My View on Sandur Manganese (Read FY17 and FY19 annual report, based on same)

1) Excellent work environment (more as subject then labour)

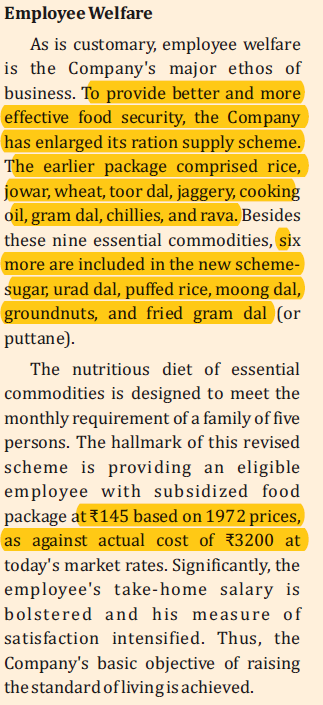

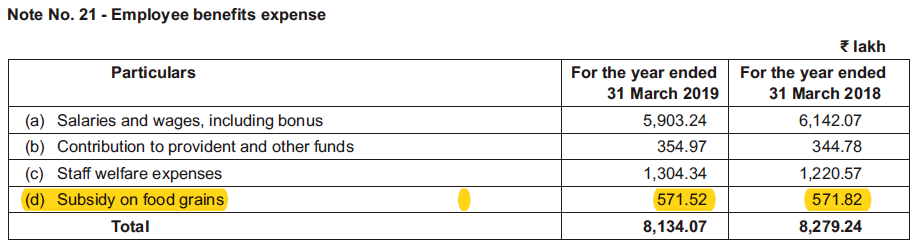

The company management has very well treated employee. The provide subsidised food to employee and never faced problem since inception as per AR. While this is good, cost of employee has large portion of subsidised food which can increase cost and reduce comepeitiveness of the company over a period.

ARFY19 Chairman speech:

Food subsidiary expenditure increased from Rs 4.78 Cr in FY16 to Rs 5.71 Cr in FY19. During same period, employee strength increased from 1879 in FY16 (1st April 2016) to 2109 in FY19 (31 Mar 2019). Average food subsidy per employee increased from Rs 25439 in FY16 to Rs 27074 in FY19 at CAGR of 2% which is lower than inflation as well.

Secondly, in FY19, the company increased six more item to sudsidised food item as per chairman speech and and higher employee strength, but despite that total Food subsidy charge declined. Need to understand exact relationship between employee and remuneration to same by the company.

2) Significant jump on Board size and higher managerial remunerations

The company has very wide group of board of directors. Some of directors are also on board of Brigade enterpise, JSW Engery and Navbharat Venture. The company has also proactively formed Risk management committee which is necessary for only Top 100 market capitalised listed company. So the company has been proactive and having good corporate governence. On Page 61 of AR FY19, the company has provided skill set and industry specialisation of board member which I have seen first time in investment journey.

