Can any one share the data regarding the volume growth of the company?

VIP’s promotors have long been seeking to exit the business (confirmed with my PE friends). Lack of clear succession, instability in management and competition from Safari.

Disc: Invested in Safari at much lower levels

Safari’s performance in the last 3 years has been beyond expectaions. From a marketcap of Rs.890 cr to Rs.9800 crore (10x after adjusting for preferential allotment in between). Interestingly, it gave many opportunities and triggers to add further during the period.

Safari Industries (India) has fixed 12 December 2023 as record date for issue of bonus shares in ratio of 1:1.

Crisil has upgraded its rating for Safari Industries, given its recent strong performance. Link: here

CRISIL has upgraded Safari’s Credit rating to “AA-” and A1+. This is a significant milestone for the company’s credit rating.

Key takeaway from CRISIL’s rating rationale wrt to growth

- The group continues to launch 3-4 stores per month, aiming to cater to premium as well as mass scale segments.

- As per CRISIL “For fiscal 2025, the group is expected to earn revenues of Rs. 1900 crore, 24% higher than 2024 with EBITDA margins improving to 18.5%.”

- “Group has its own manufacturing units for hard luggage which are operating at full capacity utilization.”

- “Group has announced capex of Rs.215 Crores for setting up a greenfield manufacturing unit in Jaipur, Rajasthan. Capex would lead to doubling its hard luggage capacity from ~6.5lac pieces per month to ~13lac pieces per month. The new capacities expected to become operational in H2FY25 and will help group to further penetrate in to North Indian market.”

- “With the capex expected to come online around December 2024, the revenues and margins are expected to see a further improvement from fiscal 2026, while capital structure remains strong.”

Disc: Invested. I am not SEBI registered Advisor/Analyst. My view may be positively biased. I am not suggesting any investment action. The information provided above is for education purpose only.

Safari industries CMP 2375 , potential to become double. - go to any good showroom and check for yourself . Co. has done fantastic rebranding & repositioning of their products in comparison to VIP industries. In March 2024, SIIL received as investment of Rs.229 Crores from Lighthouse Funds (Alternate Investment Fund -AIF). Group has announced capex of Rs.215 Crores for setting up a greenfield manufacturing unit in Jaipur, Rajasthan. Capex would lead to doubling its hard luggage capacity from ~6.5lac pieces per month to ~13lac pieces per month. The new capacities expected to become operational in H2FY25 and will help group to further penetrate in to North Indian market. With the capex expected to come online around December 2024, the revenues and margins are expected to see a further improvement from fiscal 2026

Q2FY25 – Short term pain

Negatives

- Although revenue grew by 24%, there was significant decline in realisations

- Heightened competition mainly due to inventory cleanup and attempt to push online sales by VIP Industries as well as from new D2C brands

- Decline in realisations, some increase in key inputs prices, higher marketing spends resulted in EBITDA margin declining to 10.5% and PAT decline of 25%

- Capacity constraint for Safari

- Significant increase in debtors

Positives

- Safari has strengthened its market share and has become No-2 player

- Volume growth of 40%, despite capacity constrain

- As per a brokerage report, increase in debtors was mainly due to big billion day and the payments were realised in October

- Samsonite lost significant market share as it did not respond to aggressive pricing in the industry

- VIP could not gain much market share despite pushing volumes at the cost of operating loss. VIP is still struggling with old inventory

- Premium brands, Urban Jungle & Safari Select, which are just 1 year old, are contributing to approx. 5% revenue now

- Safari’s new plant at Jaipur is on the verge of commencement, with which Safari’s manufacturing capacity will significantly increase. Completion in less than 1 year is a big achievement

- As the new plant also has significant warehousing space, expected to be more cost efficient and is nearer to Northern market, Safari should benefit from lower costs

Pics of new plant as on July 2024

With VIP struggling with its profitability and non-aggressive pricing approach by Samsonite’s mid and lower range brands (American Tourister & Kamaliant), pricing war should not continue for long. VIP’s struggle with its older inventory and Bangladesh operations continues, which has significantly reduced its financial flexibility and provides a big opportunity to Safari.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My views may be biased. I am not suggesting any investment action. The information provided above is for education purpose only.

