Thanks Sahil for adding clarity to my thoughts!

My apologies for the delay in response.

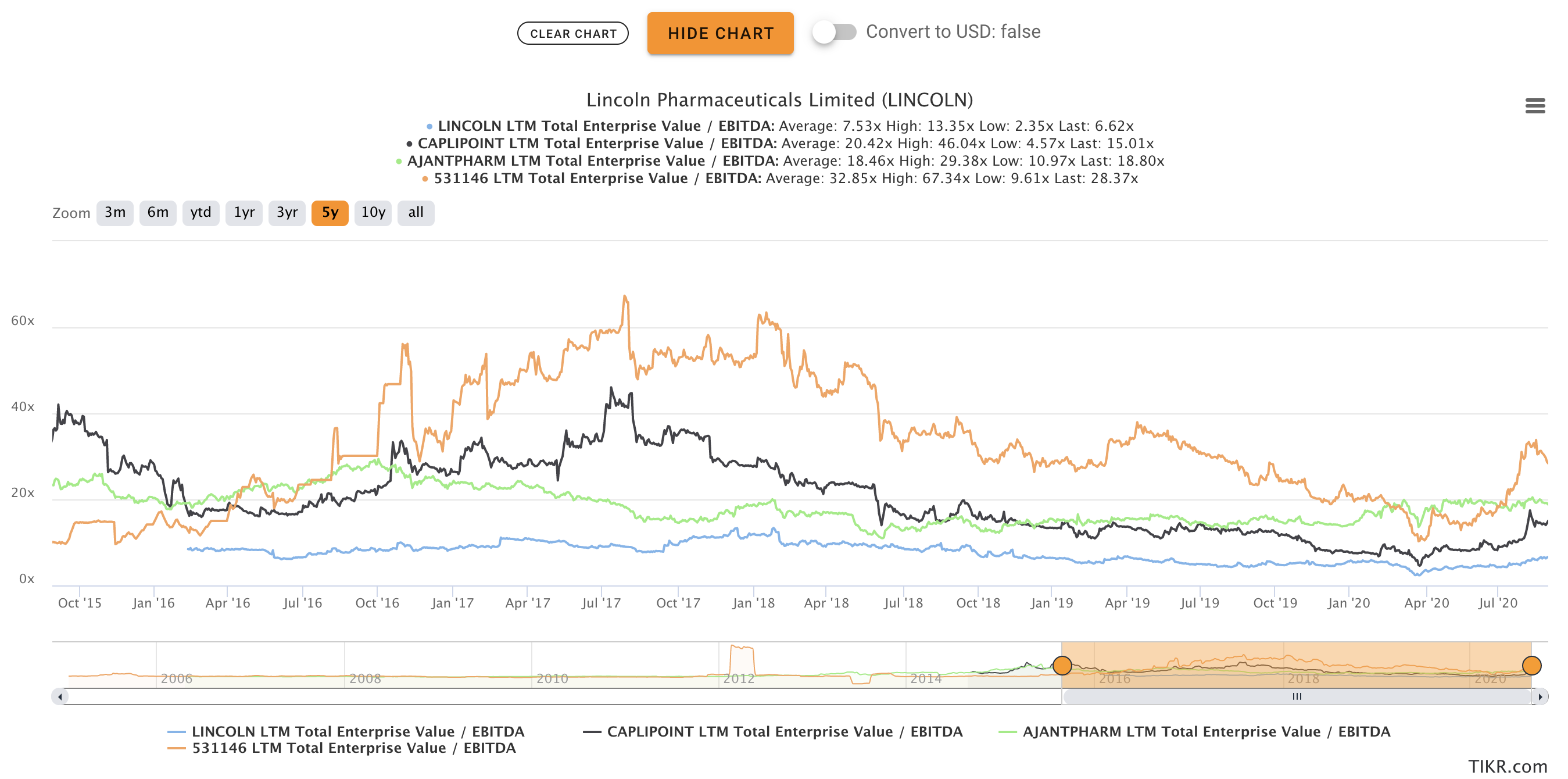

