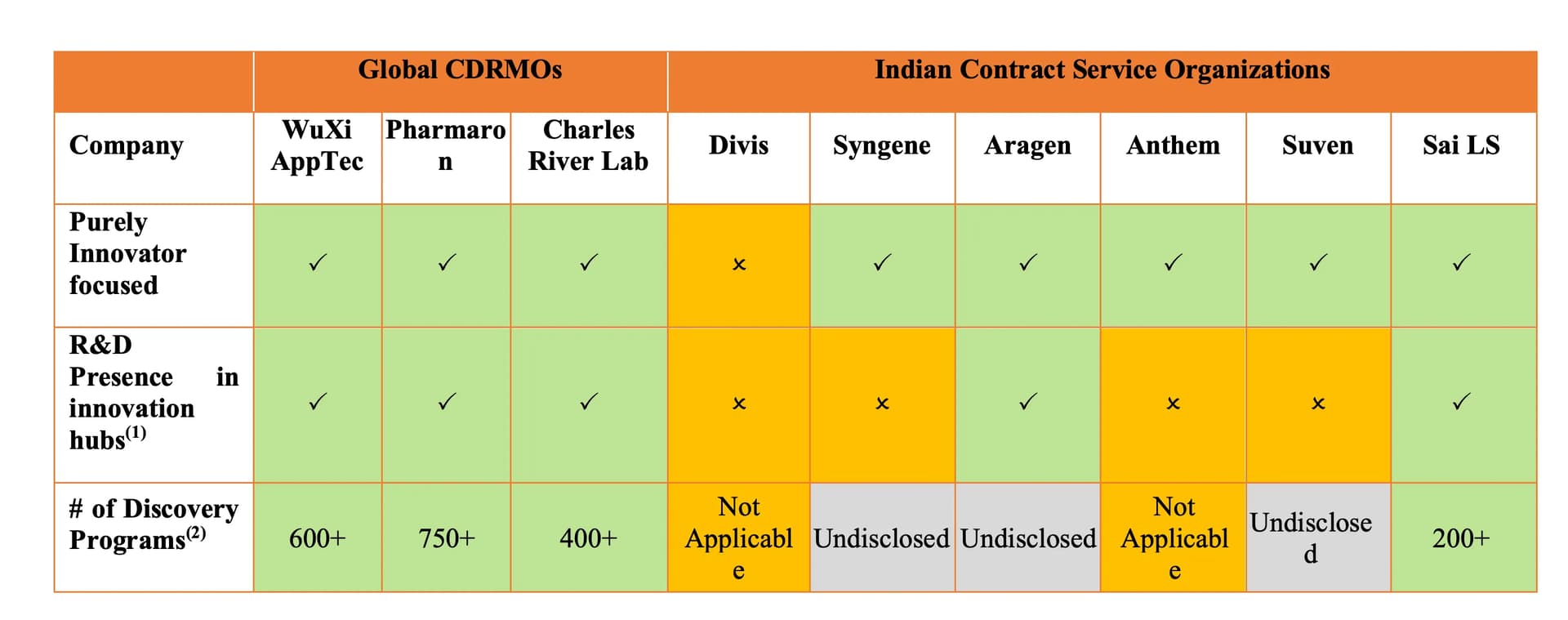

Sai Life (incorporated 1999. Managed by Krishna Kanumuri who is MD/CEO since 2004) is a small molecule focused CRDMO - i.e they do both CRO and CDMO. CRO contributes 37% to revenues while CDMO contributes 63%. Only comparable competition is Syngene in the listed space and to a small extent Anthem Bio which has around 10% CRO. Comparison with Syngene should be a put-off for many considering how poorly Syngene has grown its business over the last few years. Sai however, has grown even its CRO business 35% over the last 5 years with 38% of CRO from BigPharma (up from 33% in FY24) and 62% from Biotechs.They have increased number of Customers and have also increased wallet-share from existing ones (cross-selling and upselling).

