Coverage initiation report by Prabhudas Lilladher

3 Likes

I have prepared a detailed business analysis of Safari.

Covered detailed business and competitive analysis for the company.

Industry construct, near and long term growth trigger.

Financial performance and Valuation.

5 Likes

Disruption Series by Ambit Asset Management

How Safari Industries has disrupted the Indian luggage Industry over the past decade and probable challenges it may face during its evolutionary phase.

3 Likes

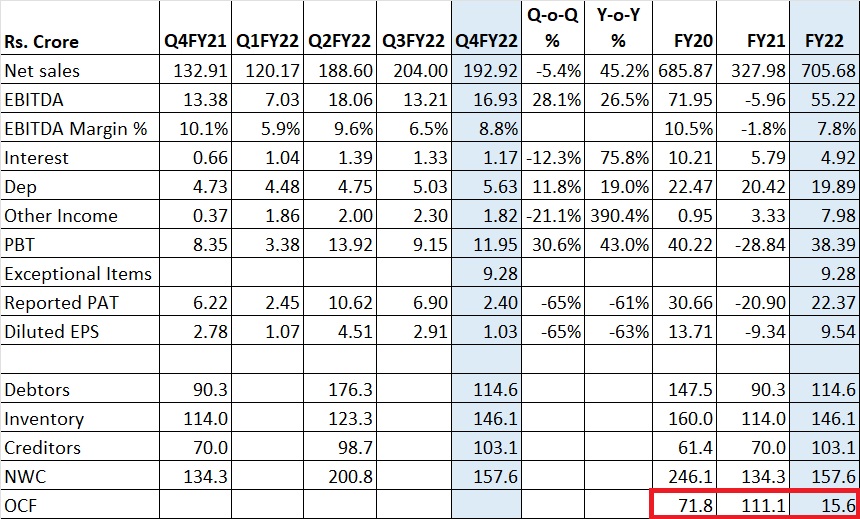

Q2FY22 Results – PAT impacted due to exceptional loss; sustained positive OCF is comforting

Safari’s top-line, though declined 5.4% QoQ due to Covid impact in Jan & Feb months, was at satisfactory level. EBITDA was also at comfortable level, though inflationary pressure is evident from YoY margin decline. PAT was impacted due to Rs.9.28 cr provision for doubtful debts (likely to be exposure towards Future Group). This exceptional loss was the key negative surprise for the quarter.

Demand outlook is healthy given revival in travel & tourism and expected strong marriage seasons. Significant expansion in the distribution network and no of SKUs in the last few years, should help Safari in achieving superior topline growth. Such strong industry environment should also help in passing on higher input cost to the customers.

I believe, biggest positive development for Safari during FY22 is tight control over net working capital (NWC). Despite 2.2x revenue growth over FY21 and 3% growth over FY20, NWC (Debtors + Inventory - Creditors) was only marginally higher than FY21 and significantly lower than FY20. With this, OCF was positive during FY22, despite significantly higher revenue. Though FY22 OCF was significantly lower than the previous year, this was bound to happen due to 2.2x revenue growth.

While the management had been indicating about focus on cash flows; there was lack of visibility given continuously negative OCF till FY19. With the demonstrated performance on cash flows over last 3 years, Safari’s has potential to grow both in terms of revenue and cash flows in future, as compared to only revenue & profit growth achieved till FY19. Upcoming plant at Halol with capital outlay of Rs.50 crore should also reduce the company’s import dependency and inventory levels.

Volatility in raw material prices and competitive intensity will remain key monitorable for medium term.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

5 Likes

I can summarize it in 3 words “All is well”.

I will be posting less about Safari now as I believe that this stock does not require intensive active tracking and its part of my coffee can portfolio.

When I bought the stock for first time, while I was convinced about industry growth prospects, Safari’s capability to achieve superior growth as compared to its peers and clean governance; I was still tracking it closely as I wanted to scrutinize it more thoroughly. This also helped in increasing conviction and allocation over a period of time. Another very critical aspect, where I was less sure was cash flows, as OCF was mostly negative till FY19. However, the company has surprised here with turnaround in OCF since then. With all the tick marks achieved, I will not track it very actively now.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only

2 Likes

I want to pick your brain around it and understand your thesis and learn from your experience

- How do you think the volume growth would be for the next year since they would increase there capacity significantly to 500,

000 units by December 2022. Do you know the current/latest volume numbers? - How do you look at the valuations?

