Shareholding norms are being updated. It will now be required for Public Listed entities to have 35% as free float i.e. non-promoter shares. So expect some 10% shares to be released by the promoter sometime soon. Do not think it will prevent these guys, deserving as they may be, skimming the profits at the expense of the minority. This is going to be a long game for decent value growth.

1 Like

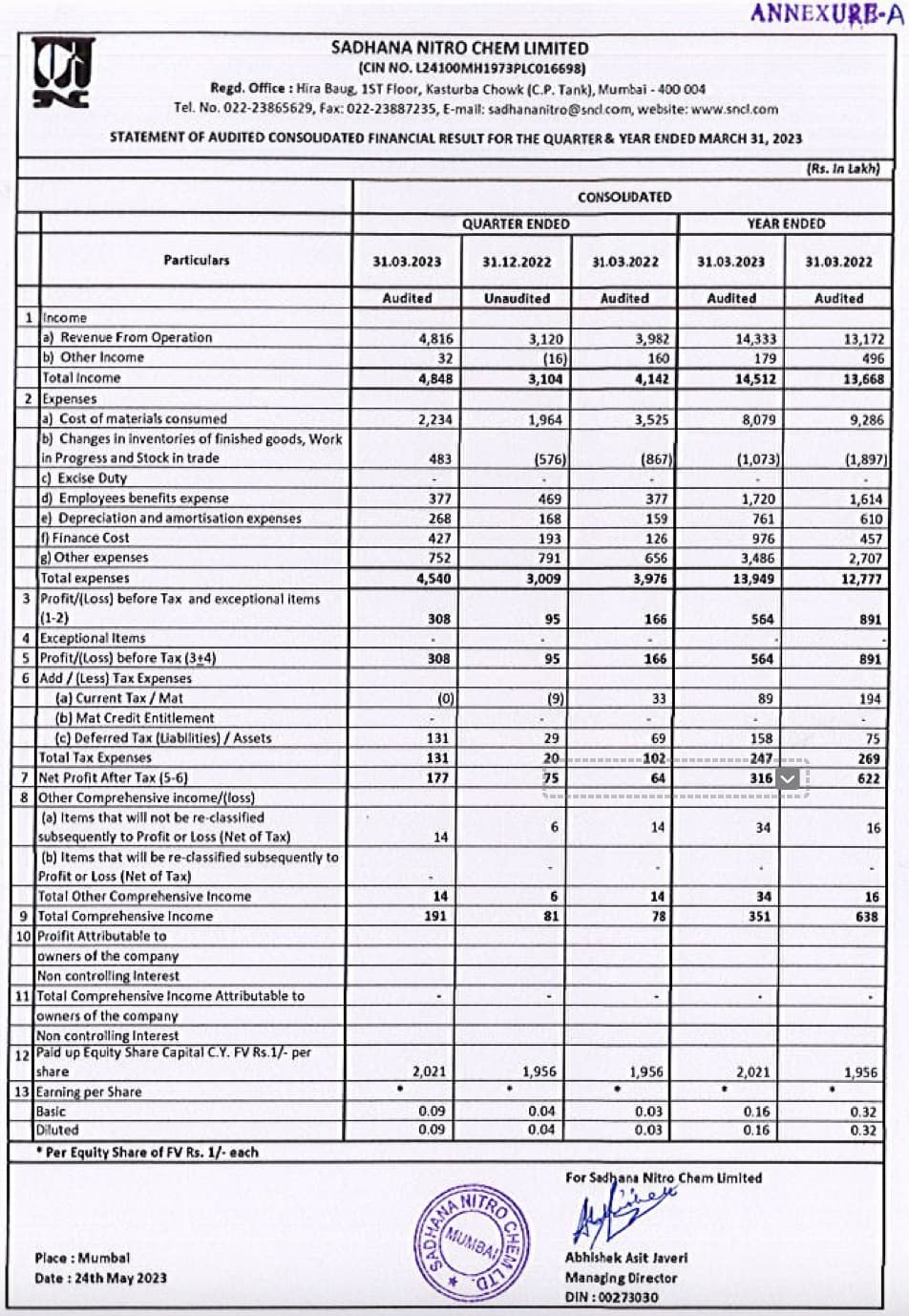

FINANCIAL RESULT FOR THE QUARTER & HALF YEAR ENDED SEPTEMBER 30, 2019

The stock has risen a lot in the last month and I am unable to understand the reasons why. One guess: Is the US-China trade deal positive for the company? Any update on the reasons behind the current surge in the stock price would be useful.

