the international travel would take time to pick up but believe me , desi travel would be back on same level. in another 3-4 Q.I enquired ppl in. my circle- the one who had got. antibody did short trip in last two months.i also track youtube travelling blogs and almost all are back on road. the key is who will survive 3-4 Q?I had VIP and Safari both since 2015 but recently. i switched to vip. reason is simple-if i have to bet on one i would go with leader.rightly so vip has outperformed safari by big margin.

Brief Note on Safari

Background

Safari Industries India Ltd (Safari) incorporated in year 1974, is the 3rd largest player in Indian luggage industry. The company’s products include hard and soft luggage, backpacks and school bags. The company’s hard luggage manufacturing plant is located at Halol, Gujarat and soft luggage is sourced from mainly from China and India.

Industry Scenario

- Luggage industry in India has grown in higher double digit in the last 6-7 years. FY21 is likely to be a washout as its fortunes are linked to travel industry. Growth rate should come back to normal level post Covid.

- It’s a oligopoly market with just 3 significant players. Though Safari is 3rd largest player (with less than 20% market share) and has presence only in economy segment, it has consistently gained market share post change in the promoter. Further market share gain and value migration from unorganised to organised (just ~25% market share) segment can help in achieving superior growth.

Management

- In FY13, Mr Sudhir Jatia bought majority stake in the company. He successfully turned it around and made it fastest growing player in the luggage industry. Mr Jatia is industry veteran and Ex-MD of VIP

- He is supported by a team of professionals, who are well qualified and have significant relevant experience. Nevertheless, the company seems to have significant dependence on Mr Jatia.

Business

- While soft luggage is major revenue contributor for Safari, the company also has presence in Polycarbonate luggage, backpacks and school bags. The company has manufacturing plant for Polycarbonate luggage (capacity expanded in FY20) and soft luggage is majorly outsourced. Safari has significant dependence on China for soft luggage, though, it plans to reduce it going forward.

- Safari is the flagship brand of the company, which caters to economy segment. It also acquired Genius, Genie (school bags) and Magnum (mass segment) brands during 2016. Presence in e-commerce and modern retail is at satisfactory level with decent visibility.

- The company has done significant increase in its distribution network over the years with customer touch points (~6000) across diverse channels like Hypermarkets, E-commerce, MBO, EBO, CSD, Institutional etc.

Financial Performance

- During FY15-FY20 period, net sales has grown 3.2x to Rs.681 crore, EBITDA margin has improved from ~5.8% in FY15 to ~10.6% in FY20 and EPS has multiplied from Rs.2.25 in FY15 to Rs.13.64 in FY20.

- Luggage industry has been badly impacted since March 2020 due to Covid and the company’s performance deteriorated significantly with 90% decline in revenue and operating loss during Q1FY21.

| Rs. crore | FY15 | FY20 | Growth (x) | Q1FY20 | Q1FY21 | Growth % |

|---|---|---|---|---|---|---|

| Net sales | 215.93 | 685.87 | 3.18 | 204.04 | 20.12 | -90% |

| EBITDA | 12.56 | 72.91 | 5.80 | 21.53 | -17.90 | PL |

| EBITDA Margin % | 5.8% | 10.6% | 10.6% | -89.0% | ||

| Interest | 2.91 | 10.21 | 3.51 | 2.98 | 2.03 | -32% |

| Dep | 2.89 | 22.47 | 7.78 | 5.35 | 5.32 | -1% |

| PBT | 6.76 | 40.22 | 5.95 | 13.21 | -25.25 | PL |

| PAT | 4.26 | 30.66 | 7.20 | 8.27 | -19.33 | PL |

| Diluted EPS (Rs.) | 2.25 | 13.71 | 6.09 | 3.69 | -8.64 | PL |

| ROE % | 5.6% | 13.3% | ||||

| ROCE % | 8.8% | 16.5% | ||||

| D/E (x) | 0.43 | 0.33 | ||||

| Debtor Days | 68 | 78 | ||||

| Inventory Days | 101 | 85 |

- Current year would be challenging. However, survival during this period is not expected to be an issue. Post Covid, the company should be back to its growth path. No salary cut during the current year; shows strong confidence of the management that business will be back to normal.

- ROE and ROCE of the company are at modest level due to relatively lower margins and working capital intensity, though improved significantly over the last few years.

- During FY15-FY20, cumulative operating cash flows were negative Rs.35 crore. Working capital, capex and acquisition of brands were funded mainly through equity dilution (raised around Rs.100 crore in FY15 and FY18). OCF (Rs.72 crore) turned positive during FY20. Debtor & inventory days have not seen manor change between FY15 and FY20 and negative cumulative OCF can be attributed to strong revenue growth. Nevertheless, market leader VIP’s working capital cycle and return ratios are much better and Safari needs to improve upon these to achieve growth without equity dilution or debt raising in future.