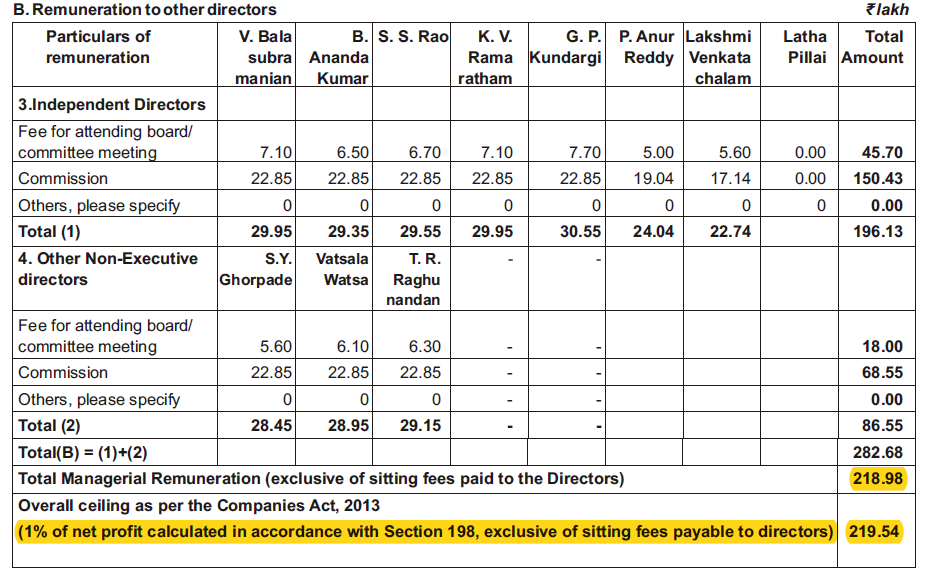

However, that has also resulted in very high charge in P&L account for the company. In fact, in FY19, the company has paid total amount of Rs 2.82 Cr (including Seating fees of Rs 0.45 Cr) as against Ceiling of Managerial remuneration of Rs 2.20 Cr. The company discloure indicate that Manangerial remuneration (excluding seating fees) is Rs 2.19 Cr which is withing Ceiling of companies Act. In my limited understanding (which may be wrong), the company has breached the ceiling of payment in managerial remuneration and need approval for Central government to regularise. Even Company Secretarial audit report is silent on same (hence there is high probability that my concern is not valid).

Also, in FY17, total seating fees paid to director was Rs 20 lakhs which has increased to Rs 63 Lakhs in FY19. Total managerial remuneration has also increased from Rs 81 Lakhs in FY17 to Rs 282 Lakhs during FY19

Further, most of time, we find increase in managerial remuneration being higher for executive director (operating person) as against Non-executive directors. However, in this company, EDs remuneration is very much in limit but NED remunderation is exceeding ceiling. We need more understanding of this.

3) Good Corporate citizen but higher financial cost

While already dealt with fair treament to employee, coming from Royal family, it has also attempted to improve quality of life in negihbourhood area. Beside providing school and other aminities (as shown in CSR), the company has contributed Rs 1.85 Cr on CSR budget in FY19 as against regulatory requirement of Rs 1.67 Cr (Page 45 pdf AR FY19). While that is not material and can be ignored, in FY19, the company has seen jump in Donations and contribution, from Rs 1.7 cr in FY18 (this is in addition to CSR) to Rs 19.7 Cr (almost 11 times) in FY19. While part of it can be explain to provide better amedities to neighbourhood and creat goodwirll, but still such large expenditure need explanation.

I believe it is not a political party donation as same need to be specifically disclosed in Annual report as per companies act.

4) Interest cost:

In FY17, the audit report says that the company is generally regular in depositing various statutory due on time. The company also had no borrowing/debt as on MArch 31 2019. However, despite above factors, We find almost Rs 7.2 Cr of Finance cost being interest on dealyed payment.

5) Delay in regulatory compliances:

FY17 Secretarial audit report has following concerns: (Page 45 PDF file AR FY17)

- Dealyed in Filing E-return with MCA

- Non-compliance in process to issue duplicate share certificate

- Delay in filing vacancy of Non executive director

- FY16 financial statement filed without auditor report and opinion (non complaince with SEBI guideline)

- Delaying in filing information to stock exchange for issue dupliate share certificiate.

FY19 Secretarial audit report has following concerns (Page 42 pdf FY19)

- Non filing of Form RE-2 under explosive rules, 2008 for April and May 2018 months

- Composition of Nomination and remuneration committee was not as per SEBI regulations (BSE imposed fine of Rs 2,17,120/-, Page 44)

- Few forms with MCA filed with delay

From the explanation provided in directors report it appear that company is not able to get right manpower to fulfill regulatory requirment. Probably, it may outcome of paying lower salary to executives (already mentioned in Point 2). CS Divya name does not even appear in top 10 employee in term of remuneration and she is not even considered as Key managerial person (hence salary is not disclosed). Same being case with CFO. CS and CFO by definination of companies act are KMP and there salary disclosure is must in audit report, but same being missing from the annual report of the company over FY17-19. I think this lapse in reporting in my understanding which shall be corrected. Having said that, not very material issue as well.

