Uptrend in prices of speciality paper (bond paper, carbonless paper) continues as per recent update here. As noted earlier, ODB2 is useful for both thermal paper and carbonless paper.

Kalidasa,

Any view on sustainability of the current profitability ?

The issues in China has given a opportunity for the company … which was mediocre for ages…

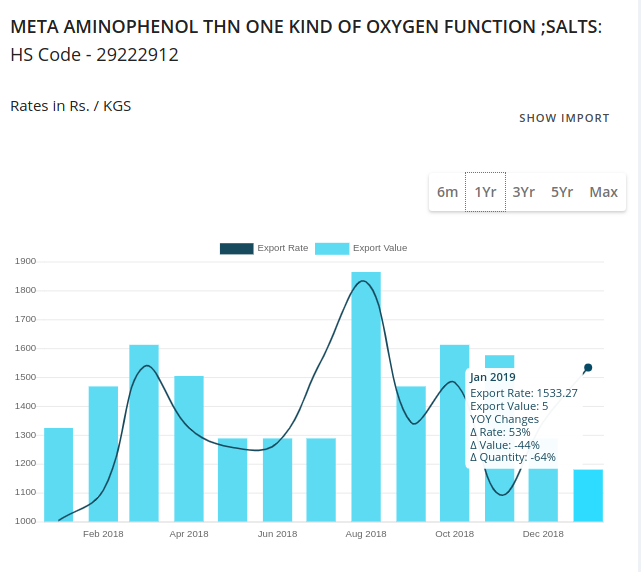

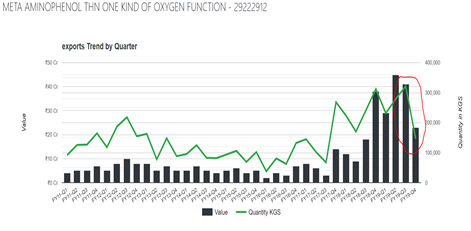

Here is the MAP export chart for Feb 2019. Again, price has increased YOY but quantity has reduced drastically.

The story of profitability seems intact. MAP and ODB2 prices remain high. In threads of other speciality chemicals stocks, one can check that the recent incidents of fires in China’s chemical factories have led to more traction for Indian suppliers, which augurs well for the company in the longer term.

A concerning issue is that the volumes of exports of MAP from the country are much lower than the last year. Are SNCL’s MAP exports lower too? If so, why? Also unclear is how well the company’s foray into wireless networking going and what the plans are, but I guess these are very early days.

Sorry about the delay in reply.

