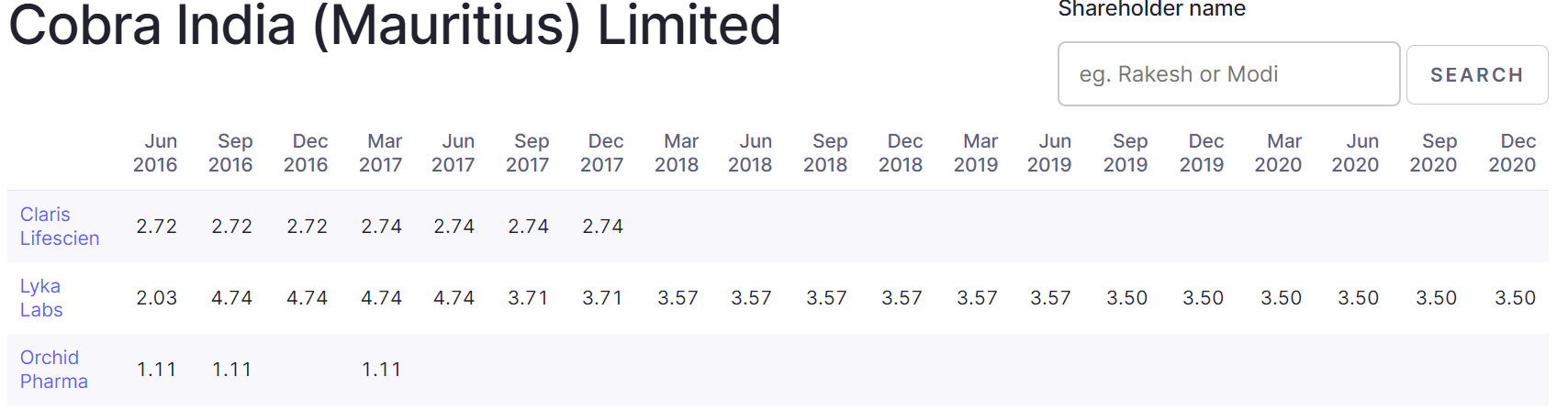

They seem to be invested only in 1 company currently - Lyka Labs. Do you have any more information regarding past investments?

Meanwhile, in a strange turn of events the proposed allotment to B & K has been cancelled.

They seem to be invested only in 1 company currently - Lyka Labs. Do you have any more information regarding past investments?

Meanwhile, in a strange turn of events the proposed allotment to B & K has been cancelled.

Only press release pertaining to respective rating which contains limited information are public. U will have to subscribe to and pay for the detailed rating rationale report to access said report. The link you are referring to is of press release and not the detailed rating rationale.

Sakar Healthcare Limited has informed the Exchange regarding ‘Swiss based HBM Healthcare Investments; a leading global healthcare private equity recently invested Rs 14.85 crore in Sakar Healthcare through its wing COBRA.’

Hi, I am unable to buy the scrip. The order keeps getting rejected. I use Axis direct, NRI account. It asks me to put in a lot size of 3,000, which I do and still get rejected. Any insights would be appreciated.

