Looking at your portfolio, it is quite interesting how for most of the stocks in common, your buy price is way lower than mine (with the exception of Rain). Also how most of your stocks are in profit, while I still have a few bleeding from 2019. I started buying IDFCF in 2019 and was fully allocated before the crash, although I did manage to buy more, my avg price is still 32. For me, the fear of missing out on something which I had conviction in is much stronger than the pain of temporary losses which tempts me to think price will run up if I don’t buy immediately.

Wondering how you managed to pick the bottom so consistently? Did you just happen to discover these stocks around their bottom? Or wait for them to fall even more even though they were already inexpensive.

I have added the relevant links to my previous post, thanks for the nudge. Just to add a bit of context, the 2017 market narrative was “chor bane mor”. There were even quite funny presentations on how kachra management will change because the next generation wants market cap. My point is that at each point in a market cycle, there are narratives (GST, unorganized to organized). The coffee can one started in 2017 with publications from Ambit folks and their launch of a PMS. This was followed by launch of Marcellus by folks who had left Ambit to start up their venture on the same principle. All this goes back to Terry Smith who has this coffee can approach for global equities for quite a long time. Point being we tend to go towards something which has done well in the recent past. That’s why I like your approach of trying to diversify investment styles. Enough of my mumbo jumbo, good luck with your investments

The key difference is that my PF was only 10% of Net worth before the crash, the increased the allocation during the crash due to the additional margin of safety which reduced my buying prices. Even now, this core PF is only 26% of net worth by buying price. I have some appetite for buying more in the event of a second market crash.

I would suggest staggering out your buys. If it runs up 10%, you still sit on a 5% gain if you staggered them uniformly. If it falls 10%, you only sit on a 5% loss.

A large part of my IDFCF buying was when price was between 18-20 rupees. It was clearly a ridiculous price for a bank undergoing a transformation and represented a unique buying opportunity. My starting buying price though was around 42 rupees. Buying on the way down (and up) requires conviction in the company, which comes from read multiple years of annual reports, investor presentations, management interviews, industry reports and such like.

Thanks for the additional context. I was not aware about this context. My understanding of coffee can investing comes from a different book (forgot the name now). I wasn’t aware about the ambit or marcellus context. The top level idea for this part of the PF is:

Lower investments due to lack of conviction due to lack of in-depth knowledge and lower expectation of returns (lower growth, often also over-valuation).

Protection of capital over long durations of time. Periodic evaluations of business triggers. The broad based diversified nature of the business should ideally provide the stability which I am looking for.

I expect returns from this part of the PF to be roughly between 10-15%, not too large. The primary objective is capital protection. After a long-enough period of time, If i have developed enough conviction in my own stock picking skills, I will happily let go of this (Coffee can) part of the PF. I just cannot allocate 50% of my net worth into micro-cap companies without even understanding if I am good enough to do so.

Ideally, I would love to own 30 companies with a outsized allocation to the higher conviction, higher opportunity size investments with constant and consistent tracking of fundamentals. My commitments to current job and family disallow me from spending more than K hours every week though, so i end up prioritizing top conviction 10-15 companies for the core PF and intend to only track with less frequency the Coffee Can PF of 10-15 companies.

Your views are always welcome, Harsh. And thanks for adding the additional context for the valuation of power companies and other links as well. I will definitely go through them when I can.

Also would like to add, since we are in a similar situation of having about a year or so of investing experience. (Although your net worth could be very different from mine and what I’m doing may not work for you)

I am almost entirely invested into equity. I keep a percentage in MFs just like you because I wasn’t confident of my abilities. But as my understanding has improved, that percentage has gone down. I don’t worry too much about hedging as I’m not managing an extremely large sum of money nor do I have to worry about redemptions. I’m okay with prolonged drawdowns.

And for risk management, I do a similar thing which you mention which is dividing the portfolio into different kinds of bets. I prefer to think of it the way Peter Lynch does - dividing into stalwarts, fast growers, turnarounds, cyclical plays. In any given time you find opportunities in all of them but the proportion varies depending on market opportunities so I like to keep it flexible as opposed to strict demarcations.

Stalwarts I suppose is another word for Coffee Can where you expect the least amount of churn. I think of these as defensive and I would increase their weightage when we have an early 2018 kind of scenario where broader market has a lot of fluff and I’m feeling scared of valuations.

Overexposure to nanocaps is a concern I relate to. Which is why I think smallcaps (Mcap > 500 cr) provide a sweet spot where you have some stability of business and information about the company/promoters available publicly.

And I’m not really comfortable having large allocations to 1-2 nanocaps (Mcap<200cr), which is why I tend to take smaller positions in a lot of them.

Monitoring the industry weights ensures that I’m not too exposed to any particular industry.

Ultimately, I like to keep things simple and the risk indicator I rely on the most is whether I can go to sleep peacefully knowing I own what I own .

After thinking about it a bit, I have decided not to pursue coffee can investing because as discussed earlier, it’s very difficult to “shut it and forget it”. A lot of these companies were also available at a very high valuation which also makes holding them psychologically challenging.