3 Likes

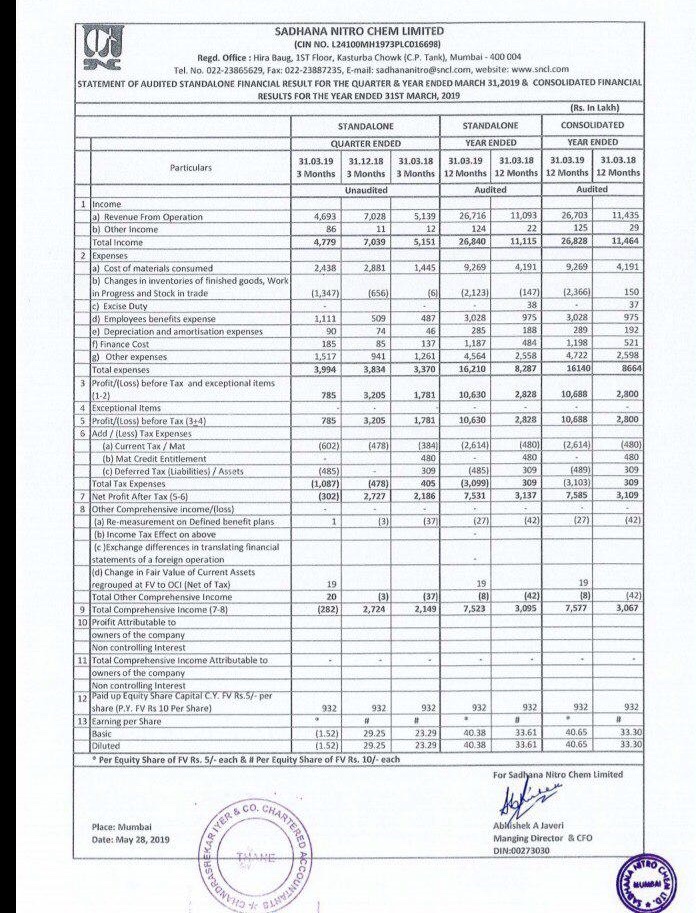

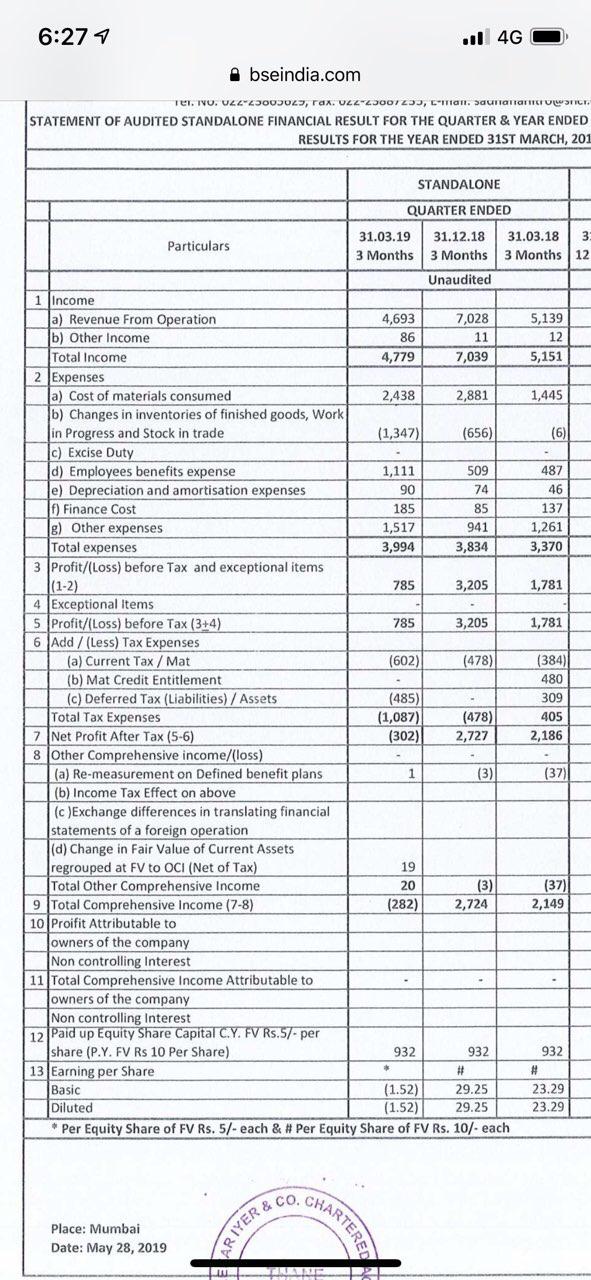

Sadhna Nitro results

- From 21 cr profit last qtr to 3 cr loss this qtr

- Current assets :34 cr of Trade receivables

Cash flow severely squeezed (500% increase in receivables QnQ) - What is the reason for loss no explanation from management

- Company is giving 75 paisa dividend

- If check Benzene price chart ( raw material ) there is no significant increase

- Employee benefit and other expense huge

- Employee expense doubled with deferred tax 4.8 cr

Questions to seniors

- Are the expansion plans only on paper / is last one year meteoric rise is completely rigged.

- Stock price corrected to less than half of peak price already isn’t it the case of insider trading

Poor results. Severe fall in revenue QoQ was unexpected particularly after capacity expansion. Management has not added any commentary—I hope they come out with a press release yesterday or today. Yes, price correction before results raises suspicion of insider trading.

1 Like

After Q3 results mgmt gave press release. All rosy things. Now after dismissal Q4 they disappeared.

Should we believe, someone wanted to trap poor retail ?

Also, when stock was hitting series of UCs , SEBI asked for clarification to company. Why not now when there are continuous LCs ?