Results for Quarter and Nine months FY2020:

Hi,

Any research update on the company

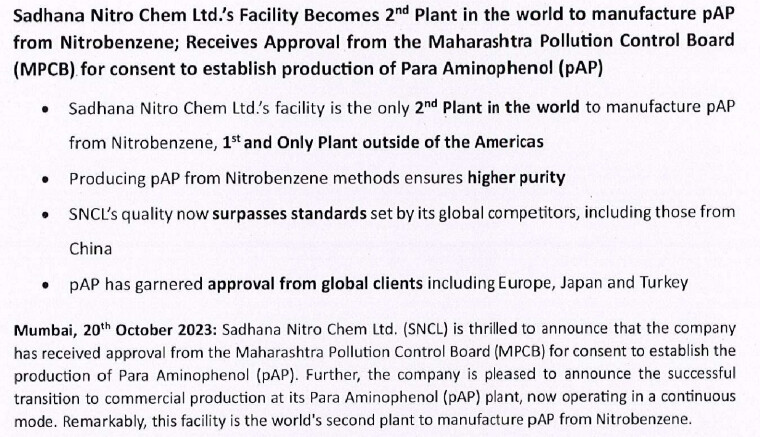

SNCL was supposed to start operations for a greenfield project of manufacturing PAP from Nitro Benzene route in May’21, however, there are no signs of it. They received approval under PLI scheme for making 36000 MT of the PAP.

Anybody has any update there?