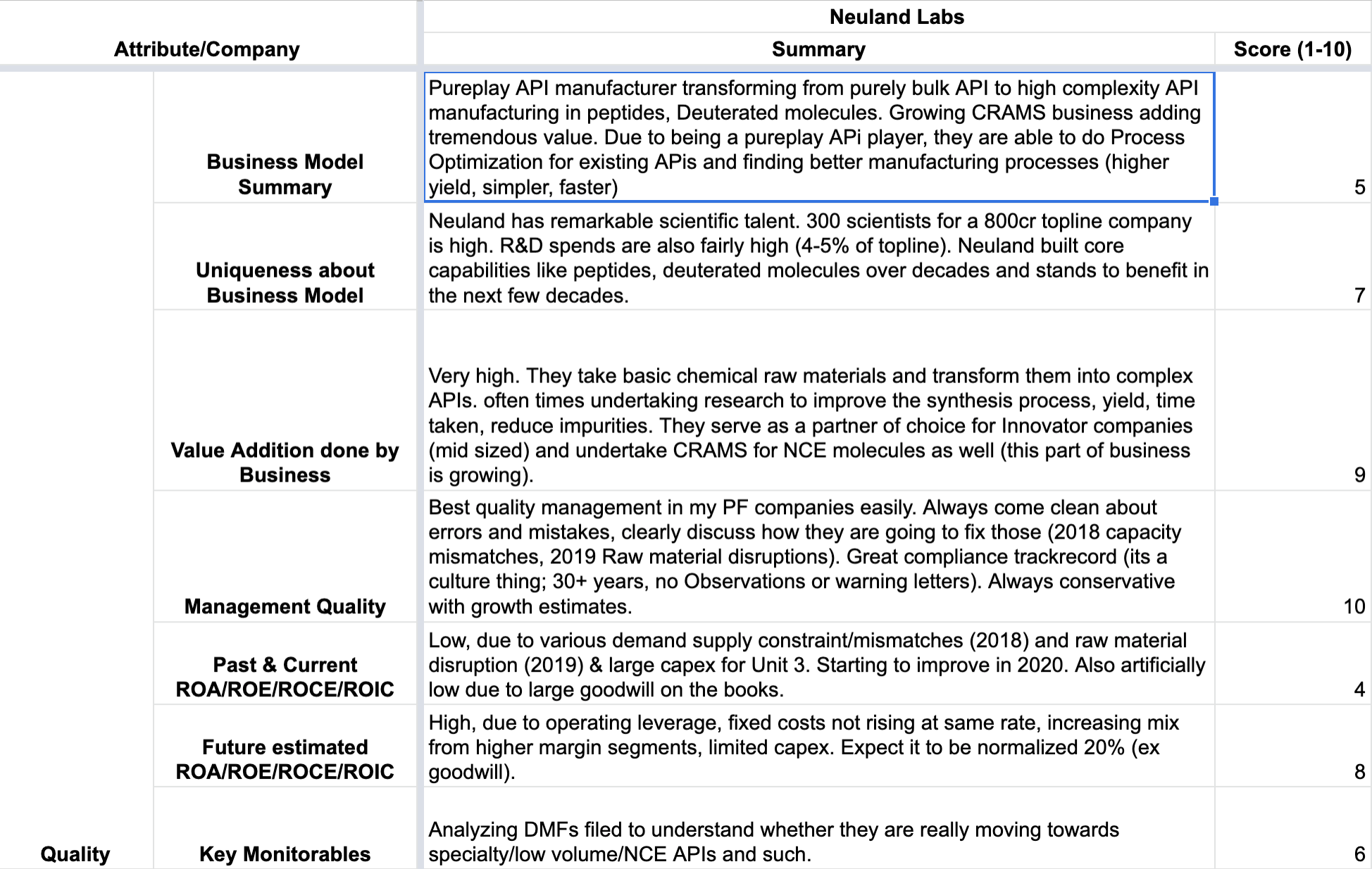

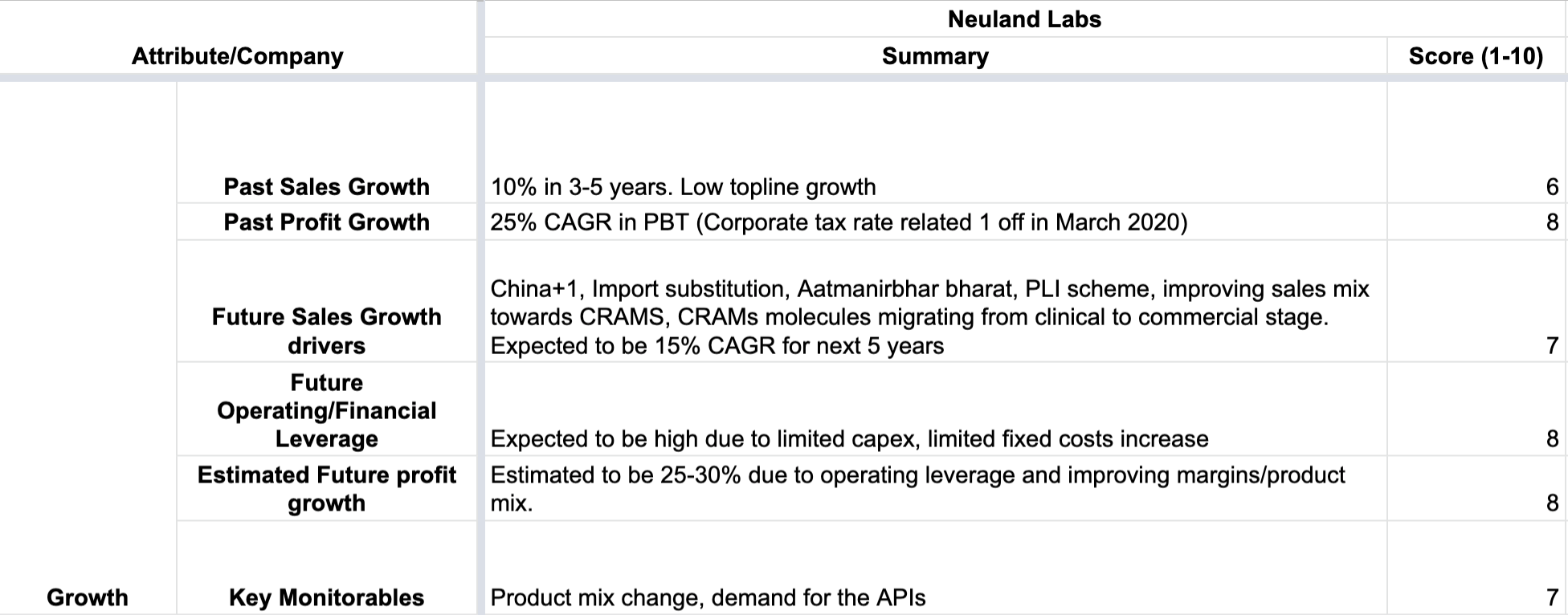

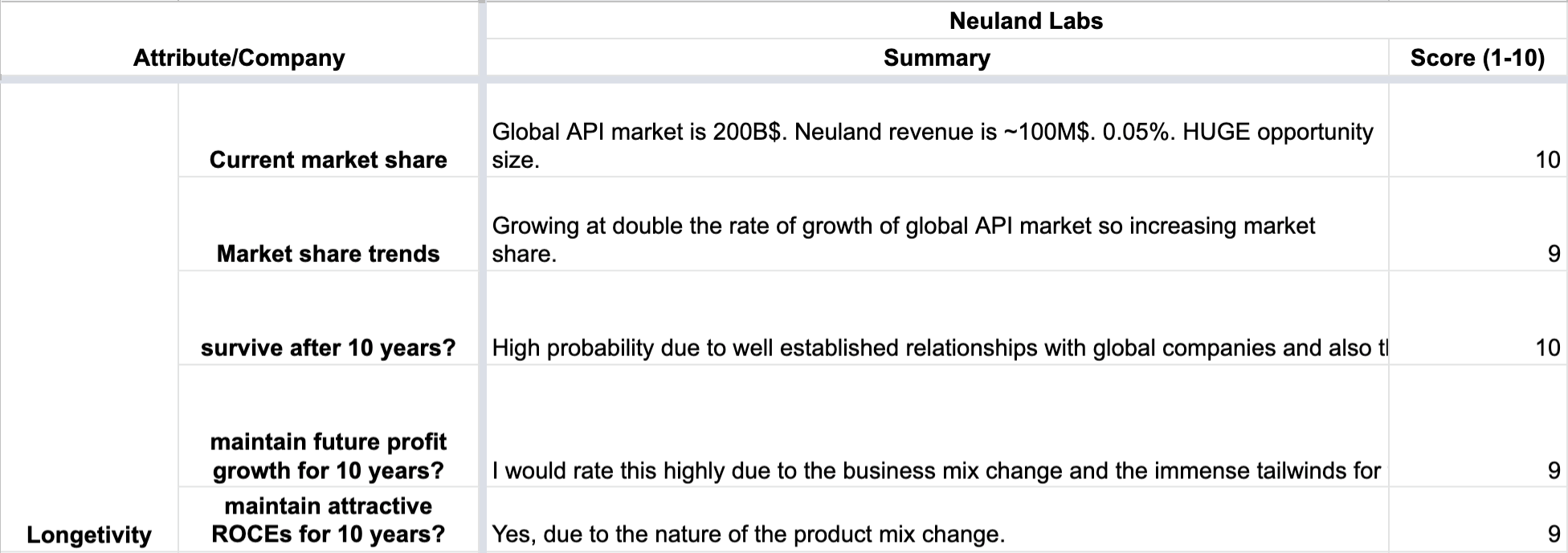

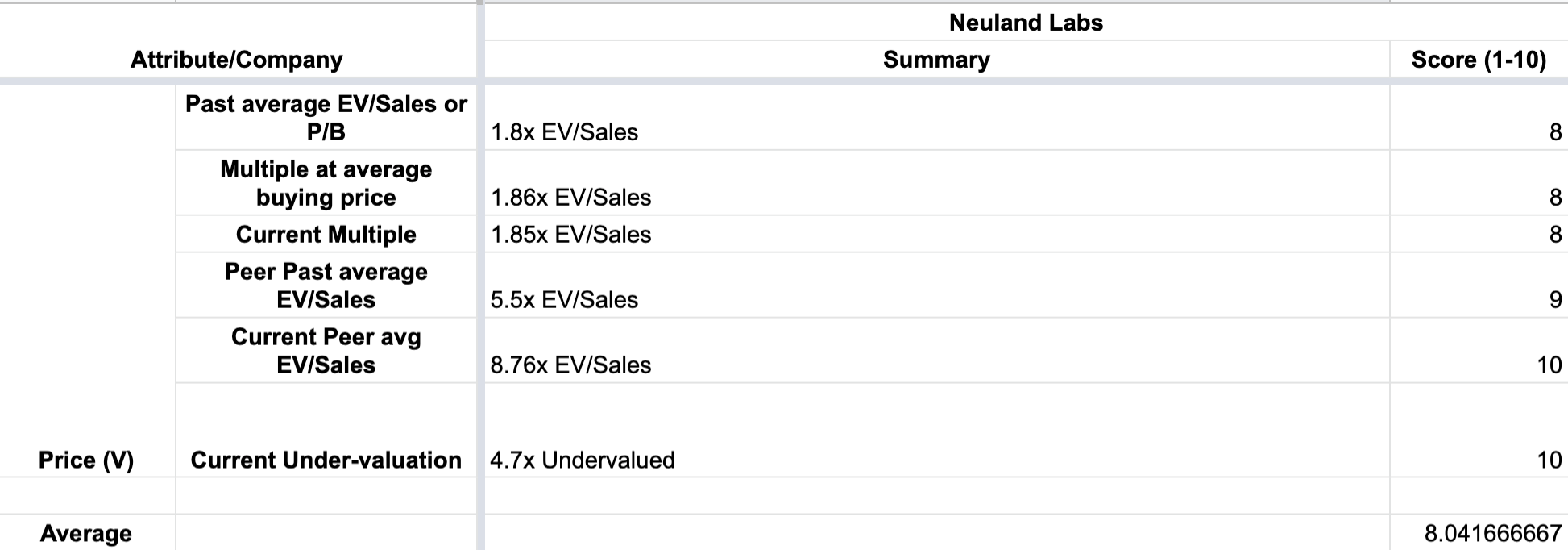

In the core PF, I have added Neuland after some research which can be found on their thread. I also added a little bit of Suven Pharma because both of them seem very different types of companies although both are primarily being driven by CRAMs. Would be interesting to see how it plays out.

Another company I added a little bit and that I intend to build a position over time is Amara Raja. The opportunity size for Battery makers in India is simply huge (specially with the switch towards EV). Amara is the better of the 2 battery makers because it is more efficient and profitable.

Another company i added is Vaibhav Global: A vertically integrated retail ecommerce platform that is largely into discounted jewellery. They have some serious operating leverage going for them. Their market share in their target markets (US, UK discounted jewellery) is 3% (up from 1.5% few years ago) versus market leader’s market share of 93%. Average revenue per household is 3$ versus 60$ for QVC. Vaibhav global’s next leg of growth is being driven by their digital businesses (website, app, other platforms like Amazon). The valuation is a little outside my comfort zone, which is why I will look to build a position over time.

I realize it is extremely difficult to hold a concentrated PF of stocks. This is especially difficult for beginners, and also difficult as the PF size increases. I also think it might be better to hold more stocks towards the beginning of a PF’s life cycle because that enables me to track the large set closely, and consolidate over time, as the distribution of my conviction changes. Number of stocks in Core PF is now 17 (including Vaibhav, amara, Neuland and Suven).

I still want to keep a diversified investing style (specially given the inherent risks of investing in Microcap stocks). I have decided to diversify into dividend investing. This style has always seemed very attractive to me. A regular royalty + growth of capital is a deadly combo. Even if the dividend yield is only 5% today, as long as I believe the company can grow dividends at 10% PA, this is an attractive opportunity given that typically inflation has been 5-6% in India. As a part of this, I have bought heidelberg cement, ITC, National Aluminium Company, GAIL, Bajaj Auto, Powergrid.