I have not done any such calculation. My investment horizon is much longer and I expect its revenue to grow at 20%+ CAGR for a long time.

I believe that valuation is less important for a very long investment horizon. I’m looking at it from the perspective of relatively small market cap vis-a-vis opportunity size, growth potential and capable management. I do not have any quantitative workings in excel or in my mind. However, If one is looking at it from near term perspective, broad calculation could be as following:

Assuming ~Rs.1050 cr revenue and ~Rs.90 cr PAT for FY23E, stock is available at ~3x EV/Sales and ~35x PE. You can tweak it as per your assumptions.

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only

4 Likes

on the top of the latest results and capacity addition if they can continue growing revenue, then you could see a 4x easily…1.5x current quarterly rev run rate annualized* 1.5x current npm *1.5 x pe

1 Like

just few points to consider:

- can we do 4x of June Q . probably not because of seasonality .

- can it continue to quote on this valuation - may not be.

i would love to proved wrong on above point if co keep growing 30% on revenue side and improves margin .

Agree. Growing at June rate would be hard considering seasonal volatility plus valuations are too rich. As far as margins are concerned its a comparatively inefficient player so expecting 9% margins before 3-4 years is a little over optimistic.

1 Like

@GautamBafna, can you please share Conference call transcripts/audio clips files or location?

I see that they regularly give intimation to Exchanges regarding Investor meet, however, the transcripts or audio clips are not available on their own website, BSE website or screener.

Thanks.

They do not do quarterly investor concalls. Exchange intimations are regarding one to one or group meetings with institutional investors and transcripts/recordings for those are not available. I have also never seen the management on business news channels too.

Only management interaction available publicly are AGM recordings and B&K fireside chat (link posted above in this thread). Though its bit dated but interesting one to understand the business and management thought process. For recent updates, I generally refer to brokerage reports.

4 Likes

Insightful deepdive by CNBC on Safari. More interesting because management rarely appears on business channels

4 Likes

Thanks @GautamBafna for the link. Management should consider doing concalls, its a fairly large company for its industry. Notes from the interview

||1. 20% market share

||2. Company expects industry to grow at 15% and definitely expects to outgrow the industry growth in line with the past performance

||3. Not seeing any demand slowdown currently. Prolonged marriage season has been one the factors in that

||4. Current capacity of 525k. Next year may look at adding 100k or so of capacity with investment of 30-40 crores

||5. Asset turn of 1:5

||6. Last tear capex of ~100cr created employment of ~2000cr. One of the rare industries with such effect. Have approached Rajasthan government with this data for next years plant

||7. Didn’t layoff a single employee during covid. Instead paid full year bonuses.

||8. Gross margin almost at pre-covid levels, should stabilise at 42-44%

||9. EBITDA margins should stabilise at mid teens

||10. Safari not on the block for any buyout, no matter the size of the check

||11. Promoter holding will not be diluted further.

||12. Will look at making significant impact in the premium segment in the next 5-10 year. Should be 20-25% of portfolio

||13. Online sales contribution of 20% or so is stable.

||14. A&P as percentage of sales is and should be around 4-5%.

||15. Company doesn’t spend much on traditional media, but there has been lot of spend on point of sale

||16. On question of market share Mr Jatia said, let’s try to divide the pie in 3 parts and then we will see from there.