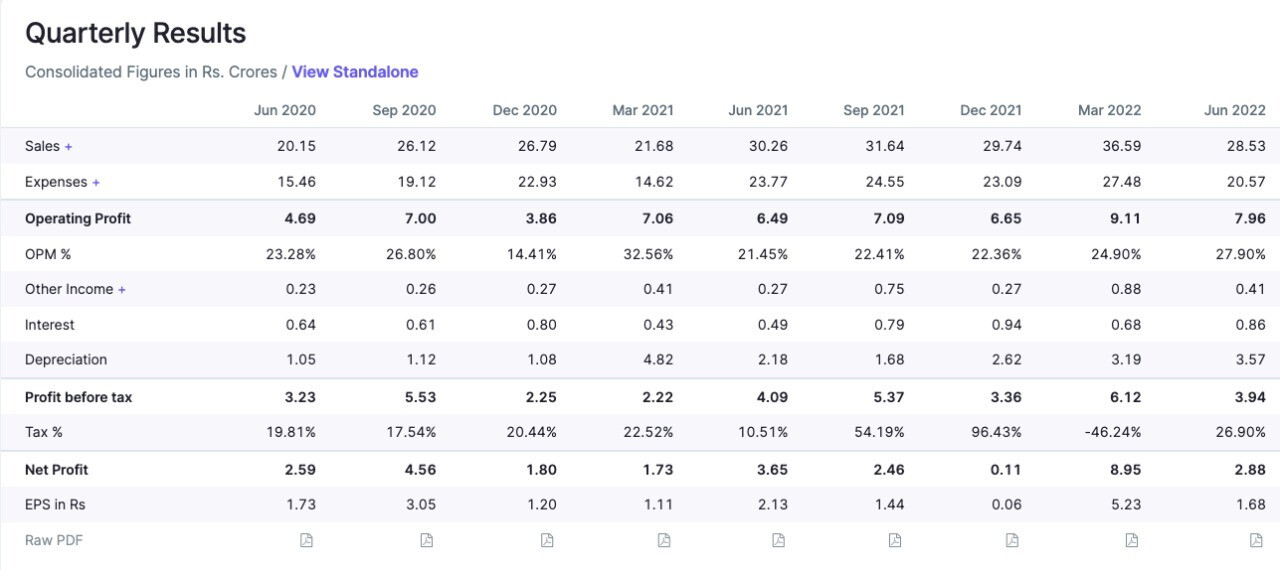

Sakar Healthcare Q-1

While there has been de-growth in sales, ebitda margins have improved. Numbers are decent considering higher depreciation owing to their foray in oncology formulations.

What’s interesting :

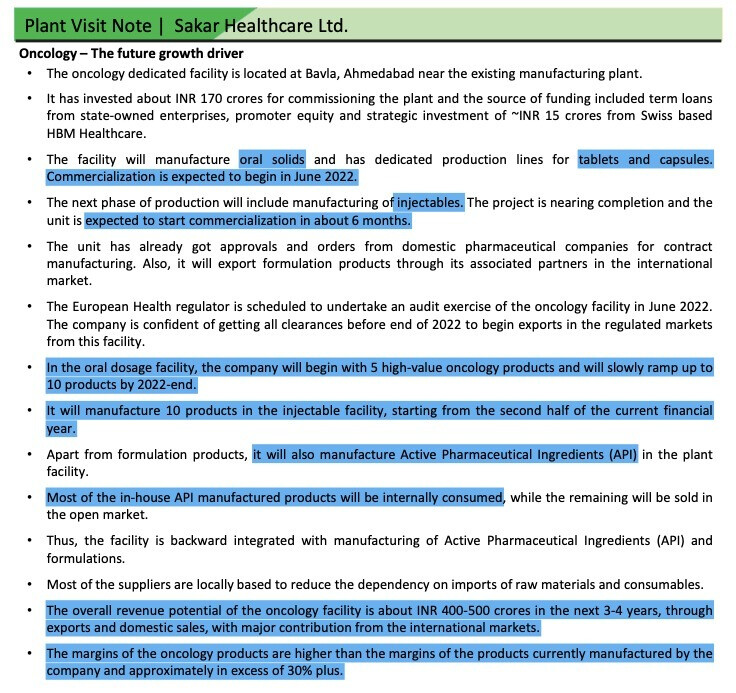

Their manufacturing facility for OSD and tablets + capsules was expected to commercialise in June 2022.

In the OSD section, they have targeted 5 high-value molecules at the beginning. (Source - Arihant Capital Notes)

The commercialisation might be delayed in my view due to following reason :

They are in the process to obtain approval from EU which will take anywhere between 4-6 weeks time post audit if there aren’t any major observations.

In case they receive any major observations, the commercialisation can be delayed by an indefinite time.

While the targets are pretty optimistic and at the same time achievable too, I’ll be keeping an eye on balance sheet position along with execution.

Disclosure - Not invested but definitely interested.