Interesting insites about Safari and Mr Jatia’s journey

Hi Gautam

Thank you for the information.

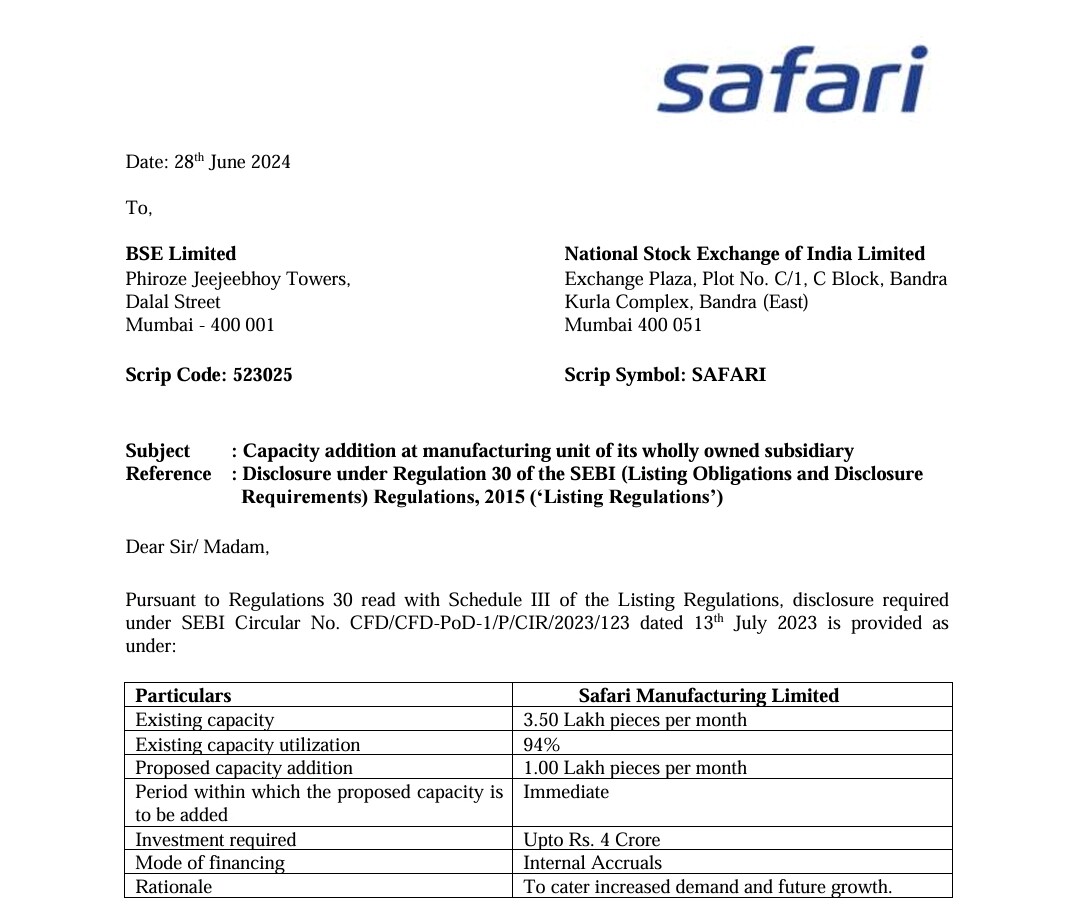

How did you arrive at the capacity addition of100% ? 30% of existing capacity, is listed in the communication to the exchange.

Source link (CRISIL rating rationale) is provided in my post. The same can be verified from various brokerage reports too. I do not know, how did u arrive at 30%. You might be getting confused with last expansion at Halol plant.