7 Likes

Quality Growth

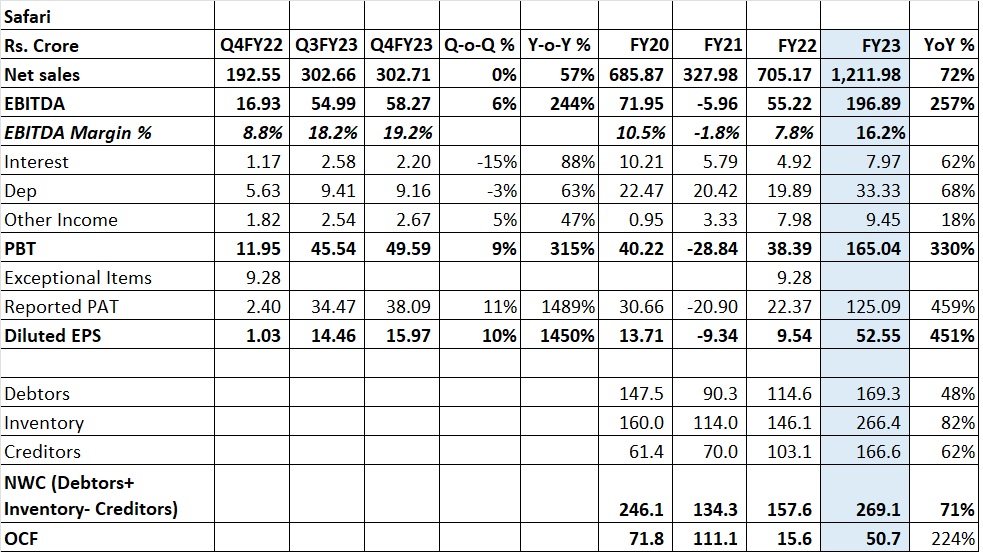

Quantitative growth has been a consistent track record of Safari (except for covid period). However, growth quality in terms of industry leading margins and positive OCF come as positive surprise. I think benefits of capacity expansion and operating leverage are yet to playout as margin expansion seems to be more due to change in sales mix and decline in input costs. This could provide buffer for continuation of aggressive sales strategy in future. OCF/EBITDA for FY23 optically looks low; this is still good considering 72% revenue growth during the year and cumulative OCF of Rs.249 crore for FY20 to FY23, which is 78% of cumulative EBITDA. I believe both Industry leading margins resulting in earnings multiplying and positive OCF during last 4 years despite high growth trajectory are beyond anyone’s expectations (including mine).

Between FY19 to FY23, VIP’s revenue has grown just 1.17x times and Safari has grown 2.1x. Safari has proven itself on all the counts and market has rewarded Safari for the outperformance. While believers of VIP still have faith due to its leadership position, market has differentiated due to muted revenue growth and loss of market share.

What Next?

- Further capacity expansion, built up of large inventory base (Rs.266 cr as on March 31,2023) and industry tailwinds indicate possibility of continuation of growth trajectory

- Possibility of superior OCF growth on low base

- Operating leverage from increased share of inhouse manufacturing and overall size

- Stated intent to enter into premium category opens up new growth avenue

Key Risks

- Increase in input prices in future

- Any moderation in industry growth

Disc: Invested. I am not SEBI registered Advisor/Analyst. The information provided above is for education purpose only.

