"Setting appropriate compensation falls squarely on the shoulders of outside directors, specifically those who serve on the compensation committee. Management may propose some outlandish scheme that inappropriately rewards executives far beyond reason.

Moreover, in addition to its misguided stock-based compensation based solely on stock price appreciation, its annual cash incentive program (AIP) left much to be desired. Rather than basing this payout on certain reliable, audited GAAP-based results, Valeant used two non-GAAP metrics—adjusted earnings and adjusted revenue.

The compensation plan at Valeant was irreparably flawed in two fundamental ways: (1) it was based solely on stock price appreciation and unreliable non-GAAP metrics, and (2) its excessive pay for extreme TSR growth encouraged reckless management behavior.

When evaluating outside directors, investors must always ask whose interests they are favoring—management’s or investors’. Investors should also always question compensation plans that could easily be abused to improperly inflate executives’ wallets." ~ An extract from the book Financial Shenanigans by Howard Schilit

Non-GAAP metrics used by Sai Life to decide the incentive plan:

Please raise this query in the next earnings call. What’s the rationale for this incentive plan? I haven’t had the time to look but there have been appointment and removal of Board of Directors in the Nomination & Remuneration Committee just before the compensation plan was changed.

An unbridled passion for being a joy kill and some spare time after concluding on Deep Industries, brought me to Sai Life Sciences.

I became interested in Sai Life Sciences because it ticked all of my checkboxes:

Pharmaceutical - Check

Acquisitions - Check

Impairment - Check

Complex Revenue Recognition - Check

But mainly the pharmaceutical part.

In the series of posts that will follow, I will look to uncover, with the help of forum members, some of the most complex financial transactions that I have seen that warrant heightened investor attention because it involves significant management judgement that directly affects the very growth which is the investment thesis for this company.

For starters, Refer to Key Audit Matter 1 & 2 mentioned in the audit report of the Standalone Financial Statements read with their respective financial statements. Plus go through the revenue recognition policy of the company.

The posts that will follow will not be an investment recommendation (definitely not a buy one :)) rather a combined effort of the forum members and myself to try to understand the company’s balance sheet in a better way.

The first post would either be on Share Based Compensation or Investment Impairment as per Key Audit Matter 2.

The above is a list of FDA approved molecules in 2025. Total 41 approved drugs of which 30 are small molecules (~70%). 7 are mAbs (Monoclonal Antibodies). 2 ADCs and 2 Oligos. A overwhelming majority are still small molecules. The highlighted rows are where Indian CDMOs are involved (Blue - Sai, Red - Laurus, Orange - Aarti). Its fantastic that 6/41 drugs are with Indian CDMOs (its likely DCAL/Cohance might be involved in Dxd used in Datroway as well making it 7/41). Also nice that Sai is involved in 10% of all small molecules approved this year which is a pretty good market share.

Tryptr contribution for Sai might be low since its a eye drop and these are typically at very high dilution and might have very little api. Lilly’s Inluriyo could be a $1b+ drug but not sure how much Sai can make in it since its likely to be a small market volume-wise. Blujepa though could be quite big as I had guessed in earlier posts. Ekterly (sebetralstat) is a drug similar to Orladeyo (berotralstat) that Sai makes but Ekterly is for acute while Orladeyo is for prevention (chronic), so Orladeyo could be a better placed drug. What might round off the year nicely for Sai is if Tradipitant which has a PDUFA date of Dec 30, 2025 gets approval as well taking the count to 4.

Disc: Invested

Update: 31/12/2025: Tradipitant has got FDA approval. The drug also did very well in GLP-1 study for preventing nausea phase-2 trial reported last month (approval is for motion sickness and also gastroperesis. first drug in 40 yrs for motion sickness). It could get a label expansion post phase-3 for GLP-1 nausea reduction and can ride the GLP-1 tailwind as well (interestingly, this is a Eli Lilly drug that Vanda had acquired). This takes count of approved molecules for Sai to 4 in 2025 (13% of small molecules approved this year)

I have been following this zoetis molecule in some depth from the time I started this thread.

It looks like this molecule is now back but in a better form. Earlier what sai was making was 1-3,5-DICHLORO-4-FLUOROPHENYL-2,2,2-TRIFLUOROETHANONE CF3 KETONE which was $380/kg. This month their export to zoetis is TERT BUTYL 5-ACETYL-3 H-SPIROAZETIDINE-3,1-ISOBENZOFURAN-1-CARBOXYLATE which is another intermediate used in simparica (unrelated to the CF3 ketone - this is another more complex half of the final molecule) and this one happens to be ~$1850/kg and almost $2m in Jan.