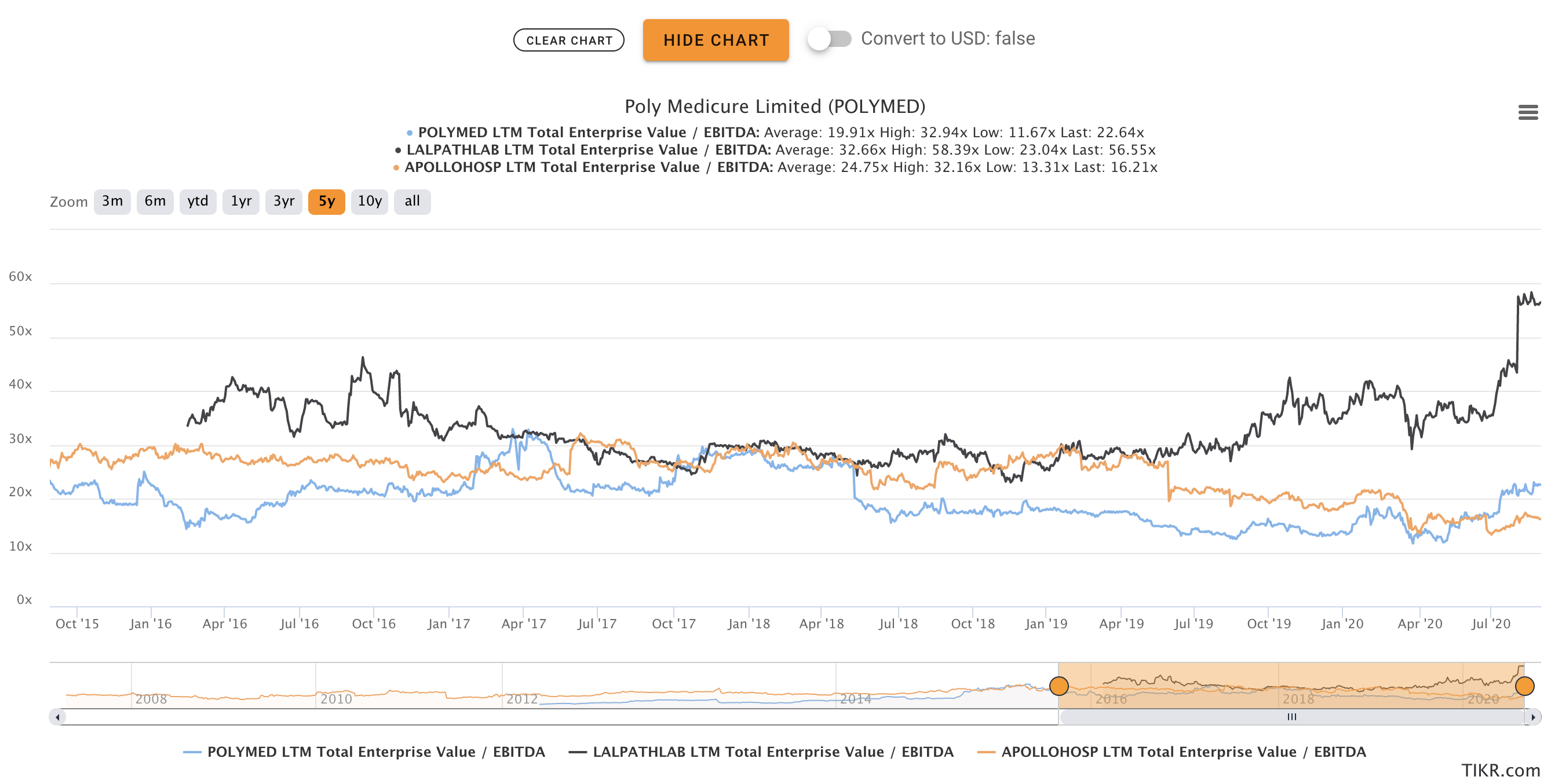

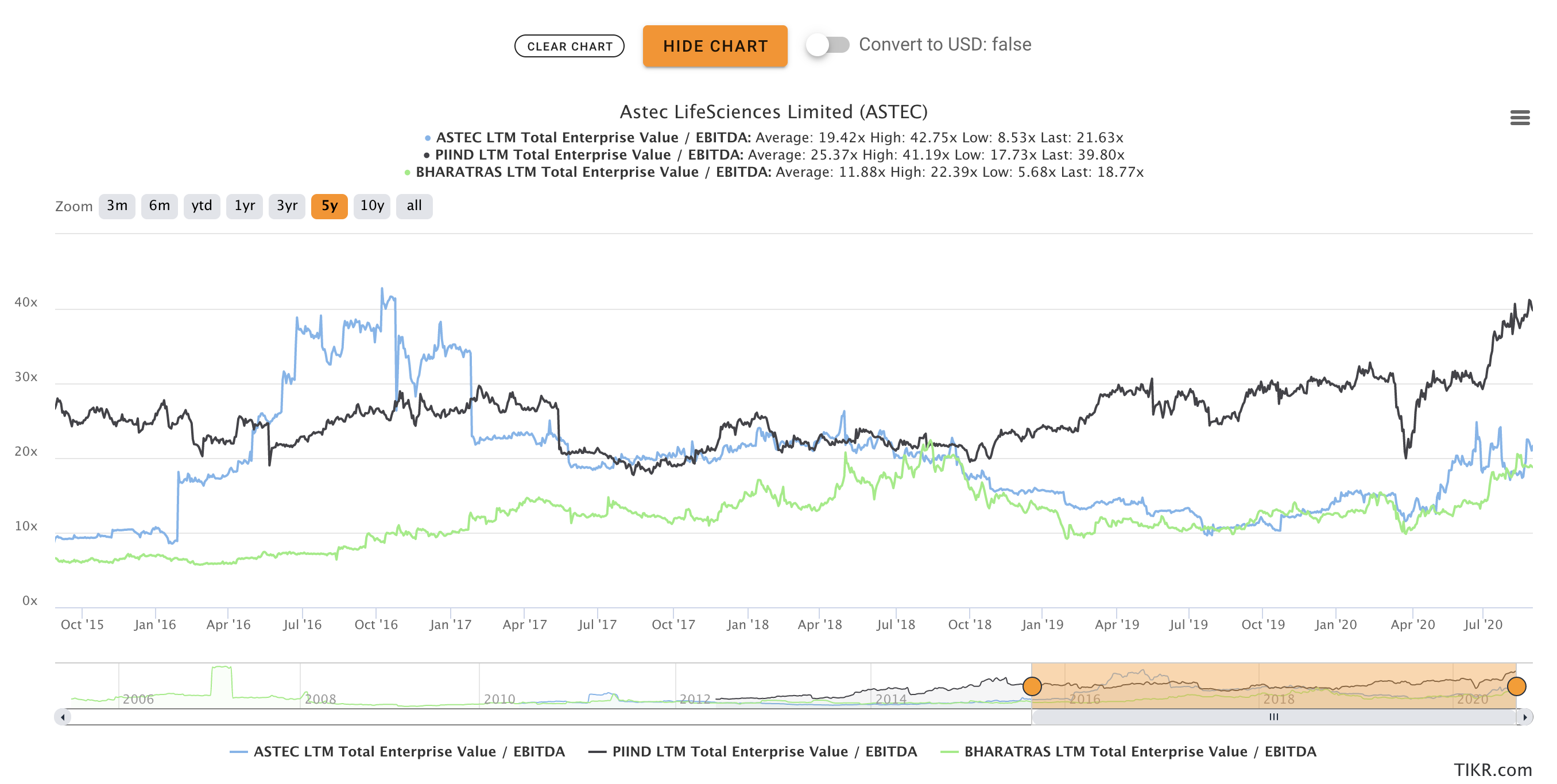

I have heard of few instances where bigger players have played out small players through price wars, because of scale they can have. An instance could be TaxiForSure. Amazon has done it.