- Auditor of the company is decent (M/s Lodha & Co). There are no questionable related party transactions and salary of Mr Jatia was at a reasonable level of Rs.1 crore during FY20. When his daughter was employed as Sr Manager with the company, salary of Rs.13 lakh was paid to her during FY19 (looks reasonable).

VIP vs Safari

VIP has much larger distribution network, brand portfolio and scale. Also, VIP’s working capital cycle, profitability and return ratios are superior as compared to Safari.

However, it is remarkable that Safari has been able to give strong challenge to VIP by continuously eating its market share despite limited resources. There has been continuous improvement in business as well as financial indicators since takeover by new promoter and growth has been much higher and consistent for Safari. Also, as compared to VIP, Safari appears cleaner in terms management actions and related party transactions.

FY21 will be surely challenging for the luggage industry but long-term prospects appear striking. Market cap of Safari is just Rs.890 crore, which looks very attractive considering oligopoly industry with double digit CAGR potential for a long period (post FY21) and Safari’s track record of above industry growth rate. Apart from sales growth; any improvement in profitability, working capital and return ratios towards market leader VIP, can be icing on cake in future. While it is difficult to ascertain possible improvement on these parameters currently, management track record of rebuilding this company step by step, does raises hope from a long-term perspective.

Views invited

Disc: Invested. This is for education purpose only and not a recommendation.

14 Likes

Looking at the financial numbers, I think they have intentionally kept profit margins lower than VIP(& Credit period high) to acquire market share from them, The day they will go for increasing margins growth will go down.

So, I expect return ratios always to be less than VIP.

The day VIP reduce their prices to retain market share, stock will be de-rated and margins/growth will also go down.

Their WC requirement is high, so they will keep diluting equity as they grow.

I would have like to own this business if it had some inherent moat/pricing power.

My notes from Safari Annual Report 2019-20:

-

Established brand in the luggage industry: The organised Indian luggage industry is oligopolistic in nature. Safari gradually improved its market share and revenue grew at a compound annual growth rate of 27% over the three fiscals through 2019. A pan India distribution network, comprising over 3,500 customer touch points, and an established product portfolio, further strengthen its market position.

-

During the year the E-commerce channel continued to grow well with increasing digital penetration and increasing shopper maturity to make higher ticket purchases online. Hyper channel growth saw some moderation with a slow down in new store openings. Muted growth was seen across general trade and retail channel with changing shopper behaviour. Canteen Stores Department is the only channel that did not witness growth during the year.

-

The COVID 19 global pandemic has impacted overall consumer demand across industries, but its impact is expected to be more severe and longer lasting in travel related industries. The consumer demand in the sector is expected to be muted in the medium term. While the timing and extent of bounce back on demand is difficult to predict, the Companyis focussing on tightening its cost structure and streamlining its supply chain to ensure all resources are optimally used. The Company will also invest selectively in consumer demand in selective channels to maximise sales in the segments that bounce back earlier

Hard Luggage Segment (Polycarbonate):

-

Significant growth was observed in the Polycarbonate zippered case category, due to an accelerating shift of consumer preference away from Soft Luggage to more durable and premium looking hard luggage. The Company is prepared to tap into this opportunity by introducing a wider range of Polycarbonate zippered cases and enhanced production capacity at its manufacturing plant in Halol, Gujarat.

-

The Company increased its thrust on Polycarbonate zippered case category in line with shifting consumer preference away from soft luggage. It continued to increase its polycarbonate ranges with a focus on upgradation in terms of features, design and price to drive strong share growth.

-

The Company discontinued its product ranges of framed hard luggage, made of Polypropylene given the lack of consumer demand in this category. The consumer preferences have shifted away from traditional framed hard luggage towards the convenience of light and four wheeled travel products.

Backpack Segment:

-

The Company continued to grow well in the Backpack category with an umbrella-brand Safari and sub-brands like Genius and Genie, that ensures that all major consumer segments have a relevant offer

-

The Magnum brand continued to grow well with an enhanced product portfolio targeting mass market value seeking consumers. The Genie brand continued to innovate with a wider range of feminine designs targeted specifically at teenage and young girls. The brand grew well in the Backpack category and also forayed into a wider range of accessorised bags. The Genius brand widened its product portfolio to include innovative Backpacks targeted at toddlers and kids, expanding its target segment to all young boy. This is in line with the company’s strategic intent targeting the high-growth Backpack market with multiple brands targeting specific consumer sub-segments.