Based on stoichiometry and mol wts, it looks to me like both these will be needed in 1:1 ratio and the CF3 ketone was already a 17k kg per year back in fy23. If they end up making the Spiro intermediate of around similar 17k kgs, this is likely to be a ~300+ Cr business for Sai. This capex now makes better sense.

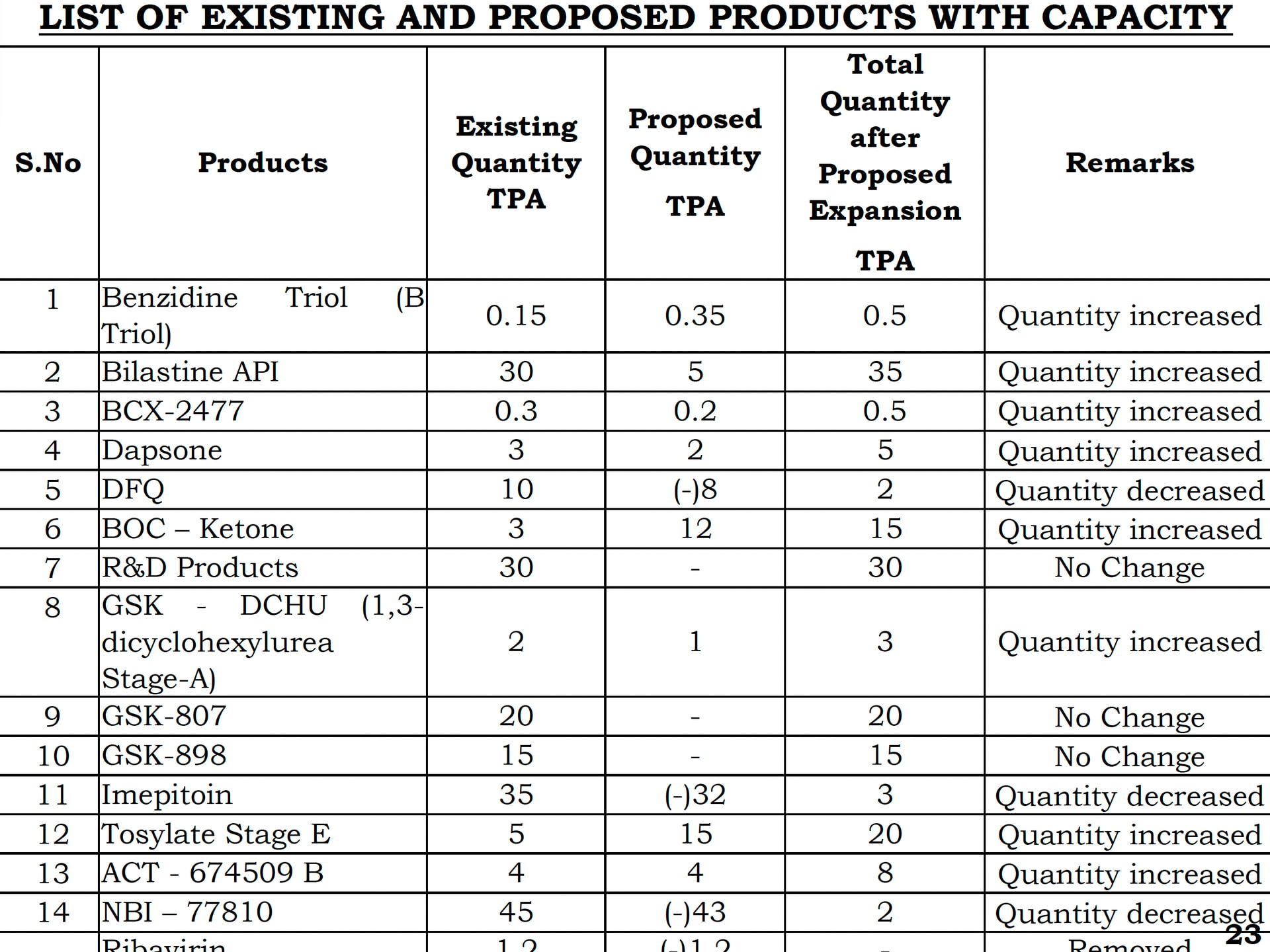

Bilastine which I was worried about would decline is actually marginally going up in volume

Benzidine Triol (Treprostinil - Tyvaso) as well is up in volume. High value, low vol

BCX-2477 is intermediate for forodesine (orphan drug). High value, low vol

BOC - Ketone happens to be the high-value simparica intermediate mentioned in last post. As I was guessing, the capacity for this proposed to be 15 TPA (~250 Cr value)

