My apologies, i respect this forum a lot and do not want to clutter it with transaction level details which might just be noise to most people. Over time i have analyzed what i have been up to. What i have seen is that there is a lot of alpha in indian equity markets but one has to be very strict in the process to capture it. Most people are unable to capture these alphas due to a lax process. So i wanted to share my current process first before i talk about what i have been up to:

My xirr over last 4 years now, is high, when i look back to see what worked for me & what didnt, where i made mistakes. I see 5 things which must all be present in my process. I will also talk about what makes it difficult for everyone to achieve this alpha from my meetings with countless investors.

Must haves in process

- what i learned from graham : Low Starting valuations. in absolute i need to think company is undervalued. As we all know valuation is very subjective. So its better to err on side of caution. Eg: MTAR is expensive, dixon, kaynes expensive. RACL at 5 pe wasnt expensive, Aurionpro at 8-9 pe growing 30% with leading IP based CreditTech products, despite its checkered past was not expensive because of the management changes that happened (Ashish Rai). But one must keep in mind, that TTM p/e or p/b is not valuation. Valuation is a subjective exercise in summarizing the cashflows from next X years. To that extent, valuation comes after business understanding not before. I cannot value that, which i dont understand. An NBFC at 5 p/b or a fintech at 80 p/e (NPST) can be undervalued if we clearly understand & are convinced by their growth triggers & competitive advantages. But definitely need to remain on our toes regarding execution since comfort of entry valuations is absent. But dismissing such opportunities out of hand without understanding the business models would be a grave mistake of omission.

- what i learned from PEAD people: Catalyst in next 6-12 months. This is key to get high XIRR. I dont want to buy & wait for 4 years to make returns. In many cases catalyst is management change (Redtape, Aurionpro), in some cases, high growth (Aurionpro, Xpro, RACL, Angel), in many cases mixture. In some cases, there is a lack of understanding of business model (NPST). We gauge this by talking to fellow investors. As wide/diverse a set as possible. if we understand it well (you’d be surprised by the high number of people who just see p/b or p/e before understanding business model). In some cases, it can be a reduction in 1-off expenses coupled with high growth in volumes in a business model with inherent operating leverage (like MCX).