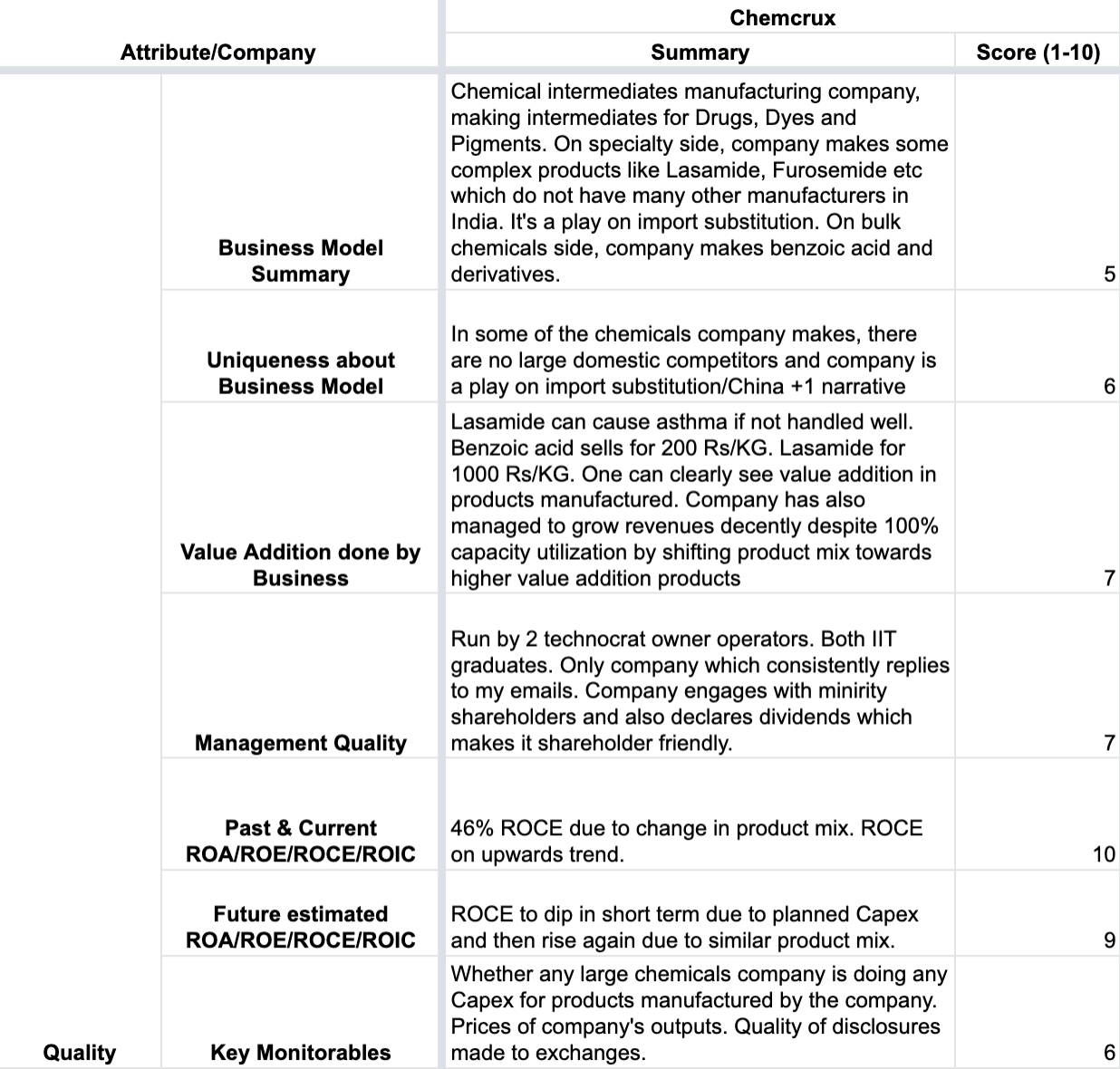

The lot size for Chemcrux is changing to 500 soon (yay!). I hold 2000 shares right now. I intend to at least half the position size to control for risk of owning an illiquid microcap. Chemcrux is now roughly 25% of my PF. This is an uncomfortably large position size.

I am very interested in Shilpa Medicare and am reading about it a lot since last few days. The company has been investing into Biologics (both biosimilars and NBEs) since the last 4-5 years and consistently diversifying revenue away from oncology APIs while also forward integrating into formulations. This makes shilpa a difficult company to understand. While it is somewhat richly valued as per EV/Revenue, but if the biologics molecules fructify in the next 5-6 years, then Shilpa’s fundamentals will definitely see a quantum jump due to the market size of the molecules involved. At same time, I do not want my PF to be overly diversified into Pharma Stocks. I’m also actively considering which pharma stock to sell, if I do decide to own Shilpa.

I think of PF construction as some form of gradient ascent. As we learn more about the stock market, PF churn is inevitable. However, after sufficient amount of time (acquiring knowledge), the churn should reduce down to 0. I consider most of my investing to have started around April/May. I fully expect some PF churn at least for another 6 months as I learn more and more about the specific companies and am able to find better opportunities than current PF stocks.

Hi Sahil, I read through your posts in other threads and had a curious question. I see that one of your biggest mistakes has been yes Bank and also see that you have very high conviction in another bank IDFC bank. Not that these two have anything in common but generally I have seen among peers is that a person who have had a bad experience with any sector refrains from high conviction bets in that sector, like say I had a bad time in NBFC and do not look at them any more as a practice. Not that I am right in doing that but thats a general psyche as I realise the risks of that sector much more than my first experience.

In above context, is IDFC bank a significant portion of your portfolio? What percentage if you can share. Also, why did you chose a high conviction in Banks again. Is it because you understand Banks very well or your liking for that sector as a vision or some other reason would be good to know. Thanks

One reason I’m able to take some concentrated bets is that the equity PF is only 33%-40% of my net worth. Even a 10% Concentrated bet is only 3-4% of Net worth.

Currently, IDFCF is 10% of PF and ~3-4% of net worth.