I have sold my safari investment last quarter (which I held since 2017). The logic behind the same are:

a) Limited room for market share gains: Safari’s market share is now ~31% of all organized retail luggage player, which has continioulsy increased since 2018 (2018: 15% m.a. | 2022: 23% m.s. | 2025: 31% m.s.). I don’t see the market share inching up beyond 35% given VIP has turned aggressive now and many new brands have entered the segment (Assembly, Mokobara, Nasher Miles). Entire sales growth for Safari was led by market share growth, while the sector has hardly grown by 10-12% over last decade.

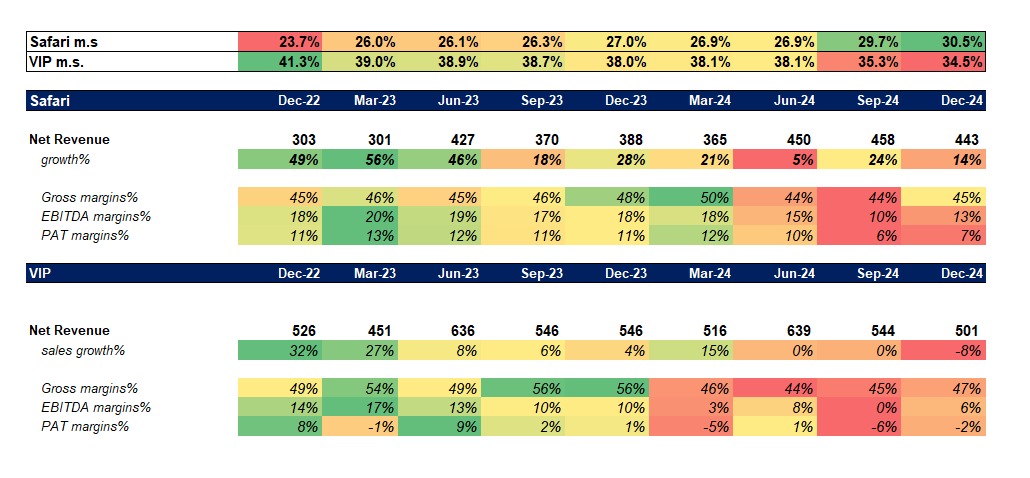

b) VIP has started to become aggressive: While I still doubt the execution by VIP’s management, they have flodded the market with cheap inventory, thus impacting profitability of the entire segment (refer below table). All the margin metrics of both Safari & VIP has turned negative in last 2-3 quarters. VIP’s Management are trying to exit to a PE Fund (still under discussion), which will further fuel the aggressivness.

c) Stock is no longer cheap at 70x trailing P/E and slowing down sales and margin decline: I entered the stock at ~30x P/E when it was going through transformation led by management change and internal issues of VIP. While I have no doubt on Sudhir Jatia’s execution skills, I fell giving 70x for a plastic luggage brand where distribution is no longer your moat, is just too much. Remember most of the luggage is now sold online (Safari sells 40%+ of its luggage online) where there is no moat in terms of limited shelf space and distribution connect.

I like the management’s intent to diversify further into premium luggage (via a new brand) and aggressiveness in setting up a new capacity. But given the aggresivness of VIP, limited room to gain market share and higher valuations, I sold the stock around 2500 levels.

I have a few points of difference and if you are still tracking the stock, would be great to hear your views

- Limited room for market share gains. This indeed looks to be the case. However, while the total market has been growing at 10-12%, the organised part of the market has been growing at ~15% - marginally better

- VIP has started to become aggressive: Agree the gross margins of the industry have clearly been affected by two issues

- VIP has openly stated that they will be dumping their inventory (primarily soft luggage) which resulted in hits in their gross margins

- They have also got more aggressive in eCommerce where discounting has also been the case (they claim they are trying to correct in some areas) as they felt they were under-represented here.