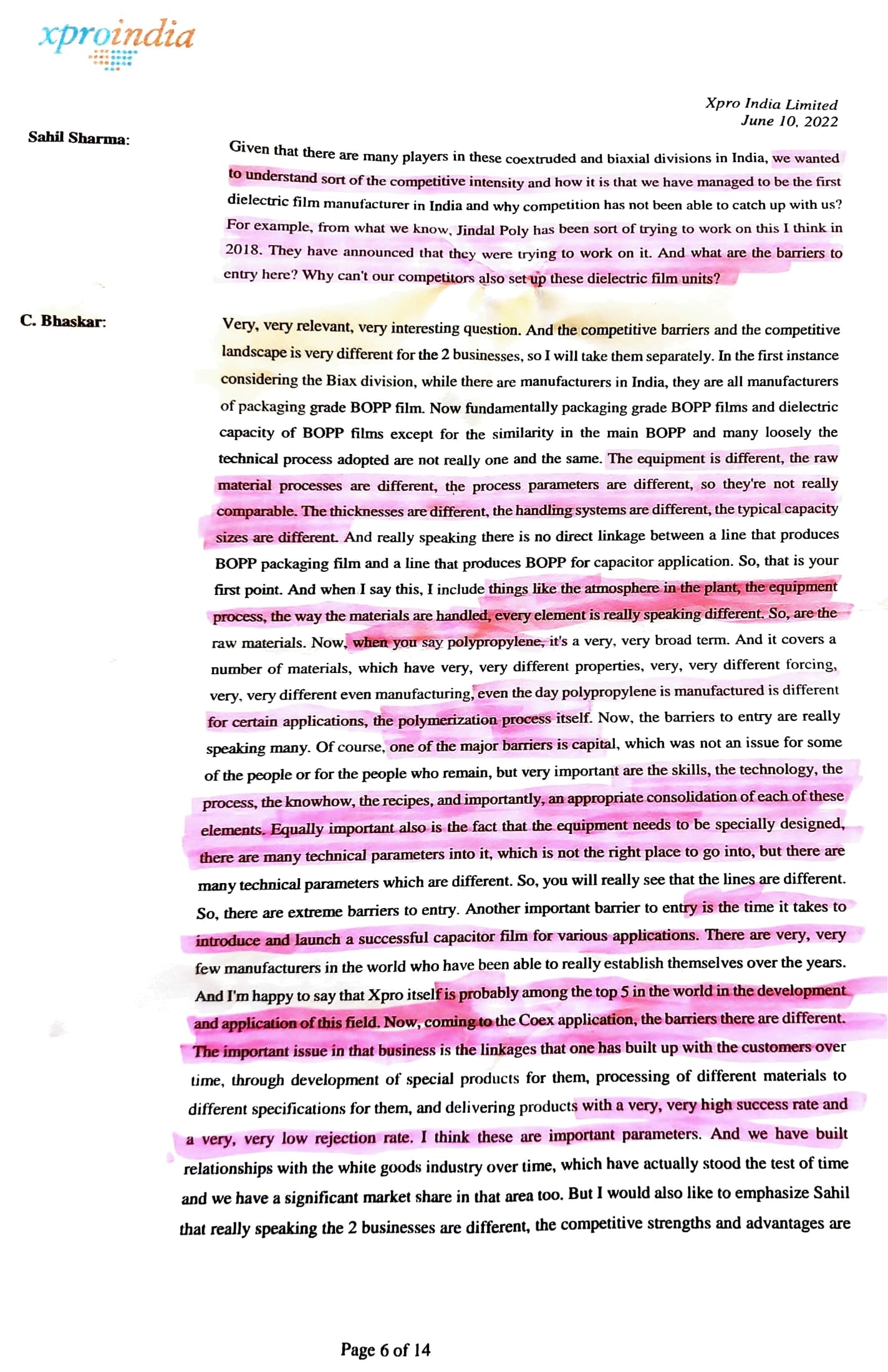

- what i learned from Munger: High ROCE/Moats: Business is a competition for profits. From competitors, substituors, suppliers, clients. Even unrelated businesses. Netflix says, day trading is cvompetition for me. Thus, it is extremely important for us to understand the durable competitive advantages of the business we are owning because without that, it is simply an exercise in google sheet forecasting & not in thoughtful prediction. Of course, tailwinds change. Competitive intensity changes. SRF setting up capacitor film lines. Cosmo getting into metallizing first, and aspiring to set up capacitor film lines. All of these are direct attacks on Xpro’s business. They need to defend. We as investors, need to anticipate & prepare for such attacks by understanding whether our business can withstand such attacks before they happen. Xpro investors might think today, whether the terminal value goes down, whether margins erode. Ive been thinking since before i invested. My understanding as it stands today, is that for at least next 3-4 years their competitive advantages are in place & secure. What happens after 3-4 years is anyone’s guess. I am as eager to learn. But in mean while the profits can grow 3-4x for xpro & moeny will get made already. This reasoning has to happen before the investment, & is powered by understanding of what makes the business unique & difficult to replicate. THis is an evolving picture. My understanding of what makes RACL unique has also evolbed over last 3 years of owning it, and definitely hellped by the plant visit we did recently. Similarly, Saregama, shivalik, xpro, aurionpro, racl are all companies with high moats/competitive advantages built over years. But one has to track their evolution over time. It is NOT enough to buy & forget it, as they say. ANy such cognitive or real world short-cut is sure to reduce our XIRR. Understanding what are the unique capabilities & value addition activities done by the business is key to understanding why ROCE is sustainably high that this is also a key variable in determinign the stretchability of valuation (kitna uupar jaaayega).

- What i learned from stan drukenmiller: Ability to take decisions with partial information, specially in environments where markets are stretched, companies will move on purely narrative, so its important to pull trigger first, with say, only 70% thesis formed, and to be willing to change my mind & sell if i learn facts which are enough to weaken the thesis (in the following days, weeks, months). Necessarily in such a style churn is high. But unless i have a decent net worth invested, i dont have enough skin in game to go deep enough to understand the company best. Chase managements, distributors, suppliers to learn more about the company.