No change in #9 and #10 which are Bluejepa intermediates. Current volume indicates revenue potential of ~500 Cr from Blujepa alone

Tosylate Stage E appears to be intermediate for Bilastine. Nothing to be excited about

ACT-674509B is Ponvory (for multiple sclerosis) - Currently owned by Vanda. Realisation ~$400/kg

NBI - 77810 big reduction. This is Orilissa. No shipments since June ‘20. So no likely impact

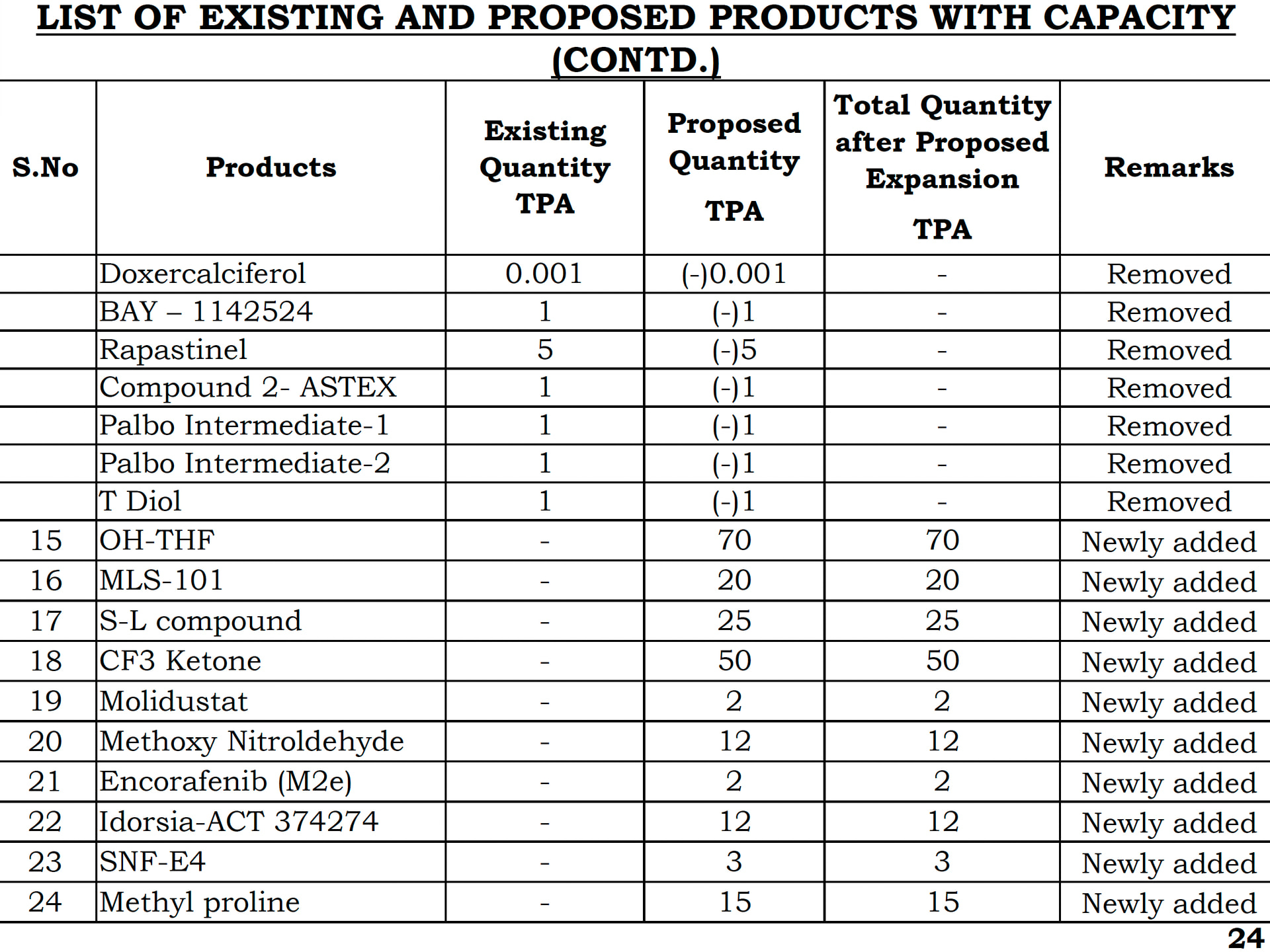

OH-THF is S-3-Hydroxytetrahydrofuran likely used in Empagliflozin. Nothing exciting. Not very high value (~190/kg)