8 Likes

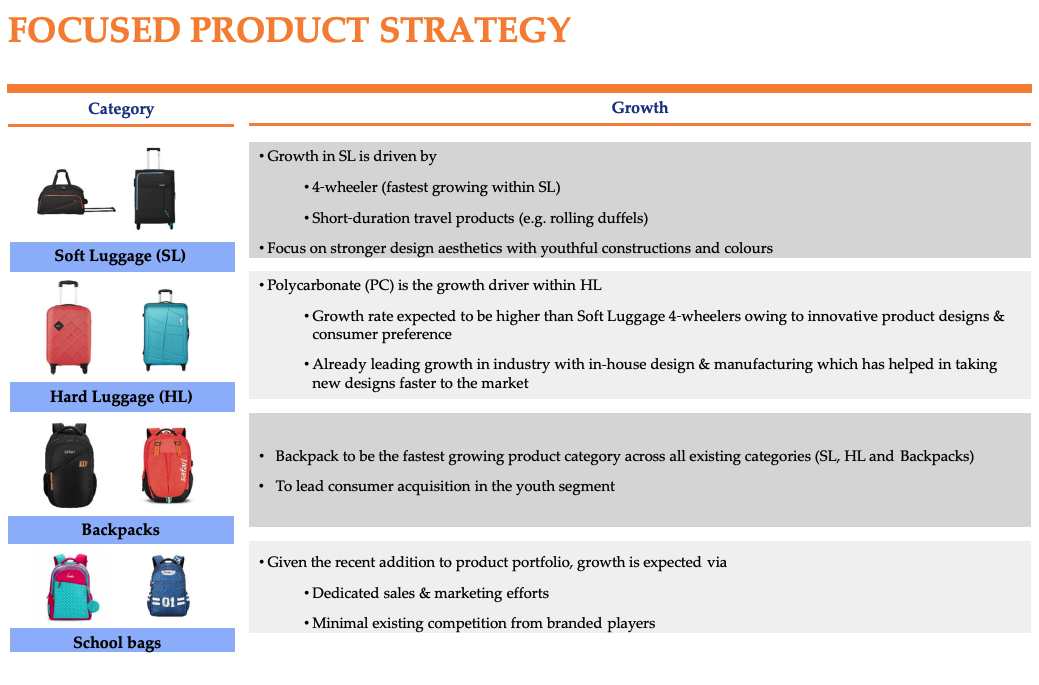

Safari has already forayed into premium luggage category under “Urban Jungle” brand.

The company has tried to differentiate by properly highlighting the key features

As both no 1 and no 2 have multiple brands, addition of new brand and product range to cater to all the segments were very much required for the company’s aspirations.

7 Likes

My notes from the annual report 2023.

- Growth in travel has sustained beyond the post lock-down revenge travel phenomenon, indicating perhaps a more permanent trend.

- The demand in the backpack segment, which was the last to recover post-pandemic, has been very strong during the year led by opening of schools and offices.

-

- Most offices now require physical presence either full-time or partially

Segments:

-

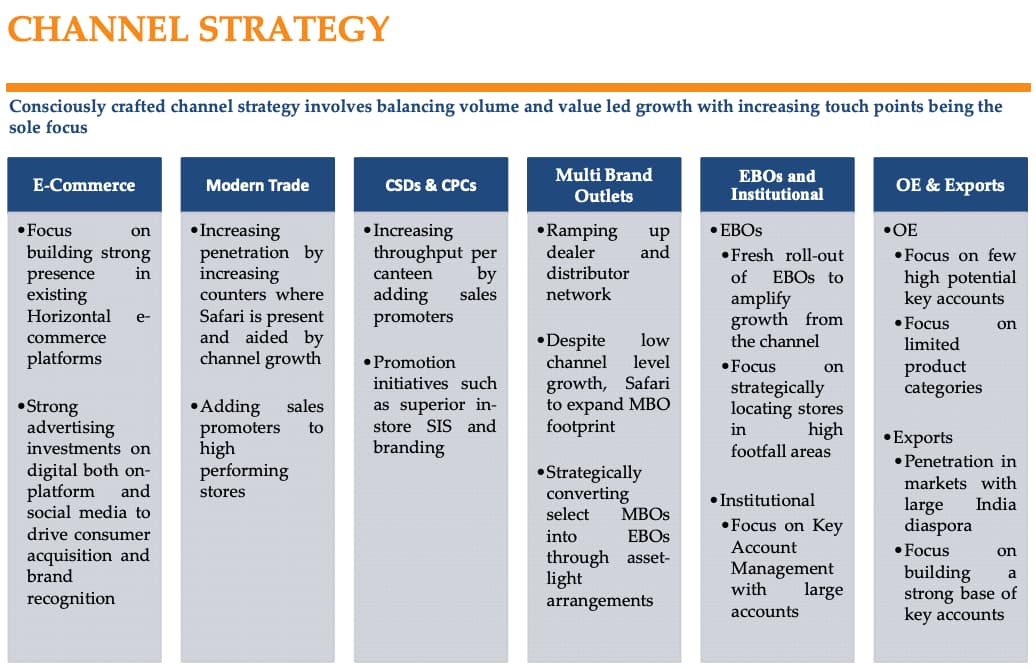

The E-commerce channel continued to lead the category growth with continued trends on increasing digital penetration, e-commerce adoption for higher ticket purchases & deeper geographic penetration.

-

In Hyper channel, value retailers continued their strong growth in the category further helped by a jump in outlet addition.