Cost/Margin consideration:

-

To diversify its supply chain and reduce costs, the Company is also increasing its outsourcing of soft luggage and backpacks from India and Bangladesh (China accounts for 64%). These improvements will help the company in reducing costs and, making its supply chain leaner and more responsive to the changing market.

-

The Company continues reaping benefits of implementing SAP system which has a positive impact on operations and value chain.

-

In addition margins may continue to experience pressure on account upward pressure on buying costs due to currency exchange rates and import duty, etc. To pass on these cost escalations, the company took a price increase for its certain products last year.

-

Imported Soft luggage and Backpacks are a major contributor to the sales of the Company. During the year, there was increased upwards pressure on buying costs of imported products from China due to adverse exchange rate movements. The Company has started hedging its foreign exchange exposure to mitigate its risk arising out of foreign exchange fluctuations. The Company continues to leverage its increasing scale to limit sourcing cost increase. The Company is also increasing its domestic procurement of Soft luggage and Backpack categories, apart from scaling up the revenue mix from Polycarbonate Uprights produced at its plant in Halol, Gujarat.

My Take:

Cons:

-

Goes without saying, FY’20 is a washout year for company considering the discretionary/travel driven demand

-

Though working capital intensity has came down (say ~50% WC/revenue for FY18 and 19 to ~40% for FY’20), however this still is lot of capital guzzling. To keep the revenue growth momentum on they may have to infuse capital (debt/equity), if not immediately then mid term (unless margins improves significantly).

Pros:

-

Company is growing at decent cliff - mostly attributed to shift from unorganized to organized and eating into competitor turf.

-

Also, management has put its act together on Margin improvement - albite little slow. Operating profit 4.4% in FY’14 to 10.5% for FY’20.

-

Margins are expected to improve further considering shift from soft luggage to Hard Luggage (better realization).

-

Improving A&P spend. 4.39% for FY’20 as compared to 3.38% for FY’19.

-

Working capital intensity is expected to come down a notch further considering soft luggage sourcing to happen from India and Bangladesh as well.

Regards,

Tarun

6 Likes

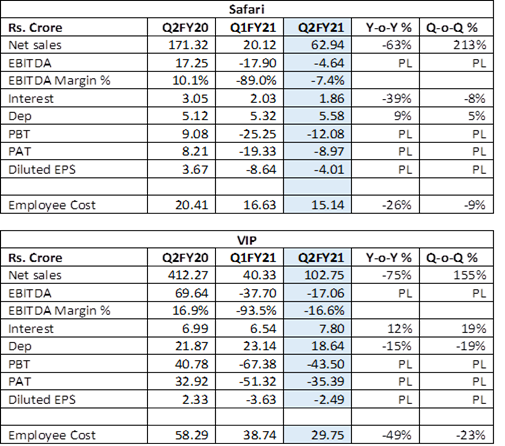

Q2FY21 result update

As the luggage industry derives its entire demand from travel and marriages, Q2 continued to be washout for Safari. As expected, significant decline in scale resulted in loss both at operating and net level. Safari reported 63% Y-o-Y decline in sales, EBITDA loss of Rs.4.64 crore and net loss of Rs.8.97 crore during Q2FY21.

Safari vs VIP - Few interesting points in Q2FY21 results

- Normally leader shows most resilience in bad times. However, story was different here with 75% Y-o-Y decline in revenue reported by VIP in Q2FY21.

- Both VIP and Safari adopted cost cutting measures. Industry also witnessed strong competition due to liquidation of inventory.

- Also, despite huge cut in employee cost and savings on rental cost due to closure of some of the stores, VIP’s operating profitability was impacted more as compared to Safari.

- Steep decline of 49% in VIP’s employee cost is surprising (26% for Safari). In my view, difficult without major retrenchment. This could give more headroom to Safari for capturing market share during recover phase.

- VIP’s management believes that the luggage industry has been pushed back by 2-3 years. Safari’s management believes that worst phase for luggage industry is over and it expects partial recovery in H2FY21 (Source: research reports).

My View

While H2FY21 is expected to be better than H1FY21, results are still not expected to be encouraging due restrictions on international travel, limited domestic travel and postponement of marriages.

However, luggage industry is expected to witness V shape recovery and companies like Safari will benefit significantly due to oligopoly in organised luggage industry. Moreover, competition from unorganised players may come down due to severe impact of epidemic on the industry.

Safari has been challenging VIP strongly by capturing market share steadily. During this worst phase also, it has shown more resilience as compared to industry leader.

Management with a proven track record, strong long-term industry growth prospects (post FY21) with an oligopoly market and superior growth as compared to market leader remain my key investment arguments for Safari.