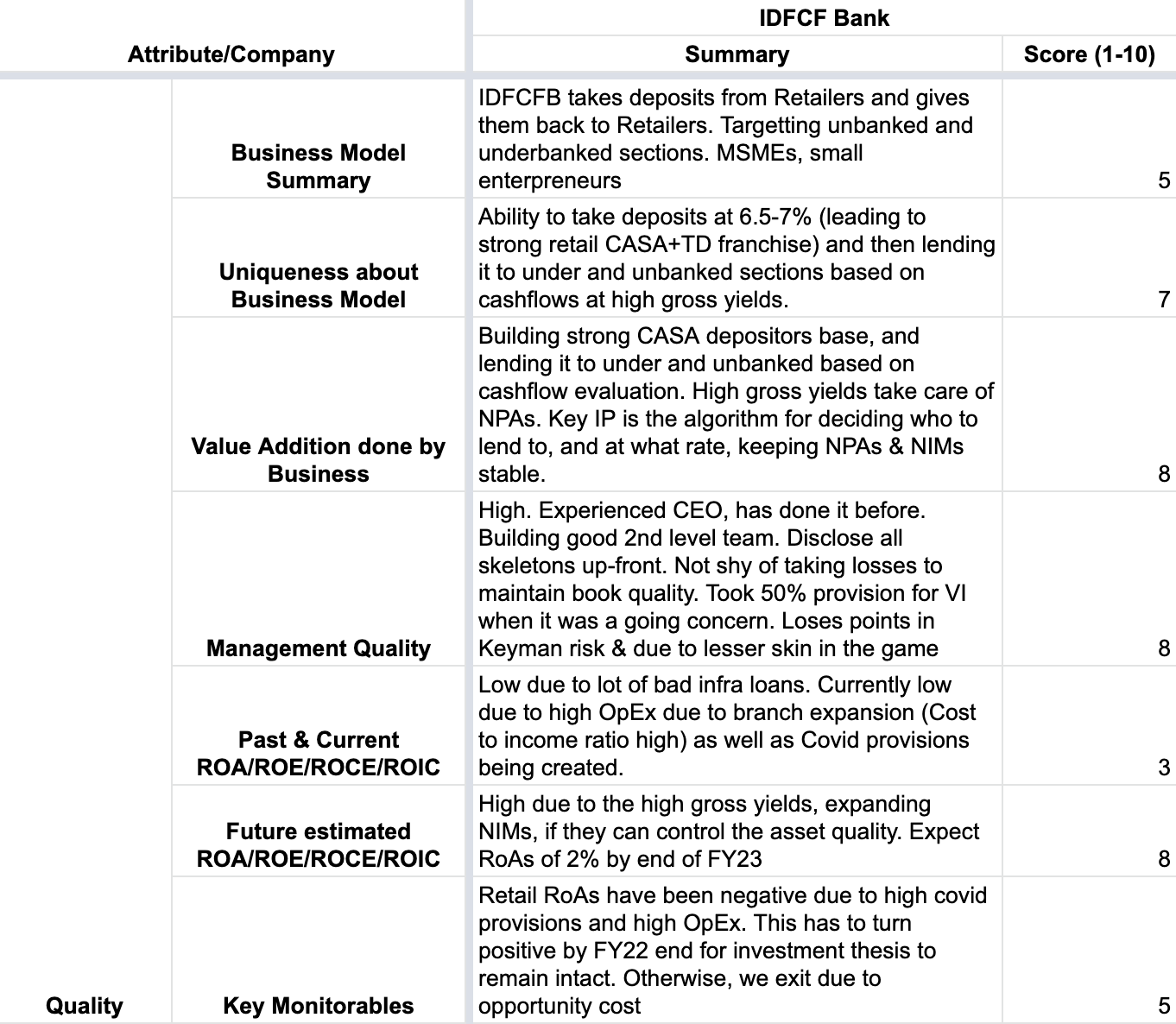

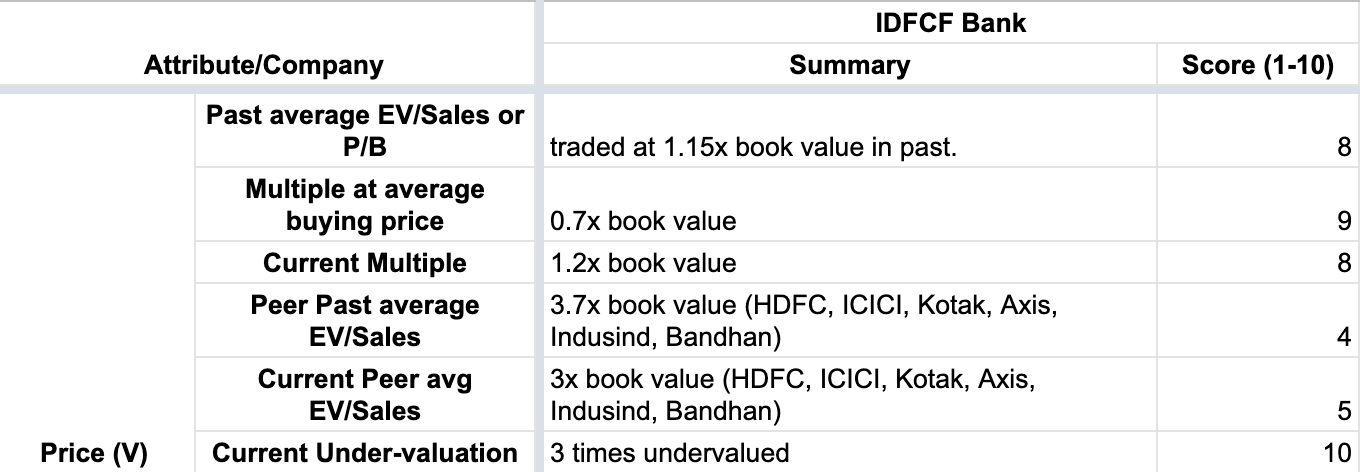

My IDFCF position has been built over time, a lot of buying happened at prices of 18-20 rupees (some before covid crisis). As a result, my average buying price was at 20% discount to book value. I’ve been closely monitoring IDFC First and they are prudent bankers. All fundamental ratios which matter for a bank, are improving for IDFC First. From next quarter onwards, their loan book will start growing up. Due to large up-front costs, retail as a unit is still loss making, but i fully expect that to turn around over time, as the up-front costs get amortized, cost to income ratio comes down, and provisions normalize over the duration of next 1-2 years. Yes bank was in many ways the exact opposite of IDFCF. My understanding of investing was very limited when I was a yes bank shareholder. It has increased a lot since then.

My own understanding is, as a large rule of thumb, market underprice turn-arounds for a very long time, until there is fair amount of certainty about the turn around succeeding. This is because base rate for turnarounds is low. Most investors main concern with IDFC First is the stock underperformance. This should not be a reason for under-allocation, as long as the business is going in right direction. They’ve been fairly prudent in creating Covid provisions, have always been up-front about credit losses, even at the cost of large frequent quarterly losses and mostly following up on most of the guidances they gave for a 5-year period. I continue to monitor the Cost to income ratio and provisions. The investment thesis is clear. I will remain invested patiently for a period of 2 years, waiting for RoAs of 1% in retail banking. If that happens, I continue to stay invested. Otherwise, I’ll exit. Imo probability of staying is high (80%). Of course this is a subjective opinion, not a mathematically sound statement.

As decided, Chemcrux allocation has gone down, since it was never a comfortable position to allocate this high a capital amount to 1 position.

Deployed some extra capital into IDFCFirst

Deployed Capital into Dividend plays.

Deployed Capital into Polymed, Astec, Neuland, Vaibhav Global, Laurus Labs and reduced a bit of allocation into Alembic as I balance that position out with laurus.

I’ve added the reason a stock exists in my PF. I will track gains only for (Core+Cyclical+Exploratory) PF stocks since dividend stocks were not added for capital appreciation (nor the hedge).

Realized gains is 9.7% pre-tax (majority of gains includes chemcrux for rebalancing, caplin for exiting position, lincoln for exiting position).

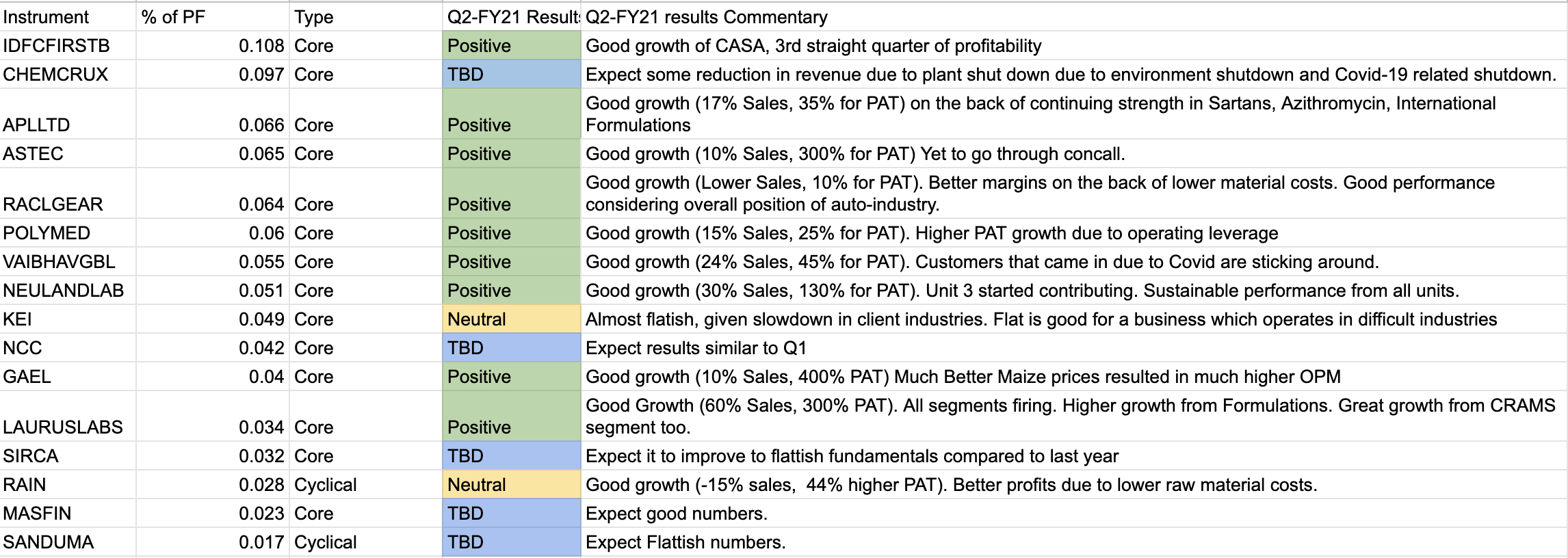

The best judgement of a portfolio is the business performance, imo. I will also attempt to track a summary of business performance at least twice a year, and hopefully all 4 quarters:

I am planning to exit my position in KEI industries next week. Nothing wrong with the company, I just found better use for my capital. Axtel Industries. Apples to Oranges comparison. However, here is everything which goes for Axtel and against KEI:

Axtel has a distinguished business model (In India). No listed competitors. And the barrier to entry is the relationships They’ve built over last 30 years of relationships with all large FMCG giants. The downstream industry is semi-secular. Not cyclical (like KEI). It’s the technical know-how that they’ve established over 30 years of repeatedly serving these FMCG companies. These relationships are difficult to substitute. KEI is a commoditized player. This is also visible in the Net profit margins for Axtel and KEI. Axtel averages > 10% NPM whereas KEi is at ~5% NPM. Opportunity size is also much larger for Axtel. It is a tiny fish in a giant pond. KEI is in a fierce battle for market share with Finolex, Polycab and Havell’s. Last few years, Finolex is the only loser in market share (cc: @jamit05. source (page 2)). Axtel does 100cr sales in an industry where the largest guy does 6,600cr a year (source).