-

The General Trade channel segment also grew well as organised companies offered better pricing to channel partners, translating to more competitive consumer pricing.

-

The demand in the Canteen Stores Department segment was stable during the year.

-

In last one year the premium segment has bounced back strongly, driven by increasing affluence and increasing consumer preference for better-featured products. This trend is expected to continue over the foreseeable future.

-

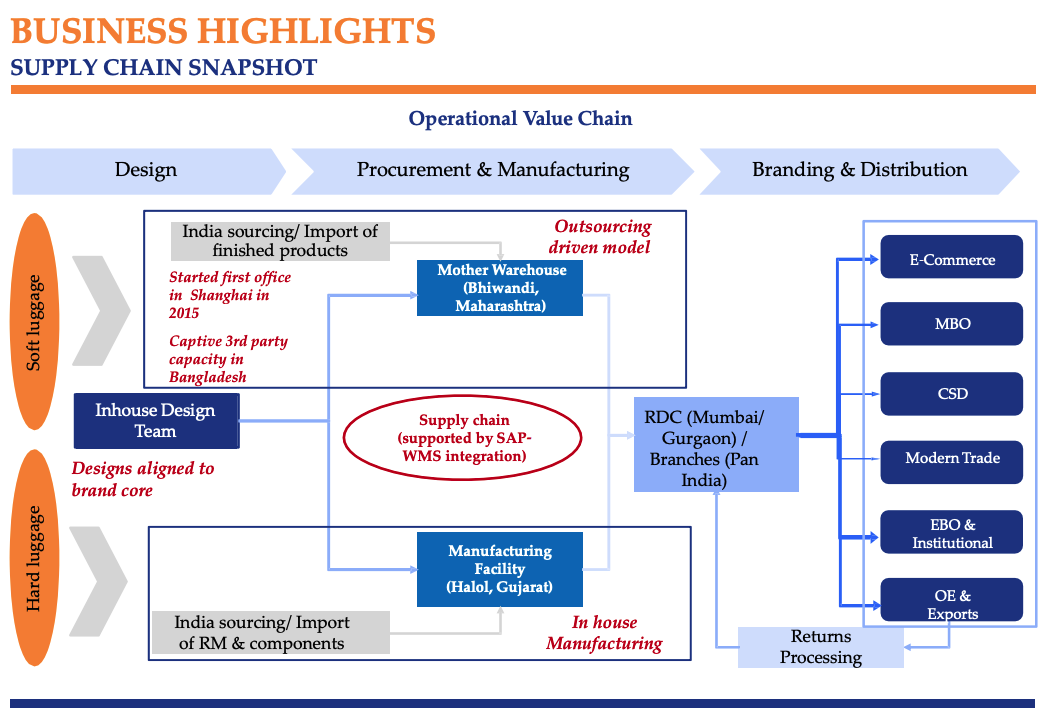

In order to meet the rising demand for hard luggage, the Company has set up a new manufacturing plant through Safari Manufacturing Limited, wholly owned subsidiary in Halol, Gujarat for production of polypropylene zippered hard luggage.

-

expanded its production capacity for polycarbonate zippered hard luggage in the existing manufacturing plant

-

The Company introduced a new brand, Urban Jungle, in the casual premium segment.

-

This brand will initially focus on the zippered hard luggage category. With a strong focus on engaging younger consumers and driving growth with digital shoppers, the Company is focussing on scaling up the Direct to Consumer business through its own brand websites i.e.

-

- www.urbanjungle.shop

-

The Company will continue its efforts on building its brands via a strong advertising presence on digital platforms.

-

To enhance its physical brand availability and recall, the Company added several retail stores in prestigious high-footfall locations. These exclusive retail stores have helped improve the premium sales mix as well as drive better brand equity with the consumers.

-

The International Business division of the Company has gained good traction in several global markets, especially the West Asian countries with large Indian diaspora taking advantage of the latent equity of the ‘Safari’ brand in this segment.

-

a structural shift towards domestic manufacturing has also helped manage the margins better.

-

The Company has significantly increased its procurement of soft-luggage and backpack categories from domestic market and Bangladesh, the sourcing locations continue to be more cost competitive compared to China.