Sai has 18 out of the top 25 (was 9 in 2019) BigPharma names as their clients - names like AbbVie, Lilly, Bristol Myers Squibb, Pfizer, Merck, GSK, Genentech/Roche, AstraZeneca, Sanofi etc (they have MSAs with 8 of these) as customers who all have multiple molecules with Sai. They also have a dedicated CRO facility likely for Schrodinger. Sai has 30 commercial molecules (7 of these are blockbusters) and has in fact taken 5 drugs from discovery to commercial which has to be the most for any Indian CRDMO. There are 6 in phase-3/pre-reg phase. The molecules are across therapies from CNS, Oncology, Infectious diseases, Cardiovascular, Anti-histamine etc.

Discovery phase lasts until the IND filing (Investigational New Drug). Only post IND filing the trials can start and the drug goes through Phase 1-3 and NDA filing. Sai is there in the entire value-chain from Discovery to Commercial.

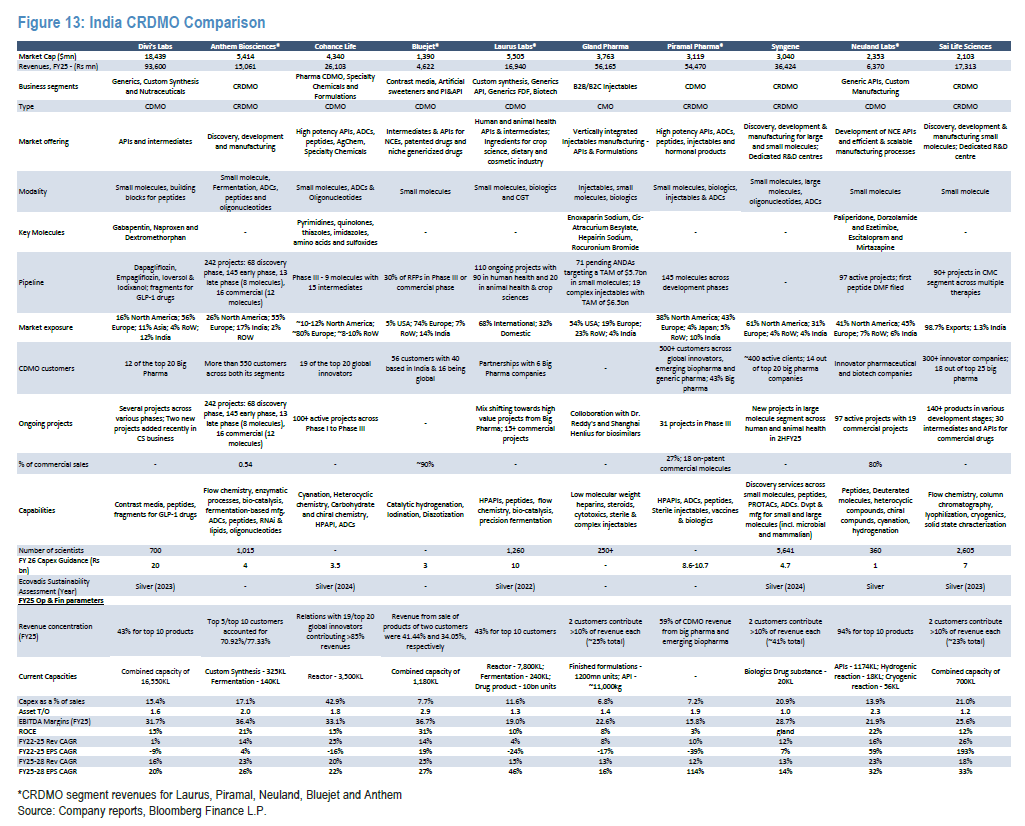

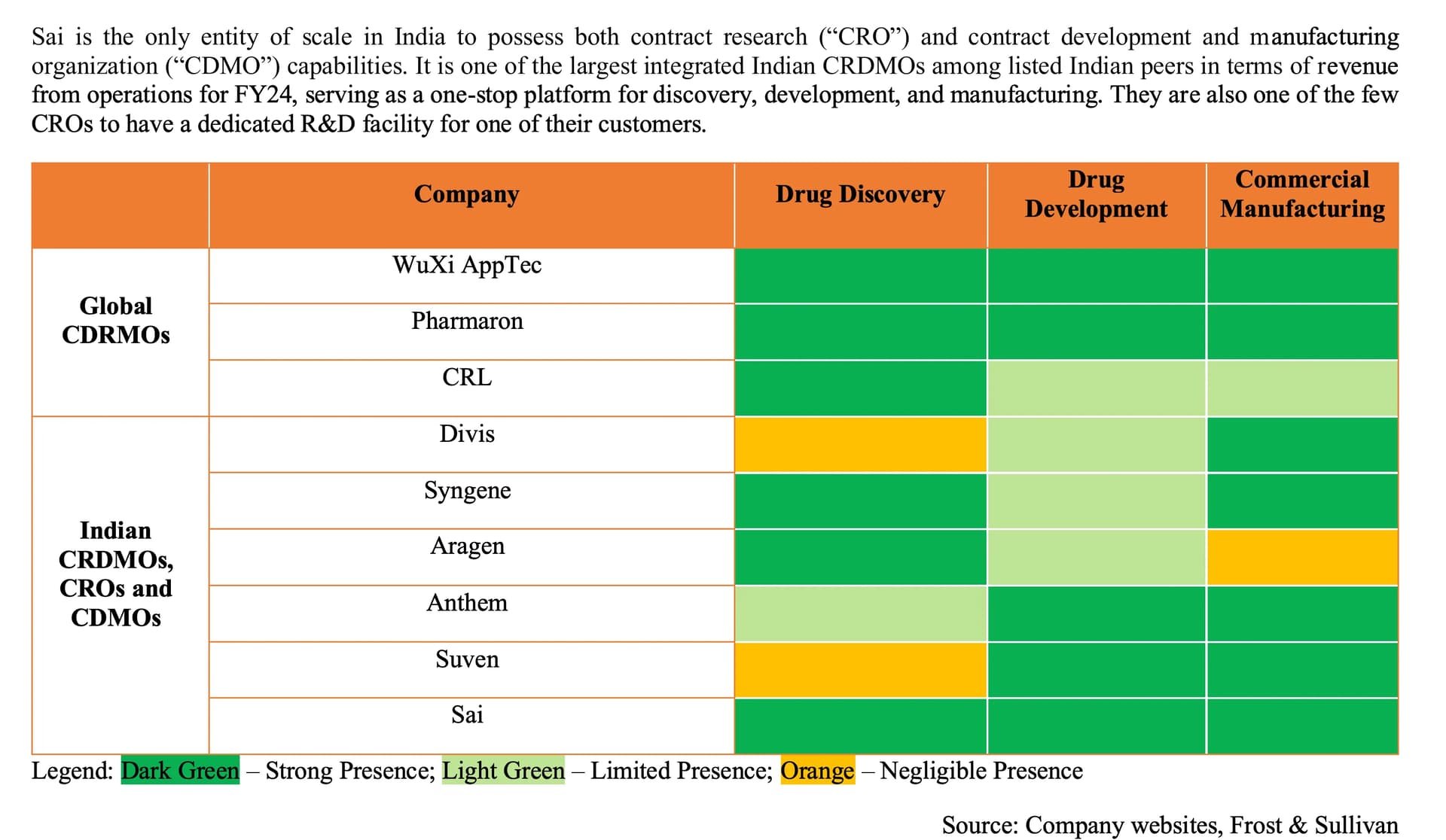

Sai and Aragen are the only ones that work with innovators with labs in innovation hubs in the West (Sai has labs in Watertown and Boston to work alongside innovators)

The only one in India that is comparable to a WuXi/Pharmaron and probably only one in India deriving almost all its revenue from innovators.