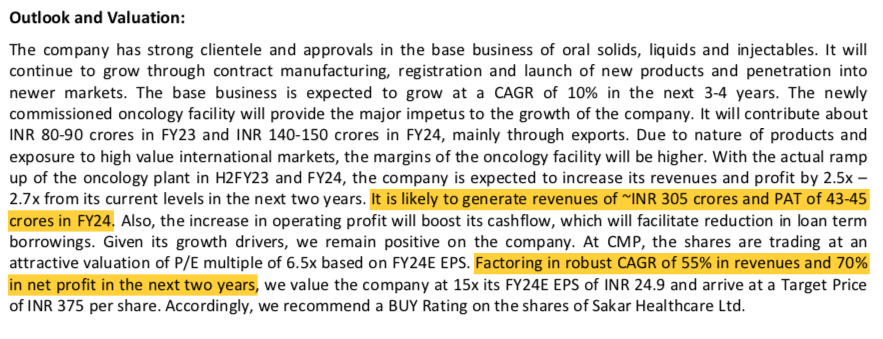

→ FY22

Rev = 125 cr (Considering only Base business with no contribution from oncology)

Ebidta margin = 24%

Ebidta = 30 cr

PAT = 15cr

→ FY24 (as per report)

Rev = 305cr

PAT = 45 cr …3X jump in PAT from FY22 in 2 years

→ FY26

→ Base Business (assuming growing @10%CAGR)

Rev = 185cr

Ebidta = 45cr (margin considered as 24%)

→ Oncology Business

Rev = 450cr (approx avg of 400&500)

Ebidta = 135cr (margin considered 30%)

Total Rev = 630cr

Total Ebidta = 180cr

If it gets 15X Ebidta Multiple (which is its current multiple) then Mcap will be 2700 …like 6X-7X from current Mcap of 420cr

Please feel free to comment your view

Disc : Invested

Note : Entered into an agreement with reputed client (Cadila Healthcare) for oncology product

Whose report is this? Can you share the full report if available.

If I am not wrong, at the AGM the management said oncology plant is complete and we have received WHO GMP approval. We are now starting for validation, stability etc. for the plant. Commercials will be from next financial year onward.

Arihant Capital is the author of the report

Received WHO - GMP approval for oncology Oral Solid Dosage (OSD) and Active Pharmaceutical Ingredient (API) manufacturing blocks

The company makes a profit of 15 crore in last year. Instead of giving dividend to the shareholders , the management invested 7 crore rs in mutual fund. Is it justified ? It may be that they have a capex plan, but a few rupees can be given as a dividend to the shareholder.

The company also takes loan from its directors. There is a phenomenol growth in management’s salary in 2022. any experienced investor can comment upon my view .

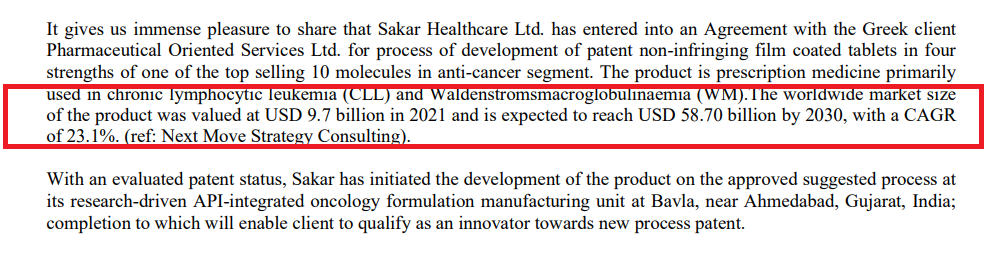

Market growing at 23 % CAGR… not sure how reliable these estimates are. But nevertheless, looks to be a positive development for Sakar.

https://archives.nseindia.com/corporate/SAKAR_11052023113423_Announcement.pdf

Compiled some notes today, Enjoy

Sakar Healthcare.docx (3.9 MB)

EPS has fallen 2 years in a row now. The March 2024 eps is lower than the March 2020 eps. Its trading at a PE of 60 (ind avg is 35). PB is 2.6.

No dividends being paid. Both ROE and ROCE are among the lowest in the industry. Don’t see how such a high PE is justified.

Hi any one has notes from AGM ?

