Today I received a mail form their CS, pasting here if anyone is interested. Though i am still not satisfied with few answers.

We are pleased to know and appreciate your continued support, faith and association with the company.

With regards to the concerns raised by you, the clarifications sought by you are as follows:

-

In the year 2017-18 rate of depreciation on computers was changed from earlier depreciation rate of 31.67% (which was as per companies act) to 13.96%, please elaborate the reason for the same. Same issue of depreciation rate change is there in the Factory Building in 2018-19. May please clarify.

Reply: The company has been consistently applying the rates of depreciation prescribed under the companies Act, 2013 on the respective asset class and there have been no changes in the rate of depreciation applied to the respective asset class. Rate of depreciation applied on the asset class computers is 31.67% and not 13.96% and similarly depreciation at the rate of 3.17% has been consistently applied all through the years on the asset class Factory building.

-

From the year 2017-18 we are showing Intangible assets in the balance sheet and amortizing it @31.67%. May please provide details/nature of such assets for the year 2017-18 to 2019-20.

Reply: The intangible asset class as presented in the balance sheet consists of companies Product registrations and product permissions obtained by the company in overseas market where the company sells the respective products in its own name.

-

As mentioned in the prospectus and in credit rating reports we are in contract manufacturing and sell our own formulations through dealers in various semi regulated export markets. I want to know more about the export business we are in, do we manufacture formulations on their behalf or we are doing it under our own brand.

Reply: The export portfolio of the company consists of company own products registered in companies name in overseas market where the company sells its own product through its appointed distributors.

-

We are in the formulation business from last so many years, do we have any IPs in this field.

Reply: The company does not have any IP.

-

What is our current strength of scientist and PHDs engaged in R&D work.

Reply: Company has in-house team of scientists who are engaged in R&D work.

-

In the recent quarterly result i.e. Q3 2020-21, our margins were impacted due to higher raw material cost and that was the first time we faced such a situation in last so many quarters. May please explain the reason for contraction in the margin. Along with that I also want to know how we manage fluctuations in raw material prices, do we have pass through mechanism for increase in raw material cost in our final product?

Reply: As rightly pointed out by you the Q3 results have been impacted by the increase in raw-material cost, which resulted in reduced margins. The increase in raw material prices was unprecedented resulting out of pandemic situation and sudden hold of imports, though the markets are stabilizing gradually, and we also expect the spike in raw material prices to normalize which would help the company regain its margins. The selling price of the final products are adjusted to take care of the fluctuations in raw material prices in the ordinary course of business. The price trends in Q3 being exceptional and temporary the company chose to absorb the price fluctuation instead of passing it on to our regular buyers in the larger interest of the company’s growth and goodwill.

-

For the last seven years our margins are in the range of 20-25% and that time we were doing regular capex. So now when we already established capacities can we expect any expansion in margins going forward due to overhead savings etc. may please share your views on it.

Reply: The company is in the process of strategizing its growth trajectory which includes expansion into oncology segment to achieve increased profit margins, impact of overhead savings could be known in the following periods of operations.

-

From the last four years we are continuously diluting equity share capital by way of share warrants and preferential allotment, though increasing stake by promoters showing their conviction in the business but at the same time it is impacting return on equity. Do we have any plans for further dilution, may please clarify.

Reply: The company is in growth stage which requires infusion of funds at regular intervals comprising of optimal mix of equity and debt, in order the ensure optimal capital structure and optimal cost of capital there has been regular infusion of funds by the promoters. As also rightly pointed out, the conviction of promoters in their business motivates the promoters to infuse their own funds which is by way of preferential issues. We are under process of preferential allotment which details are available on the website of the company i.e. www.sakarhealthcare.com.

-

Export is the major portion of our total revenue, to neutralize foreign currency risk do we have any hedging policy in place or not?

Reply: Exports comprise major portion of company’s revenue and forex rate fluctuations being the risk faced by the company, the company has been devising various actionable to mitigate this forex rate fluctuation risk of which one being opening EEFC account and the company is also in the process of appointing treasury team which will strategize and devise the process to mitigate the risk of forex rate fluctuations.

-

We have one of the best working capital management as compared to peers, so please share insights about how we are managing receivable turnover and inventory turnover so efficiently?

Reply: The company has been able manage its working capital optimally owing to the company’s receivable and inventory management policies and practices.

-

As compared to our peers, what are the key competitive advantages we have over our competitors?

Reply: Sakar healthcare is well equipped with the Manpower, Technology and funding requirement. Further as you already know that the company got the EU GMP approval for Small Volume Parenteral (SVP) manufacturing unit of liquid injections and Lyophilised injections which is addition to the brand building for the company.