I have been studying the CDMO space over the last few months - so far I have covered BlueJet, Aarti, Neuland, Sai, Laurus and Anthem in some depth. All of them have at least 1 commercial innovator molecule contributing substantially to their sales. This is a new thing for Indian CDMOs and we might probably be in the very, very early phase of it - there is scope for exponential growth for many of them here. Among this peer set, each of them (maybe with the exception of Anthem) has a substantial part of the business in something I don’t like - Aarti with its xanthene/caffeine, BlueJet with its contrast media/saccharin, Neuland with its extensive generic APIs where there’s lot of pricing pressure and Laurus with its ARV portfolio.

What distinguishes Sai among this peer set is that there’s barely any such commodity drag. Its all high science (2605/3401 employees are scientists with 1572 in R&D alone), high margin, high value add in cutting-edge - from chiral chemistry, cell and gene therapies (CGT), targeted protein degradation (TGT), ADC linkers, peptides and oligonucleotides. The overall margins however pale in comparison to a Divis, Anthem etc - this however I think is changing. Sai’s margin trajectory is trending up and there are signs that it can continue as CDMO volumes from its existing molecules go up.

The other thing that I like about Sai is that they have a ready funnel for CDMO business from the CRO FDA approved molecules, unlike the others I studied - which seem to involve an element of luck in capturing large business.

So far among the peer set, the largest innovator molecules are (that I could triage).

| CDMO | Commercial Innovator Molecules |

|---|---|

| BlueJet | Bempedoic Acid |

| Neuland | Bempedoic Acid, Cobenfy, Austedo, Qelbree (yet to contribute) |

| Aarti Pharma | Elinzanetant, Obicetrapib (yet to contribute) |

| Anthem | Rimegepant ($50m ~25% of sales!) |

| Laurus | Suzetrigine, Abrocitinib, Sepiapterin, Mevrometostat (phase 3) |

| Sai Life | Atogepant/Ubrogepant (Qulipta/Ubrelvy), Blujepa, Tyvaso DPI, Bilastine, Orladeyo, Simparica, Phase 3 completed - Tradipitant, Lorundrostat, Camizestrant |

To me it looks like Sai has all the makings of a business that can become quite large due to its earnings power. They have 160 programs in their CDMO pipeline which gives them the healthiest business visibility among its peers. A lot of Sai’s molecules have fairly large market size as well.

Atogepant/Ubrogepant (Qulipta/Ubrelvy) is an Abbvie drug approved in Sept ‘21 (Patent expiry in 2041) used in migraine prevention and treatment respectively. Its taken every day (60mg dosage) and competition is another recently approved drug - Rimegepant (made by Anthem and Piramal - both have ~$50m in sales per year from this molecule alone). As of now Sai is making a crucial intermediate and the API supplier is WuXi. Sai is probably capturing ~50-60% of the value but is the sole supplier - crazy scale up as well from $4.2m in ‘23, $5.8m in ‘24 to $15.8m in ‘25 so far. Good thing is Atogepant/Ubrogepant are notably superior to Rimegepant in terms of MMD (Monthly Migraine Days) and also cheaper and the same is also reflected in way superior prescription growth (latest UK data). The market size is ~40m patients in the US and another 40m in EU.

Blujepa (Gepotidacin) is a GSK antibiotic drug for uUTI approved only in March ‘25 (patents till 2035) - market size is ~15M patients for UTI in US alone and much larger worldwide - also this appears to be a recurring phenomenon with multiple infections every year. Since Gepotidacin is a first-in-class antibiotic, it might be reserved for treatment of only resistant cases by antibiotic stewardship. Even resistant cases appear to be 5% of the market. The dosage as well is high at 3000mg/day for 5 days. The trend of resistance is increasing and by 2030, it could be 10% of overall market and could end up being prescribed more widely as well. The drug is yet to be approved in EU but it should get approved this year which will increase market size. Sai makes two intermediates and it contributes ~$17m in exports this year.

