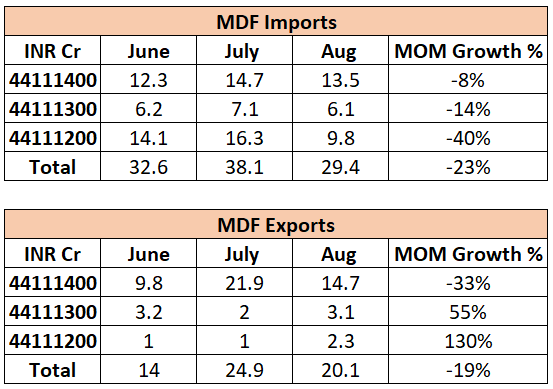

August import-export numbers are out. MoM slowdown in both imports and exports. One month data can’t establish a trend, but data may be pointing towards an overall growth slowdown.

August import-export numbers are out. MoM slowdown in both imports and exports. One month data can’t establish a trend, but data may be pointing towards an overall growth slowdown.

Buddy import slowdown is good for domestic players. Imports slowdown when price of imports is greater than domestic MDF.

Export slowdown could be because you are able to sell more in India and demand is strong.

Either ways the data does not seem negative but seems positive.

How common is it for secretarial auditors of a company to resign?

https://www.bseindia.com/xml-data/corpfiling/AttachLive/40a9b1a3-d11e-4268-9d4d-8785fb196780.pdf

Buddy import slowdown is good for domestic players. Imports slowdown when price of imports is greater than domestic MDF.

Export slowdown could be because you are able to sell more in India and demand is strong.

Either ways the data does not seem negative but seems positive.

@vnktshb Export slowdown is more likely due to slowdown in export demand, as mentioned in the interim brokerage reports I have shared above. Domestic demand should still be holding up, I agree. Let’s see. Data seems more or less neutral to me.

Freights continue to normalize, Freightos index down to 3700 now, about 2.6x pre-pandemic levels.

Though container freight costs have come down meaningfully, it is still 3.5x pre Covid levels and MDF import realizations are holding up. Stock is trading at a P/E of 10.9x after recent fall which is super cheap

PE multiple on current EPS isn’t the right way to look at a commodity stock IMO. Market looks forward and starts discounting next year’s or next to next year’s earnings and assigns a multiple to those earnings. Market most likely expects realizations and margins to compress as new capacity comes online in FY23 end, FY24 start and imports increase. Therefore, if investors are annualizing Q1FY23 EPS and calculating 1 Year FWD PE of ~10-11x, market is usually one step ahead and maybe factoring in a 20-25% earnings compression next year and assigning a multiple to that. Although, even with such an earnings compression, the stock has the potential to go higher from current levels.

Meanwhile Greenpanel keeps consolidating.

market is usually one step ahead and maybe factoring in a 20-25% earnings compression next year and assigning a multiple to that - can you share any data points/ report to test the assumption of 20-25% compression?

No I haven’t done the potential earnings compression analysis. There are 2 clear triggers for short-to-medium-term earnings compression - significant capacity coming online starting FY24 and imports potentially increasing towards or close to pre-pandemic levels if freight rates continue to normalise.

IMO its too complicated to model earnings compression as there are too many factors at play. I am just looking at current price action for Greenpanel and Rushil and adding to it the borrowed knowledge of experienced investors who have seen multiple commodity cycles play out (I have no lived experience of playing a commodity cycle yet), to hazard a guess that evaluating Rushil on the basis of annualized Q1-FY23 EPS may not be how market will value it.

Having said that I still feel Rushil is undervalued even considering the potential earnings compression. Also, the earnings compression is likely to be temporary - maybe for a few quarters - as growth in demand is expected to absorb the supply that is coming online. Unless of course, there is a domestic demand slowdown or an import glut due to knock on effects of a global slowdown, both of which at present are not 0% probability events at all.

All this is of course in the medium term. If somebody has a 5 year horizon for Rushil, I am sure all this won’t matter. That’s because there is a secular trend of MDF adoption in India and there is still massive headroom for MDF to grow and replace ply. I don’t have a 5 year horizon however and hence I worry about timing my exit. During the next 5 years, Rushil’s price will significantly fluctuate in tandem with demand and supply situations. I will try to time an exit and time a re-entry during these cycles. Best case I succeed, worst case I learn a few key lessons on commodity cycles. My position size is under control.