- what i learned from fellow investors like @sharemarketgen_ : Unwillingness to take a business drawdown. if i see slowdown in business, then i must sell regardless of how much i like the underlying business & its competitive advantages. This is also somewhat similar to technofunda style which many folks practice. Shivalik, saregama at high PE + slowdown in growth are a sell at least in my framework.

I am very selective in set of companies i invest in, because i demand all of these characteristics to be present in the company i invest in Many ideas come & go, most are ignored/discarded.

Element of luck. What is luck?

Of course, all these are possible due to the pitch we play on, prepared by Modiji, Yogiji i am fortunate enough to be able to find so many amazing companies despite having a strict criterion because of the awesome economic conditions we have right now in our country flowing from the awesome political conditions. Politics is upstream from economics & must be understood. The reason we have strong growth, improving logistics, improving law&order, are all due to great policies. On the other hand, poor policies such as excessive freebies which encourage uneconomic behavior from populations (this is always a fine balancing act, there is no right or wrong here) is extremely detrimental to the economic health of a unit of population & thus must also be tracked equally closely. The reason i need to understand & appreciate these facts is because they create the economic & market conditions which allow me to follow my process. The reason i can choose to discard companies growing at 15% the reason i can follow a strict process of seeking every condition i have outlined above, is the policy framework of where we stand. CHoosing to turn a blind eye to this, is detrimental to our overall understanding of markets because it makes us overestimate our skill & underplay the luck involved. The reason i can invest in so many great companies is because i happen to be in the right place at the right time today. Tomorrow, if facts change, i would definitely need to adjust/relax my process too. And i am more than willing to do that.

Current portfolio (subject to change any time)

Current portfolio with thesis (in order of decreasing allocation):

1.Aurionpro: Started out being a turnaround play (management change, ashish rai a leading professional who left his job being MD of at FIS, APAC+MEA to buy a 10% stake in a co to turn it around, plug the accounting holes, create world leading IP for creditTech right here in Bharat & take it to the world)

2. Angel one: Discount Broking in India is one of most misunderstood businesses now. It is not cyclical in the traditional sense. The F&O volumes keep going up. at 11x earnings + 4% dividend yield this was a no brainer. There are management actions to keep increasing terminal value of biz by leveraging the digital first distribution they have built.

3. XPRO: Only domestic manufacturer of capacitor films with large & growing Bharatiya & global TAM. Import substitution using capex they are doing in FY24/25/26 will play out, it is difficult to replicate the setup due to customization & configurations involved. This is a complex machine. Some risk to terminal value in case SRF succeeds, but that is itself 4 years out. I expect profits to grow 3-4x in meanwhile.

4. Shilchar: One of best transformer cos in the country if we see their execution track record. Best in class margins, ROCE, growth. Healthy mix of renewables led capex. healthy mix of exports which is higher margins. Key advantages on supplier side. Deeply cyclical sector so need to be very closely tracked. Large demand, lead times in both USA & India leading to strong order books. Strong guidance in AGM as well of 800cr revenue in 3 years.

5. PDS: A very unique sourcing platform for global retailers & apparel brands. Unique acquisition/hiring techniques leading to a culture of innovation & excellence rather than internal politics & decay (can totally relate to this fact given i work at a large corporate). Guidance to increase PAT 3x in 5 years. valuations are not very demanding if one normalizes for margins & interest costs.

6. NPST: Relatively recent co i started studying. very interesting line of business. They are the TPAP & TSP which enables payments in UPI stack by providing payment APIs to payment aggregators such as AirPay, CashFree (think of these as the lower sized competitors of razorpay, ccavenue, billdesk) for P2M transactions. There are no fintech competitors in this space (only banks like hdfc, sbi, axis) which makes it a blue ocean. And the fact that they had the vision & courage & foresight to venture into this business even before UPI took off during covid, tells us about the management capabilities. Very good business model which is clear in the profitability & fast market adoption of their solutions.

About 70% of portfolio is invested in above 6 positions.

PS: Please do not overindex on any companies i have mentioned because i am liable to sell them at any point if i find better opportunities without prior notice. I am not a SEBI registered advisor. Do your own due diligence before investing in any companies. It is your risk capital. Your gains, your pains.

")