- VIP is looking very weak at the moment to continue discounting and this could be a potential trigger for competition to stabilise

-

VIP are under intense pressure from the analyst community to meet year end margin targets as they had indicated the gross margin pressure was a short term inventory liquidation issue (old inventory should now be nearly fully liquidated). Q3 had a sequential 150 bps improvement in gross margin and a further 300 bps is indicated in Q4 with gross margins to go back above 50% in Q1 Fy26 (these may not be achieved but pressure will remain)

-

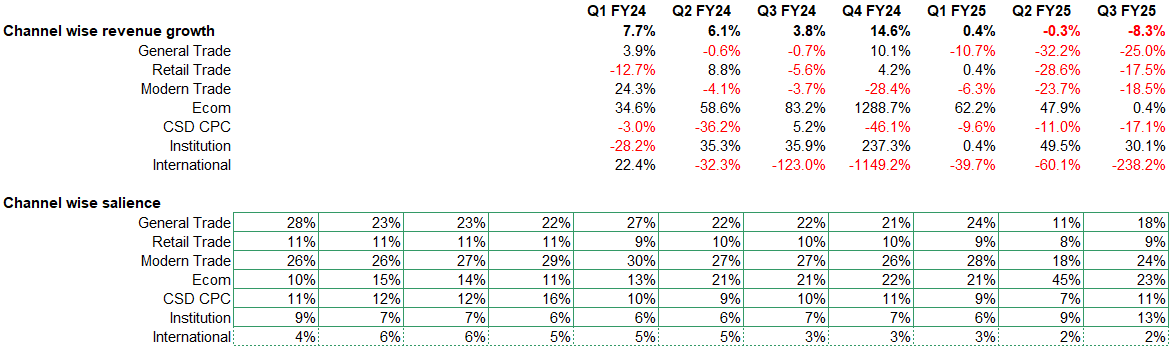

VIP seems to have over compensated on ecommerce (and that also seems to be slowing). However, the physical trade numbers are collapsing and I can imagine they will be facing a lot of push back from the trade to their ecommerce push. See below - look at YoY General Trade, Retail Trade and Modern trade growth). How they deal with this will determine further industry competition - they could respond with price cuts in physical trade - but then their margins will further collapse. They claim the approach is more ad spend - but let us see. Either ways - as a company they are now fighting multiple fires.

-

PE introduction may be accelerated though as business difficulty increases - and at a cheap price. However, I guess your interpretation of PE entry is that price discounting will be a way to try to regain share ? (they will unlikely use discounting as a long term business strategy in my view). They will face challenges in short term discounting as well - so there is also a good chance Safari may become the market leader and VIP may decide to settle for a strong second in the short term (in any case this is all just speculation so worth nothing)

-

New entrants - Mokobara and Assembly - are probably more targeting VIP customers than Urban Jungle customers (although Nasher Miles may be closer to Urban Jungle). This space will be interesting because as the big guys discount, the profitabilty of these businesses is further challenged. The macro environment will probably determine how many continue to get funding - and whether competition increases or decreases (or are potential targets for M&A - most likely Safari would be a buyer - but I don’t know if they have any M&A appetite)

- Valuation: There is no running away from this one. At best even if one assumes the gross margin impact is short term (and say was 2% better), you would still be at a 55-60 PE (at current prices) which for the current business growth looks high - even assuming that growth is closer to the 15% as per the organised market share. Unless they find newer growth drivers (backpacks for further push), higher share in premium / M&A at EPS accretive prices or adjacencies - difficult to add here for me unless there is a price drop, revenue growth change or gross margin improvement

Disc: Invested recently. Not yet a full position. Likely to be biased and not investment advice

Key Industry trends in 9MFY25

Intensified Competition - VIP resorted to deep discounting to liquidate old inventory (majorly soft luggage) and was also aggressively expanding online channel, which resulted in VIP reporting net loss in this period. Samsonite, which was number two player earlier, decided not to play on price (particularly American Tourister brand is in price sensitive segment) and reported significant decline in sales and market share in India. This helped Safari become number 2 luggage player since Q2FY25 onwards. Safari, reported highest revenue growth among top players and about 20% decline in PAT. Few D2C players such as Mokobara, Nasher Miles, Uppercase etc have been able to improve their presence, majorly through cash burn. Safari also made aggressive marketing spend on its new premium brands Urban Jungle and Safari Select. While everyone suffered in this battle, Safari suffered the least.

