Thanks for bringing up this point. I agree when viewed this way, the compensation seems on the higher side but this is at the moment only an enabling resolution. We need to wait and see how much they actually take and what are the revenues at that point of time. Sakar’s promoter remuneration has been within normal range until now though it has increased rapidly in recent years. I view it as a negative but not a show stopper as yet. If the revenues increase in line with the salary, it would be okay I guess. But yes, this is a point that needs to be watched.

3 Likes

Hello guys,

i had two questions -

-

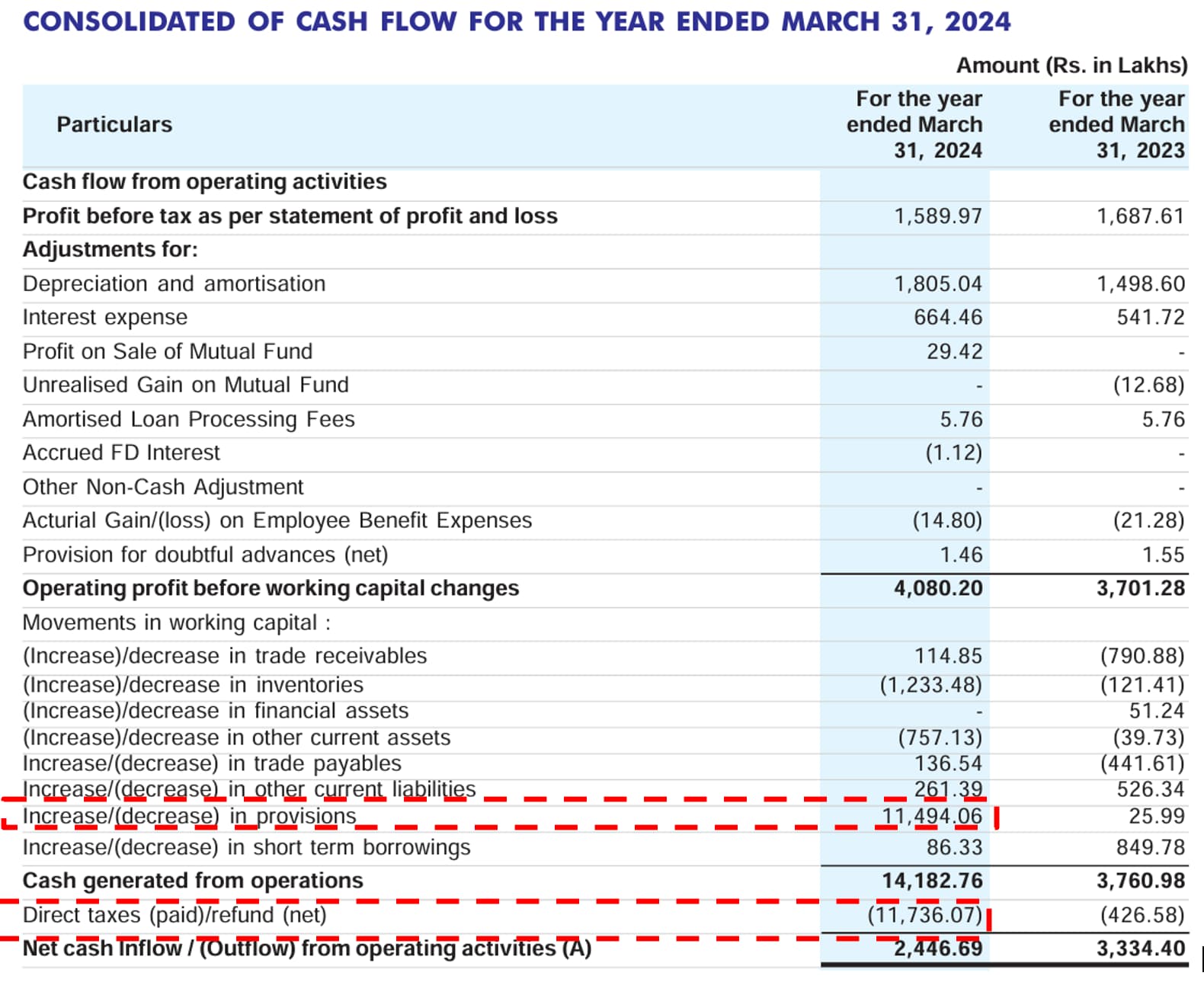

As per the AR 2024 cash flow statement they received ~Rs 115 crs via increase in provision and there was a tax cash outflow of Rs ~117 crs - can anyone clarify on this transaction as there is nothing in balance sheet provisions and notes - Attaching screenshot below for reference -