1 Like

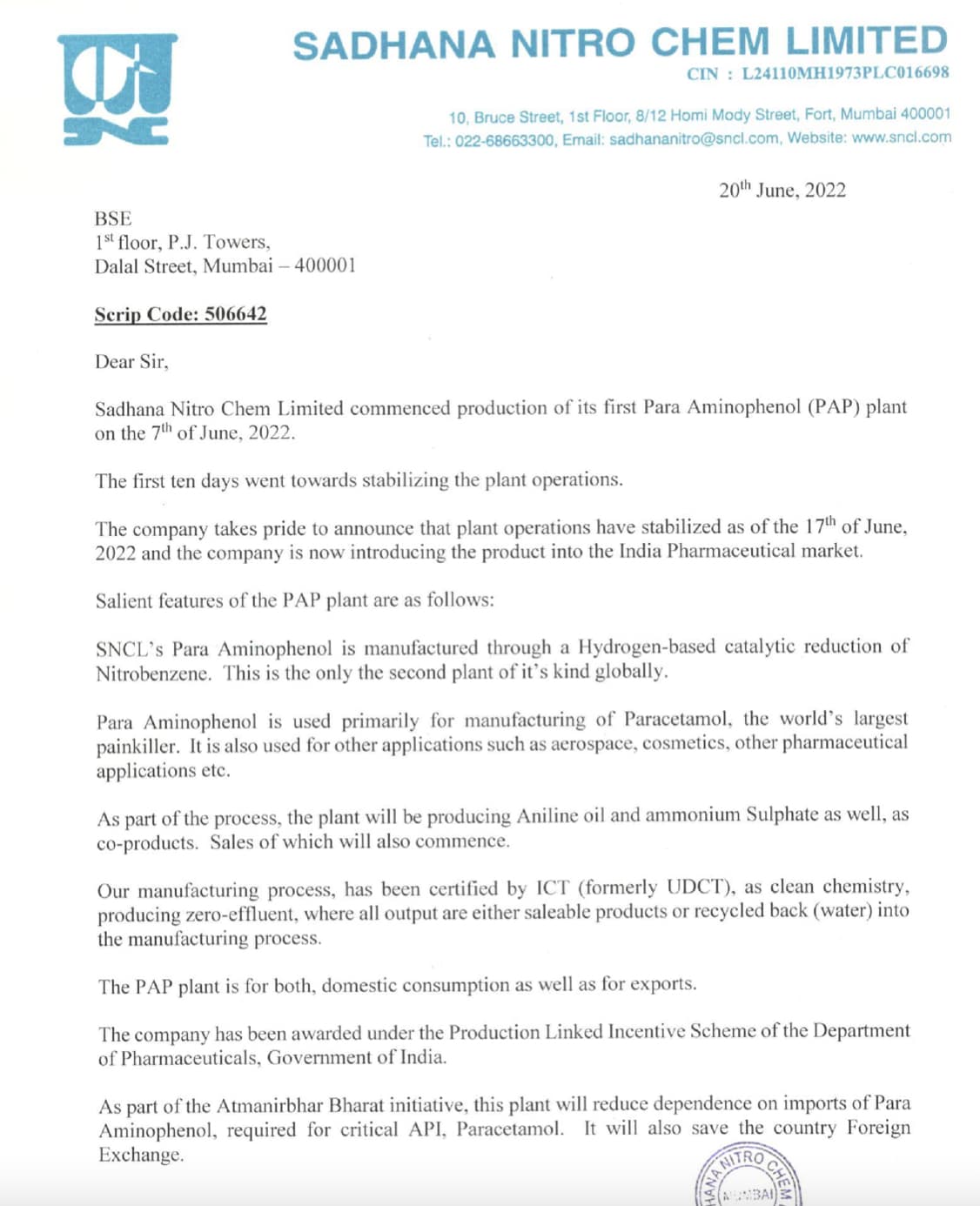

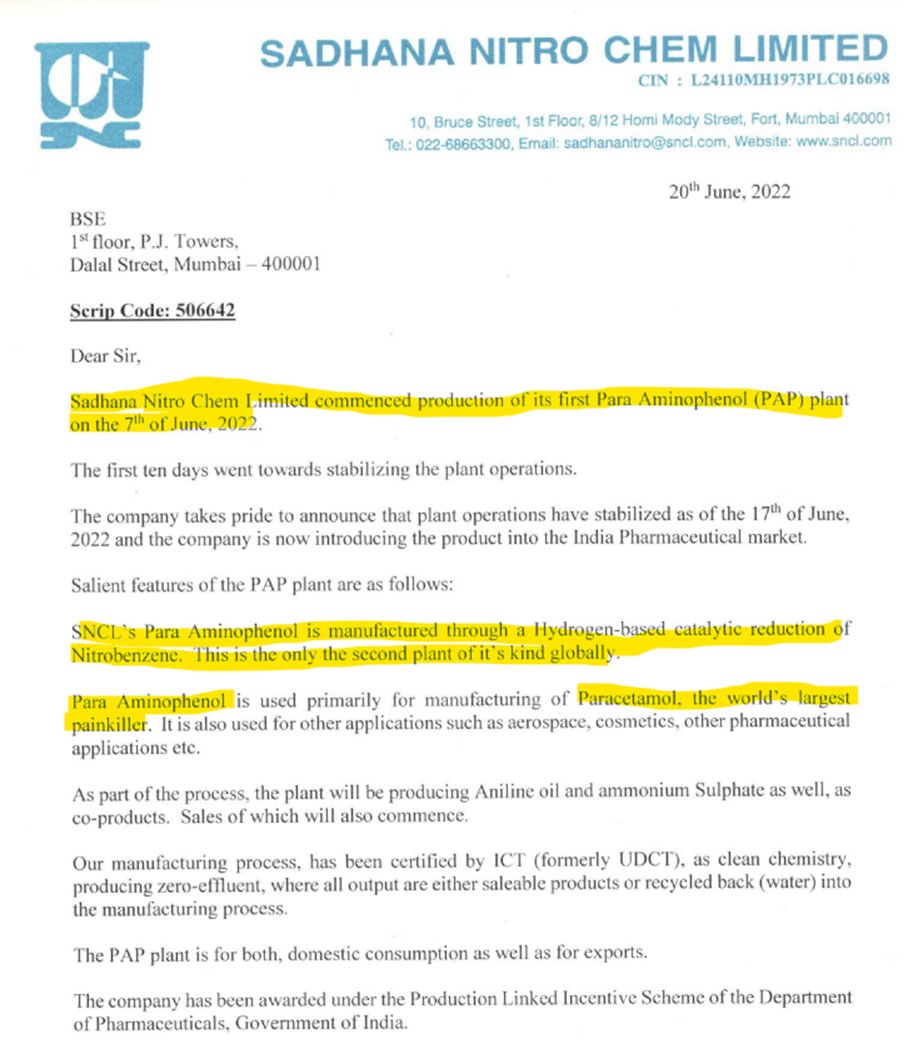

In the recent results Sadhana Nitro has announced Completion of the PAP Plant.

"The Para Aminophenol (PAP) plant construction has been completed. Electrical Trials are

starting this week. This will be followed by water run trials. On Conclusion of the water run

trials, the plant will start commercial production. "

1 Like

This is the Same route which Vinati failed to develope.

Only second company in the world to develop this

27d35c52-b916-4fe8-9821-535eab624460.pdf (2.2 MB)

Q1 results.

1 Like

what will be the revenue for 36000 MT ? and what could be the margins for them ? Any info regarding this

#Sadhananitro

It started in the year 1973 and has built a strong reputation of manufacturing quality products along with excellence in service to clients worldwide.

1/n

Sadhana Nitro Chem Ltd is engaged in manufacturing of chemical intermediates, heavy organic chemicals and performance chemicals and wireless network equipment and services.

2/n

Current products: Nitrobenzene, Meta Amino phenol (MAP), Metanilic acid, Aniline, Ortho Aminophenol, Para Amino Phenol, Ammonium sulphate, diethyl keto acid etc.

Currently 99% of revenue comes from chemical intermediates and 35-38% Revenue is from MAP with 50%+ exports

3/n

What actually I like about Sadhana?

