What kind of implications can this have?

6 Likes

As per the latest share holding pattern ended March 2022 hni investor dolly khanna hold 137608 shares in the company .It is worth 62.2 cr

2 Likes

Great to see Sandur getting the deserved attention of the big guys!

Dolly Khanna’s name appeared in latest Mar, 22 shareholding with 1.53% stake in the company.

Rights issue came well in time.

Environment Clearance for expansion is in place.

There is also a possibility of government allowing export of ore from Karnataka.

Quite a few happy events happening. Hope to see good run of the stock as well.

However, we need to keep watching the commodity prices (Iron ore, Mn ore, Coke, Coking coal etc). Recently (couple of months ago) the spread between Coking coal and Coke was squeezed erratically - which would have normalized by now, I assume.

Look forward to March 22 quarter results and management commentary.

4 Likes

Management interview (link)

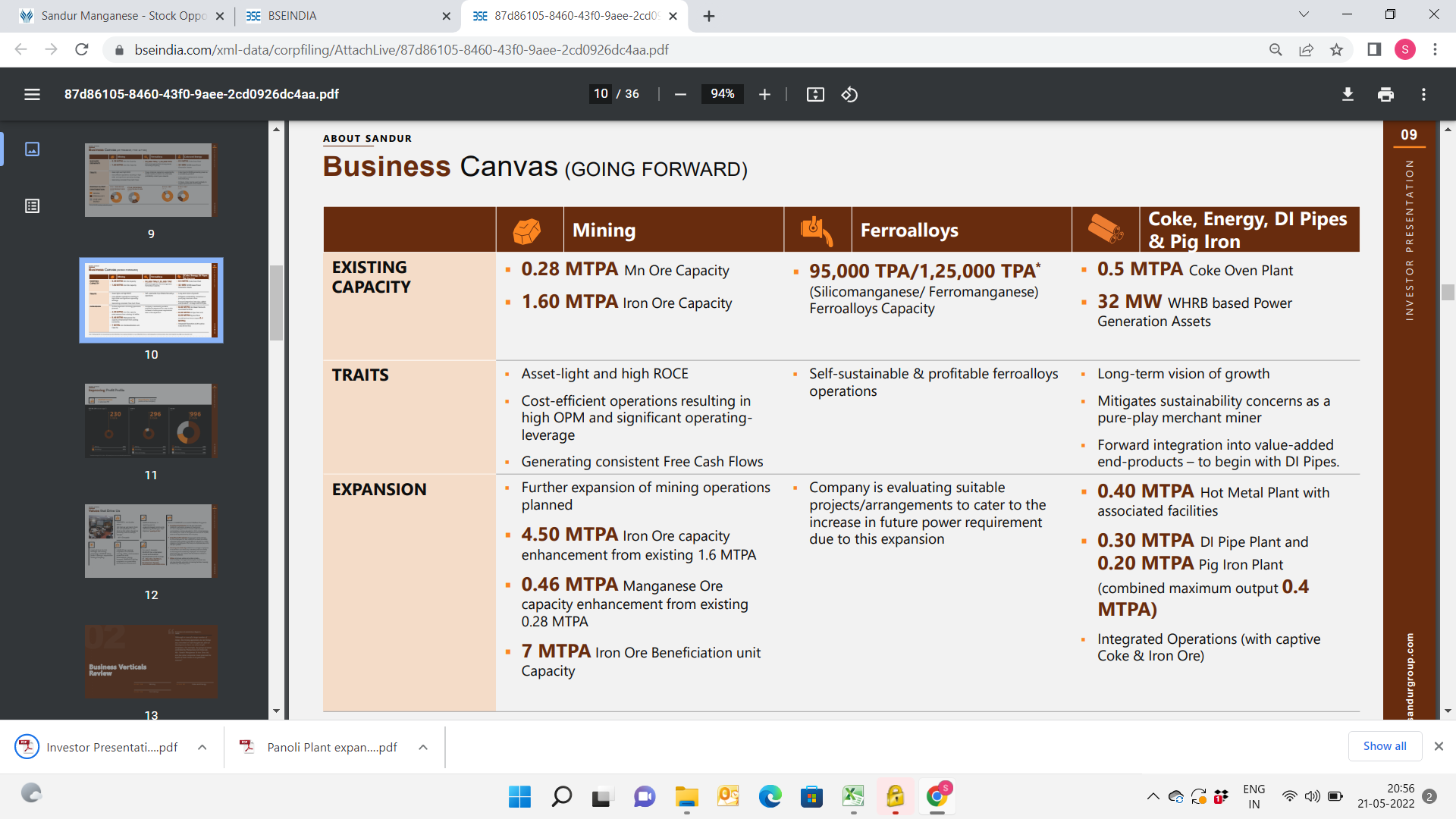

- Sandur pellets plant will be setup in next 24 months and will allow captive use of iron ore (especially when EC approval for expansion of iron ore mining comes through)