-

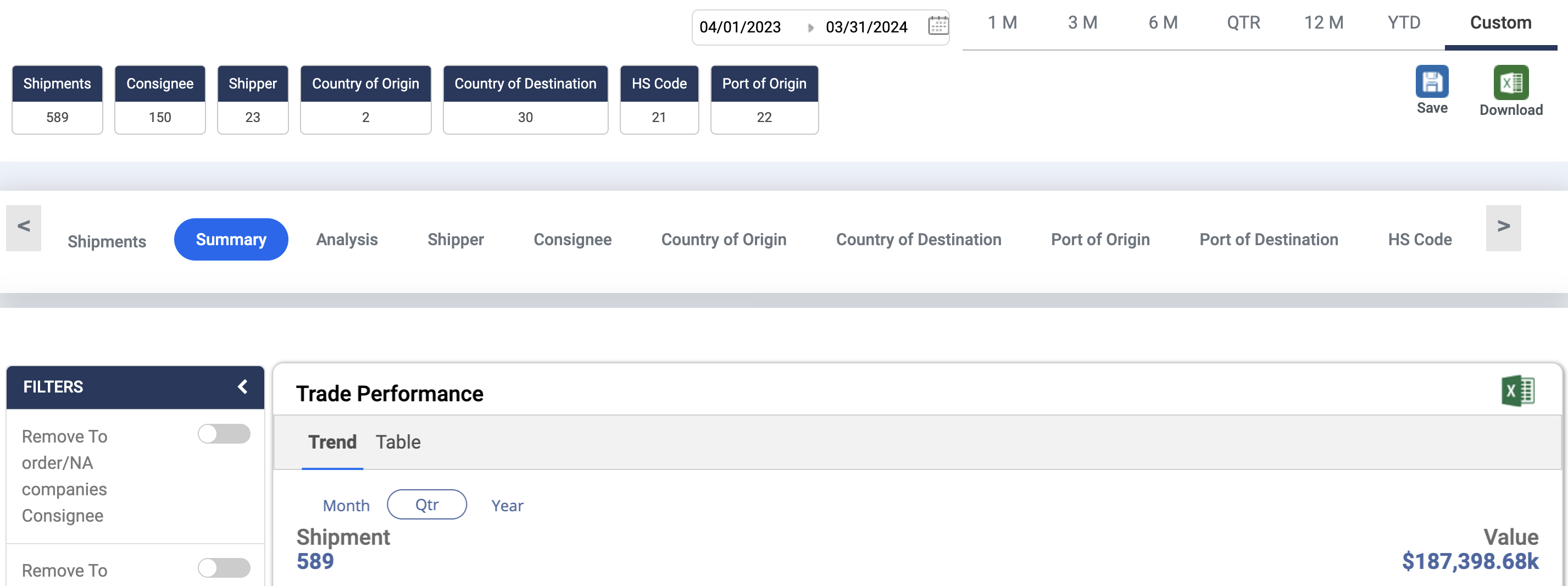

I was checking Sakar healthcare’s export data on Volza - as per company’s AR 2024 - they exported goods worth Rs 94 crs - but as per the volza portal the exports were to the tune of ~$ 187 mn which translates to ~Rs 1500 crs - there were six sakar healthcares with same address - couldnt find anyother company online which could also be named Sakar Healthcare and all these shipments source country was India - Anyone has any idea what is it that i am doing wrong here - Attaching screen shots of volza below for reference -

Thank You

4 Likes

Hi, On point no. 1, this is an error. There is some typo or something, I have got it confirmed from the company. While this is an error, the company has confirmed that the final figure of Net Cash Inflow is correct due to the offsetting impact of Increase / (decrease) in Provisions and Direct Taxes.

1 Like

Here is a link to the presentation at the event organised by Arihant Capital

2 Likes

Nuvama Emerging Ideas 2024 Conference note on Sakar:

Sakar Presentation was today, This is Pre-Conf.