6. Financials

a) Very High Investment property :

The company has Investment property worth Rs 50 Cr as on March 31 2019. This include one residential and commerical property with estimated fair value of Rs 79 Cr as on March 2019. The company get only Rs 33 lakhs (Rent Rs 59.6 lakh- Dep Rs 26.5 lakhs) from this property which is substantially lower than Cost of capital in my opinion. The company may explore way to liqudiate same or use assets more productively. Total Property Plant Equipment as on March 31 2019 is around Rs 90 Cr (Net of Depereciation Rs 74 Cr). So almost 30% of gross block (without consider capital WIP) is blocked in investment assets.

b) Very high cash and bank Balance

The company carry very high current account balance of Rs 22.6 Cr as on March 31 2019. Total operatin revenue being Rs 702 Cr (so around 2 Cr per day), the company have 10 days sales as balance in current account which is very high. They have move same in fixed deposit and earn income.

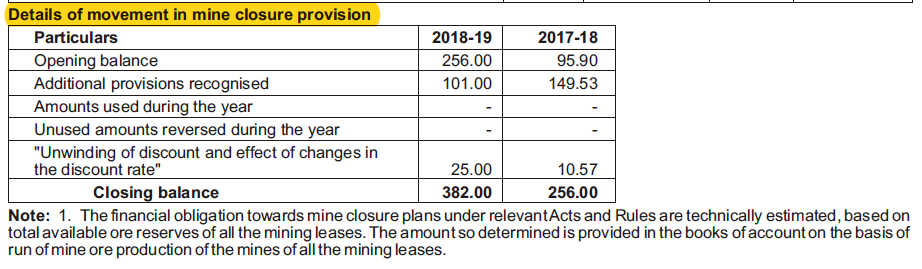

C) Mine closure provision

The company has provided for cost of mine closure basis on estimate. This is positive point as even very large mine owner like Hindustan zinc, I have not seen such provision. Once mine operations are over, there is huge cost inolved to surrender the mine back to Government (which may mean to minimise environment impact and also uliise waste dug generated from ore extraction. It is very high cost element in global market in my limited understanding). This is first company I have seen which provided for mine closure which is very positive in my view.

I was not able to go through new project of 1 mn tpa capacity expansion. The company has tied up fund of Rs 470 Cr with Banks as per note. There was no loan outstanding as per March 31 2019 financials.

Summary: While there are some complinace related issues, the company having board committee evaluating Environment (Reclamation and rehabilitation plan implemnetation committee since 2012), Risk Management committee, environment concern surrendering land for forest, 3 years 5 Star rating, Care for all stakeholder including employees, disclosure of analyst meet QA to stock exchange), I form overall very positive view for the management. In my personal scale of ability and willing (Credit analyst evaluate credit in ability to pay and willing to pay of maangement, I modify same as ability to perform and willingness to share with stakholder for equity investment), I find company willingness to treat stakeholder fairly exceptionally great . On ability to perform, they have managed in past mine well (but cost may be higher due to ESG concern), one need to see how management perform on new project implementation on time and without cost over run. The project is very large to scale of operation and hence they may need new team and skill-set.

Disclosure: No investment, My view may be biased, have limited understanding of steel sector, not sebi registered advisor.

@ayushmit @dd1474 @ashwinidamani

Can you please share your views on the amalgamation scheme?

Scheme of amalgamation dated 9 Mar 2020

Fixing of record date to 30 Mar 2020

My understanding:

Transferee company is Sandur- business of mining iron ore, manganese ores. No of paid up shares- 0.87cr, 10rs each. Current liabilities- 154cr, current assets- 230cr.

Transferor company is Star Metallics- business of setting up/operating power from various sources. No of paid up shares- 9.33cr, 10rs each. Liabilities- 3.8cr, current assets 31cr

Scheme- To receive 1 share of Sandur for every 72 shares of Star Metallics. This means 9.33cr sh of Star Metallics to become 9.33cr/72= 0.13cr shares of Sandur. Thus 0.87cr existing shares of SM to dilute to 1cr shares, right?