PS : I may be completely wrong in my analysis. Invested and keeping my eyes on several metrics to gauge demand slowdown/margin compression.

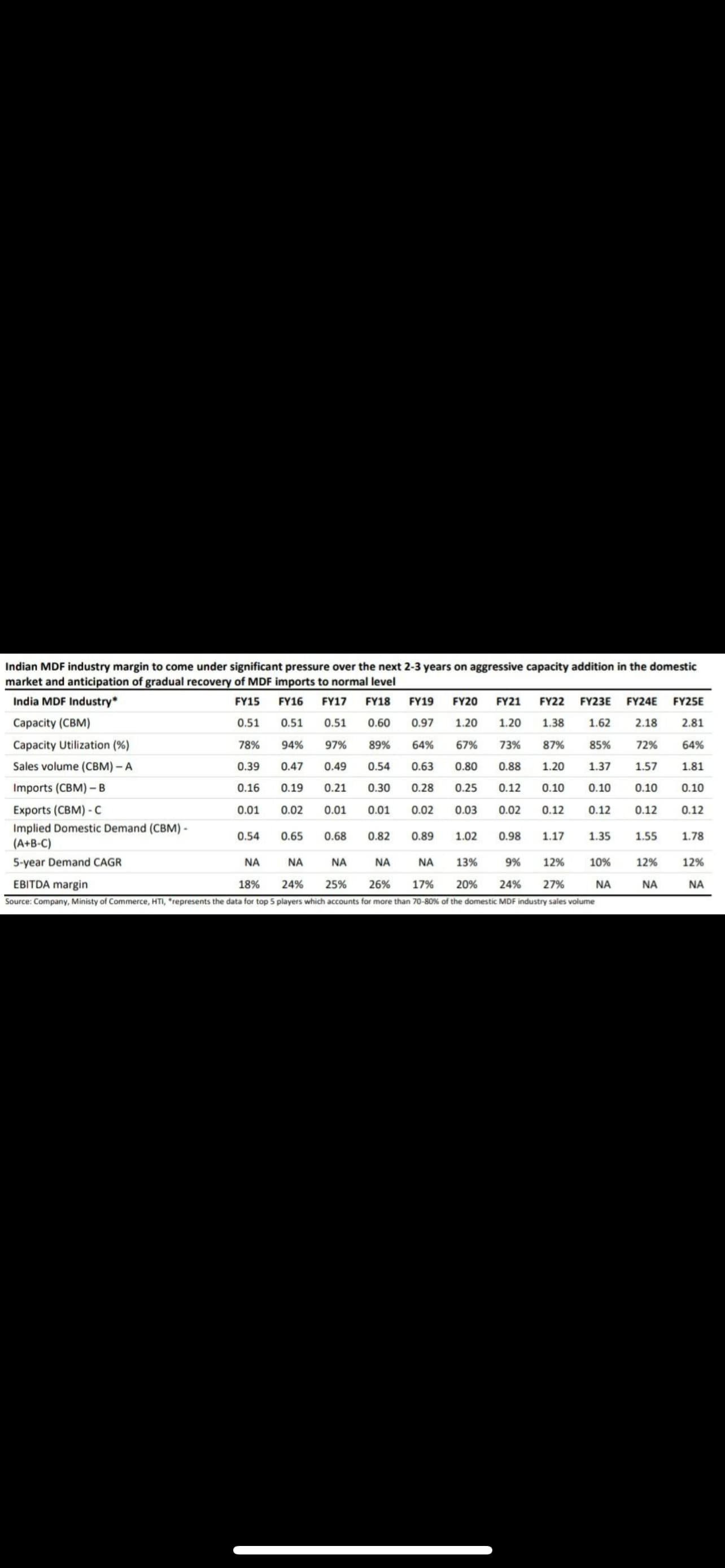

From Rushil Decor Press Release

Andhra plant has annual full capacity of about 2,40,000 CBM. With the help of this plant RDL has the potential to generate a revenue of Rs1000cr topline in MDF segment on full

capacity utilization.