1 Like

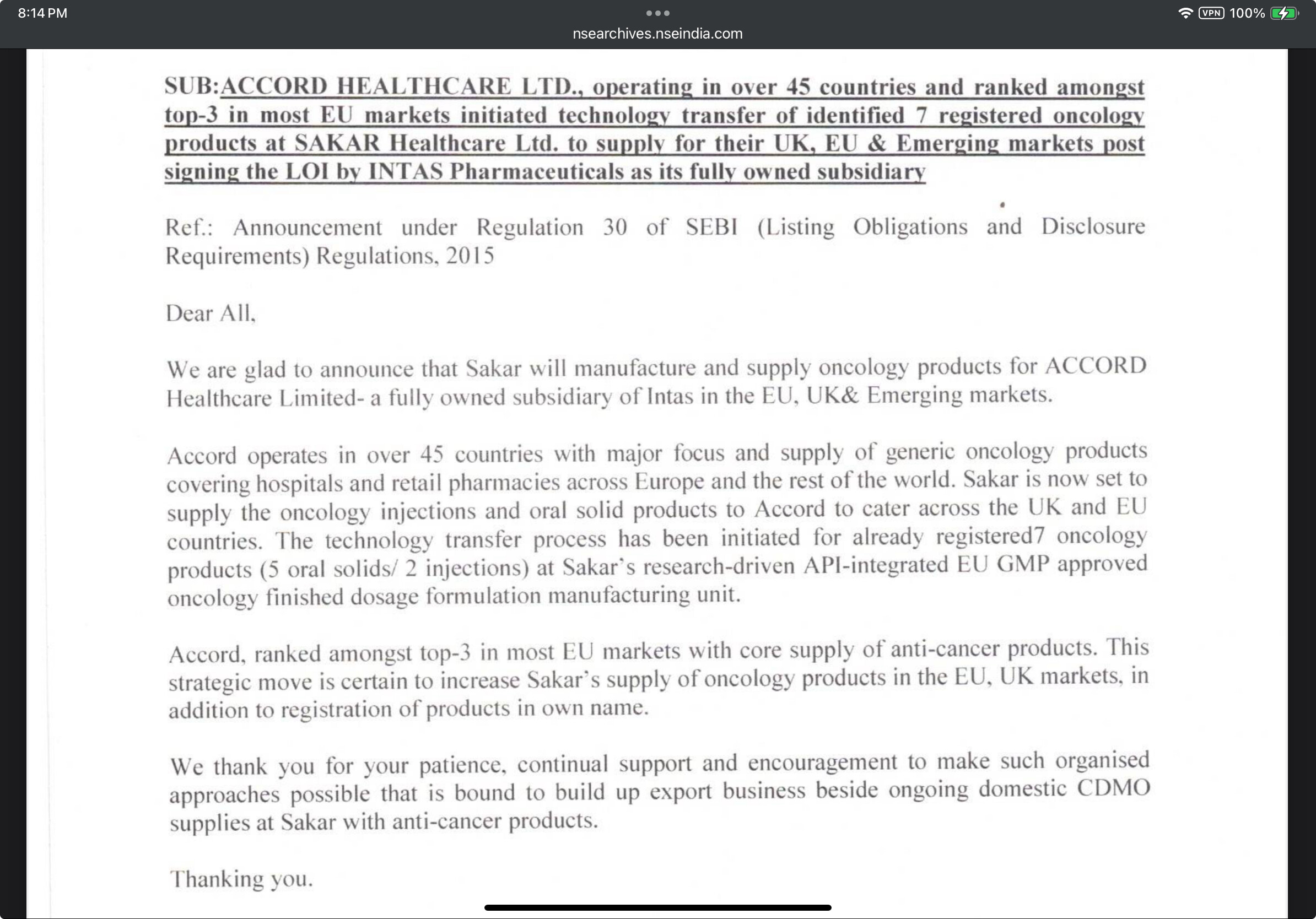

Sakar health care will supply 5 oral solids / 2 injections to accord healthcare for oncology products .

5 Likes

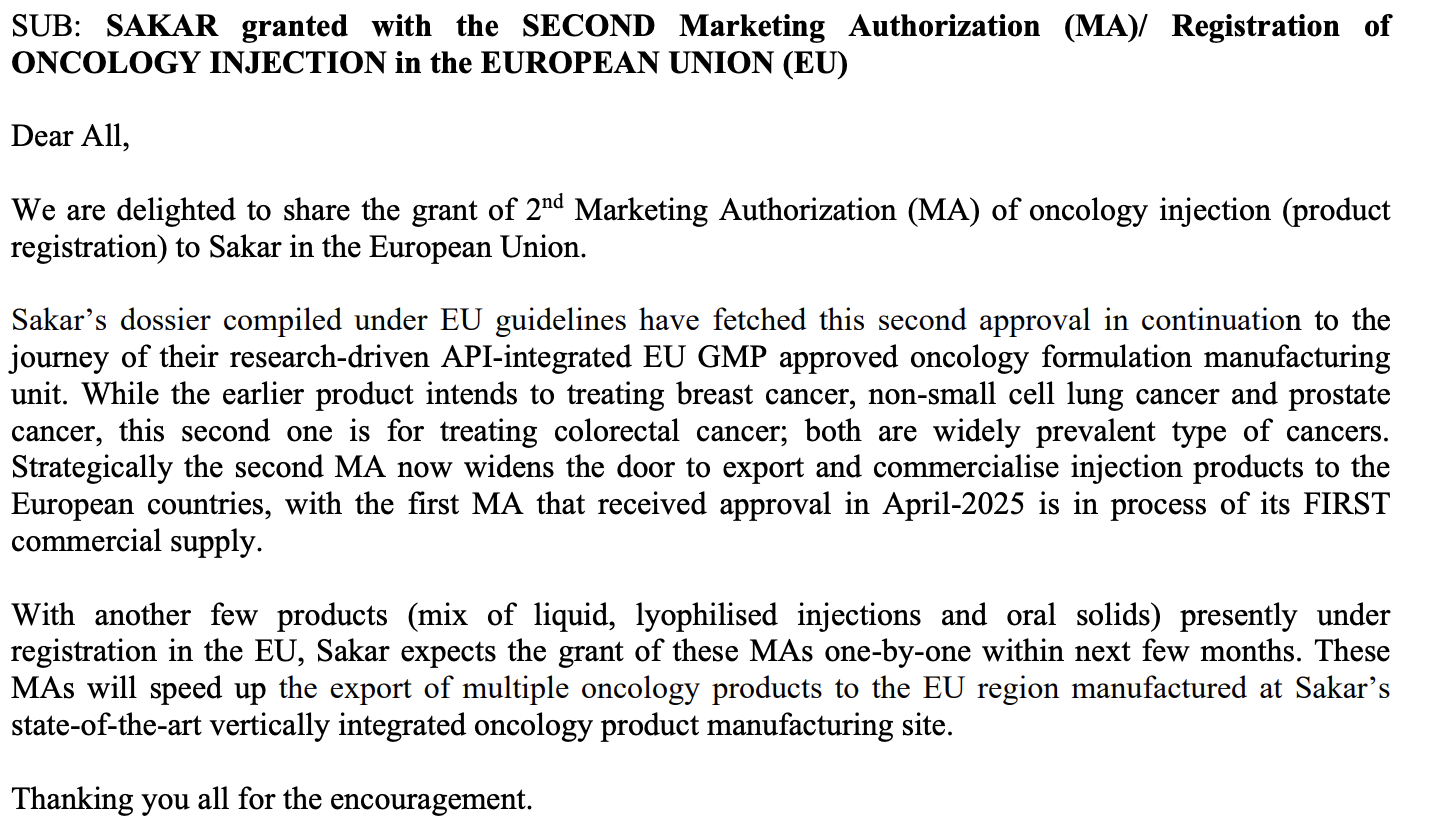

SAKAR granted with THIRD & FOURTH Marketing Authorization (MA)/ Registration of

ONCOLOGY INJECTIONS in EUROPE

There has been two more Marketing Authorisations (MA) granted with oncology injection (product registration) to Sakar in the European Union, taking the count to four MAs.