Benefits- SM seeks to have captive use of Mn ore in the existing ferroalloy plant of Star Metallics and setup a 1 MTPA steel plant in its vicinity for the captive consumption of iron ore as well. After the setting up of steel plant, it’ll become eligible to participate in mine auctions.

Disclosure: invested.

Very helpful table.

Is there any reason you have taken standalone statements for cash flow conversion calculation rather than consolidated? The difference is nominal but wanted to know for my understanding.

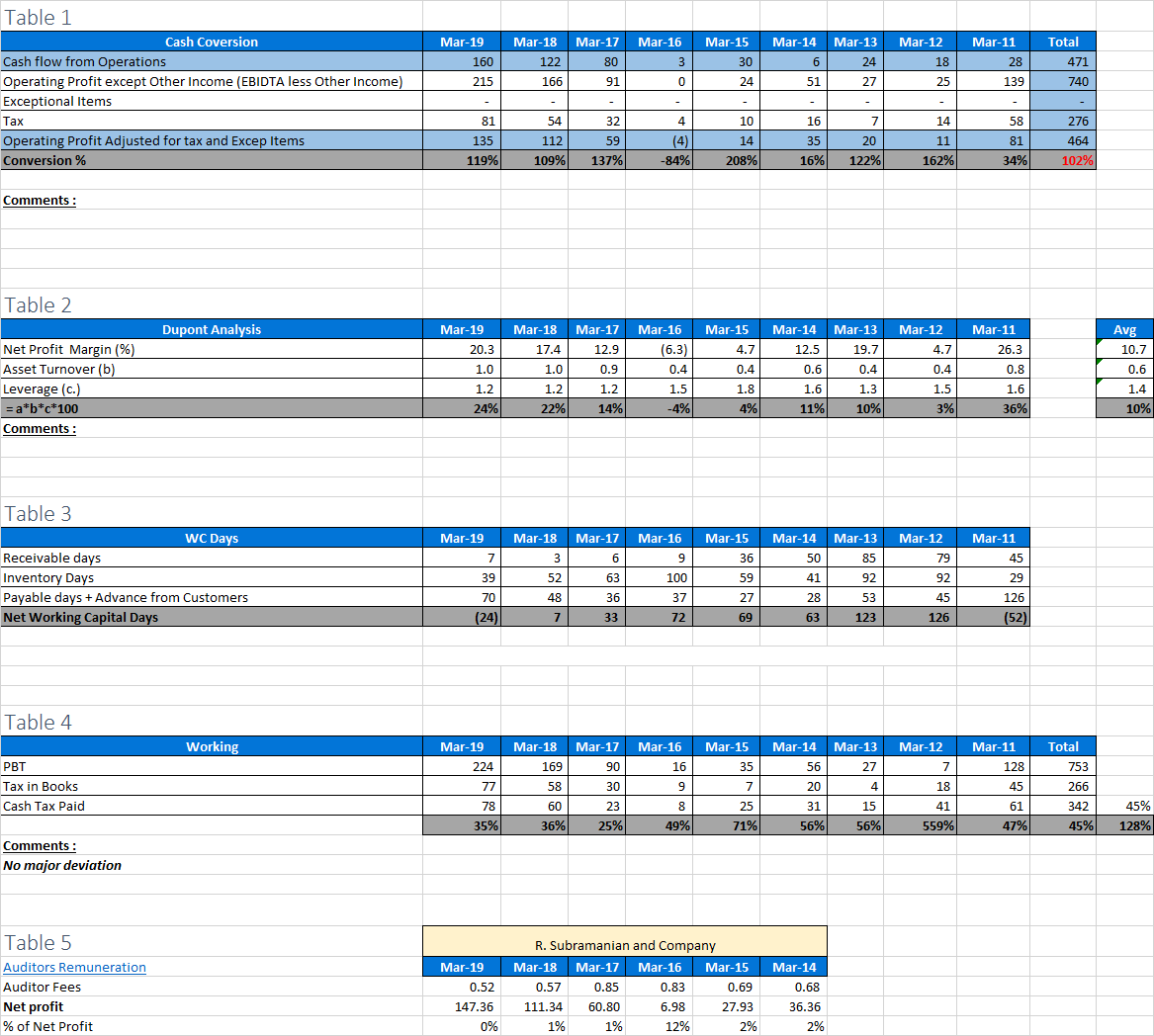

| Rs Cr | Mar-10 | Mar-11 | Mar-12 | Mar-13 | Mar-14 | Mar-15 | Mar-16 | Mar-17 | Mar-18 | Mar-19 | Total |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Cash from Operating Activity (CFO) | 33 | 56 | -66 | 32 | 16 | 36 | -7 | 85 | 128 | 169 | 481 |

| Operating Profit | 36 | 140 | 18 | 26 | 57 | 42 | 20 | 99 | 174 | 224 | |

| Exceptional item | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | |

| Tax | 14 | 45 | 18 | 4 | 20 | 7 | 9 | 30 | 58 | 77 | |

| Operating Profit less Excep Item, Tax | 22 | 96 | 0 | 22 | 37 | 36 | 11 | 69 | 116 | 147 | 555 |

| CFO/Net Profit (Conversion) | 150% | 58% | -389.59 | 144% | 44% | 101% | -67% | 123% | 111% | 115% | 87% |

In Dupont analysis you have mentioned that there is no debt. This is true as on March 31, 2019. However they will have 400 crores of debt as on March 31, 2020. Sandur is spending 600 crores on two Waste Heat Recovery Units (200 crores from its cash reserves and 400 crores of debt).

Under current conditions assuming one month or more of shutdown principal repayment will not be a problem since the loans are on 1 year or 2 year moratorium. However interest payments on a 400 crore loan will significantly reduce the bottomline if things do not get back to normal soon.

I’ve read your write up on the cement sector and it has been immensely helpful. Since many cement companies also undertake capex on WHR, wanted to understand the following:

Sandur is spending 600 crores on WHR units - How would you calculate and analyse if the PV of the cashflows derived from the capex exceed the money utilized for capex?

Hey @aswin,