FY22 revenues was Rs624crs out of which Rs434crs was MDF and Rs190crs was laminates

From Century Plyboard interview on CNBC TV18 in October 2022

Imports have increased due to decline in shipping costs. But due to 15-20% increase in MDF cost internationally, is helping domestic manufacturers utilize their capacity well. Though imports have no meaningful impact on North India MDF supply, the higher supply (led by imports) in South India is likely to continue and domestic industry will need to compete with imports going forward. MDF industry is currently growing by 15-20%, hence there isn’t an oversupply despite the increase in MDF imports.

Brutal drawdown in the stock in the month of October. I am trying to learn price-volume action for stocks. The price action for Rushil since October when it broke through the 520 support levels and closed the gap (474-520) and the volume action today, makes me think either results are quite poor or the resignation of the Secretarial Audit may have more to it than meets the eye.

Its also possible that Rushil has a good Q and price jumps back up (This happened recently in RACL Geartech, where the stock had started correcting in anticipation of Europe related slowdowns but results were strong and the stock is up 15% today), but the price volume action makes it look less likely to me. Greenpanel has also been consistently correcting.

Since I am trying to learn price-volume action and how to play commodity cycles via Rushil, I decided to exit my position today with minor profits. I was pretty torn about this decision and I am still not 100% sure about it. I don’t expect disastrous results from Rushil this Q, in fact results should be strong (Realizations may come down from Q1 but volumes should be strong). However, with freights coming down and imports resuming and exports coming under pressure sooner rather than later, peak margins are probably behind us. So its best to respect price action here in my opinion.

PS: None of the above is investment advise. I am a novice at technicals and commodity cycles. The above post is for shared learning and also to document my trades for future analysis.

2 things to add here to make this a case study for all:-

Greenpanel which is a player with much higher capacity and higher vap is getting a 15x Pe. Pe derating started when imports from South East Asia picked up.

When playing commodities:- understand where you are in the cycle. Once demand softened in Usa and Europe for Mdf. Import numbers for mdf in India started increasing as Freight normalized.

Rushil with a much lower added value mix might get a 10-12x pe when Greenpanel with a much higher value added gets 15x pe. Logical to think, at full utilisation assuming some margin contraction that is a mcap of 800-1000 crores.

Weighing risk reward, margins, where you are in the cycle, export/import data, and when supply comes on stream (FY24)+ Only then going to technicals is what funda investors can learn from here.

However the cost at which Rushil has installed capacity will be atleast 60-70% lower at which new capacities are coming in, within a time span of 1 year from installation.

This makes ROI much better for Rushil & also makes decision making tedious for competitors.

Roughly Rushil got capacity at 400CR & same is costing 650+ in current scenario

Replacement cost theory doesn’t help much when earnings is what market values…

Anyways machines wont be sold and cash redistributed to shareholders. Thus, difficult to understand these theories… better to value on Pe or other metrics

In this case i feel it will help as timelines for new facility to come into existence will be 2 years minimum. So they can cater to demand & fill market void, resulting in healthy cash flows. Also if this is a commodity play BEP for competitors increase, so tough call on their part

Again data differs here. Just check suppy coming on stream along with Se imports. In for peak commodity bust it seems. Imports have surprised the participants

On the contrary if you see for FY23 & FY24 expected capacity & demand, it establishes my POV, with demand & supply being at par almost. Also upcoming projects have to be delayed due to Europe crisis, as these machines are German imported & costs rising alarmingly.

Import estimates are already breached. Will show up from Q3 onwards

I think the view for after 2-3 years seems rosy right now. But near term there seems to be some headwinds. Imports have definitely picked up but the freight costs are no where near pr-covid level.

Greenpanel has mentioned that prices of quite a few of its chemicals including adhesives have been hiked which will be leading to margin pressure in the near term.

Given rising cost scenario with ample supply due to imports managements will not be hiking their product prices any more, hence their margins will be impacted in the near term it seems.

Long-term from a 3 year plus horizon given a healthy construction market they both seem very promising. The entire industry seems extremely lucrative from a 8-10 year horizon. Owner of action tesa expecting the entire industry to have a potential to be 10x in 10 years.