5years of hardwork to start producing PAP and the opportunity that the company is having with great technology process superiority and also team understanding to convert the batch process to continuous process (RM to PAP is just 10Hrs)

4/n

5 Key Triggers:

1.PAP

2.PLI Scheme (36,000 TPA)

3.Expanding Downstream Capacities

4.Forward Integration plan to produce Paracetamol (Indians favourite drug)

5.All other business in one Thali

5/n

1.PAP

PAP – Para Amino Phenol which is the main API for Paracetamol, and we all know how we use Paracetamol and its just a pain killer and used for Fever

6/n

Demand for this product is very high in the world and also in India, And China is the only source with 95% marketshare (160000 TPA World demand for PAP)

7/n

Now we have Sadhana who has entered into PAP by NitroBenzene route with the help of a scientist and company is doing great work here

8/n

2.PLI Scheme

Government of india is helping to get cost benefits worth of Rs. 58crs over the periods for Sadhana with an approval PAP Plant of 36000TPA

Committed Investment by Sadhana = 198Crs

9/n

PAP through Nitro Benzene is one step process and its one of the best way to produce PAP

Do read the research report to understand Nitro Benzene to PAP

researchgate.net/publication/35…

10/n

3.Expanding Downstream Capacities

More than 80% of PAP Worldwide is used to manufacture Paracetomol,7% is used in RUBBER Anti-Oxidant,5% in Dyes and others etc.

Company is also focusing on Dyes segment and wants to keep expending its customers.

11/n

Focus is more on raw material, and they believe the end product will he at high quality.

2 ways to produce PAP

A.PNCB

B. NB

12/n

4.Forward Integration plan to produce Paracetamol (Indians favourite drug)

In recent Annual concall company told it wants to get into Paracetamol and its just 1 step process from PAP

13/n

For this company need FDI approval and I expect this to happened in next 2 years then the revenue mix will be like

•PAP – 40%

•Paracetamol – 40% (High margin business)

•Other business – 20%

14/n

5.All other business in one Thali

I expect around 300crs of top line by FY2027 from other business for Sadhana

My numbers (FY 2027 5Year view)

36,000 X 1000 X 450Rs = 1,620 Crs

36,000 X 1000 = PAP

450Rs = PAP Price per KG

economictimes.indiatimes.com/mobile?utm_sou…

15/n

Economic Times (ET) Mobile Applications - ET for Mobile AppsThe Economic Times (ET) on iPhone, iPad, Android, Nokia, BlackBerry and other mobile applications to stay connected through ET Mobile News Services. Get complete access to Markets on The Economic Time…https://economictimes.indiatimes.com/mobile?utm_source=Appsflyer&utm_medium=onelink&shortlink=135dde21&c=ETMWEB_Sharing_Text&pid=ETMWEB_Sharing_Text&af_channel=ETMWEB_Sharing_Text&source_caller=ui

I am taking margin of safety upto 35% in sales and expecting around 1000crs sales only from PAP

PAT Margins I expect to be around 20%

Total Sales = 1000 + 300 = 1300crs

PAT Margins 20% = 260crs

16/n

Sales CAGR = 50%+ for next 5 years

PAT CAGR = 80+ for next 5 Years

Expected Price to Earnings FY27 = 25

17/n

Risk:

1.If prices for PAP go down from 450Rs

2.For sales of 33000TPA PAP company need to invest 300Crs

a.100Crs from Internal Accruals

b.100Crs Debt

c.100Crs Equity capital

18/n

3.If company can’t sell its PAP (We need to track every quarterly number) (Clients tracking)

4.High Risk high reword game (Assuming PE to be 25)

5.Any other risk can come

19/n

Disclaimer: This is only for educational purposes & not a recommendation & I am writing this only on a request from one of my friends in twitter.

I may or may not hold the stock personally and I love to understand business so thought of keeping track of it.

Thanks for reading

Be careful my understand can also be wrong

And don’t buy by just reading this do your own research and take your own call.

I am just sharing my thoughts only.

• • •

Adding twitter thread on Sadhana by Koushik Mohan

4 Likes

I think companies like IOL Chemicals making PARACETEMOL are bleeding ,how do we expect the raw material supplies for the same can perform better ?

1 Like

Think of it like consumption of Paracetamol Irrespective of who is producing is increasing. Most importantly even if it’s stagnant, think of the tectonic shifts in PAP producers and how that will add to Sadhana’s business growth

2 Likes

latest update from sadhana : * ODB2 Expansion: We are excited to report that our ODB2 production capacity has

expanded significantly from 550 tons to 2200 tons. With robust orders in the pipeline,

we’re expecting a consistent increase in capacity utilisation.

- Global Positioning: This boost in ODB2 capacity solidifies our standing among the top

two ODB2 producers worldwide. As the China +1 policy gains traction globally, we’re

diligently building stronger relationships with our clientele. Our goal is to consistently

broaden our market presence and secure a larger market share. - Updates on PAP: The Company is encouraged by the advancements in our PAP

operations and look forward to sharing more details shortly.

5 Likes