- Why was rights issue priced so low? To reward existing shareholders

- Capital allocation focus has shifted from earlier making a 1MTPA integrated steel plant to now making a DI pipe plant and increasing capacity for ferro alloy and coke oven plant (due to change in market dynamics)

Disclosure: Not invested

6 Likes

How is the face valued rights issue rewarding the shareholders, didn’t get that part?

Won’t the additional shares issued will adjust the price downwards? And the existing holders will be forced to subscribe else they will lose out due to steep adjustment in price.

Not sure what am I missing here.

In fact, from the rights issue price and CMP, this looks like a wonderful arbitrage play. Can experienced boarders\special situation investors share thr findings plz.

Disclosure :- Not invested

In my opinion, this is not shareholder accretive. There are many people who will not subscribe to this. And those share will be subscribed by promoters. So those who dont subscribe will be at a loss and promoter will gain out of it.

Correct me if I am misinterpreting something here. @ayushmit your views please.

- this can be seen as rights come bonus issue for those who subscribe the issue.

- those who wont subscribe will loose value of their holding (but who wont and why)

3.simple reason for not raising money through rights premium and using internal accruals and borrowings for expansion can be following

promoters may not be having that much liquidity to invest and so rather to borrow and invest themselves, its always better that company borrow and invest. by keeping it at Rs.10 they wont dilute their stake also.

Disc: invested since year and half

Promoter are already at 73%, can they go beyond 75% via unsubscribe right entitlement ? Even then does sebi allow beyond 75% holding

There are many people who dont track markets regularly and just keep on holding shares. those are the ones who will be at a loss. Unlike bonus, rights will not be issued automatically. So I believe that promoter would be able to increase their shareholding % without incurring any cost. Retails shareholders who dont track news and markets closely will be at a loss.

Disclaimer - Invested from lower levels.

2 Likes

Situational question: We buy at 10/Share via the rights issue and the value now 1600.

If we sell what is the capital gains on the rights issue? Seems like a complicated issue.

I read this yesterday Buying Rights Shares .

Thoughts from those experienced in these matters?

Cost of acquisition will be the purchase price of original shares only. Unlike bonus or split, the price does not get adjusted in this case for calculation of capital gain. I feel, inter-se promoter holding will undergo a change with this right issue and individual promoter shareholders will increase their shareholding.

Hi,

Kindly share your views on the below question ?

If i have 100 shares, currently the value is around 100 X 4700 = 470,000. What happens if I don’t subscribe to rights issue, will the value decrease to 100 X 1600 = 160,000.

If that’s the case, then it is unfair for the investors who are not tracking this stock because of an urgent/important commitment, personnel emergency, hospitalization etc…

Apologies, I will delete this question after sometime, if it is not appropriate for this thread.

You will get Right Entitlement(RE) shares in porportion to the number of shares u hold. And these will trade on stock exchanges for the entire rights subscription period. In this timeframe, if you want to renounce the rights u can sell these RE shares.

Now, theoretically the base price of these RE vl be the difference between mkt price pre-rights and post-rights i.e for example ur each RE vl be listed arnd 1600 arnd - the difference between ur value and marked down value. u can sell these REs to pocket ur difference.

Now the price of these REs will fluctuate as any other securities prices do - so u can get more or u can get smwat lesser price. But dat will be the risk u are carrying anyways.

To check more on this, search for RE price charts on moneycontrol for recent rights cases e.g. Shopper Stop’s RE vl come as ShoppersStop RE.

Disclosure :- Invested.

3 Likes

“But the epic scale of the challenge has automakers and battery makers working the labs and scouring the globe for materials as common as dirt, not precious as gold.”

- Is the quality of the managanese coming out of Sandur enough?