Disclosure: Invested

9 Likes

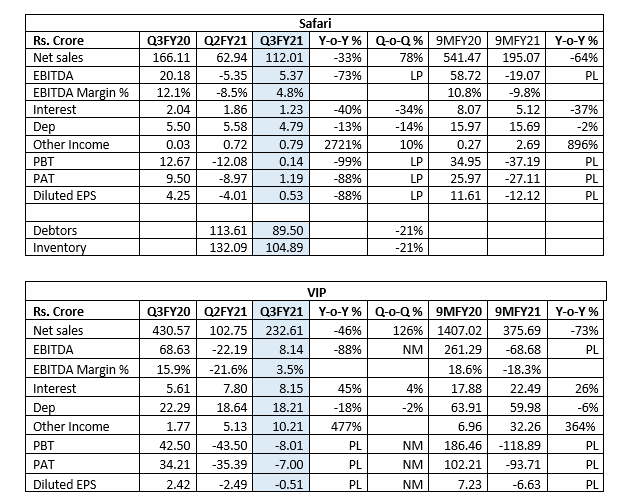

Q3FY21 Results

Luggage industry has been witnessing q-o-q improvement but scale of operations is still significantly lower as compared to pre-covid level due to limited domestic as well as intentional travel. As expected, Safari reported 33% Y-o-Y decline in sales, although it improved 78% on Q-o-Q basis. EBITDA margin was at 4.8% and also PBT was positive during Q3FY21, as comparted to operating loss in Q2FY21. Though profitability remains under pressure due to lower scale of operations, sequential improvement in scale and profitability is comforting. Another comforting factor is continuous improvement in debtor (down by Rs.58 crore in 9MFY21) and inventory level (down by Rs.55 crore in 9MFY21).

Safari vs VIP

• VIP’s financial performance was weaker than Safari’s performance during Q3FY21 and 9MFY21.

• Safari continues to gain market share from VIP. While VIP boasts about significant cost advantage of Bangladesh factory, has stronger brand and products across price categories; the same has not helped it in gaining/protecting market share from organised as well as unorganised players.

• It seems that Safari’s management has been performing better in terms of execution and that could be the soft emerging moat. Let’s see if it emerges into stronger and visible one in the coming years.

FY21 would be the worst every year for the industry and Safari has almost crossed it with no major dent (except for net loss during the year). There is decent possibility of V shape recovery in travel now. Revenge tourism, start of regular train services & international travel (possibly from Q1FY22) and opening of schools should augur well for the industry in short to medium term. New covid nos have already started declining globally and mass vaccination & herd immunity should be the key catalysts helping the travel and luggage industry. Hope story would become number story soon.

Management with a proven track record, strong long-term industry growth prospect (post FY21) with an oligopoly market, superior growth as compared to market leader, relatively small market cap as vis-a-vis opportunity size, makes Safari attractive.

Disclosure: Invested

11 Likes

Entry of MFs

Tano India Private Equity Fund, which owned 5.15% stake in Safari, has exited by selling 11 lakh stocks through bulk and block deals yesterday. Tano was early investor in the company, held about 12% stake earlier and contributed in shaping up Safari in new avatar.

These stocks were bough by Motilal Oswal AMC (800,000 shares, ~3.57% stake) and Sundaram MF (300,000 shares, ~ 1.34% stake). It’s a very interesting development as mutual funds have entered the stock for the very first time.

Other prominent funds/persons owning the stock include SAIF, Malabar Fund, Mr Ashish Kacholia (well known investor) and Mr Rajeev Chitrabhanu (Ex CEO of JM Financials and helped the current promoter of Safari in acquiring it from erstwhile owner).

Disclosure: Invested

2 Likes

Few Points which I would like to share based on my reading Safari -

- Sudhir Jatia was the MD of VIP before building Safari

- FPI/FII limit to shareholding was increased to 49%.

- BoD includes Mr Sumeet Nagar, who is the MD of Malabar Investment – they hold Apollo Pipes, Vaibhav Global, HLE, GMM etc in the portfolio as well.

- BoD also includes Mr Shailesh Mehta, founder and managing partner of Granite Hill Capital Partners. Former Chairman & CEO of Providian Financial Corp. general partner with Invesco funds and operating general partner of Sequoia India.

- BoD includes Piyush Goenka - partner at Tano Capital

- BoD includes Mrs Vijaya Sampath – Former Global Group General Counsel and Company Secretary for the Bharti group.

- Salary hike of KMP was higher than other people. (MD took 22% increase, CFO 14%, CS 13%) Avg hike was 8.79%

- Soft Luggage – 67% of Sales + Hard Luggage – 33%.

- Al Mehwar also a shareholder in the company

- Canteen Stores Department is the only channel that did not witness growth during the year 2019-20.