Two of the product dossiers for Carboplatin and Docetaxel compiled under EU guidelines have fetched approvals from Bulgaria and Bosnia. Both the dossiers are a part of Sakar’s present effort in regulatory front from its research-driven API-integrated EU GMP approved oncology formulation manufacturing unit.

While the earlier products (MAs) intends to treating breast cancer, non-small cell lung cancer, prostate cancer, colorectal cancer; Carboplatin is intended for ovarian, lung cancer along with other solid tumours.

Strategically these approvals now widens the scope to export anti-cancer injections to the European countries, while Sakar prepares the commercial supply with the first two received MAs.

With a mix of oncology products in process of registration in the EU and rest of world markets, Sakar expects to receive grant of more MAs within few months. These MAs will speed up the export of multiple oncology products to the EU region manufactured at Sakar’s state of the art, vertically integrated oncology product manufacturing site.

1 Like

Presentation after 3 years:

Maiden Concall as well:

Here’s the recording:

3 Likes

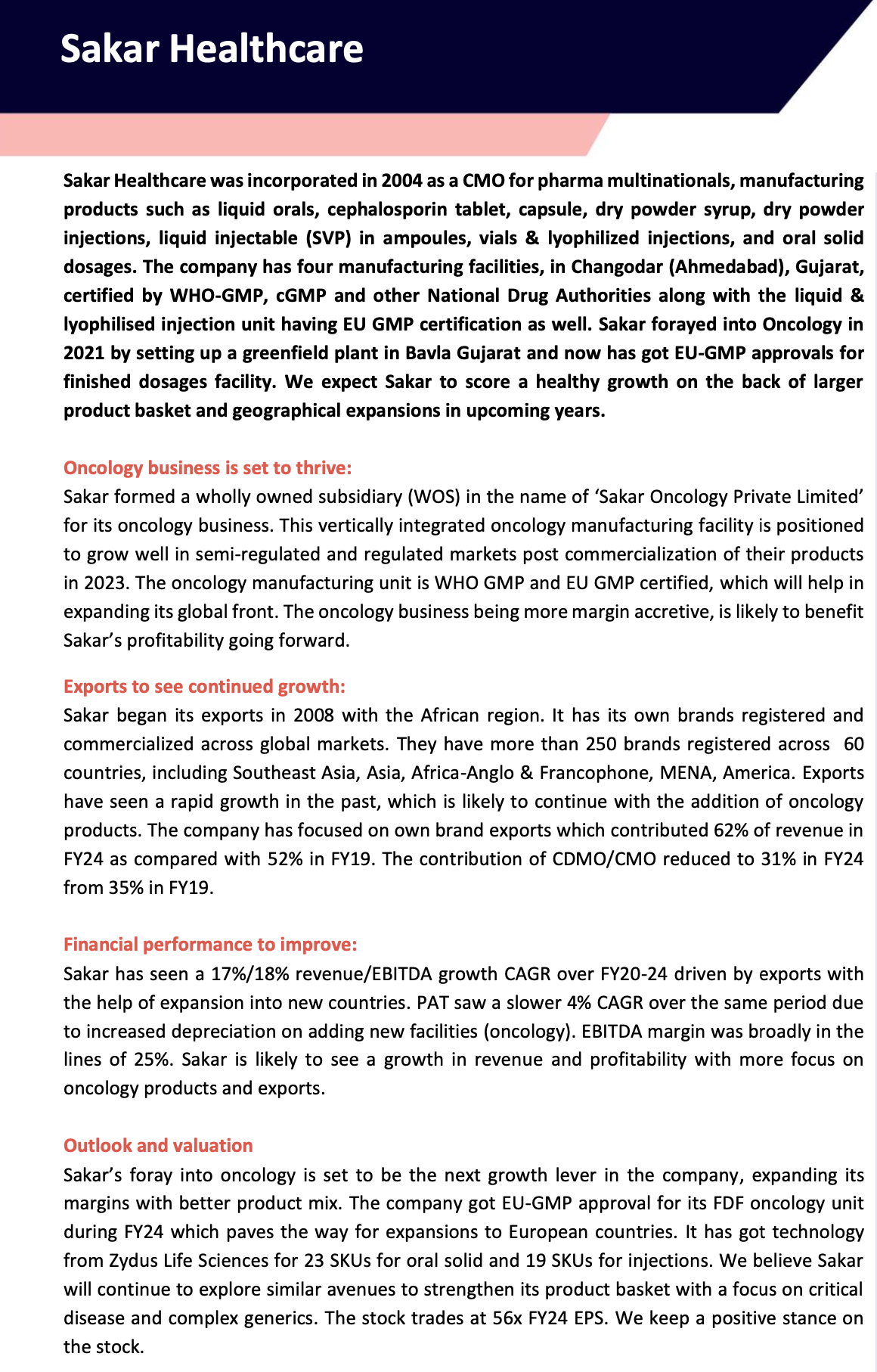

Sakar Healthcare Ltd: At an inflection point

1. Summary

Sakar Healthcare Ltd is a Gujarat-based pharmaceutical company evolving from a contract manufacturer to an integrated pharmaceutical player with a niche focus on Oncology. The company operates vertically integrated facilities (API to Formulations) and has recently achieved a significant milestone by securing EU-GMP approval for its dedicated oncology unit. This approval opens the door to high-margin regulated markets in Europe.

