Safari industries has recently made a preferential allotment to Malabar investment funds at Rs 340 (post split). Malabar funds will put in 51cr for a 7.09% stake in the company

Sudhir Jatia - earlier MD of VIP took over the reins of Safari in 2011-2012 buying out the owners stake. The deal was facilitated by JM Financial . An interesting story about how Rajeev Chitrabhanu ( MD & CEO of JM) made that happen can be found here.

Further, in July 2014 - Sudhir Jatia & PE fund TANO capital infused money into the company (~70cr) through issue of warrants to the promoter ( all of which have been converted since then) & preferential allotment to Tano at Rs 600 per share (BSEINDIA)

Post this infusion the company took some strategic steps in reviving the brand by incorporating a wholly owned subsidiary called Safari Lifestyles to carry on business of retail trade in travel products and related activities and in 2015 it acquired the trademark and goodwill of the brands ‘Genius’, "Magnum’, ‘Activa’, ‘Orthofit’, ‘DBH’, ‘Egonauts’, ‘Gscape’ and ‘Genie’ owned by Genius Leathercraft Pvt. Ltd.

Thie strategic thought process seems to that adopted by VIP Industries which has 6 core brands and some of them have been similarly acquired.

Of particular note is that when Blowplast ( the marketing & distribution arm ) was merged with VIP Industries ( the manufacturing arm ) , Mr Jatia was the MD of Blowplast indicating that marketing & distribution is his forte. When the impending entry of Harvard educated Radhika Piramal into VIP as the MD became clear, Mr Jatia resigned as the MD. You can read more about it here. and here.

This background is important as Mr Jatia since then took over Safari and has transformed its fortunes and now is a serious competitor to VIP taking away market share from it. However, its still early days for Safari but the business rivalry between both the companies is intense & fierce esp in context of the historical background & there are no prizes for guessing who is winning.

Some data points

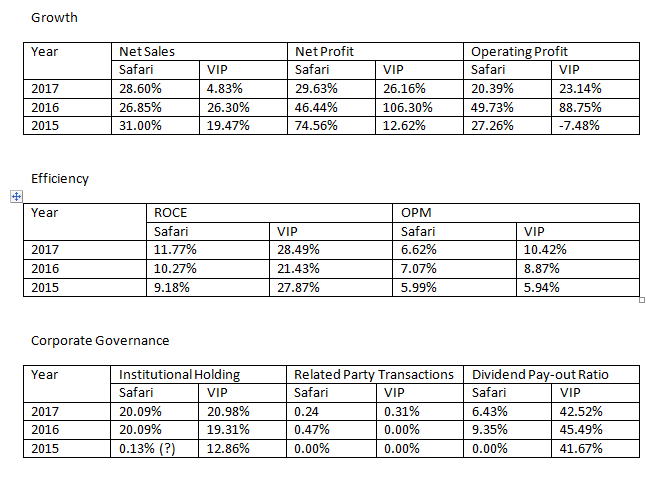

Since 2014, Safari has posted topline CAGR of 29% while VIP is at 9%

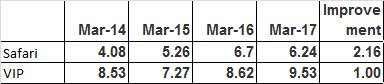

Operating margins of Safari have increased by 2.16% while VIP has managed to increased it by 1%.

Debtors days while still high for Safari compared to the more established VIP, has reduced by about 9 days since 2014. The impact of this is clear as the company turned CFO positive for the first time since 2014 compared to VIP which has always been positive.

Details about the overall luggage market can be found in the Safari investor presentation here

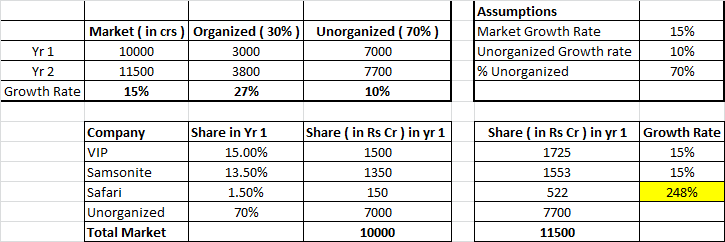

Some relevant numbers are that the overall luggage market is 23% luggage & 77% bags. Both put together did 138 million units in 2016 with 32 million units of luggage. These 32 million units had a value of 91 billion or 9100 crores. Safaris market cap is about 800 crs & VIP is 3500 crores. So the opportunity size is large enough.

A large part of this sector is unorganized & the unorganized sector constitutes about 70%-80% which kind of matches with the sectoral numbers put out by Safari in its presentation. VIP has a market share of about 50% & did 1300 cr of topline, meaning the organized market is 2600 crores which puts the total market size at 11000 crores ( assuming 70% unorganized ). So its safe to assume between 9000 to 11000 crores of size with the bags market as an optionality.

In addition, the sector is growing at a fast clip.

The numbers put put by the tourism department indicate that domestic tourist visits are growing at a CAGR of 13% over a 15 yr period ( from 220 mil in 2000 to 1613 mil in 2016 ) . This means more luggage needed. You can find the report [here] & look at table 18 (http://tourism.gov.in/sites/default/files/Other/english%20India%20Torurism%20Statics%20020917.pdf). In general travel & tourism is posting good growth rates with several companies connected to this sector posting good numbers lately.

The overall sense is that there are a lot of tailwinds for Safari.

Risks

- 80% of the sales are soft luggage which is imported from China so currency risks remain due to overdependence on China

- raw material cost fluctuations

- 28% GST in luggage. The VIP AR mentions that it will have the reverse effect of migration from organized to unorganized & will certainly lead to an increase in prices

- up against VIP & Samsonite - formidable competitors with an established brand position occupying 90-95% of the organized market.

- Amazon - this is a product that can easily be amazoned so that is a certainly a big risk

- Valuation risk ( one needs to take a call on whether there is a margin of safety )

On the technical front - there is a cup n handle breakout today on the charts.

Best

Bheeshma

Views and criticisms welcome

Disc-Invested