- The Company discontinued its product ranges of framed hard luggage, made of Polypropylene given the lack of consumer demand in this category. The consumer preferences have shifted away from traditional framed hard luggage towards the convenience of light and four-wheeled travel products.

- To diversify its supply chain and reduce costs, the Company is also increasing its outsourcing of soft luggage and backpacks from India and Bangladesh.

- RONW 14.21%

- In top 1000 companies as per Market Capitalization

- Hard Luggage is manufactured and soft luggage is imported.

8 Likes

Safari Industries has announced that global investment firm Investcorp will invest about ₹75 crore via compulsory convertible debentures. The company’s management hopes to close the transaction in March 2021

2 Likes

I couldn’t able to download the file

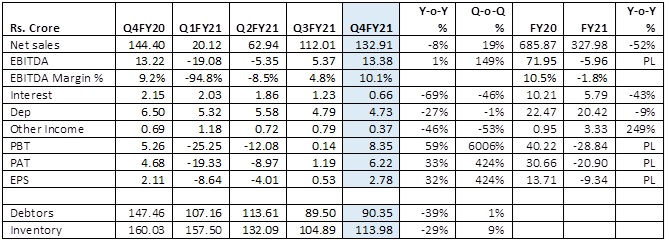

Q4FY21 Results

Although revenue of Safari declined by 8% Y-o-Y and EBITDA was flat during 4QFY21, performance was ahead of expectations. This is remarkable as tourism and travel activities in India during 4QFY21 were at a much lower level as compared to normal times. It appears, Safari has gained from its competitors from both organized and unorganized sector. EBITDA margin improved to 10.1% due to cost control measures, despite steep increase in input costs. PAT improved by 33% on Y-o-Y basis and 424% on Q-o-Q basis.

For the full year FY21, revenue declined by 52% and the company incurred significant net loss due to industry headwinds. Nevertheless, significant operating cash flows achieved through decline in debtors and inventory is comforting factor. Balance sheet has strengthened as the company has significant amount of net cash in books, achieved through recent capital raising and working capital improvement.

With the current resurgence of Covid-19 infections, resultant lockdowns resulting in significant reduction in travel, closure of markets & malls, deferment of opening of education institutions and weddings; sequential performance would again deteriorate.

The overall impact on the company’s performance, though significant, is expected to be transitionary and gradually recovery is likely with herd immunity and vaccination. While there are apprehensions regarding availability of vaccine, data in a recent research report by Investec indicate abundant availability in India likely over next 2-4 months’ time.

Globally, leading hotel stocks such as Hilton, Marriott etc are now trading at or near all-time highs on expectations of a strong revival in the tourism sector. Though we may be lagging international market, luggage manufacturers in India will also witness strong revival as and when recovery in travel and tourism sector starts.

Management with a proven track record, strong long-term industry growth prospects with an oligopoly market, small market cap as vis-a-vis opportunity size, makes Safari attractive. Entry of 2 Mutual Funds in the stock for the very first time and investment by Investcorp during 4QFY21 improves confidence on the stock, despite intermediate challenges.

Disclosure: Invested

9 Likes

Key takeaway from FY21 Annual Report – “Focused, resilient and clean”

Industry Developments

- Demand declined sharply during first half of the year due to COVID 19 pandemic but there was significant recovery especially in luggage segment in the second half led by the opening of economy, festive and marriage demand. Demand in the backpack segment was muted throughout the year.

- The E-commerce channel (Safari already had a strong presence there) saw the strongest uptick in demand. General Trade segment also saw a good revival in demand. The demand in the Canteen Stores Department segment (another important sector for Safari) remained muted throughout the year.

- The pandemic has accelerated the shift from Unorganised to Organised players as many sourcing avenues for Unorganised players such as Chinese imports have become increasingly unviable.

- The company believes that while there is a large degrowth in the industry due to COVID 19 impact and also the second wave of the pandemic has added to uncertainty which is likely to impact revenue in the near term, the overall long-term outlook for the sector remains very robust. As the pandemic is expected to come under control this year with large scale vaccinations, the travel industry is set for an unprecedented boom.

- Growth in backpack segment is expected to remain poor in the medium term, till physical attendance in schools, colleges and offices becomes the norm again. This segment is relatively small currently.

Company developments

- The Company was impacted adversely during the year due to the overall industry slowdown, but it continued to perform ahead of the market.

- During the year, there was upwards pressure on raw material cost and sourcing costs of imported products from China. The Company has started to gradually increase prices for its products to cover the increase in costs and ramped up procurement from India and Bangladesh for cost control and supply security. The Company limited the number of new product launches during the year.