MLS-101 is Lorundrostat - Pretty big molecule (Company filed NDA earlier this month). Could be ~$20m for Sai (~$1100/kg drug)

S-L Compound is likely spiro-lactam and is Atogepant/Ubrogepant (Qulipta/Ubrelvy). This is $3500/kg molecule. Likely potential here is $87m (~750-800 Cr)

CF3 Ketone is Simparica earlier intermediate which stopped in FY23. Even this is back and big. 50 TPA is 3x their FY23 volume of ~17T. Could be ~$20m

Idorsia ACT374274 is Quviviq for migraines. This is big potential drug. ~$13m potential (~120 Cr). This drug is scaling up very well as per public data

BCX-6494 and BCX-7611 is Orladeyo. Latter is ~$7150/kg. So even 2.5 TPA is $18m (~160 Cr)

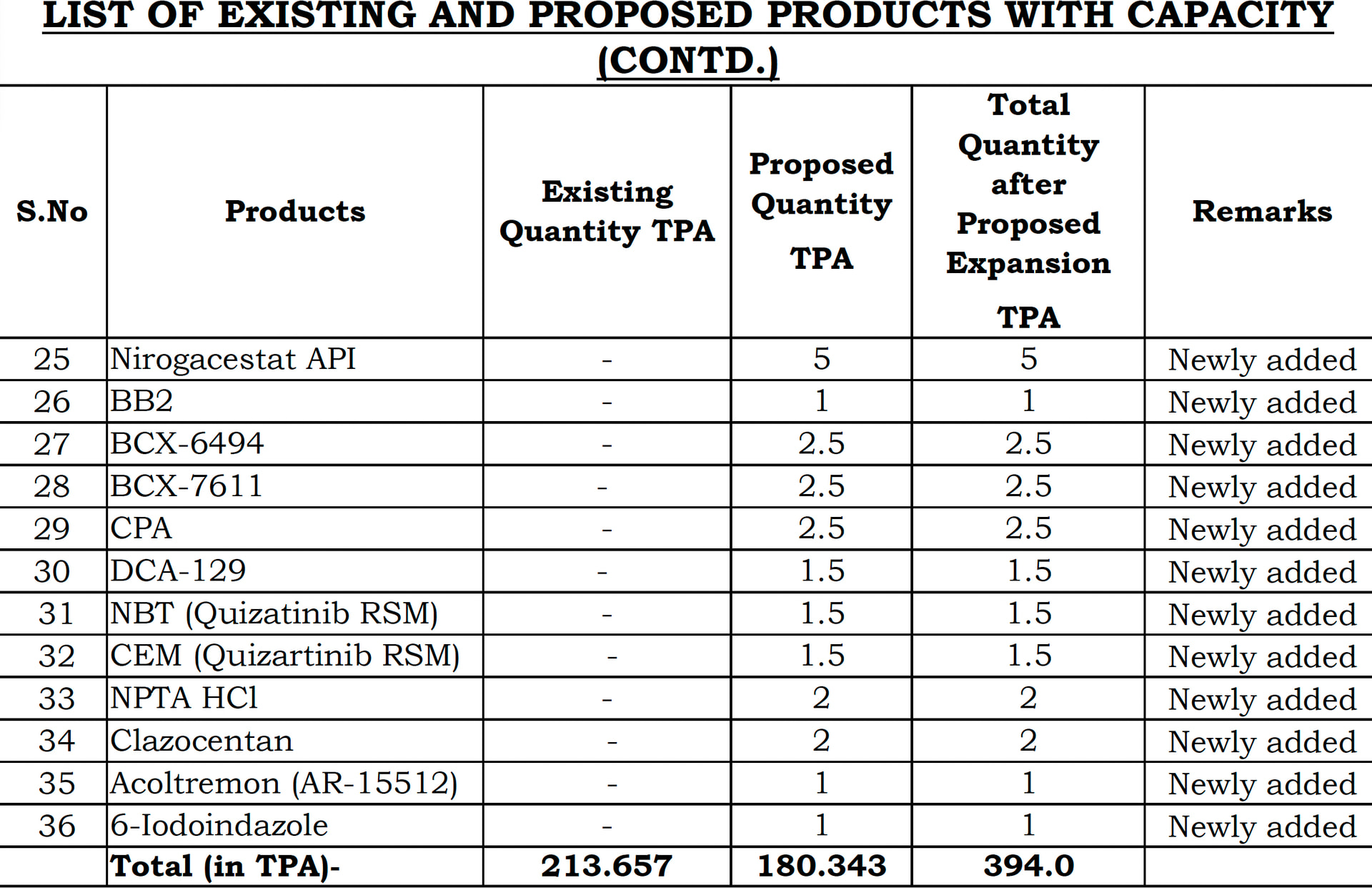

Rest are mostly much smaller so ignoring them. Overall capacity is going up from 213 TPA to 394 TPA. There is pretty good visibility from this capex of ~3000 Cr+ in revenue. Current CDMO revenue is only ~1350 Cr so the expansion I think can help them double revenue in the next 2-3 yrs.