3 Likes

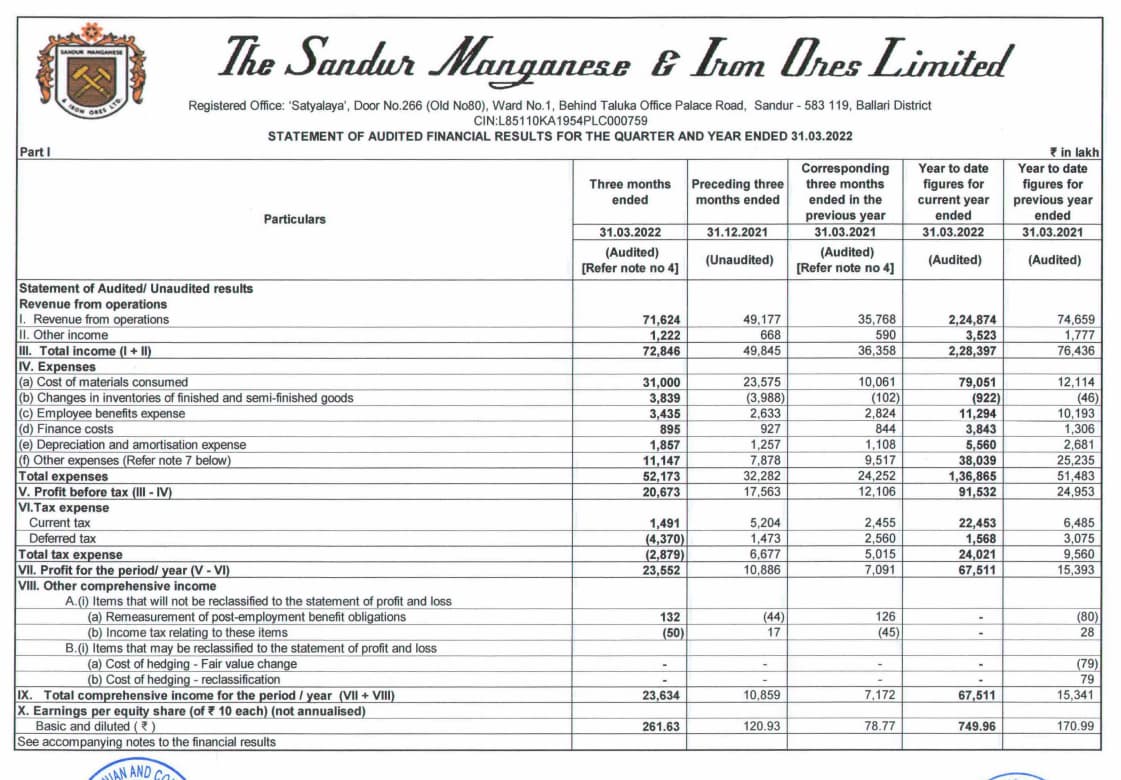

Tailing QOQ PAT Profit jumped from 109 cr to 236 cr in March 2022

Iron Ore Prices has improved PBT by Rs. 30 crores and savings in Tax due to New tax regime of Rs.37 cr adoption by the company.

Deferred Tax income seems to be reversal of deferred tax expenses created in previous period which has actualized in last quarter due to new tax regime and other aspects

3 Likes

How is the result overall?

Any idea of ore prices for Q1?

No mention of rights issue progress or expansion in notes.

Dividend is very average .

But stock is less then 5 PE.

Bumper Q4 FY22 results from Sandur Manganese.

Allround improvment in Revenue & PBT in all segments Viz. Mining, Ferro Alloys, Coke & Energy both on QoQ and YoY.

Revenue for Q4 is Rs 716 Cr as against Rs 357 Cr (YoY ) and from Rs 491.78 Cr (QoQ)

PBT increased from Rs 121 Cr to Rs 206.73 Cr (YoY) and from Rs 175.63 Cr (QoQ). This is significant increase in spite of good increase in Inventory during this Qtr when compared to corresponding Qtr (YoY & QoQ )

Dividend Declared: Rs 5/-

4 Likes

Some more fuel added to the spectacular growth that Sandur is witnessing:

Management viewpoint:

7 Likes

Volume Increase of Mining of Iron Ore and Manganese Ore will be Consistent Cash Cow in the future Year. Current year story will further improve in the coming years

It will be crucial to watch how DI and Pellet Expansion plays Out ?

Investor Presentation March 2022.pdf (3.0 MB)

1 Like