- The trend of rising preference for Zippered Hard Luggage category continued as it is perceived to be more premium and durable. The Company continued to invest in enhancing production capacity of hard luggage at its plant in Halol, Gujarat (net gross block addition of Rs.16 cr).

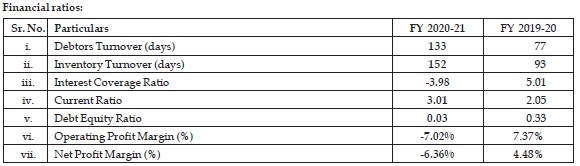

Financial Performance

- Total Income for FY21 was Rs.331 cr (Previous Year Rs.687 cr) and net loss was Rs.21 cr (Previous Year PAT of Rs.31 cr).

- Cost control measures have been taken by the company as visible in reduced employee cost, other expenses including advertisement & sales promotion.

- While there was significant reduction in absolute debtor and inventory level, debtor days and inventory days increased due to reduced scale of operations. The company did write-off of about Rs.9 cr of debtors, which is not alarming considering the stress in the industry. Out of Rs.90 cr of debtors, Rs.78 cr have aging of less than 3 months and Rs.10 cr are more than 1 year old. Overall situation seems fine here.

- Debt was negligible due to reduced working capital requirement.

- Cash flow from operations were Rs.111 crore in FY21 as against Rs.71 crore in FY20. Despite losses, reduced working capital on account of reduction in scale of operation was the key reason for this.

- Net addition in the gross block was Rs.16 crore.

- The company raised Rs.75 crore through issue of CCDs to Investcorp PE fund. While this will result in some dilution, the company now have buffer funds for accelerated growth and future opportunities. Funds were parked in FDs as on balance sheet date.

Corporate Governance

- Board composition in terms of qualification and experience of directors, presence of independent directors etc seems comfortable. All directors except one had 100% attendance in the board meetings.

- Entire amount of CSR requirement was spent during the year despite losses.

- M/s Lodha & Co is the company’s auditor and M/s. Moore Singhi Advisors LLP has been appointed as internal auditor. Both the firms are reputed.

- Increase in auditor remuneration was only due to certification expenses for CCD issue and audit fee remains stable and reasonable.

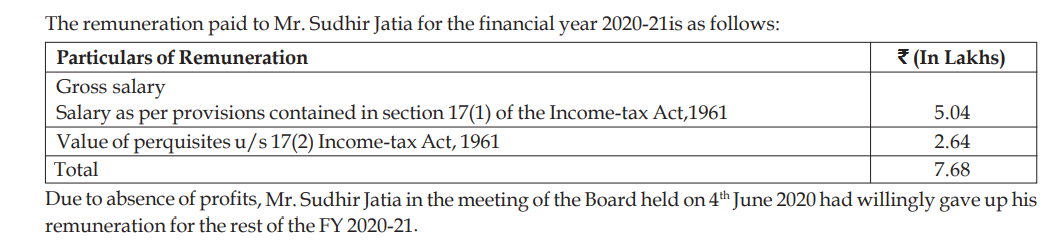

- Due to absence of profits, Mr. Sudhir Jatia in the meeting of the Board held on 4th June 2020 had willingly gave up his remuneration for the rest of the FY 2020-21 and accordingly he received only Rs.7.68 lakh as remuneration.

- Mr Sudhir Jatia’s daughter Ms Tanisha Jatia has joined as product manager from Sep 2020. Remuneration paid to her was Rs.17 lakh, which looks reasonable considering her US education and previous employment in US.

- Related party transactions are absolutely clean with no fund movement/transactions with key managerial persons and other related parties apart from remuneration.

Disclosure: Invested

13 Likes

AGM Notes (Held on August 11, 2021)

Recent performance - While the company has seen strong Y-o-Y performance during Q1FY22, second wave of covid did have an impact. Digital channels have contributed in recovery witnessed during last few quarters. Demand for backpacks is muted due to closure of schools & colleges.

Impact of covid on Distribution network – Digital has become more robust and only marginal impact was there on traditional network. Big Bazaar was one of the important customer-touchpoint and its weakening impacted all the luggage players.

Competitive advantages – Strong brands and capability to supply at competitive rates. Unorganised players were solely dependent upon China and sourcing from China has been significantly impacted.

Growth outlook – Positive outlook and does not see much challenge for near term recovery if covid wave three is not there. Growth prospects for long term are very strong. Competitive intensity is not high in the industry due to limited number of organised players and no major disruption is envisaged in the industry. Does not plan to enter premium segment or new categories in near term but all growth options are open for long-term.

Fund raising of Rs.75 cr during FY21- Funds were raised from Investcorp, which would be used towards brand building, expanding distribution network, production capacity and supplier channel. Funds were raised through CCDs as it was cheapest, fastest and most convenient option.