Disc: Invested. No recent transactions. I am a novice and just putting out info I am finding with my own interpritations. I am likely to be wrong. These are complex businesses where lot of things can go wrong and these capacities are just notional indicators of where the company is heading

Here are the key takeaways from the discussion on the CDMO (contract development and manufacturing organisation) space.

Revenue and lumpy growth

CDMO revenue mix: There are two streams – commercial stage molecules and clinical phase molecules; clinical revenues are highly cyclical and volatile.

Quarterly vs annual view: Even for commercial molecules, numbers should be judged on yearly performance, not quarter-on-quarter, because of inherent lumpiness.

Company-specific impact: Some firms are doing well while others are weak; the current correction in CDMO stocks (40–70% from 52‑week highs) is not an industry-wide structural issue but more company-specific.

Drivers of guidance cuts and growth

Growth visibility: Guidance cuts by some companies are linked to molecule uptake and vendor diversification (how many suppliers a pharma innovator uses and how volumes are shared).

Partner de-risking: Innovators are adding additional vendors to de-risk supply chains, which influences revenue distribution and growth for any single CDMO.

Inventory destocking: Inventory stocking/destocking happens across the industry depending on launch quantities, achieved market share, and sell-out; it is part of the normal cycle, not necessarily a structural problem.

Tactical vs strategic supplier shift

From tactical to strategic: Indian CDMOs are transitioning from being “tactical” suppliers (one or two big molecules with outsized impact) to “strategic” partners with a broad molecule and technology base.

Diversified portfolio: Once a CDMO becomes a strategic supplier with a wider portfolio, quarterly swings remain but become less extreme; the key is breadth across commercial and development pipelines.

Product concentration risk: Current volatility is more a product-concentration issue than an inventory issue; firms with too much dependence on a few molecules see sharper swings.

Long-term outlook and cycle

Multi-year growth cycle: Industry veterans see Indian CDMOs in the early phase of a multi-year (5–10 year) growth cycle, not yet in the “reaping” phase.

Investment phase: To become true strategic partners, CDMOs must invest in a broad range of technologies and capacities; markets may be misjudging this investment phase as a period of underperformance.

Time horizon: This is described as a 10–15 year relationship-building journey; short 1–2 year snapshots or one-off events like specific US acts should not drive the full thesis.

Geopolitics, China, and the Biosecure Act

Biosecure Act: The US Biosecure Act is now seen as “immaterial” or largely noise; the bigger themes are global diversification and geopolitics.

China risk: Customers cannot keep 80% of their supply chain in China, which is a strategic competitor; geographic diversification of suppliers is “here to stay,” structurally benefiting India.

RFPs vs real business

RFPs overplayed: RFP (request for proposal) numbers are being overemphasised by the market; many RFPs are exploratory and not serious business leads.

Relationship-led conversion: Serious RFPs and sustainable business come from deep customer relationships and strategic partnerships, not one-off bid processes.

Metrics to track: Investors should focus on strategic pipeline quality, customer base, and breadth of technologies rather than headline RFP values as “predictive metrics.”