Sandur already holds 80.58% in Star, therefore, 1 share of Sandur will be issued to “outside” shareholders of Star. On that basis, 19.42% of Star was held by shareholders apart from Sandur and based on that calculation, 2.52L shares will be issued to them ((19.42% of 9.33cr)/72). That is a dilution of 2.88% on existing 87.5L outstanding shares of Sandur. Total outstanding shares after this scheme will be 90.02 lacs.

The latest credit report (link) provides useful details about company liquidity (as on March 31, 2020):

- 87 cr. of free cash and liquid investments

- Applied for COVID loan moratorium which is a bit surprising as company has interest moratorium until April 2021 (am I missing something?)

- Availed 330 cr. out of the sanctioned 400 cr. term loan

As promoters have pledged 55% of their holdings to avail term loans, the current share price of 500 implies that pledged shares are worth ~175 cr. Does this not trigger a breach of loan covenant? Any insights will be useful ![]()

Hi Harsh,

Loan moratorium seems logical as during such uncertain times and when factories are not operating (or operating below optimum utilization), its best to go for moratorium. There won’t be cash flow for coming months and its best to keep surplus funds for expected and un-expected payments. Cash flow mismatches can kill any company as nobody would extend line of credit when things are bad. This will cost a bit on interest cost, but looks ok.

The pledge they have is non-market linked. Its an additional security for the term loan (non-disposal undertaking). But as pledge has been a risky thing, most of the people avoid cos where they see pledge of shares.

The capex is coming onstream at perhaps the worst point of time…who would have thought that all the markets will be shut down for sometime. One will need to wait out a couple of qtrs to see if things are stabilized and reasonable offtakes are happening. Till now iron ore prices have been stable in international market (there have been price cuts in domestic market) and manganese ore prices have increased…these can act as cash cows for the company and take care of some of the hits during these times.