-

Current Status: Transitioning from low-margin generic manufacturing to high-margin oncology exports and CDMO services.

-

Key Trigger: The recent EU-GMP approval and a strategic manufacturing agreement with Accord Healthcare (UK) for supplying oncology products to the European market.

-

Financial Health: The company is growing revenues (CAGR ~17%) but faces near-term margin pressure due to high employee costs and operating expenses related to the new plant. Return ratios (ROE/ROCE) are currently suppressed (~6-8%) due to heavy capex that has yet to fully monetize.

2. Company History & Evolution

Founded in 2004, Sakar Healthcare has steadily moved up the value chain.

-

2004-2008: Incorporated as a private limited company. Started operations as a contract manufacturer for domestic players.

-

2008-2015: Expanded product portfolio to include Liquid Orals and Small Volume Parenterals (injections). Established presence in semi-regulated markets (Africa, SE Asia).

-

2016: Listed on the NSE Emerge (SME Platform), raising funds for expansion.

-

2019: Migrated to the NSE Main Board, signalling maturity and better governance standards.

-

2020-2023: Strategic pivot to Oncology. Construction of a dedicated API and Formulation oncology facility at Bavla, Gujarat. Secured WHO-GMP certification.

-

2024: Achieved EU-GMP approval for the Oncology unit (Liquid & Lyophilized Injections, Oral Solids). This is a major inflection point, validating their quality standards for regulated markets.

-

2025: Signed a landmark contract with Accord Healthcare (UK) and received the first patent for the Imatinib process.

3. Promoter Background & Management

The company is family-owned and professionally managed, with the second generation actively involved.

-

Mr. Sanjay S. Shah (Promoter, Chairman & MD):

-

Background: The founder with over two decades of experience. He holds a commerce and law degree.

-

Role: visionary behind the shift to oncology and regulated markets. He focuses on strategic tie-ups and overall administration.

-

-

Mr. Aarsh S. Shah (Joint Managing Director):

-

Background: Holds an MBA/Management degree and represents the next generation.

-

Role: deeply involved in International Business Development, specifically targeting the EU and regulated markets. He is instrumental in securing recent tie-ups with global majors like Accord and Zydus.

-

-

Mr. Rita S. Shah (Non-Executive Director): Involved in CSR and general administration.

-

Professional Management: The company has recently hired senior professionals, including a new COO (Mr. Sudhir Ghule) and VP of Strategy (Mr. Bikramjit Ghosh), indicating a move towards professionalizing operations to handle scale.

4. Promoter Remuneration

Analysis of the Annual Report FY25 reveals the following remuneration trends:

-

Sanjay Shah (MD): Remuneration increased significantly to ₹72.00 Lakhs in FY25.

-

Aarsh Shah (Jt. MD): Remuneration also stood at ₹72.00 Lakhs in FY25.

-

Key Observation: The remuneration policy seems aligned with the company’s growth, but the jump in remuneration (approx. 50-60% increase for promoters) during a year where free cash flows were negative due to capex warrants monitoring. However, it is within the statutory limits of the Companies Act.

5. Business Model & Strategic Focus

Sakar operates on a hybrid business model that de-risks its revenue streams while chasing high growth.

-

Contract Development & Manufacturing (CDMO):

-

Manufacturing for domestic giants like Zydus Lifesciences, Cipla, Glenmark, Dr. Reddy’s, and Intas.

-

Provides steady cash flow and factory utilization.

-

-

Own Brand Exports:

-

Sells branded generics in 60+ countries (Africa, SE Asia, LatAm).

-

Higher margins than contract manufacturing.

-

Strategic Shift: Moving from semi-regulated to regulated markets (Europe) with the new EU-GMP approval.

-

-

Oncology (The Growth Engine):

-

-

Vertical Integration: Sakar manufactures both the API (Active Pharmaceutical Ingredient) and the Finished Dosage Form (FDF). This captures the entire value chain margin and reduces dependency on external API suppliers (specifically China).

-

Product Portfolio: 55 oncology molecules developed (Imatinib, Gefitinib, etc.). 11 Marketing Authorizations (MAs) already granted

-

6. Manufacturing Capabilities & Infrastructure

Sakar owns two manufacturing units in Gujarat:

-

Changodar Unit (General Formulations):

-

WHO-GMP certified.

-

Produces Tablets, Capsules, Liquid Orals, and Dry Powder Injections (Cephalosporins).

-

Utilization is high; caters to legacy business.

-

-

Bavla Unit (Oncology & Research):

-

EU-GMP Approved.

-

Capabilities:

-

Oral Solids: Tablets & Capsules (High containment OEL Level 4 for safety).

-

Injectables: Liquid and Lyophilized (Freeze-dried) vials.

-

API Block: Dedicated block for oncology APIs using Flow Chemistry and Green Chemistry principles to reduce waste and cost.

-

-

Research: In-house R&D center recognized by the Department of Scientific & Industrial Research (DSIR).