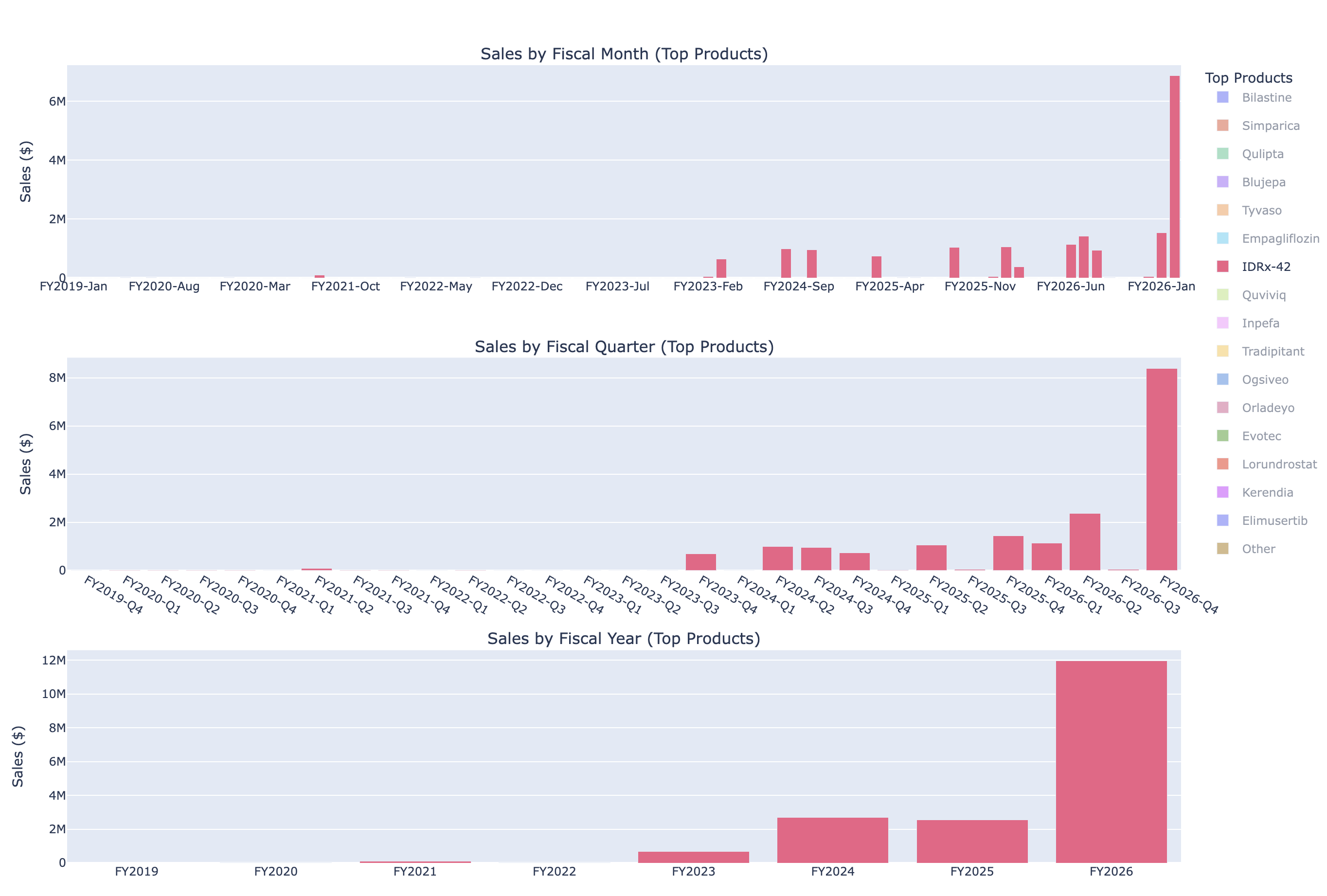

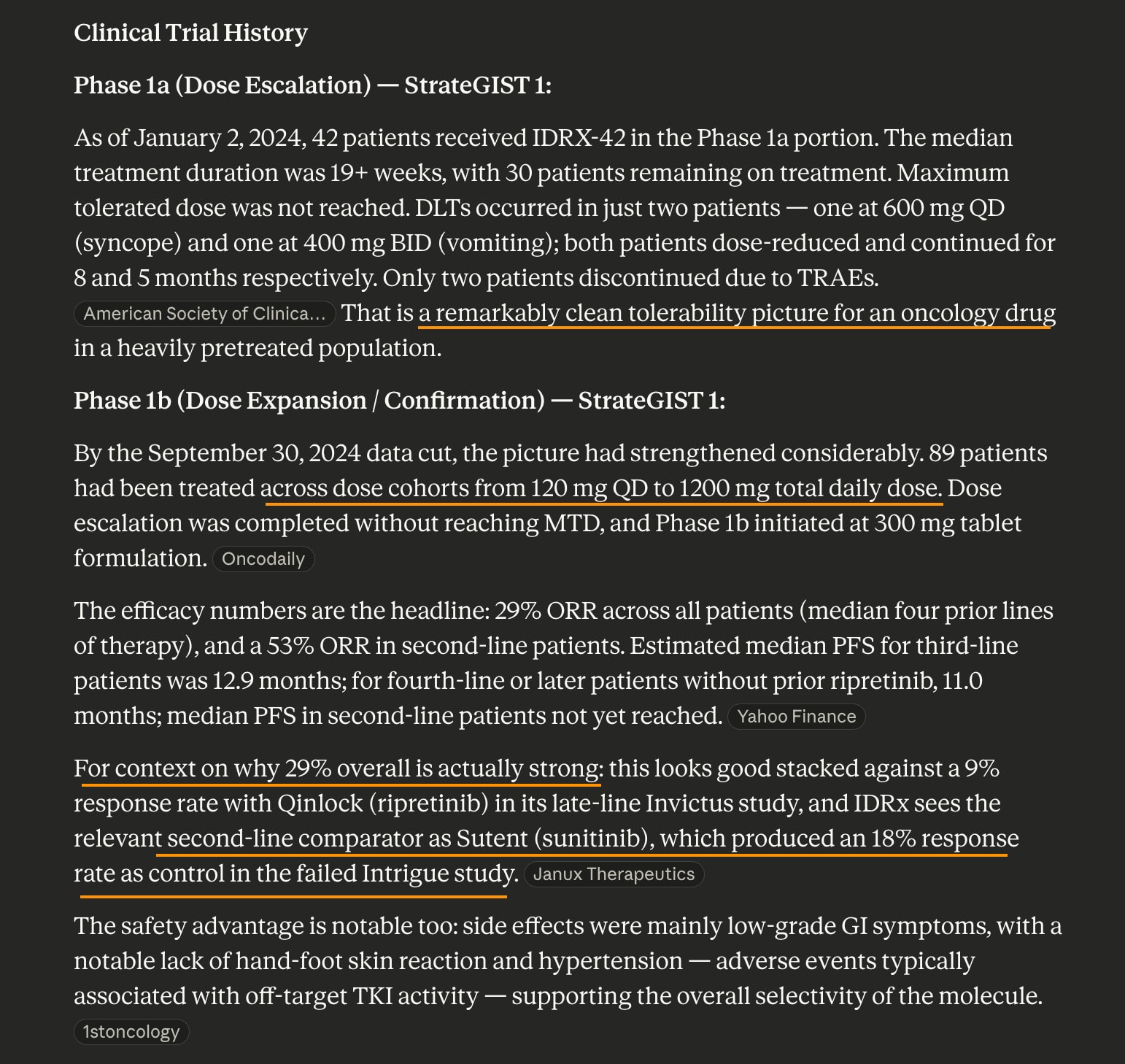

Feb exports have decent contribution from N-4-1-METHYL-1H-PYRAZOL-4-YL-BENZYL]-6-7-3-PYRROLIDIN-1-YL-PROPOXY-IMIDAZO1,2-APYRIDIN-3-YL [N-1] which is N-1 (one step to final API) for GSK’s IDRx-42 and another intermediate for same drug.

The scale up is phenomenal at $8.4m in Q4 (almost equal to Qulipta in value in Q4 so far) for a drug which is just in phase 3 mainly because, though its just ~120 kgs, its ~$55k/kg (second intermediate as well is ~$10k/kg). This seems to be another big future potential contributor, so I dug in to see what drug it is, whats the market size, competitor, odds of approval etc.