This line in credit rating report was interesting - “The company has availed debt of Rs. 330 crore out of the sanctioned amount of Rs. 400 crore in FY2020 for funding the capex. Around Rs. 590 crore has been spent towards the capex till March 2020. The company’s liquidity profile continued to remain adequate, aided by unencumbered cash and liquid investments of Rs. 87 crore as on March 31, 2020” So company has used internal accruals of close to (590-330+87) 347 Cr which is almost close to the market cap of about 400 Cr?

Ayush

Disc: Invested along with clients

They have an interest moratorium upto 2 years from April 2019 i.e. April 2021. Does that mean they have to pay down the capital part of the loan during this time but not the interest? My question was why do they need a moratorium when they already have one until April 2021. This may just be a minor detail and you can feel free to ignore it ![]()

Thanks for clarifying it! I did not know that.

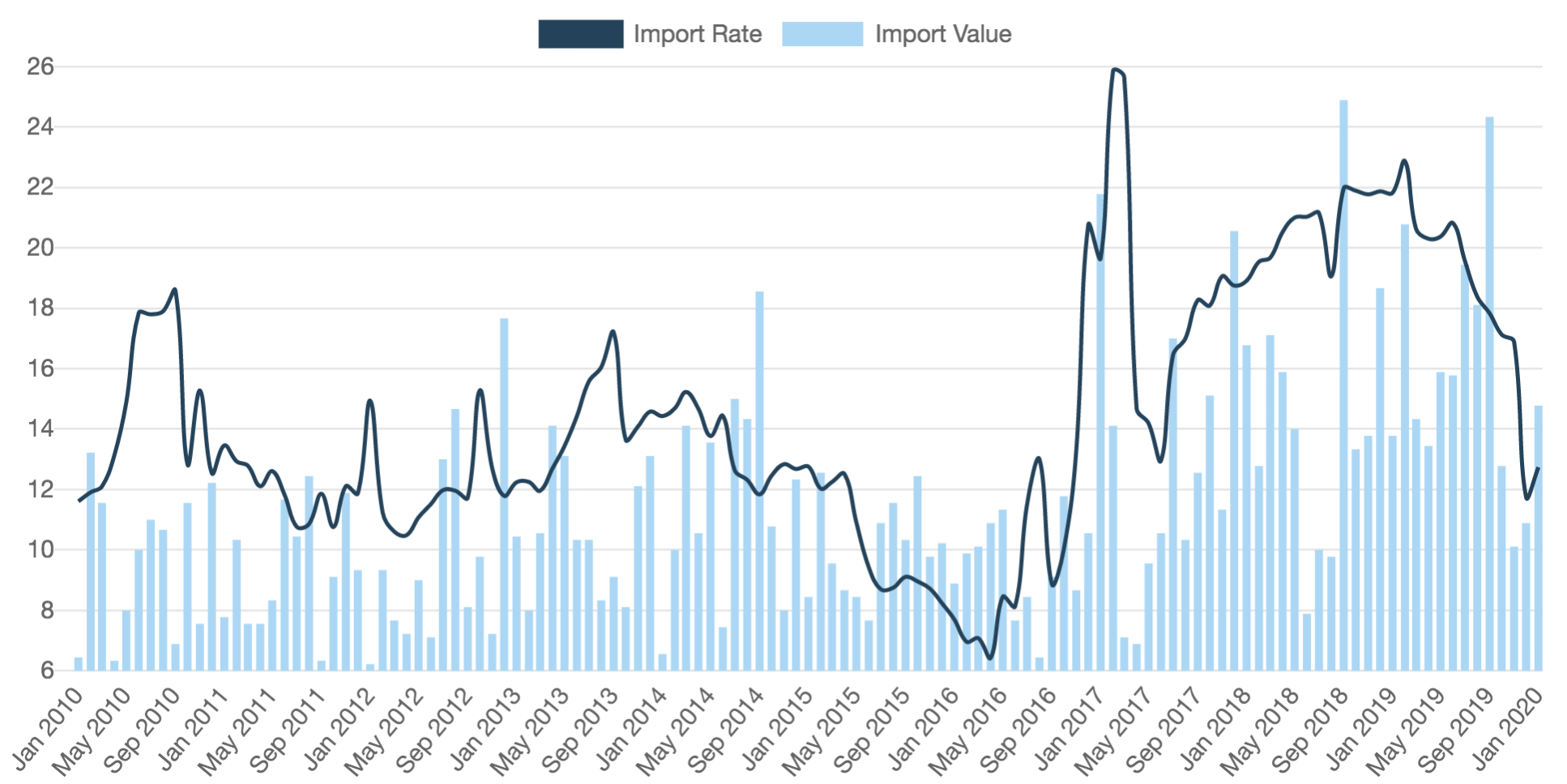

In Indian markets, manganese ore prices import rates have been going down across all purity levels since 2019. (is my interpretation of screener data correct? and is it okay if I share screenshots from premium version of screener?)

Market can do weird things with prices

Thanks!

Harsh

Harsh, good questions…sharing my thoughts (they may be in-correct though)

-

They might be having loan repayments (which get refinanced during normal times). One can check the annual report loan schedule to see the repayment schedule…however, we will have to wait for FY20 annual report to get clarity, as they have been debt free in past so we don’t have details. This could be something technical in nature. If moratorium is there, its a safer thing…as there won’t be cash outflow burden for an year. Co can choose to repay as and when things stabilize but won’t be under any pressure. Actually cos would have to provide for the interest in these periods but cash outflow won’t happen.

-