Has been continuously working upon strengthening leadership team, which is stable and strong.

Disclosure : Invested

10 Likes

4 Likes

Was reading the Annual report for safari and came across the remuneration section:

Note the date: 4th june 2020 i.e during the covid.

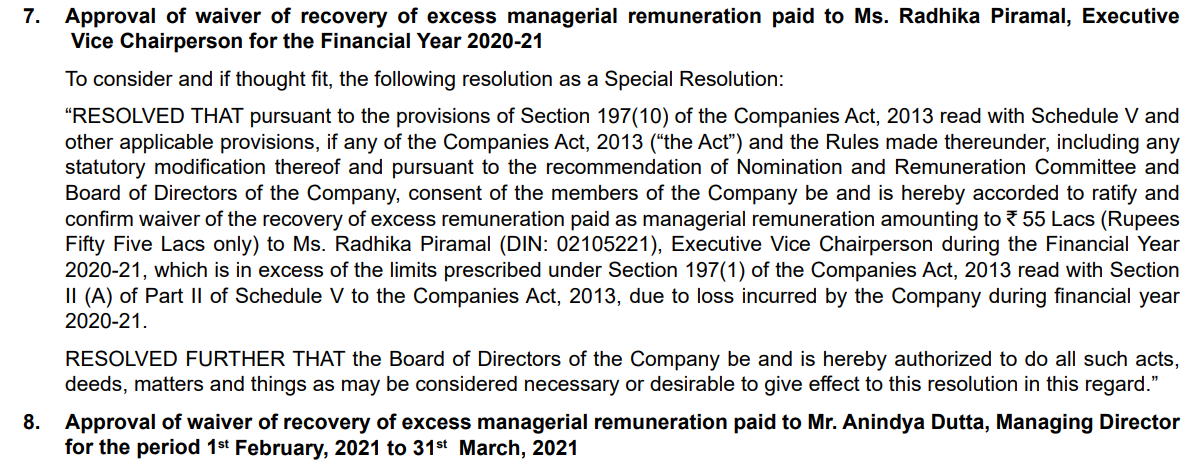

Whereas their peers VIP had to pass a resolution to cut back the excess remuneration paid to the MD and Vice chairman:

Which implies that even after the pandemic had struck and clearly knowing that this business will be hit massively they didn’t cut back on the remuneration.

Hence the promoter of safari is much more in sync with company performance rather than just stripping the shareholders by eating up huge remuneration.

7 Likes

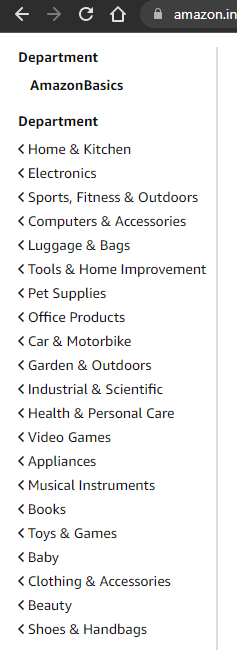

Reuters has broken an incredible piece on Amazon’s private brand strategy.

The documents reveal how Amazon’s private-brands team in India secretly exploited internal data from Amazon.in to copy products sold by other companies, and then offered them on its platform.

Just look at the categories of Amazon Basics products, it includes backpacks and luggage too.

This is a serious threat to many of the listed businesses which operate in the above categories.

Hope the CCI takes major action against these online retailers.

Full article:Amazon copied products and rigged search results, documents show

Additional reading: How the Amazon and Flipkart private labels affect other sellers on the ecommerce platforms

8 Likes

5 Likes

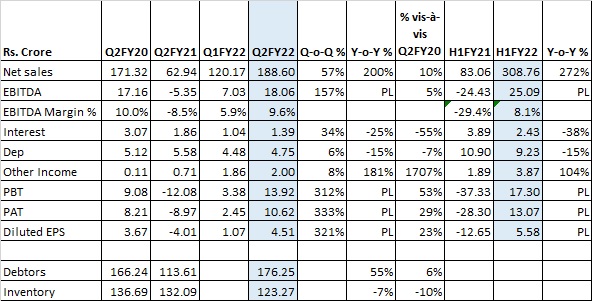

Q2FY22 Results - Impressive Performance

Safari Industries’ Q2FY22 financial performance is impressive, with revenue growth of 200% on Y-o-Y basis and 10% growth over Q2FY20. While all travel dependent companies including airlines, hotels and Safari’s own competitor VIP are somewhere around 70-90% of Q2FY20 revenue; Safari is at 110% in Q2FY22. Safari is consistently able to gain market share as evident from the fact that Safari’s revenue during Q2FY20 was 42% of VIP, which has improved to 57% in Q2FY22.