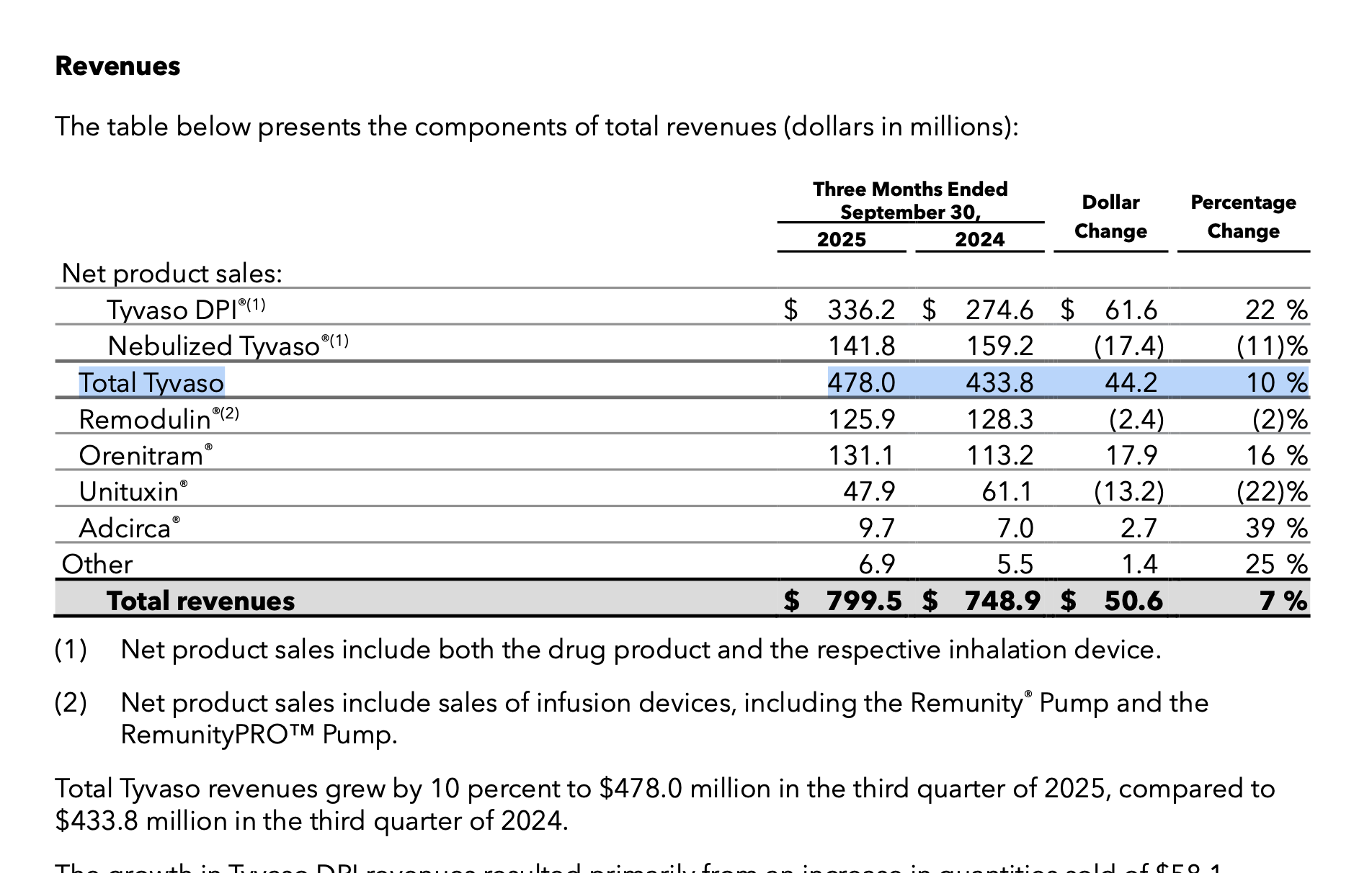

Treprostinil (Remodulin; Tyvaso; Orenitram) by United Therapeutics has been in the market for a long time but recently the DPI (Dry Powder Inhaler) got approved and its driving up the numbers for Sai that makes a crucial intermediate. This is ~$70k/kg intermediate. Sai makes ~$8m/yr but its scaling up. Patent expiry is May ‘27.