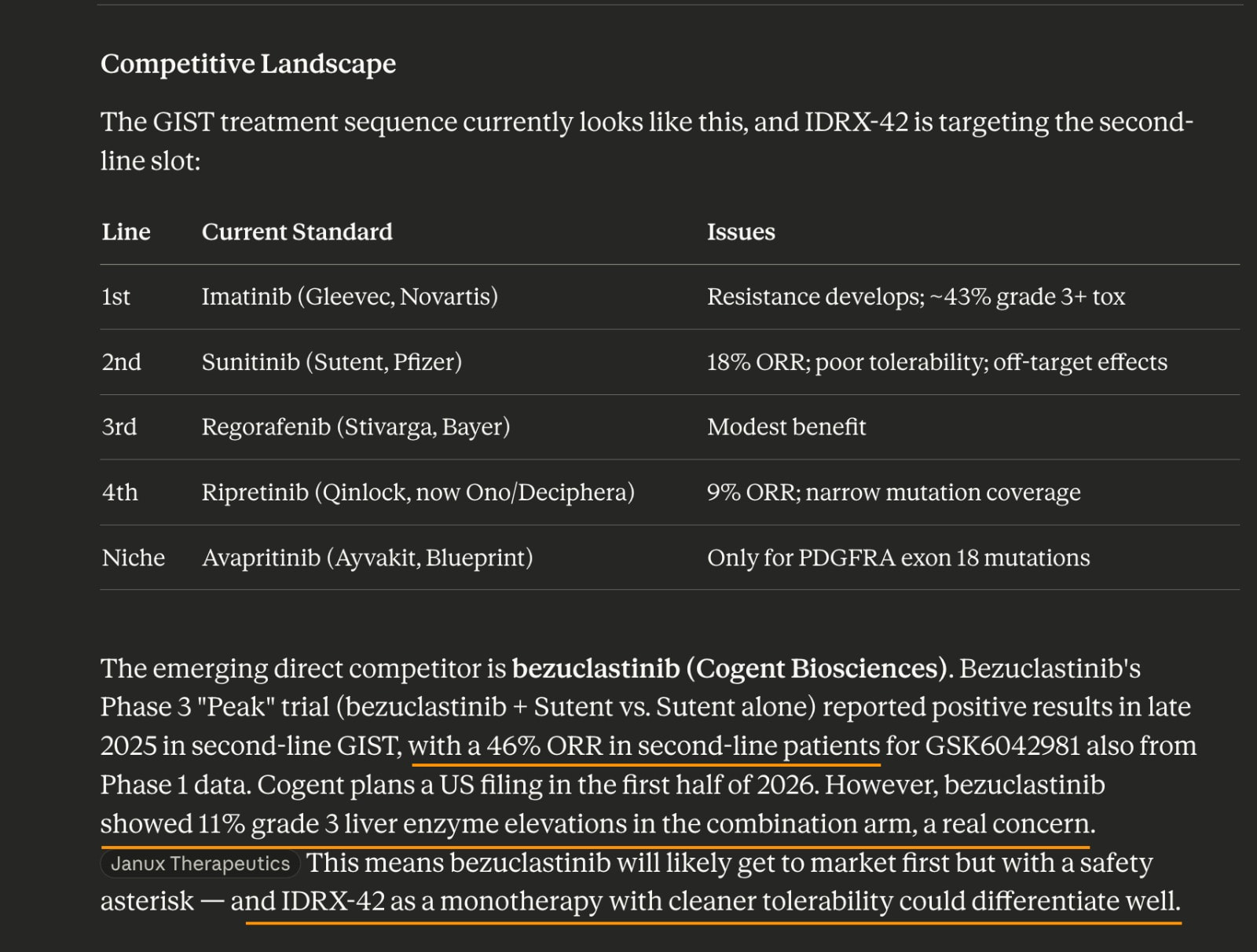

It is used to treat cancers in the digestive tract where about 80% are driven by KIT-gene mutations and the disease is treated sequentially with TKI drugs with imatinib first-line (generic version of this is made by Sakar for European markets), then sunitinib, then regorafenib, then ripretinib. Turns out patients accumulate resistances as they are passed from one line of defence to another. IDRx-42 appears to be very selective in targeting KIT-mutations.

Sai seems to be building a base of several high-complexity/high-value small volume molecules which will act as a good robust revenue base that will protect it from big drawdowns in sales if there is destocking in any of top molecules.

You, Sir, are imparting invaluable, practical lessons on ‘how to research a complex business like CRDMO (any business you pick up for research, for that matter). Please change your handle to ‘Prof Phreak’ . I want to convey my gratitude.

Expanding on this - we know Sai is involved extensively with Merck for linker-scaffold work in discovery stage and they did a linker-payload with Dxd for GSK. Then the company mentioned this last quarter

I had assumed then that it must be for GSK since thats where they were close to a complete linker-payload, so bioconjugation was the logical next step (albeit a great, exponentially higher proof of capability).

In Dec data, there are two entries for this and this is to Amgen. So looks like Sai has a third ADC customer now for certain.

PURIFIED RECOMBINANT MONOCLONAL ANTIBODYHU-IGG1 MAB CONJUGATED WITH DERUXTECAN- HU-IGG1-MAB DXD-D8ASPER DOCUMENT

This also seems to have Dxd as payload (and explains why they keep importing Exatecan - this is key RM for making Dxd) but its bioconjugated to mAb here which is purified recombinant humanized IgG1. I feel its a huge step because they get their feet into complex biologics work. The other thing is D8 (the other line item was a D4) - implies DAR 8 or Drug-to-Antibody ratio that is similar to commercial Enhertu. They have however imported the Antibody itself from Amgen, so they are one step short at this point of being an end-to-end ADC player in the discovery stage. They do however do discovery biologics work in the Boston lab, so its only a matter of time when all of it comes together for an end-to-end ADC molecule.

Your research into products of sai life is the most detailed work I have seen on product portfolio by anyone in cdmo sector.can you suggest some methods through which you found their portfolio?it will help others in persuing independent research on cdmo.

Team of Jefferies analysts noted that the list’s inclusion of WuXi AppTec hands Indian manufacturers a win, “especially in the small molecule and peptide space,” the analysts wrote. The India-based contract research, development and manufacturing organization space is estimated to make up a $6.9 billion market size by 2030, according to Jefferies.