Hi friends ,

Have been following this spot since Jan , Indeed december last year … Its slow motion movements and less popularity made me think that you all may like to have a slight glimpse over it …

As a part of breaking the ice , let me give some idea about the Company …

Key statistics :

Category : dyes and pigments

location :mumbai

1 year return : 666.61%

Mcap : 394 ( microcap )

Book value :33.68

Deliverables current : 83.51

Pe ratio :12.58

Ind pe: 21

Fv:10

Peg :0.79

Intrinsic: 429

Eps:33.3

Shares outstanding :9.2 million

Price to sales ratio : 3.45

Last dividend reported :1

Debt to assets : 37.68%

Profit margin : 30.38%

Equity share capital : 9.32 ( was constant at 9.2 for few earlier qtrs)

25may eod :-

Cmp :423

Bids pending: 107409 , offers 0 , traded quantity for 25 may :2459

About sncl :

Sadhana Nitro Chem Ltd. (SNCL) is an ISO 9001:2008 firm producing high quality chemicals since 1973 .

-

Engaged in the manufacture and marketing of : Nitrobenzene ( C6H5NO2) , its downstream derivatives and other intermediariess for various applications in aerospace, pharma and agro, optical brightening agents, plastic additives, special fibres, epoxy resin hardeners, dyes and performance chemicals.( Azo dyes , direct dyes , reactive dyes , florescent brightening agent , colour dyes , leather dyes , hair dyes , agro chemicals , pharmaceutical and m fibers ) , aniline , light stabilizer , textile printing oxidizing agent , electroplating agents , etc

-

Derivatives and products other than Nitrobenzene and meta amino phenol are : 1. 33DDS ( dinitro diphenyl sukhane ) 2. M/Acid ( metalinic acid ) 3 . Aniline 2,5 disulphonic acid , 4 . Aniline 2,4 disulphonic acid 5.btca ( butane 1,2,3,4 tetra carboxylic acid ) 6. Dibutyl ke to acid 7. 3,3 diamino diphenyl sulphide 8. Sodium meta Nitrobenzene sulphonate 9 . Colour formers 10. N,N dietyl meta amino phenol

-

In order to provide immediate and assured service to the vast European clientele, SNCL has also set up a 100% subsidiary Anuchem b.v.b.a. in Antwerp, Belgium.

-

SNCL is a government recognized 2-Star Golden Export House. ( Means ministry of commerce has awarded them golden status certificate for 3 terms or more and they will enjoy that status irrespective of performance henceforth )

** New developments : 2018

- Name change evoting approval ( sadhana nitrochem to sncl limited)

- Acquisition of business of Spidigo Net Private Limited ( paid up capital , rs 100000/- turnover 9.985 crores , category :internet service provider )

- Strix wireless system private limited 's shares acquisition evoting ( paid up capital of 3920010 /- turnover of approx .9973 cr for 2016-17 ) : category : wireless and networking technology hardware and software

- Loans and securities wrt section 186 of companies act 2013 http://www.rna-cs.com/insight-on-section-186-of-the-new-companies-act-2013/

Additionally , investment limit of 25 cr over and above ceiling - Solar power plant with battery backup costing 4.28 cr acquired from PAE renewables pvt limited

Some of the earlier devp: http://www.sncl.com/newpdf/Out%20come%20of%20%20BM%20100317.pdf

- Website : http://www.sncl.com

Statement facts :

total current assets : 35.7

Total current liab :52.21

Yrly bottom line up by 15 times and income from ops doubled hence prompting towards a growth story

Guys all of you you are welcome to provide your views on this please …

Wish u a lovely investing career with a tinge of golden flakes

@Article in business standard

Sadhana Nitro Chem standalone net profit rises 1648.80% in the March 2018 quarter

Capital Market | | Last Updated at May 02 2018 09:04 IST

Sales rise 166.82% to Rs 51.39 crore

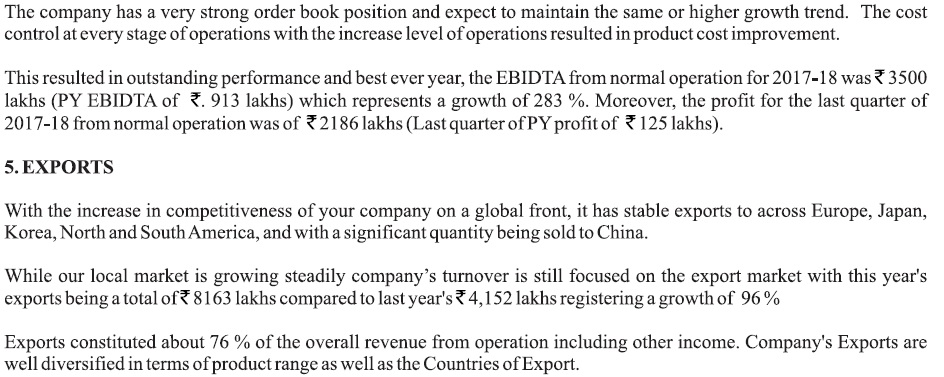

Net profit of Sadhana Nitro Chem rose 1648.80% to Rs 21.86 crore in the quarter ended March 2018 as against Rs 1.25 crore during the previous quarter ended March 2017. Sales rose 166.82% to Rs 51.39 crore in the quarter ended March 2018 as against Rs 19.26 crore during the previous quarter ended March 2017.

For the full year,net profit rose 3237.23% to Rs 31.37 crore in the year ended March 2018 as against Rs 0.94 crore during the previous year ended March 2017. Sales rose 92.97% to Rs 110.55 crore in the year ended March 2018 as against Rs 57.29 crore during the previous year ended March 2017.

Particulars

Quarter EndedYear EndedMar. 2018Mar. 2017% Var.Mar. 2018 Mar. 2017% Var.Sales51.3919.26 167 110.5557.29 93 OPM %37.9812.20 -31.4615.10 - PBDT18.271.76 938 30.162.86 955 PBT17.811.25 1325 28.280.94 2909 NP21.861.25 1649 31.370.94 3237

Powered by Capital Market - Live News

=====================================

Disclaimer : 1. Not invested though wanted to 2. 2. Wanted to bring in a healthy discussion for all the experienced& honourable members of the forum 3. Can someone please help me with the Detailed Risk Analysis based On Fundamentals … ( Long term perspective )

Citing 2 risks related to shirt term holding / trading : 1. Too little volumes per day (hovering around 2-3k ) 2 . Uc / lc stock( locking trends in general )

=============================

Regards ,

A little disciple