For these reasons, I will slowly switch out my position in KEI for position in Axtel. Why not keep both? I do not want to deploy more capital at this stage. KEI is the weakest stock I own in core PF.

I plan to track my investment thesis in each PF stock in a simplified way in order to keep it as structured as possible and also track evolution of my thoughts over time. Adding it in the structured way for IDFC First bank. Will add others over time:

Disc: Invested. This is not investment advice. I am not a sebi registered advisor. This is a microcap and carries several risks with regard to ownership. Please consult your investment advisor & perform your own due diligence in case you feel the urge to invest in it.

Disc: Invested. This is not investment advice. I am not a sebi registered advisor. This is a microcap and carries several risks with regard to ownership. Please consult your investment advisor & perform your own due diligence in case you feel the urge to invest in it.

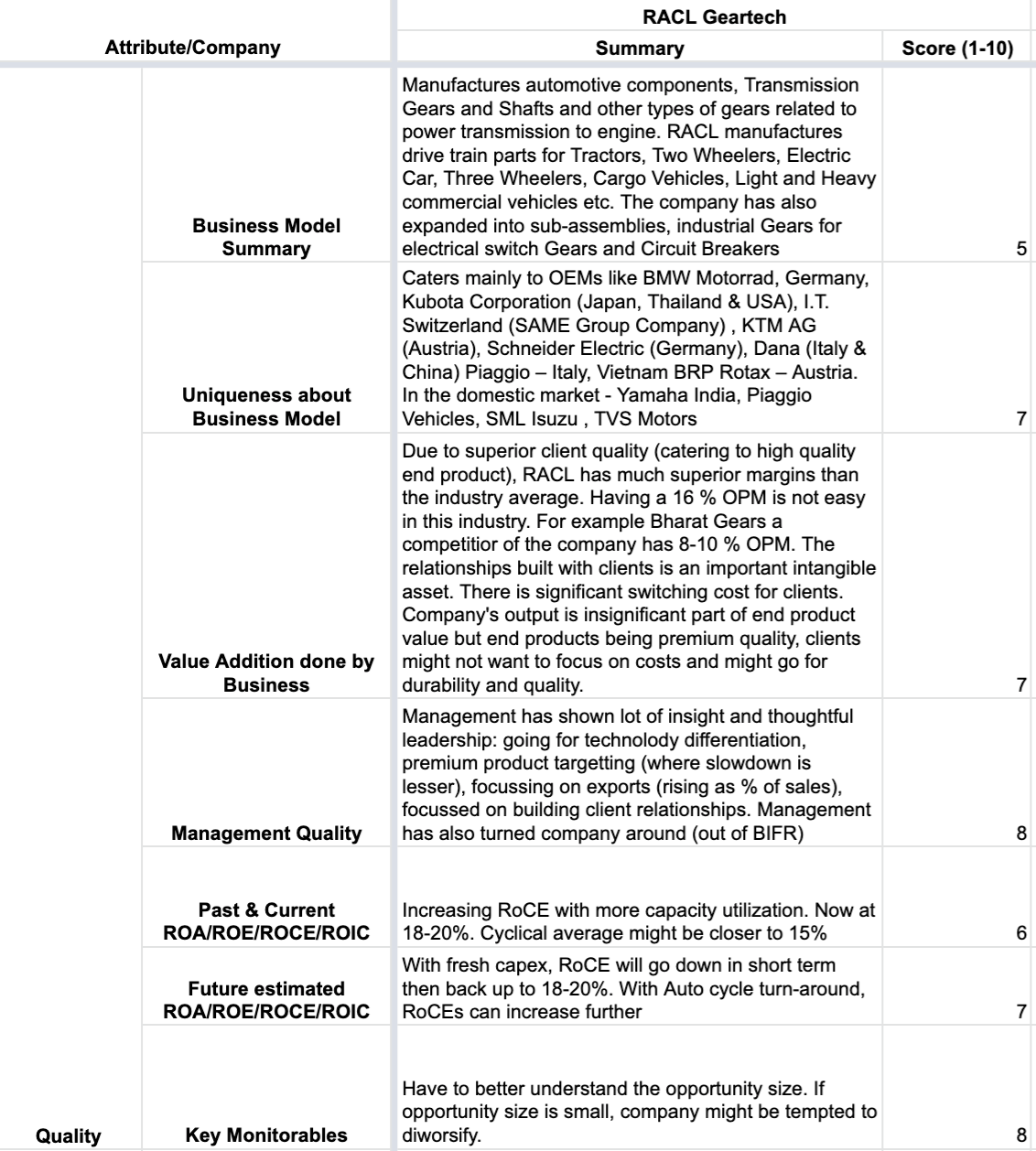

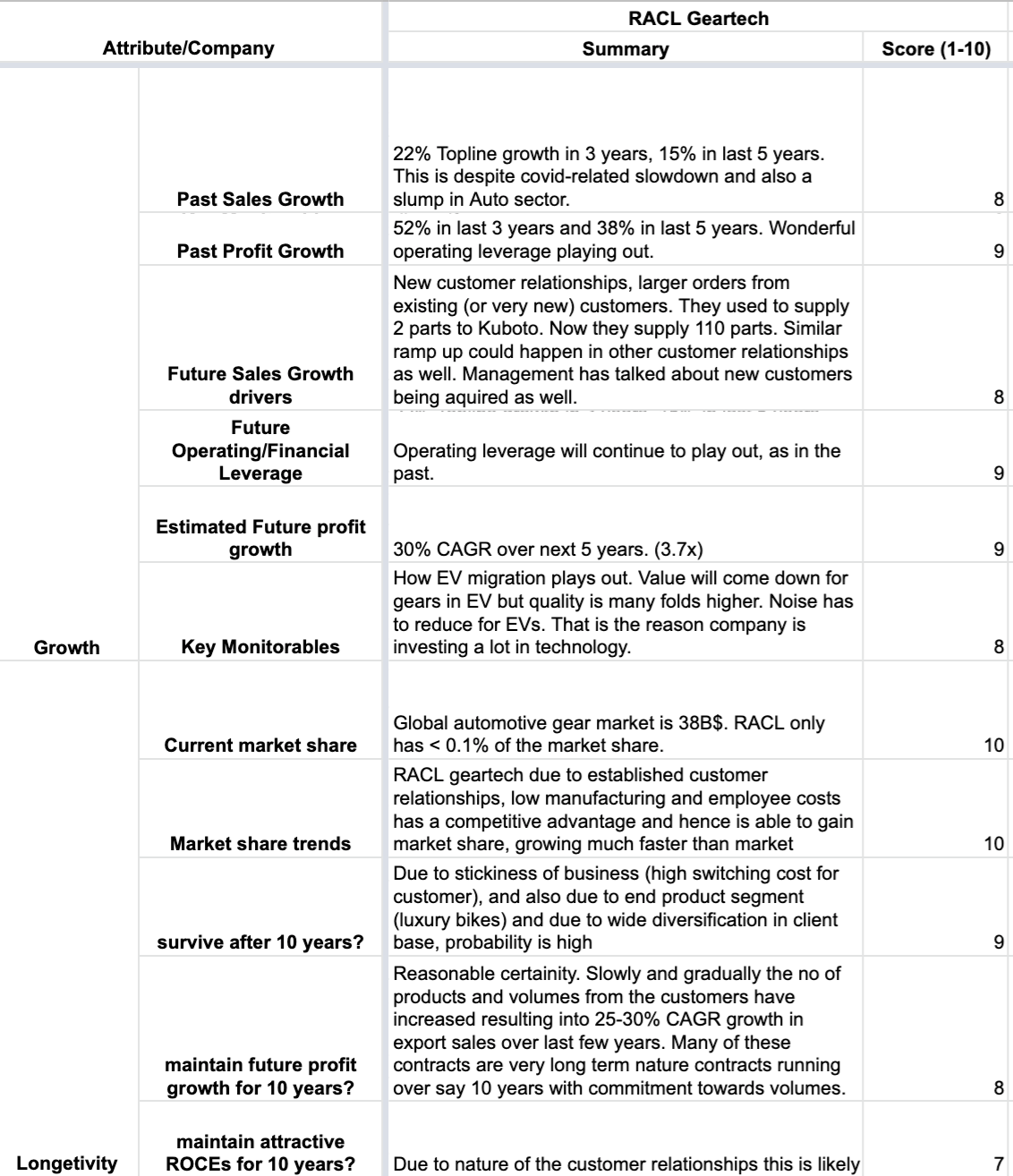

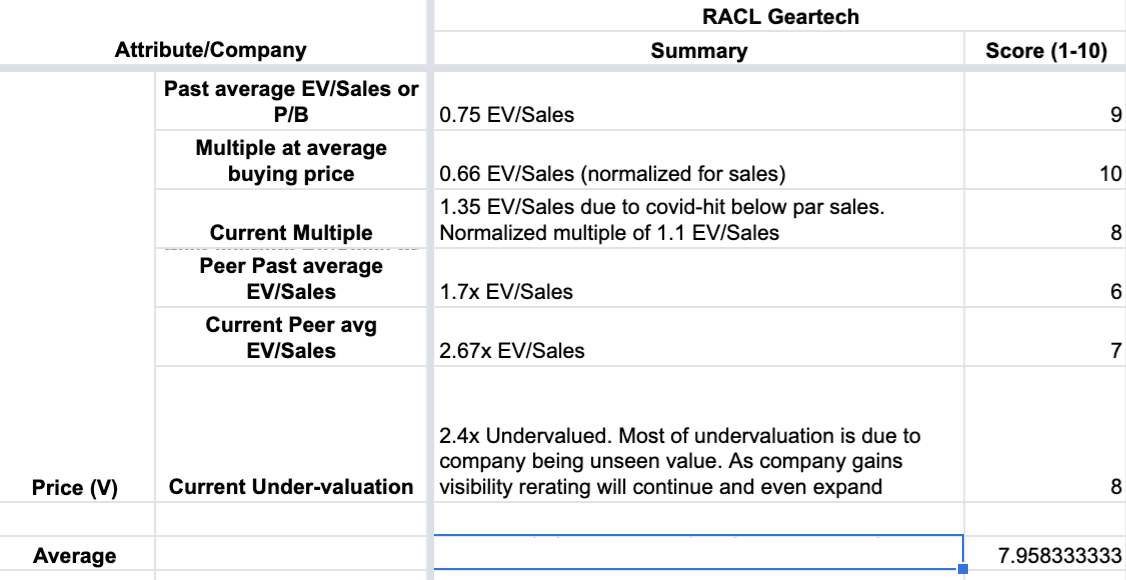

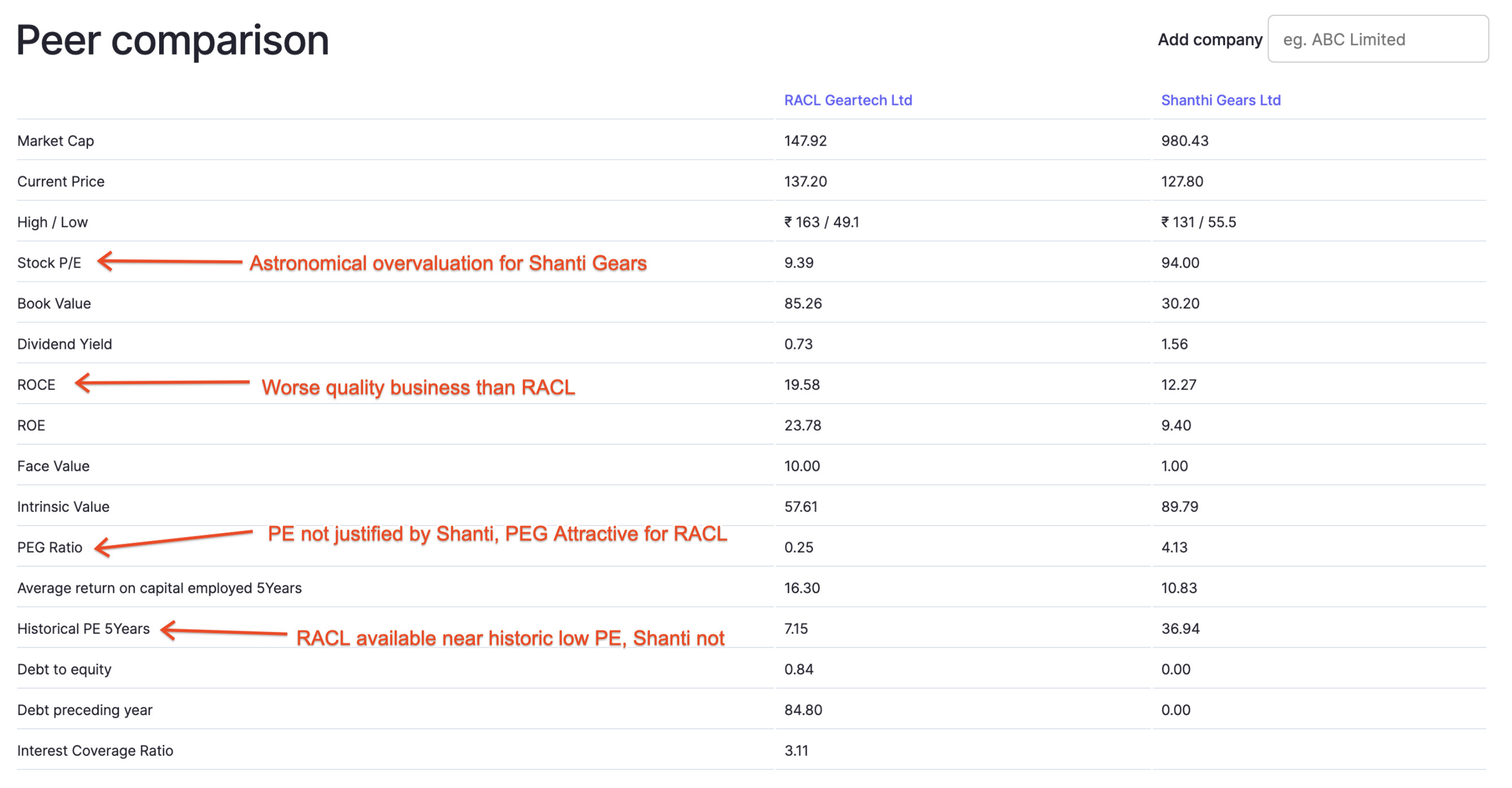

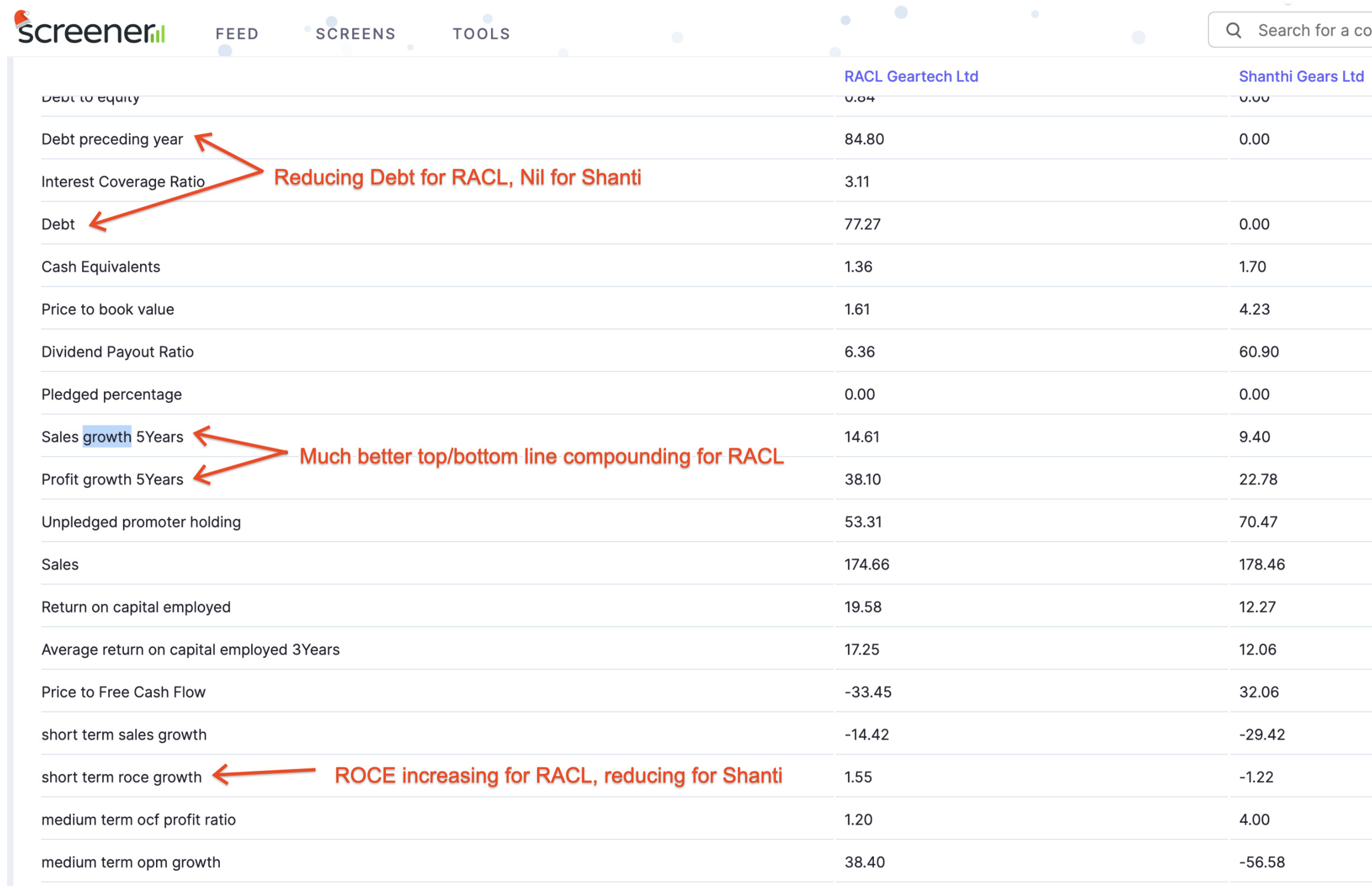

All in all, I would not be surprised if the Shanti gears bubble pops sometime in next 1 year. RACL (in my opinion) would get rerated once it reaches some scale (Ive covered above why I think it would reach some scale) and some institutions start covering it.

Total realized+unrealized profits (only for Core PF): 40%

Note that my capital deployed has gone up 4x compared to 1 year ago, so a lot of it has been deployed in the 2nd half of the year. I will only measure the total returns on capital deployed not the CAGR because it is too cumbersome to maintain a log of each and every buy/sell/capital deployment. I do hope that zerodha provides a CAGR facility soon.