-

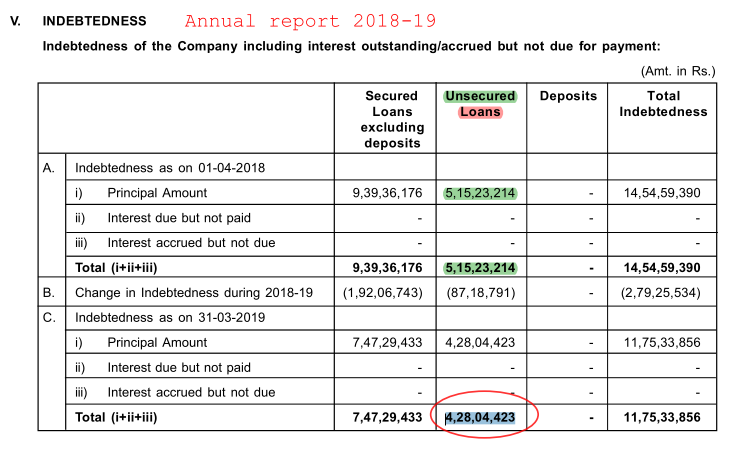

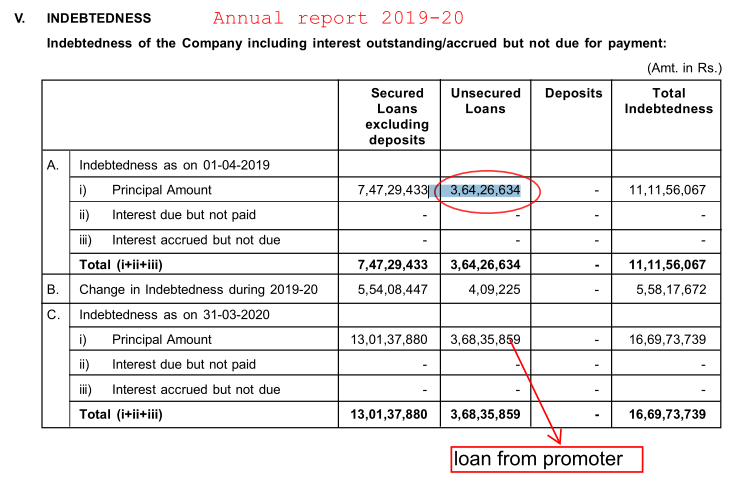

As per our latest board meeting, we are converting promoter’s loan into equity in form of preferential allotment. Whether that loan carries any interest or it is interest free, may please also share the rationale behind its conversion in equity.

Reply: The loan of the promoters is unsecured and interest free though notional interest is charged in the books of account in compliance with IndAS stipulations. The loan of the promoters is being converted into equity in compliance with the stipulation of our bankers to ensure the debt equity ratio required for the proposed expansion of the company’s operations into Oncology segment.

Oncology Capex:

-

As capex for oncology plant is already going on, please share the breakup of how much money has already been spent and balance capex amount. Alongside also share a timeline, when that plant will start generating revenue.

Reply: The oncology project is scheduled to be implemented in two phases with total capex of approximately 145 crores. The phase I capex is estimated at 115 crores out of which the company has incurred approximately 57 crores towards capex of oncology project uptill the end of Q3 and the company estimates that the revenue generation from October 2021 for oncology products planned in Phase - I. Phase II capex is estimated at Rs. 30 crores is planned for implementation in FY 2023.

-

As per CARE latest credit rating report total capex for the oncology segment will be around 140 crs, how much asset turnover we can expect from this upcoming plant, and any guidance on margins.

Reply: The rating activity has been carried out by ICRA and assets turnover of approximately 3 times is estimated by the company from the planned capex estimated to be achieved over a period of 5 years after complete implementation of the project. The company estimates improved margins adding to the existing margins of the company.

-

There are many companies which are dedicated only to oncology segment, from as big as Natco pharma to Shilpa Medicare and in small cap companies like Beta drugs limited. They are established players and dedicatedly working on R&D for new molecules in oncology API. What kind of advantages we have over these established players, please share your views on it. and whether we are targeting any particularTKIs or molecules in the oncology segment.

Reply: Ahmedabad being a Pharma hub of India, with world renowned and established companies, provides a locational advantage to Sakar of being a local manufacturer of oncology products. Presently all the big pharma companies get many of their oncology products manufactured at far away locations and Sakar’s proposed oncology manufacturing facility provides them ease in terms of localization, control, supervision and logistics benefits. Sakar being a preferred manufacturing location for all the big pharma companies already will be benefited from the existing relations giving Sakar required initial thrust required to successfully launch itself into oncology market segment. The company has already identified molecules for the oncology manufacturing facility.