-

7. Financial Analysis: Quality of Earnings

Based on FY25 Annual Report and Q2 FY26 Results.

-

Revenue Growth:

-

FY25 Revenue: ₹178 Cr (up ~17% YoY).

-

Q2 FY26 Revenue: ₹57.56 Cr (up 34% YoY). The growth trajectory is accelerating as the oncology unit contributes more.

-

-

Margins:

-

EBITDA Margin: ~20-24% range. Margins have seen some compression recently due to high employee costs (hiring for the new plant) and R&D expenses.

-

Gross Margins: Healthy at ~46-47%, indicating good pricing power or low raw material costs relative to sales price.

-

-

Other Income:

- In Q2 FY26, Other Income was ₹1.21 Cr, which is minimal compared to core operations. Earnings are largely driven by core business operations, which is a positive sign.

-

Quality of Profit:

- Cash Flow vs. PAT: In FY25, the company reported a PAT of ₹17.5 Cr but Operating Cash Flow (CFO) was ₹34 Cr. This is a very positive sign, indicating that profits are being converted into actual cash and are not just “paper profits” stuck in receivables.

8. Balance Sheet Analysis

-

Debt Profile:

-

Debt-to-Equity: Comfortable at 0.30x (FY25).

-

Total Borrowings: ~₹86 Cr (Long-term: ₹53.5 Cr, Short-term: ₹21.3 Cr).

-

Coverage: Interest Coverage Ratio has improved to 2.95x in FY25 (from 0.72x), indicating better ability to service debt.

-

-

Working Capital:

-

Inventory Days: Increased significantly to 166 days (FY25) from 76 days. Red Flag: This suggests inventory pile-up, likely due to the new oncology plant stocking up before commercial sales or delays in offtake.

-

Debtor Days: Stable at 63 days.

-

Current Ratio: 1.41, indicating adequate liquidity to meet short-term obligations.

-

-

Receivables:

- Trade receivables stood at ₹30.7 Cr (FY25). The aging profile needs monitoring, but the debtor turnover ratio is healthy.

9. Cash Flows

-

Operating Cash Flow (CFO): Positive (₹34 Cr in FY25). Driven by strong operating profits before working capital changes.

-

Investing Cash Flow (CFI): Negative (-₹30.7 Cr). This is primarily due to heavy Capex (Purchase of Property, Plant, Equipment) for the oncology unit.

-

Financing Cash Flow (CFF): Negative (-₹3.4 Cr). The company is repaying some borrowings and paying interest, balanced by some equity/warrant inflows.

-

Free Cash Flow (FCF): Currently negligible or slightly negative due to heavy reinvestment in Capex. This is typical for a company in a high-growth expansion phase.

10. Capex & Opportunities Going Ahead

-

Recent Capex: The company has invested over ₹150-200 Cr in the last few years to build the Bavla oncology facility.

-

Future Capex: Management has guided for ~₹27 Cr of additional Capex for FY26, primarily for maintenance and minor upgrades. The major heavy lifting is done.

-

Asset Turnover: The current asset turnover is low because the new plant is not yet fully utilized. As utilization ramps up (operating leverage), the Return on Capital Employed (ROCE) is expected to expand significantly from the current ~8%.

11. Future Prospects

The investment thesis rests on the “Operating Leverage” play:

-

Regulated Markets Entry: With EU-GMP approval, Sakar can now sell in Europe where price realizations are significantly higher than in Africa/Asia.

-

Accord Healthcare Deal: The contract with Accord (a major UK generic player) validates Sakar’s capabilities. Manufacturing for Accord’s EU requirements will fill capacity and provide steady revenue.

-

Patent Portfolio: Grant of the Imatinib process patent allows Sakar to launch this blockbuster drug with a cost advantage (using their proprietary process).

-

Forward Integration: Moving from just CDMO to filing their own dossiers (MAs). They have 11 granted MAs and 30+ dossiers ready. Owning the IP (Intellectual Property) yields higher margins.

12. Key Risks, Red Flags & Contingent Liabilities

-

Contingent Liabilities: The Annual Report explicitly states “NIL” contingent liabilities as of March 31, 2025. This is a clean chit.

-

Red Flags:

-

Rising Employee Costs: Employee expenses jumped 46% in H1 FY26. While necessary for the new plant, if revenue ramp-up is delayed, this will crush margins.

-

Inventory Pile-up: The jump to 166 inventory days is a concern. Investors must watch if this unwinds in Q3/Q4 FY26 as sales to Europe begin.

-

Low ROE: Current ROE is ~6%. This is below the cost of capital. The stock is expensive if growth does not materialize immediately.

-

-

Auditor: Statutory auditor is J.S. Shah & Co. No adverse remarks or qualifications in the report.

13. Related Party Transactions (RPT)

-

Loans: The company has unsecured loans from directors (promoters), which stood at ₹1.11 Lakhs in FY25 (down from ₹265 Lakhs). This shows the promoters are supporting the company with funds when needed, but are now being repaid.

-

Remuneration: As noted, promoter remuneration is rising.

-

Rent: The company pays rent to Aaron Infracon LLP (a related party) for some premises. This is a standard RPT but should be monitored for arm’s length pricing.

14. Competition with China & Risk Factors

-

China Dependency: Sakar has mitigated this risk significantly by setting up its own API manufacturing unit. By making its own oncology APIs (like Imatinib, Bortezomib), it is less reliant on Chinese imports, protecting it from supply chain shocks and price volatility.