You can share. Yes, you are right. However recently Moil raised prices sharply by 45% (international prices seem to have increased) - https://www.bseindia.com/xml-data/corpfiling/AttachLive/58c87867-22a0-4dc7-9980-0851b9e279e7.pdf. This may not sustain though.

-

Yeah, I used to feel market is wrong given such attractive valuations and growth prospects but with this Covid event, anything can happen.

Ayush

https://www.bseindia.com/xml-data/corpfiling/AttachLive/37f51e1a-d621-422b-bcc7-f08a2bb7c79f.pdf

Mining operations, ferroalloy plant and power plant stopped from March end. Coke oven was operated at minimum capacity to avoid damage. Company paid full salaries to employees. Operations restarted from beginning of May.

Q1 to be adversely impacted due to lockdown and tepid demand from Indian steel industry. Expect downward pressure on iron ore prices. Applied for moratorium. Adequate liquidity position.

Nazim Sheikh (Company MD) announced his intention to resign from the post as he is vulnerable to be affected by COVID due to his health situation. His resignation will be taken up tomorrow by the board.

The board accepted resignation of Nazim Sheikh and appointed Bahirji Ajai Ghorpade as MD, who was born on 22 May 1995 and is 25 years old!

@ayushmit Is it normal to have such a young MD?

Founders of SMIORE:

Y.R. Ghorpade (Yeshwantrao Hindurao Ghorpade) (1908 -1996) - Ruler of Sandur

M.Y. Ghorpade (Murarirao Yeshwantrao Ghorpade) (1931 - 2011) - Eldest son of

Y.R. Ghorpade - Ruler of Sandur

===========

Ajaisinh Murarao Raje Ghorpade - Eldest son of M. Y. Ghorpade - Now Ruler of Sandur

Bahirji Ajaysinh Raje Ghorpade - Eldest son of Ajaisinh Murarao Raje Ghorpade - became the new MD of SMIORE now

He is the next eligible ruler from the royal family. Inducted on Board in 2015 at the age of 20 to gain experience.

Sandur Manganese has created a Upflag Pattern Breakout

Wholetime director, Rajnish Kumar Singh will resign from the company in November.

Hi,

New to this forum. Request someone to please explain why the Company has mined very little post 2011 until 2016. Is it a demand thing ?

Ratings Reaffirmed:

supreme court ban on mining

Can you pls elaborate more on supreme court ban on mining