2 Likes

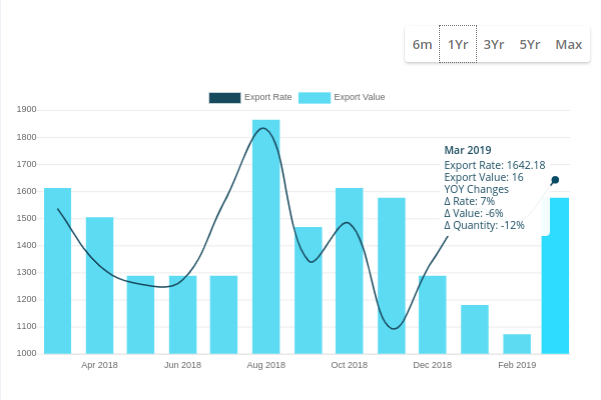

The MAP export prices continue to be higher than the same month in the previous year but the volume again is lower:

A few notes from the investor presentation dated June 14:

-

It is concerning that there was no prior warning from the management about disruptions due to capacity expansions leading to lower capacity utilization in Q4 (and the previous quarters?). It seems the company is facing unexpected challenges in capacity expansion. Furthermore, it seems that we can expect such disruptions in the next few years.

-

MAP capacity expanded to 2,400 tonnes in FY19. Capacity expansion details don’t reconcile with their previous presentation where the MAP capacity was supposed to increase from 2400 TPA to 3000 TPA.

-

Colorformer capacity has been doubled to 500 TPA. ANDS capacity has been doubled to 1440 TPA. But there is no word on the revenue of these products in FY19.

-

The company is planning further capacity expansion for ~35 crores into downstream products to increase diversification. However, this seems to be in initial planning stage as they have not provided the details of the current and projected capacities of these products.

-

No word on the company’s foray into wireless networking.

-

The share price has been in downtrend in the last three months. The presentation came two weeks after the results even as the share price collapsed.

Promoters pledge their shares to borrow funds. It is like a collateral security against the borrowing. In the given case, the pledge was released, which in other words means that the borrowings were fully repaid and so, there was no more a need for pledging share as a security. This was a good news.

The prices of MAP rose as high as 70%, which drove the revenues of the company. MAP (Meta Amino Phenol) contributes more than 70% of Company’s total revenues. Against that, the prices of raw materials did not rise as much, and hence, the Bottom line also showed immense growth. I don’t have the break up of what materials (in what proportion) makes 1 tonne of MAP. But I do know what is required to make 1 tonne of Nitrobenzene(which is the major raw material for MAP). This might give u an idea on the raw material prices front.

To produce 1 tonne of Nitrobenzene,

0.64t of Benzene, 0.515t of Nitric Acid, 0.0033t of Sulfuric Acid and 0.004t of Caustic soda is mixed. The prices of Nitric Acid largely fluctuated in +/-20% range. Sulfuric acid prices rose 50%, but, that didn’t impact much as the proportion of SA in making Nitrobenzene is very less. I am yet to search on Benzene and Caustic soda prices. If anyone has information, kindly share

1 Like

Any idea on the reason for no dividend …despite healthy free cash from operations and payment of debt…

The company is now available at a market cap of 327 Cr… against a PAT of 75 Cr in last FY … What is the market expecting ?

Whether to pay dividends or not is a matter of question for the Board. We, on the other side, can always judge a company based on its history of paying the dividends. As we all are aware, the general reasons why a Board may not declare dividends:

- They need money for expansion

- It may also choose not to pay dividends because the decision to start paying dividends or to increase an existing dividend payment is a serious one. A company that eliminates or reduces its existing dividend payment may be viewed unfavorably and its stock price may decrease.

In regards to your second question- What’s been weighing down on sentiment for the stock:

There are 2 things to note:

Is the supernormal growth sustainable?