-

Competition:

-

Global: Competing with Chinese CDMOs. Sakar’s advantage is “Western Compliance” (EU-GMP) which many low-cost Chinese players lack.

-

Domestic: Competes with Shilpa Medicare, Natco Pharma, and Gland Pharma in the oncology space. However, Sakar is smaller and focused on niche, complex generics where competition is lower than plain vanilla generics.

-

15. Probabilities:

Sakar Healthcare is at a classic inflection point.

-

The Bull Case: The heavy capex cycle is over. The “assets” (EU-GMP plant) are ready, and the “approvals” (EU MAs) are coming in. FY26 and FY27 could see a J-curve in revenues and profits as the new plant utilization goes from near-zero to 40-50%. The Accord deal provides revenue visibility.

-

The Bear Case: Regulatory delays (USFDA/EU inspections) or failure to scale up sales could leave the company with high fixed costs (employee/interest) and a bloated balance sheet, leading to value destruction.

Final View: For an investor, Sakar presents a high-risk, high-reward opportunity in the small-cap pharma space, betting on the successful execution of its European oncology strategy.

Concall (First ever) - Nov 2025

Executive overview: pivot to regulated-market oncology with vertical integration

-

Management positioned Sakar Healthcare as “transition into a research-driven oncology-focused pharmaceutical organization,” using a three-vertical model: CDMO/CMO, own-brand exports, and out-licensing/contract development with tech transfer.

-

Strategic emphasis is on EU-regulated oncology commercialization enabled by the company’s “EU GMP approved oncology unit” and API-to-FDF vertical integration (HPAPI/API + oral solids + sterile liquids + lyophilized injectables).

Assets, capabilities and operating model (what differentiates the platform)

Bavla oncology complex (EU-GMP; integrated API + formulations):

-

Single-shift rated capacities disclosed:

-

97 million tablets/year, 29 million capsules/year, 13 million injection vials/year

-

Lyophilization: “freeze dryers… can manufacture 22,000 and 10,000 vials of… 10 ml each per cycle”

-

-

API block: 12.3 MT/year HPAPI, with “high-containment systems up to OEL level” for cytotoxic handling.

-

Manufacturing technologies called out as part of “green chemistry” / efficiency stack: flow chemistry (VaporTech UK), GI granulation, de-dietrich glass reactors, “stop-loss lyophilization systems”.

-

Bioequivalence: “all bio-equivalent studies are conducted in EMA-USMT approved PROs” and “R&D samples… procured from Europe.”

Changodar unit (legacy platform):

- Continues to run cephalosporin oral solids, DPI, SVP, oral liquids; described as maintaining “high-capacity utilization and export volume.”

Commercial mix shift:

- “own brand export business… now contributes over 70% of total revenues,” which management links to improved profitability and market recognition.

Regulatory progress & pipeline: marketing authorizations (MAs), dossiers, APIs

Oncology product development and filings:

-

“55 oncology products developed in-house.”

-

“32 CTD dossiers developed, ready to register and launch.”

-

“80-plus dossiers have been submitted worldwide.”

-

“11 registrations or marketing authorizations have been granted” (management later details EU split).

Europe MAs—countries and molecules (material disclosure):

-

Europe approvals to date: “five marketing authorizations” in Bulgaria and “one from Bosnia” (total 6).

-

Molecules explicitly named:

-

Docetaxel injection

-

Irinotecan injection

-

Carboplatin injection

-

Gemcitabine lyophilized injection (freeze-dried)

-

Tamoxifen tablets (oral solid)

-

-

EU expansion pathway: approvals are via “national procedure” and can be leveraged via “decentralized procedure to move into the other countries in Europe,” with a “dual effect” from (i) MA multiplication and (ii) filings by “partners in respective countries.”

API regulatory status:

- “written regulatory confirmations for 16 APIs” at WHO-GMP unit; “seven lined up for CEP approval.”

IP signal:

- “The first patent grant has definitely validated… our R&D strength” (no further details provided).

Commercialization mechanics & timelines (how revenue converts after MA)

Near-term EU launch timing:

-

For Bulgaria, management expects first meaningful exports in Q4 FY26: “we are expecting quarter four of this financial year to capture this export to Bulgaria.”

-

They have “received three purchase order” for some of the approved products; “another two are in the pipeline.”

Why the lag exists (operational steps):

-

Post-MA work includes artwork finalization, serialization, partner PO finalization, API procurement, manufacturing, testing and batch release:

-

“serialization… required for the product to move into the European market” (they cite TraceLink for Europe).

-

Typical first-cycle time: “ranging from 90 to 150 days”; subsequent cycles: “90 days lead time” from Sakar.

-

Commercial model choices:

- Two structures: (1) partner holds registration after dossier licensing; (2) Sakar holds registration while sharing dossier—control differs. In most cases, launch sequencing is agreed upfront; only “4%-5% cases” change due to market acceptability/indication dynamics.

Financial performance (Q2 & H1 FY26) and margin bridge

Top-line acceleration:

-

Q2 FY26 revenue: INR 5,756.04 lakh (+34.6% YoY, +9.1% QoQ).

-

H1 FY26 revenue: INR 11,029.66 lakh (+31.4% YoY).

Profitability:

-

Q2 EBITDA: INR 1,135.39 lakh (down 1.3% YoY); EBITDA margin 20% (vs 27% last year).