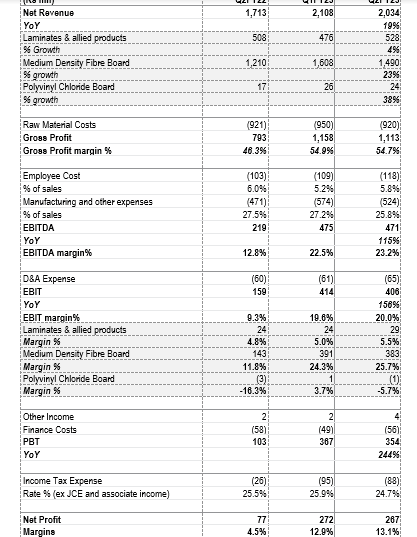

Please take note of the Rushil Decor results below and give your judgement!

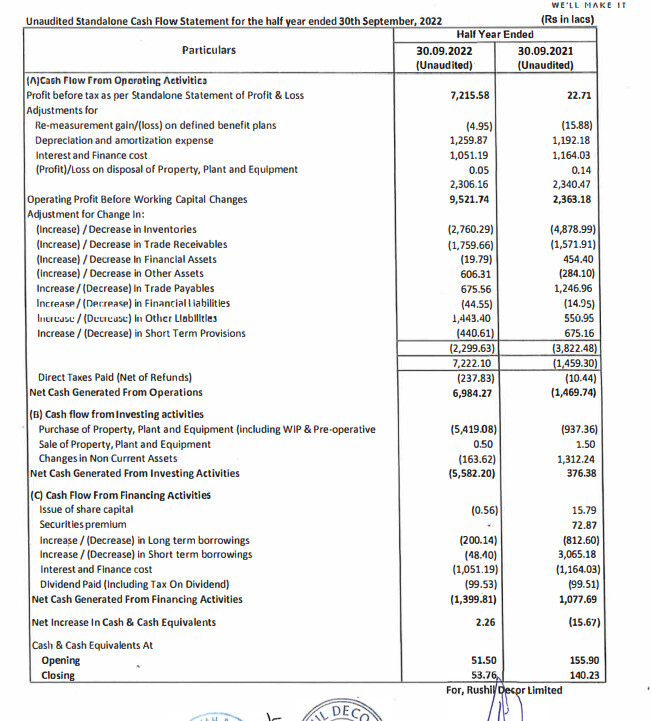

Look at the YoY growth and looks likes margins in MDF might have expanded QoQ. cash flows from operations have gone up significantly YoY. Rs27/share EPS in the 1HFY23

MARGINS in MDF - Improving in line with Management guidance of increased “Value added products”

MDF MARGINS

FY22 Q2 - 11.84%

FY22 Q4 - 15.00%

FY23 Q1- 24.30%

FY23 Q2- 25.72%

Rushil will set up a 1.2 million sheet p.a. new, modern, make-in-India, greenfield decorative laminates (including bigger size i.e. Jumbo size) manufacturing plant in Gujarat. The investment in the fully-integrated plant amounts to Rs. 60 crore.

QoQ check, seems utilisation or realisations have fallen in mdf.

YoY doesn’t matter here as plant utilisation for MDF must have been extremely low.

Mr. Market it seems already was expecting this…

P.s Last comment here on this thread. People unnecessarily get offended when even slightest of discomforting evidence is posted on the company they own…

This isn’t only the case with Rushil, also check Greenpanel QoQ. Market values future more than past. There too QoQ there’s a fall

if someone is spreading gloom and doom, then one should be happy and add more at CMP if conviction is still intact. ![]()

Thoda gloom doom faila do yaar cement stocks mein, lene ka hai ![]()

Good results

EPS 13 Sep Qtr, same as Jun Qtr

Annualized EPS 50

Stock cheap at 400

results are subdued, but not bad in any way, for both greenpanel and rushil…

Key questions that each investor should answer (IMHO) = what timeframe they are looking at; what are the industry prospects; what’s underlying business strength - sales/pat/ cfo/ wc days etc.; what valuation are they willing to buy the stock at; what’s the right to win for each player…