Some Updates on the diffs:

I’ve sold Alembic Pharma and replaced it with Sequent scientific + additional buying in Laurus Labs. In general, as per my earlier post, I’m always on the lookout for replacing PF companies with better quality companies and this is a step in that direction. Sequent is play on animal pharma and has characteristics of FMCG in terms of industry structure, level of consolidation, pricing of the end products and certainty of earnings. Recent promoter change to Carlyl will help Sequent move to the next orbit of growth, helping them enter China, US and companion animals. All significant opportunities. EBITDA margins are improving by 1.5-2% every year.

KEI has been replaced with Apollo tricoat. Tricoat has a much better value addition proposition (including exclusive use of DFT and ILG technologies to create superior products) and with their Rs 2,000 chaukhats replacing Rs 6,000 and worse wooden chaukhats, this company in the structural steel section is expecting to grow at 30-50% in the next 3-4 years at least. I estimate their market share to be < 1% and hence they have a long growth runway in front of them.

I found RACL to be quite under-valued and hence added a bunch there.

RACL and NCC have moved to higher % of PF due to large price appreciation.

Added Axtel industries. They make machines for FMCG companies to make their products. They are able to deliver European standard quality at Indian price (aided by better manufacturing and labor costs). Backed by a technocrat promoter and several years of long lasting client relationships, I consider the probability for complete loss of capital to be low. They are a primary supplier to all large FMCG companies (inside and outside india), and have barely scratched the surface in terms of the market share.