-

H1 EBITDA: INR 2,405.97 lakh (+8.4% YoY); margin 22% (vs 26%).

-

Q2 PAT: INR 453.98 lakh (vs INR 479.63 lakh).

-

H1 PAT: INR 921.11 lakh (+27.8% YoY).

-

Gross margin: “remained healthy at 46%.”

Drivers of margin compression (management attribution):

-

“operating leverage impact from newly commissioned oncology lines.”

-

One-time / front-loaded cost items:

-

Business development: “extensively traveling… attending the conferences… shoot up… 7, 8 times.”

-

Higher power & fuel linked to domestic production increase.

-

Product registration (filing-related) expenses.

-

Management confidence on recovery:

- “from the third quarter onwards EBITDA will be back on track” and year-end EBITDA expected to revert towards guided levels, as these are “basically one-time expenses.”

Guidance, growth algorithm and execution visibility

FY26 guidance reiterated (aggressive H2 implied):

-

Management reiterated being “on track” for INR 280 crore revenue for FY26 and around ~25% EBITDA margin (discussed vs current margin compression).

-

Implied H2 step-up acknowledged by investors; management explicitly agreed: “Yes, absolutely,” attributing it to:

-

Q4 export commercialization off EU MAs, and

-

Domestic oncology CMO ramp-up as tech transfers complete.

-

Oncology revenue mix and trajectory:

-

H1 FY26 oncology contribution: “around 37%” of sales (vs “full last year… around 19%”).

-

Oncology H1 split: “roughly 50-50” between domestic CMO and exports.

-

Export geographies already served (non-EU): UK, Mauritius, Lebanon, Algeria; includes tender participation via partners.

Order book / contract visibility (material statement):

-

Management cited “50-plus agreements on oncology… covering more than 250 SKUs,” and claimed “potential of more than INR450 crores” from contracted overseas partners.

-

Timeline to execute filings: they expect partners to file remaining dossiers and registrations to mature largely by FY27: “this will be done by next financial year… FY ’27.”

FY27 outlook (directional, not a formal number):

-

Export sales expectation: “will double what we will be doing in FY26” based on MA flow; they also referenced 50%+ overall growth for FY27 over FY26.

-

MA expectation framing: while ~250 dossiers planned, management uses a conservative lens—“considering… 100 marketing authorization… taking a simply 20% deduction” (statement is internally inconsistent but indicates discounting/derisking of approval conversion).

Longer-term capacity monetization:

-

At full utilization of oncology plant (single shift), revenue potential: “around INR 1,000 crores” (product-mix dependent).

-

Time horizon: “roughly around FY '30” to reach that scale, contingent on “250 to 300 full-fledged marketing authorization.”

Balance sheet, capex status, and working capital

-

Assets (Sep 2025): INR 44,859.78 lakh (vs INR 41,526.10 lakh Mar 2025).

-

Net worth: INR 30,325.29 lakh (vs INR 28,547.59 lakh).

-

Leverage: debt-to-equity 0.38.

Capex and CWIP clarity:

-

CWIP discussed at ~INR 17 crore; management said this includes oncology-side expansions/modifications (not just maintenance).

-

Cash flow capex referenced as INR 27 crore, which “includes the capital work in progress of INR 17 crores”; of this, “around INR10 crores” already captured, “INR17 crores will be taken care of in the next six months.”

-

Forward capex: “do not foresee any further capex… except… maintenance” in FY27.

Working capital improvement:

-

Working capital cycle reduced from 165 days (Mar) to 135 days, driven largely by inventory normalization: prior WC elevated due to “finished good stock based on the orders” executed in FY26.

-

Management sees current level as “an ideal number,” with intent to drive further efficiencies.

People/leadership and cost structure

-

Headcount and employee cost: management indicated staffing is at “optimum” for projected scale; no material ramp expected unless technical needs arise.

-

New senior hires: “Except the finance person, the rest were there.”

-

Employee cost impact: “Majority of the expenses have been captured” and should remain similar; being fixed, it should deleverage as sales scale.

Key watch-items / risks explicitly evidenced in call

-

Execution lag risk: MA-to-revenue depends on artwork/serialization/testing and partner readiness; first-cycle can take 90–150 days.

-

Margin volatility near-term: heavy BD travel + registration expenses + ramp inefficiencies from new oncology lines temporarily depressed EBITDA to 20% in Q2.

-

Guidance dependency on Q4: FY26 guidance relies on meaningful Q4 EU commercialization plus domestic CMO ramp; any slippage could affect the back-ended revenue profile.

Newsworthy takeaways (most actionable)

-

Six European MAs (Bulgaria x5 + Bosnia x1) with explicit molecules (docetaxel, irinotecan, carboplatin, gemcitabine lyo, tamoxifen).

-

Commercial exports to Bulgaria expected in Q4 FY26, with three POs already received.

-

Oncology now 37% of H1 FY26 sales (vs 19% last year), split ~50/50 domestic vs export.

-

Management claims 50+ oncology agreements / 250+ SKUs and “potential of more than INR450 crores” from these contracts.

-

Capex largely concluding: INR 27 crore cited (incl. INR 17 crore CWIP), and no major FY27 capex expected beyond maintenance.

-

Clear long-term ambition: ~INR 1,000 crore oncology revenue potential at full utilization, targeted around FY30, predicated on 250–300 MAs.

Disclosure:

Compiled Notes from here & there, No Buy/Sell Recommendation

===========================================================================

4 Likes