Sakar is not doing any Concalls. But here’s a good news:

Company is presenting at Bharat Connect Conference - Rising Stars September 2024.

It will be taking Questions as well.

Timing is 26th September, 2-3 pm

Here is the Registration Link:

Its totally free, thanks to Arihant Capital.

Enjoy.

I just checked the DuPont Analysis of the company to see ROE Breakup.

The company’s leverage is increased and asset turnover has decreased.

So be careful.

Nothing much happened in the AGM, but I am giving some information below.

Du Pont analysis is the past but market discounts the future. Sakar has setup a Rs.250-crore plant which includes an API, formulations and R&D facility dedicated to Oncology. The unit has received WHO GMP and EU GMP certifications. Revenues from Oncology have just begun and are not captured in current financials.

Last year, a contract with PharOS of Greece was signed in May for product development (mentioned as among the Top 10 products in Oncology). The product has been developed successfully by the company’s R&D and bioequivalence studies by the customer will get initiated soon. I believe some milestone payments have already been received for the same. Similarly, contracts with Ferring Pharma and Bazell Pharma of Switzerland for development and supply of two Oncology products have also been signed last year, and the Annual Report mentions validation work is going on. Currently, company has 6 products are under development in oral solid and 7 in oral liquid category in Oncology alone. Most of these products are either in validation or in accelerated stability study phase. Meanwhile, for the export markets, regulatory filing has been done for 17 product registrations till now in the EU and 10 in Latin America, Southeast Asia, Africa. Work is in progress on another 28 product dossiers. Nine agreements have been signed internationally on Oncology products of which 6 are in Europe / UK. In the domestic markets, 10 agreements have been signed in India. Commercials have started with 9 customers, and this will go up to around 12 by FY25 end. Approvals from EU are expected to start coming in from Q4 of this year. In addition, company is also in discussion with several potential customers for strategic tie-ups.

Meanwhile, rest of the business (non-oncology) is expected to grow at 7 to 8 % in line with the market growth. Here, Sakar in mainly doing CDMO / outsourced manufacturing for customers such as Zydus Lifesciences, Intas, Emcure, Glenmark, Torrent etc. I believe Zydus is the main customer. The Annual Report mentions technology transfer from Zydus Life Sciences for 23 SKUs of Oral Solids and 19 SKUs of injections, besides some others such as API supply to Jodas and Meta Life Sciences. Sakar does not market its own brands in the domestic market.

Overall, till date in FY25, filing has been done for 33 product registrations in all (including 17 mentioned above) & 4 registrations have been received. By the end of this financial year, dossier submission is expected reach 50. Company now has 290 product registrations in its own name and 321 registrations in all. Pharma is a long gestation business, it takes years to set a facility, file for product registrations, get approvals, sign customer contracts and revenues to start flowing in.

In FY24, Oncology revenues were just Rs.30 crore of the total of Rs.150-odd crore revenues. Going ahead, Oncology revenues are expected to double in FY25 and touch around Rs.100 crores by FY26. Once the product approvals start coming in, company expects to generate Rs.500 crores from Oncology alone over three years. Moreover, these will be at a higher margin of around 28 to 30 % compared to the existing business.

So, a lot of work has been happening which is not reflected in the current financials. The management has raised equity funding along the way which has kept debt levels under control. I have been invested in the stock for nearly four years now, and so far, I find the management has executed well. Last year, Tata Capital took a stake in the company, providing a stamp of approval for the business. All these expectations are factored in the current valuations.

I understand that there is a lot of work happening which is not being seen in the numbers yet. Looking at the scale of capex and the way they have been handling the debt, the future of the business looks promising.

At the same time, the shareholders have approved the salary increase of MD and JMD 5 fold to 2.4 crores and 1.8 crores respectively, with Net Profit of ~12 crores. The incremental revenues from new capex are yet to be seen. As per my calculations, a very small proportion of the new capex will be adding to the top-line and bottom-line in this financial year. The cap on the salaries of the management vis-a-vis the Net Profits is 10% in total. How do you read this?

I will really appreciate if someone can help me get more clarity on it.