Here is a collation of last 5-year financials of the company:

| Particulars | 2015 | 2016 | 2017 | 2018 | 2019 |

|---|---|---|---|---|---|

| Revenues | 48.1 | 35.3 | 56.9 | 114.4 | 267.0 |

| Op. EBITDA | -3.9 | 1.4 | 8.3 | 34.8 | 120.5 |

| EBITDA (Incldg Other Income) | -3.5 | 2.2 | 8.8 | 35.1 | 121.8 |

| EBITDM% | -7.3% | 6.2% | 15.5% | 30.7% | 45.6% |

| PAT | 3.9* | -4.9 | 0.5 | 31.1 | 75.9 |

*2015 includes Exceptional Items of Rs.13.4crores

And secondly, the fluctuation in the raw material prices.

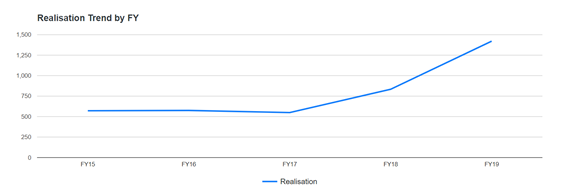

The supernormal profits were generated on account of price hike in MAP.

-Export prices of MAP grew from Rs.571/kg(FY15) to Rs.1421/kg(FY19). MAP’sprices grew skyrocket in past 2 years (FY18 834/kg & FY19 1421/kg)

Being the major revenue contributor product in the company’s overall product line and at the same time exports contributing 76% of the total sales, company’s revenues were bound to rise.

But are the price levels sustainable, is the question here.

During FY19, the export data of MAP showed large cuts in quantity.

In January’19, the Exports qty reduced by 64%.

In February’19, the Exports qty reduced by 89%

In March’19, the Exports qty reduced by 12%

Before putting a list of questions, assuming that the likely scenario will continue, at 50% capacity utilization of MAP (generally assumption based on FY18 numbers) and at 60% capacity utilization of Color Former, Estimated Revenues stands ~193 crores. If the market were to value this company’s sales at 2x, then the share price turns out to be Rs.208. (LTP 26.6.19 Rs.167)

But that’s not it!

Here is a list of questions which if answered, will clear the air on ‘Sustaining the robust growth’

-Are there any plans to increase the capacity of MAP by 600TPA?

-Since when Company did the company add International names in the Clientele?

-Why did the company stop producing ODB-2 (Colour Formers) in the past?

-What is the current and proposed Revenue mix-MAP, ODB2, ANDS?

-Why was there a steep decline in Exports of MAP in last 3 quarters of FY19?

-What is the Price per kg at ‘Normal levels’ for the company’s products?

-Is the company exporting Aniline?

-From where does company purchase Benzene? How are the prices fixed, quarterly or is there a Long Term Purchase Agreement?

-Who is the closest competitor of the company? Management stated that they will be 60% larger in MAP than their closest competitor. Which competitor are you talking about?

If we can get answers to the above questions, it may be possible for us to take a view on whether the growth is sustainable or not.

1 Like

I do not know if anyone has noticed (except a short query by @rupaniamit last year), but this stock figures in Group ‘X’ of BSE. I personally tend to avoid Group X, and other similar Groups.

Further, this stock has been placed in ASM: LT Stage 1, which translates to ‘Additional Surveillance Measure: Long Term Stage 1’. The details of this are available here: https://www.bseindia.com/static/markets/equity/EQReports/additional_surveillance_measure.aspx

and here: https://www.bseindia.com/markets/MarketInfo/DispNewNoticesCirculars.aspx?page=20181027-1

Since this is a measure introduced by SEBI to protect investors’ interests, I guess this says a lot without mentioning specifics.

I hope that this makes sense to more enlightened investors. I’m still in the learning phase, so please feel free to correct me anytime.

Regards

Sandeep

I personally tend to avoid Group X, and other similar Groups.

Group X mainly means it is listed on one of the exchanges, not both (BSE says “only listed/traded at BSE and satisfy certain parameters”). There are several such companies. To each on his or her own, but I don’t think that is any reason to avoid a stock. I don’t know what “other similar Groups” means. Lets at least try to do some basic research before commenting.

About ASM LT Stage 1, there are very specific volatility and top holder-trading-related rules as detailed in one of your links. This does not imply that there is any wrongdoing going on with the stock.