Manufacturing focus – Safari has spent more than Rs.2 bn on expanding capacity and added 6 lakh per month (1 lakh brown field and 5 lakh green field plant in Jaipur) and its manufacturing capacity is now ~12.5 lakh pieces per month. VIP did not focus on capacity expansion with capex of just around Rs.32-35 crore. Nasher Miles is also shifting from import to manufacturing and setting up a 50,000 piece per month unit. Mokobara mainly imports from China.

With a very large-scale hard luggage manufacturing units at Gujarat and Rajasthan, Safari is it at distinct advantage as it can optimize its cost of production, warehousing and transportation.

Will Industry rivalry continue for a long period? Current intensified competition is majorly driven by deep discounting by VIP. VIP does not have financial muscle to sustain this as its balance sheet has weakened in the last few years. Also, it does not have cost advantage with higher transportation & warehousing cost due to some manufacturing in Bangladesh. It is already under pressure from investors & analysts to improve its profitability. Even if VIP is bought by a PE player in future, new owner cannot ignore profitability as it’s a listed company. New entrants, though currently burning cash, have to stop at some point of time as and when investors plan exit through listing or stop infusing fresh funds. Also, history says that cash burning companies either start focusing on cash flows or they are shut down. Most of the new entrants are currently focusing on premium segment.

While Chinese import is a threat, but transportation & warehousing cost is higher for import and also established players are able to differentiate with aspirational branding, warranties and distribution network. In past also, industry witnessed competition from China and unorganised players, when soft luggage largely dominated the industry. Also, there was perceived threat from entry of Amazon through own brands. While these resulted in some disruptions, but domestic players continued to thrive.

Will Safari’s growth slow down? Safari may not be no 1 player currently in terms of market share, but it is strongest player in the industry in terms of financial health, manufacturing capacity and more importantly, management capabilities. In my personal view, it still has potential to gain market share in its traditional economy products (Safari has become strongest brand in affordable luggage segment), premium segment where its market share is very low currently and backpacks & school bags, which is still dominated by unorganised players.

I believe that industry growth in future will be driven more by shorter replacement cycle and ownership of multiple suitcases in a family as per colour and style preferences. While new entrants have been able grow rapidly on a small scale; significant investments will be required by them in manufacturing and distribution network to become relevant players, which may not be a easy task.

With all this, I believe that Safari should continue to witness industry leading growth and gain market share. Mr Jatia (Safari’s promoter and MD) has a great track record of timely identifying industry trends. As and when growth tapers, Safari has option of diversifying in other businesses as well. While this may not be required over next few years; but strong leadership gives comfort that they will be proactive as and when it is required.

Is valuation high? The stock has multiplied over a period, driven by beyond expectations performance. As per screener.in, historical 10-year median PE is around 70x. With a more matured business, PE may not sustain at such high level in long term. Current PE is around 66x TTM earnings. While current PE also look optically high, but it’s on depressed earnings of last 2-3 quarters. Hence it may not be giving correct picture if one’s assumption is normalisation of earnings growth and compounding of earnings.

Philip Fisher writes “In evaluating a common stock, the management is 90%, the industry is 9% and all other factors are 1%”.” So far, this is perfectly validated in the luggage industry, lets see what lies in future.

Disc: Invested. I am not SEBI registered Advisor/Analyst. My views may be biased. I am not suggesting any investment action. The information provided above is for education purpose only.

Hi, Thanks for that wonderful comparison !. Is it possible to have updated comparison to find the real man ? ![]()

Sustaining high valuations look tough, going ahead for Safari..

Operating Margins are at significant lows. Spends on marketing, distribution will only rise. High sales growth to remain a challenge given the inventory cleansing by VIP at throwaway prices in the mass segment and higher price segment (urban jungle from safari) seeing lots of competition - from both existing and new.. VIP’s Carlton, Mokobara, Nasher Miles, Products from Brand Concepts, Samsonite..

Where can the new growth come from ?