Sold GAEL. In general I’ve come to observe that I like owning companies with small but growing market shares backed by some competitive advantages. GAEL does not fit the pattern, already holding 40% market share.

Sold Sirca paints. The company has a lot of potential but are already a large player in their primary market. The wall paints play is more of a hope rather than a certainty IMO. I have studied Indigo paints well and intend to add it when it IPOs, unless the price is ridiculously high.

Sold Rain industries. Bought Sandur manganese. It’s a very well run company which was very under-priced, not very levered and a purer play on commodity cycle turn around than RAIN.

Given the ridiculous prices at which ITC was, I have increased that position after studying it a bit more.

New companies that I intend to study are Neogen and Navin Fluorine. At some point, it can become difficult to ascertain between a company that I expect compound earnings at 25% and one where the compounding might be 30%. For this reason, unless there is a compelling reason to switch, I would like to stick to current companies and also maintain only 15-16 non-commodity core PF companies at most.

Disc: This is not a buy or sell recommendation. I am not a sebi registered advisor. Please consult your own advisor before investing.

You can use XIRR for calculating returns. You simply need to keep track of cashflows (transfers between your bank account and Zerodha account), and apply XIRR formulae in excel. Baically you are calculating return on money deployed in your trading account.

I personally feel this as practical and efficient way to calculate portfolio performance as you don’t have to track everyday buy/sell transactions. Let me know if you need any help there. Link below has the summary of my XIRR values, it don’t have the methodology though