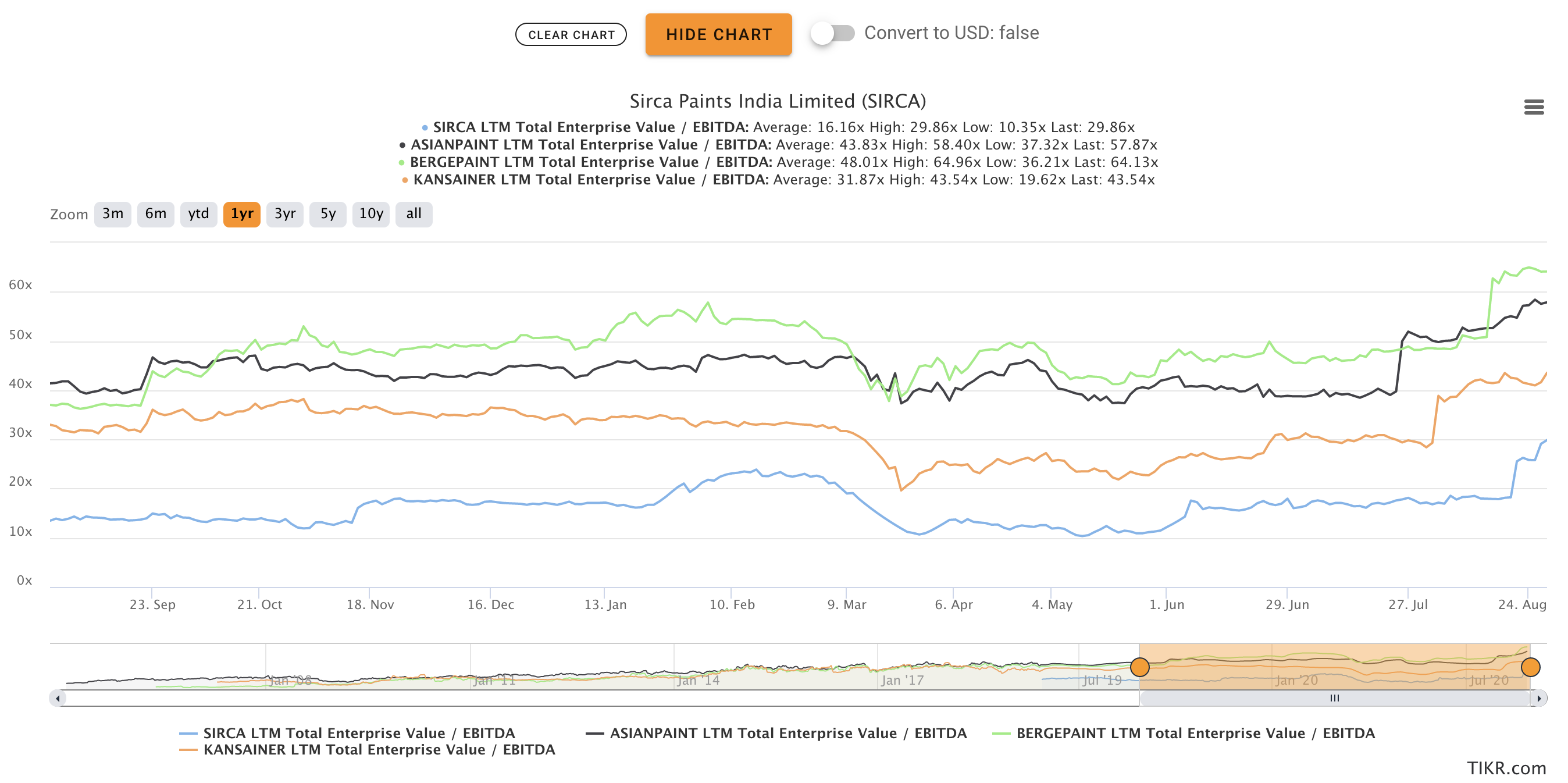

I am not saying, Sirca would fall the same fate. I am only trying to build a narrative (which you rightly pointed out).

I think they have a mention of this in one of their ConCalls. Quoting it directly here:

Harshil Shah: Also lastly what are the competitors that you are most competing with fearful of and why are people deciding to go with you versus the more traditional established brands

such as Asian Paints?

Apoorv Agarwal: So our major competitor in the market stands as ICA Pidilite which was ICA before

and was taken over by Pidilite in early 2017. He acts as a major competitor for us in

the market.

Harshil Shah: Why would people be choosing you over something like an ICA Pidilite, is it a pricing difference, is it working capital you are providing to these retailers or is it the quality?

Apoorv Agarwal: No, working capital is in fact we think that ICA Pidilite is providing a lot more in terms of credit that they supply to the market is even higher than ours, but then our presence, see, Sirca brand started from the Northern part of India 15 years ago and ICA before being ICA Pidilite was majorly a South centric brand, but now moving forward with ICA Pidilite, their marketing strategies and their core mission with the

company seems to be that they are positioning again their brand as a local

manufactured brand and they are moving towards 100% local manufacturing and they are stopping imports vis-à-vis we, Sirca Paints, we are focused majorly to keep focus on our premium Italian wood coating range which we are going to keep on importing from Italy and do a vertical and horizontal expansion of the product lines from the new facility. So our major edge is that we want to keep the position of our pure Italian

brand in the market and enjoy the specification of architects and interior designers and also the end users giving them the feel of a pure Italian product. Besides that, we want to increase the product portfolio from this new facility so that we can take over the increasing chunk of the Italian PU in future because the Italian PU market is growing at a tremendous rate in the coming years and is taking over Indian PU at a massive rate.

That’s what I found it in the Q1 ConCall. The industry is growing at 20% CAGR, and there is enough for everyone.

Sirca is in good sector, has tailwinds, and if executed well, can capture good market share.