Bilastine by Faes Farma was approved sometime ago in Europe and isn’t approved in US. It is used for treating allergic rhinitis (seasonal allergies) and is a widely used product in Europe as Bilaxten. Patents have been expiring across countries over last 3 years but the product is holding its own with Sai making $16m/yr (no growth though)

Orladeyo (Biocryst) and Simparica (Zeotis) are commercial drugs Sai was making until ‘22/’23 or so but stopped likely due to scale up issues (my guess). Simparica (chewable flea/tick treatment for dogs) esp is a very, very large market and was growing exponentially when it stopped abruptly. I suspect inability to scale-up is what made them lose these molecules. If you track their capacity expansion - its 200 KL in 2017, 450 KL in 2020 and 565 KL by 2022. After this, they added capacity only in ‘25 (110 KL to take it to ~640 KL). FY23 their borrowings had ballooned to 900 Cr+ and interest coverage ratio as well dipped to a dangerous ~2x. This must have put the brakes on their expansion and made them lose customers who needed serious expansion fast (esp. Zoetis). Again all this is my hypothesising. The IPO has substantially brought down the debt and now and the company is expanding capacity again to 1300 KL by 2027 likely due to scale up of Atogepant/Ubrogepant, Blujepa and the phase 3 molecules which are nearly commercialisation.

While management says there are 6 in phase-3/IND, I could only locate 3 of these.

Lorundrostat (Mineralys) is a drug for treatment resistive hypertension. Market size is rather large here at 11-17% of hypertensive having treatment resistance which puts market size at 13-20m patients in US alone. There is another drug which is also in phase 3 by AstraZeneca called Baxdrostat which is also has phase 3 success. Both drugs will likely get to NDA filing in Dec ‘25.