Despite steep increase in input costs, EBITDA margin stood at 9.6% in Q2FY22 as compared to loss in Q2FY21 and 10.0% in Q2FY20. With this and decline in interest cost & increase in other income, PAT grew by 29% as compared to Q2FY20.

There has been a marginal improvement in debtor and inventory days also.

Safari has announced an MOU for purchase of land and building at Halol, Gujarat for a consideration of Rs.22.51 cr, to be used for manufacturing unit. Recently, both Safari and VIP’s managements have mentioned about increase in-house manufacturing, which should be margin accretive for both.

Luggage market is shifting from soft luggage to hard luggage over the last few years. Safari’s management was able to identify this trend early (as evident from mention of in the last few annual reports, in-house manufacturing of hard luggage and outsourcing of soft luggage), while VIP has recognised this now. Over the last few years, VIP had invested in Bangladesh plant for soft luggage to take advantage of low labour cost. Now, it would incur capex both in India and Bangladesh to expand in-house hard luggage manufacturing as its existing capacity is running at 100%. In such a scenario, VIP might not have geographical advantage for hard luggage manufacturing from Bangladesh as it is not so labour intensive.

Looks like Safari is able to consistently get things right and narrow the market share gap. What a good combination of oligopoly industry with strong growth potential, a company which is able to grow better than its peers and available at EV/Sales of 2.5x (annualised 2QFY22 sales).

Any resurgence of covid wave and further increase in input cost remain key risks in foreseeable future.

Disclosure: Invested

10 Likes

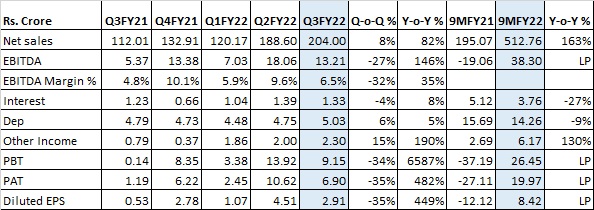

Q3FY22 Results

Safari Industries’ Q3FY22 revenue growth was strong but there was disappointment on the margin front. Revenue grew by 82% on Y-o-Y basis, 8% on Q-o-Q basis and 23% over Q3FY20 (pre-covid normal quarter). While EBITDA margin stood at 6.5% against 4.8% in 3QFY21, it declined significantly from 9.6% in Q2FY22. This seems to be due to input cost inflationary pressures and high competitive intensity.

VIP-vs-Safari

VIP’s revenue growth during the quarter was strong with 71% Y-o-Y and 20% Q-o-Q growth. Additionally, VIP’s EBITDA margin improved to 14.4% in Q3FY22 as compared to 12.7% in Q2FY22. VIP’s margin profile is much better, but its revenue at Rs.397 crore is yet to recover to pre-covid level (Rs.431 crore in Q3FY20 and Rs.430 crore in Q3FY19).

VIP, the largest Indian luggage company, has sequentially also done better in terms of gaining some market share, which it was losing consistently. However, similar trend was there in the previous Q3s too, which reversed in subsequent quarters.

Way forward

After covid resurge during the last 1-2 months, situation is again improving. Travel and related sectors are expected to do better in coming time. Also, opening of schools and colleges should benefit backpack business (under Genius, Genie & Safari brands). Luggage is one of the few sectors which has strong growth potential, have limited number of organised players and also witnessing value migration from unorganised to organised players; yet market caps are small.

Luggage market is shifting from soft luggage to hard luggage over the last few years. Hard luggage’s market share, which was about 30% two years ago, has improved to about 60% now. VIP had set-up soft luggage plant in Bangladesh to take advantage of low labour cost. By the time plant was streamlined, trend has changed in favour of hard luggage. Safari had only hard luggage capacity in-house, which it is in the process of doubling now. VIP is also investing in both India and Bangladesh plants (though no cost advantage in case of hard luggage) for hard luggage. In such scenario, Safari would also have similar cost structure. Both the players would benefit from lower manufacturing cost due to inhouse production and reduced working capital intensity. New capacity would also help in producing more polyproline based products, which has lower cost as compared to polycarbonate.

While the quarterly results were below expections, long-term story remains intact. Superior revenue growth, normalization of margins and improved working capital cycle can be next set of triggers; over medium term. At the CMP of Rs.890, while TTM PE of 75x looks high due to depressed earnings (on covid-led decline in revenue & profits initially and margin pressure in current quarter), stock looks attractive at ~2.6x market cap/sales (annualized at current qtr sales).

Disc: Invested

11 Likes