-

With e-commerce continuing to be a lead growth channel and consumers moving to digital platforms for content consumption, it is critical for the long-term to invest aggressively in this area for continued growth.

-

Is now investing behind scaling up its own brand websites.

-

While the overall growth for the domestic economy and travel sub-sector continues to be very strong, the risk of a global slowdown continues to be a demand-side threat. To continue to outperform the market and sustain profitable growth is the most important medium-term challenge.

-

The long period of supply disruption during the pandemic-era as well as adverse ocean freights and currency movement have put imported soft-luggage products at a significant pricing disadvantage versus the domestically produced hard-luggage. This has accelerated the consumer (preference) shift from soft-luggage to hard-luggage, which was already happening, driven by increasing preference for more premium-looking and durable hard-luggage products.

-

The Company continued to invest in zippered hard luggage by continuing to expand its range of polycarbonate zippered cases as well as launch of polypropylene zippered cases.

-

Backpack: The backpack category had a sharp bounce back in demand this year led by the first full year of physical schooling post the pandemic and rising physical attendance in offices. With huge numeric potential still untapped by the organised sector, the Company is looking to invest aggressively behind this category as a strong growth driver.

-

The Company has also made significant investments in modernising and improving its warehousing capability. The Company has invested in upgrading its SAP system which has a positive impact on operations and value chain. These improvements will help the Company in reducing costs and making its supply chain leaner and more responsive to the changing market.

-

While the pressure on raw material and sourcing costs has eased out in the second half of the year, the Company intends to keep improving price realisation through product mix improvement.

-

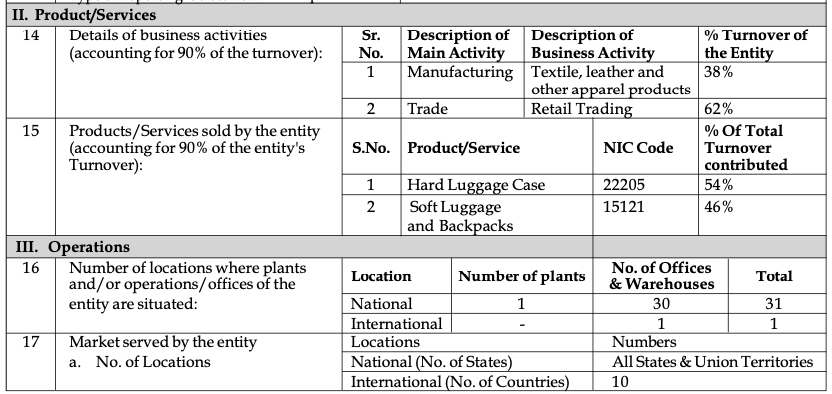

exports as a percentage of the total turnover of the entity = 0.47%

definition of segments:

- General Trade - standalone stores selling luggage, backpacks and other types of bags exclusively

- Modern Trade - large format stores offering a wide variety of merchandise including luggage and bags

- Ecommerce Resellers - companies selling luggage on Ecommerce marketplaces like Amazon, Flipkart, etc

- Canteen Stores - A department with the armed forces running canteens for soldiers. They sell various merchandise including luggage and bags at special rates

- B2B - various organisations doing one-off bulk purchases for employees or their own customers

- D2C - consumers directly buying from the Company’s websites

Risks :

The major risks as identified by the Company are

- demand-risks due to recessionary trends in the global economy,

- currency risk associated with imports,

- unfair competition, etc.

Going through their strategy presentation from 2021, they have remained focused on the growth areas. a few slides that are useful from that I have pasted below:

10 Likes

thanks for the detailed notes. Checked reviews of their products and brands on Amazon, their website. Company is building strong brands in school bags, backpacks (genie); premium luggage(urban jungle) and safari is already reknown brand. USB charging port, 30 days return policy, luggage organiser, premium designs I think are working well for the company. The management is continously expanding capacity and having strong focus on tier 2 and below markets. Having established safari in the sub 3500 rs. luggage brand now the focus is on acquiring premium customers as well. Brand is giving tough fight to samsonite, AT, Skybags as per customer reviews.

4 Likes