I earlier raised concern regarding the stock price decline that looked like insider trading but it is a suspicion, not a given, considering the international pricing data of the manufactured chemicals may have been available to those traders.

Regards

1 Like

Perhaps I did not articulate properly. My apologies. I meant that for these stocks, liquidity may be a concern, and also such stocks tend to fall rather precipitously in a falling or even volatile market, so that there could be sudden, and significant losses for the investor. As I said, I personally do not prefer such stocks.

However, I would reiterate that placing a stock in ASM stage is certainly a concern, for if one reads carefully the reasons, it clearly shows that the trading in the stock is limited to only a few individuals or entities and that wider participation is missing. This is always a red flag for me. I wished to raise this as I have been following this topic, but could not find this particular issue dealt with here.

I hope that I have been able to put my views in a proper manner. If not, please do feel free to guide me appropriately. I am willing to learn.

Further, as you have rightly pointed out: to each his own.

Regards

Sandeep

Liquidity is a concern due to the artificial reason of ASM, nothing to do with Group X. Why does BSE have 5% and 2% daily limits? If a stock is being illegally manipulated, shouldn’t BSE suspend trading in the stock and prosecute the offenders? What is the use of putting artificial daily limits?

ASM is sometimes a negative, sometimes merely a created perception of negativity. Consider the criteria used by BSE for ASM. Stocks with limited stockholder participation in trading tend to go into ASM. I would not be surprised if a higher proportion of companies with >70% promoter holding are in ASM. SNCL has high promoter holding of nearly 75%, which is the maximum allowed for a public company. So, is BSE’s criteria for ASM saying that high promoter holding is a bad thing? In a way it is, since a small group of stockholders make all the decisions. I don’t think this is the point you are making about ASM. Generally high promoter holding is considered positive since the motivations of the promoters are aligned with the company.

The question in investing is whether ASM is already priced-in in the stock price or not. The stock may come out of the ASM in the future–that would be positive for the stock. There are various styles of investing. Some people invest only in low-beta stocks, some invest in distressed companies. Some people have a diversified portfolio whereas others have concentrated. No style is right or wrong.

2 Likes

Very well put. Thanks. And some points to ponder and research, especially about ASM. I will try that!

Regards

Sandeep

1 Like

Company doesn’t have good corporate governance moreover its not shareholder friendly due to following

- If you see the last 10 yrs PAT it had incurred losses in 7years and made negligible profits in 2 years and major profit only in 17-18 yr PAT is 31 crs and 18-19 81 crs. Management hasn’t played any role in turning company profitable its the price volatility( 4x in 1 year) of MAP and other chemicals due to ban in China.China is shifting its factory outside cities and price wont sustain

- If you Compare PAT and remuneration of promoters

Chairman 70 lacs __ 168 lacs(17-18 to 18-19)

Spouse 27 lacs ___ 168 lacs " "

Son 64 lacs ___ 168 lacs

How could you give same remuneration to person having 40 yrs of experience and one with 2 years of experience. - Company allotted 17.5 lacs preference shares in 2012-13 and around 75 lacs preference shares in 2015-16. When price of MAP started bottoming out and price went to increase, co passed a resolution that co will redeem its preference shares at 80% premium when its profitable. Is this type of governance co has

Strictly avoid bad corporate governance companies however attractive proposal is - Company has made allotment of 1.2% stake to Promoter at that time price was 241 and it has shooted up to 935 in next 9 months

4 Likes

The share has been in 10% upper circuit for the last 2 days and without any corporate announcement. It almost definitely trades based on insider information. The biggest problem with the company is that it is concentrated within very few hands, is engulfed in insider trading, and suffers from corporate governance issues which favor those few hands.

However, unlike the frequently copied-and-pasted refrain on the internet that “management hasn’t played any role in turning company profitable”, I believe the management has worked very hard to keep the company going during a long unfavorable period before 2017 and in growing its marquee clientele.

I continue to hold SNCL shares as a small percentage of my portfolio—failed to exit when the time was right. I will exit at some point of time, but that time is not now since the company is undervalued in my opinion and will benefit immensely in the coming years.