years to scale up capacity as it is a difficult business to build up.

This demand supply gap for DI pipe is expected to move the prices up. New contract prices have moved upward of Rs60,000/tonne vs Rs50,000/tonne for already booked orders in last year. This new prices will get reflected after 2 quarters. Management expects new DI pipe pricing (+30% hike) will be gradually accepted by government as there are no other options due to few players expanding capacity and it has high entry barriers for new entrants.

EBITDA margins for DI pipe have risen to 30% but have been at 20% mark on historical

average. (To be noted that Tata Metaliks is not backward integrated on captive iron ore and coke, while Sandur is - so realistically the margins should be higher for Sandur)

Disc: Invested.

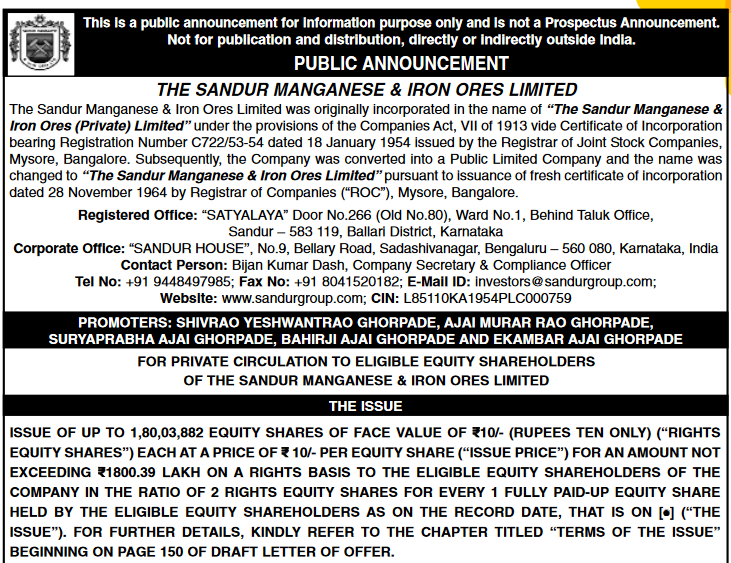

Is there a Special Situation Here??

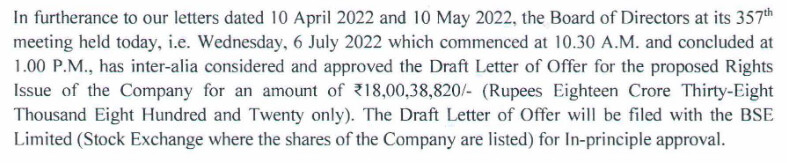

Sandur Manganese Record date for Rights is 27th July.

Which means if i buy shares tomorrow, Shares will get credited to my demat by 26th( T+2), I will be entitled for Rights… And as the record date is 27th July, If i sell the shares on 28th of July, as per the record date, still i will be entitled for Rights? because as on record date i was holding the shares.

RE will get credited to accounts before Issue Opening Date, and It will start trading on 8th August…

For Each 1 Share held, one will get 2 Shares of Sandur…

Sandur Stock Price has to adjust itself to 1/3rd… and RE to Trade around 800-1000??

As one has already sold stock on 28th July maybe around 2800-3400… He would be able to take back the Invested capital and then later sell rights issue at premium around 800-1000 which he has just paid 10Rs per share…

So all in all a opportunity to make 40-50% Gains in Short Term???

Is my reading right here???

Any Special Situation Experts who can validate this?? Is my reading Right??

Disc- I was in sandur Journey from 500 to 3500 and completely sold all shares when rights issue was announced assuming that record date will be prior to announcement of rights in april. However management has brought a record date on 27th July…

But Ex Rights Rate will it not be August 8th?, Because price adjustment on 26th Means that Marketcap will go 1/3rd. Shares get adjusted only when Equity Size Increases, but that will happen when RE will be Credited?? Am i Right?

I am no accounting student. Can someone please explain what investor has to do if they intend to keep their invested amount the same? Or will it become the same after August 8th? Currently my holding is way off from what it was couple of days ago. Is this some real loss or notional loss which will be gone once the ex date is gone.

This is NOT a loss to you. Suppose you used to own 100 shares as of yesterday at the closing price of INR 3300. Today is the first day the shares are trading without the rights benefits. Since the number of shares would be 3x after the rights issue, the price today became 1/3rd (market cap should be same as of yesterday). Hence you see the price today of INR 1100-1200.

Within a week or two, you would get 200 “Rights Entitlements” in your demat (2 for every share you used to own). The price of each would be - (Market Price of the ordinary shares - 10). 10 is the rights issue price. You could sell the rights entitlement in the open market or as you stated, if you wish to keep your invested amount same then subscribe to the rights issue by paying up INR 2000 (200 rights entitlement * 10 rights issue price).

Just like an IPO, online through ASBA supported by most bank websites

Selling RE:

For selling rights entitlement one can use the demat account where its shown as Sandur-RE.

Why to sell ? if you want to exit and make money on your entitlements as RE is quoting around 800-900/share.

Subscribing to Rights issue:

I found it easy to do it via ASBA route , if you have accounts with banks link sbi, Axis etc where you apply for IPO, look for Sandur and apply like you apply for IPO. I find no option in any of the demat providers to subscribe its only there with bank sites as demat guys dont have the ASBA option.

Why to subscribe ? Company is allotting at 10/- share when it was quoting 2000+ , who wants to miss it ? either subscribe or sell the RE dont stay inactive and loose out.

Quantity :

You are eligible to apply for 2x the quantity that you hold.

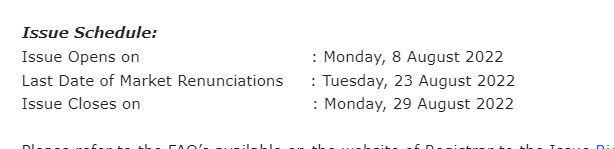

Dates:

8-aug to 29-Aug-2022.

22-Aug is RE can be sold in the market ( I read that it is 23 Aug in some other places) , and 29-Aug is closure of RE -ASBA application. Hope it helps