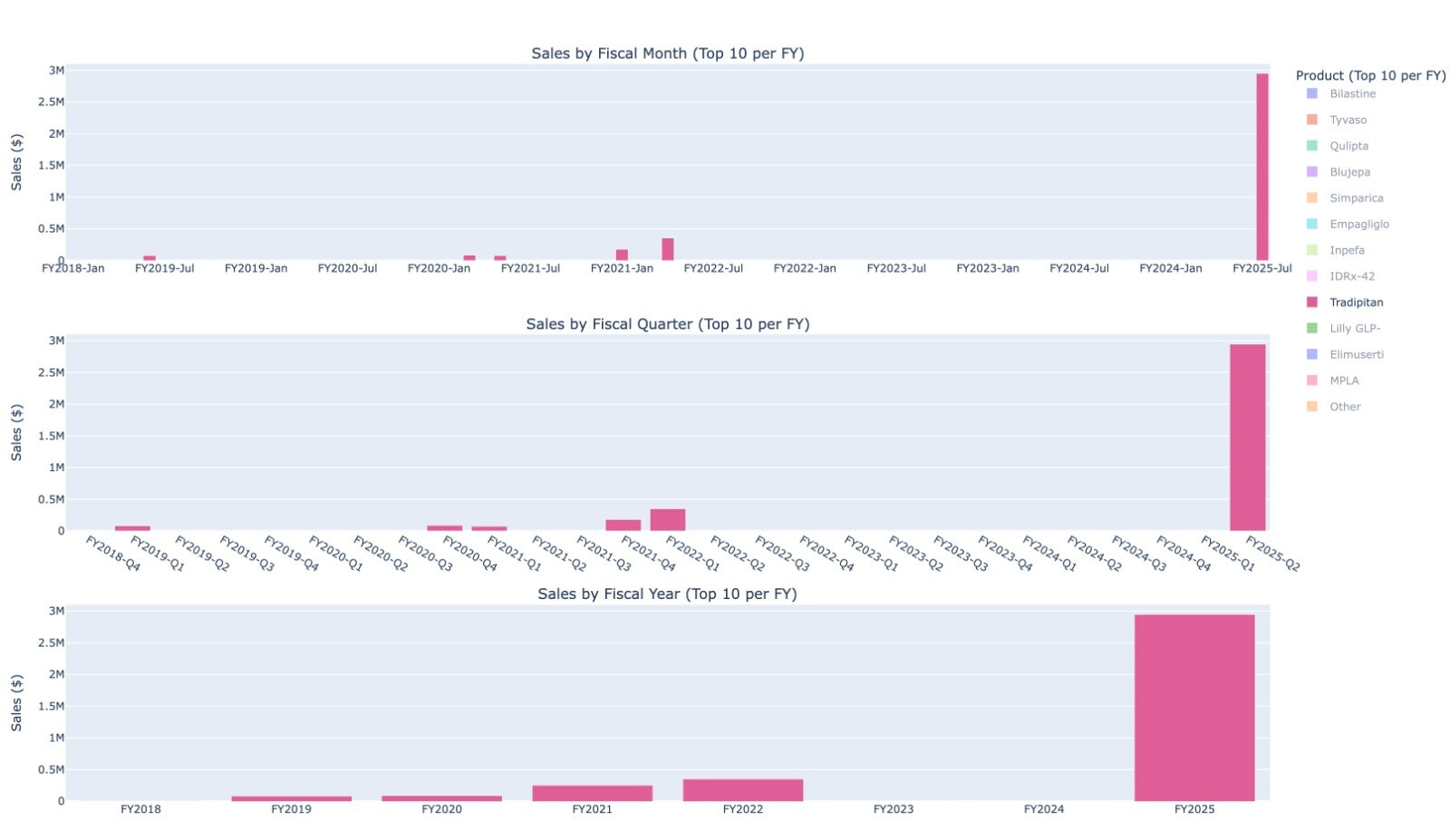

Tradipitant by Vanda Therapeutics is a motion sickness drug which has been filed for FDA approval and should get approved by Dec ‘25. There’s no other approved NK1 for motion sickness and this will be a first-in-class drug.

Camizestrant is a breast cancer drug by AstraZeneca and phase 3 readouts are very positive. Not sure when the phase 3 will complete but it should be in the near future but commercial supplies possibly not before 2027 I think.

Manufacturing Units

Unit II, Hyderabad - Houses the R&D campus for Discovery R&D and for CMC process development.

Unit III, Bollaram - Intermediates for early-stage programs

Unit IV, Bidar - This is the primary manufacturing facility which currently has ~640 KL capacity and will be expanded to 1200-1300 KL by 2027. This facility is FDA approved and has had inspections last year.

Unit VI, Bidar - Oncology unit with HPAPI block (for ADC linkers)

Watertown, Boston, MA - Exploratory Biology Lab

Manchester, UK - Process Chemistry CoE

Valuation

Valuation isn’t cheap at 75x trailing. I think its perhaps 50-60x FY26E. I feel its most comparable to Laurus but Laurus has nearly 50% coming from ARV and generics alone unlike Sai which has a much higher quality earnings. At 18k Cr mcap vs Laurus 48k Cr mcap, I think Sai is very undervalued relatively. Another 47k Cr mcap company like Anthem has 25% revenues coming from Rimegepant alone (Rimegepant is split between Piramal/Anthem while Sai is sole supplier for Ato/Ubro. But lower value capture through intermediate might make it comparable). Sai can very easily do similar numbers with Atogepant/Ubrogepant and in addition to it has several other molecules - I feel Sai is comparable to Laurus/Anthem in terms of value. No one else has a funnel like Sai and I think if they manage their Process R&D and capacity expansions better, can grow for a prolonged period of time easily compared to peers.

Risks

- Sai has lost two crucial molecules in '23. If it was for other reasons than capacity constraints, it might be a reason to worry. Losing late-stage/commercial molecules from CRO/CDMO is the biggest risk

- Valuation isn’t filthy cheap. TPG recently sold 15% of the company at ~875/share. It is amazing that 15% of the company got absorbed though (knowing how BlueJet was struggling to offload).But do I really know more than TPG bothers me a lot.

- While the client concentration is reducing every year, it is inevitable that something like the *gepants grow and overshadow the rest increasing concentration risk. Its a good problem to have though, like Anthem’s Rimegepant

Disc: Invested and have recent transactions. I am a novice who is studying this sector and am bound to have made lot of erratic assumptions. Please do your own research