Rushil Decor is a building materials company which is into manufacturing of MDF, laminate sheets and PVC boards. On a TTM basis, MDF division comprises of 64% of revenues whereas laminate sheets comprise of 35% and the PVC boards < 1%. Company sells its products under the brand name - Vir (Vir MDF, Vir Laminates).

Industry Analysis

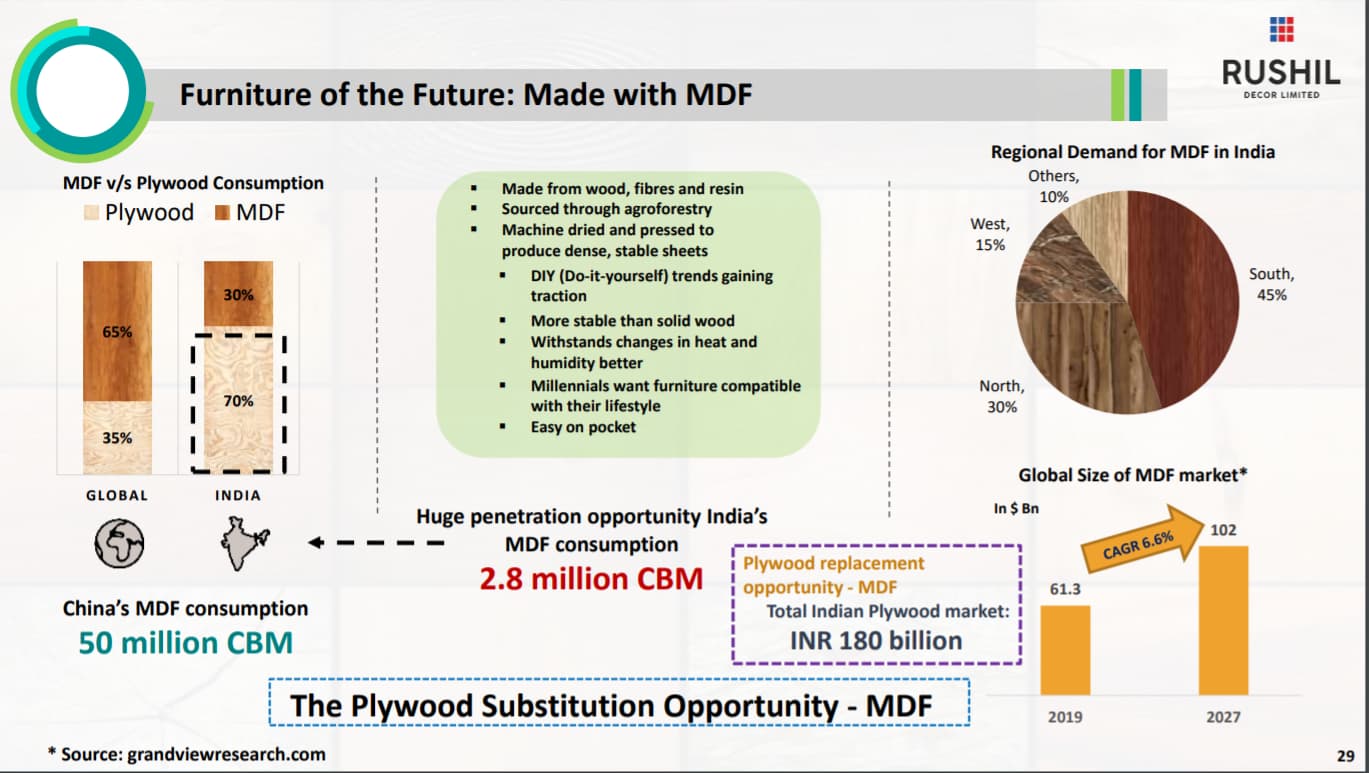

1. MDF vs plywood - In the furniture industry, traditionally India has been a plywood market. MDF adoption is a fairly recent story (Since 2010s). Globally, MDF comprises of 65-70% value share in the furniture industry whereas plywood only has 30-35% share. In India, the %s are reversed with MDF only having a 35% share. However, MDF adoption has picked up massively in recent years as modern furniture manufacturers prefer MDF over plywood. One of the main reasons for MDF being a preferred furniture material is because MDF manufacturing is a 100% automated, factory-led process with zero manual labour involved whereas plywood is almost 100% manual labour led. This obviously leads to much higher uniformity, consistency and smoothness of colour and finish in the quality of MDF surfaces compared to plywood surfaces which makes it a better material for furniture manufacturers. For the same reason, MDF also gels better with millennial aesthetics and therefore most of the low cost furniture we see today from brands like Pepperfry or Urban Ladder or IKEA are made of MDF (The costlier ones are made from real wood).

2. Organized vs Unorganized industry - While most of the plywood industry is comprised of unorganized players, 100% of the MDF industry is organized and it will remain that way going forward. Reason for this is that setting up a state-of-the-art MDF plant is very capital intensive as it requires German machinery. Fixed asset turns are in the range of 1.2x-1.6x. Foe example, Rushil’s new plant in AP was setup for a capex of INR 450 Cr and depending on realizations per CBM, can generate a max topline of INR 720 Cr at full capacity. A 100% organized industry provides a lot of comfort to investors as the behaviour of industry participants are more rational and predictable.

3. Raw materials - The main raw materials used for manufacturing MDF is wood fibres and binding chemicals and adhesives. The wood fibres (primarily eucalyptus) are all taken from plantations in India and to that extent there is no wooden raw material risk

risk from China or other countries. Chemicals may be imported to an extent but I don’t expect them to be greater than 15-20% of the total r/m cost of MDF manufacturing companies. This protects MDF companies largely from shipping costs and forex risks.

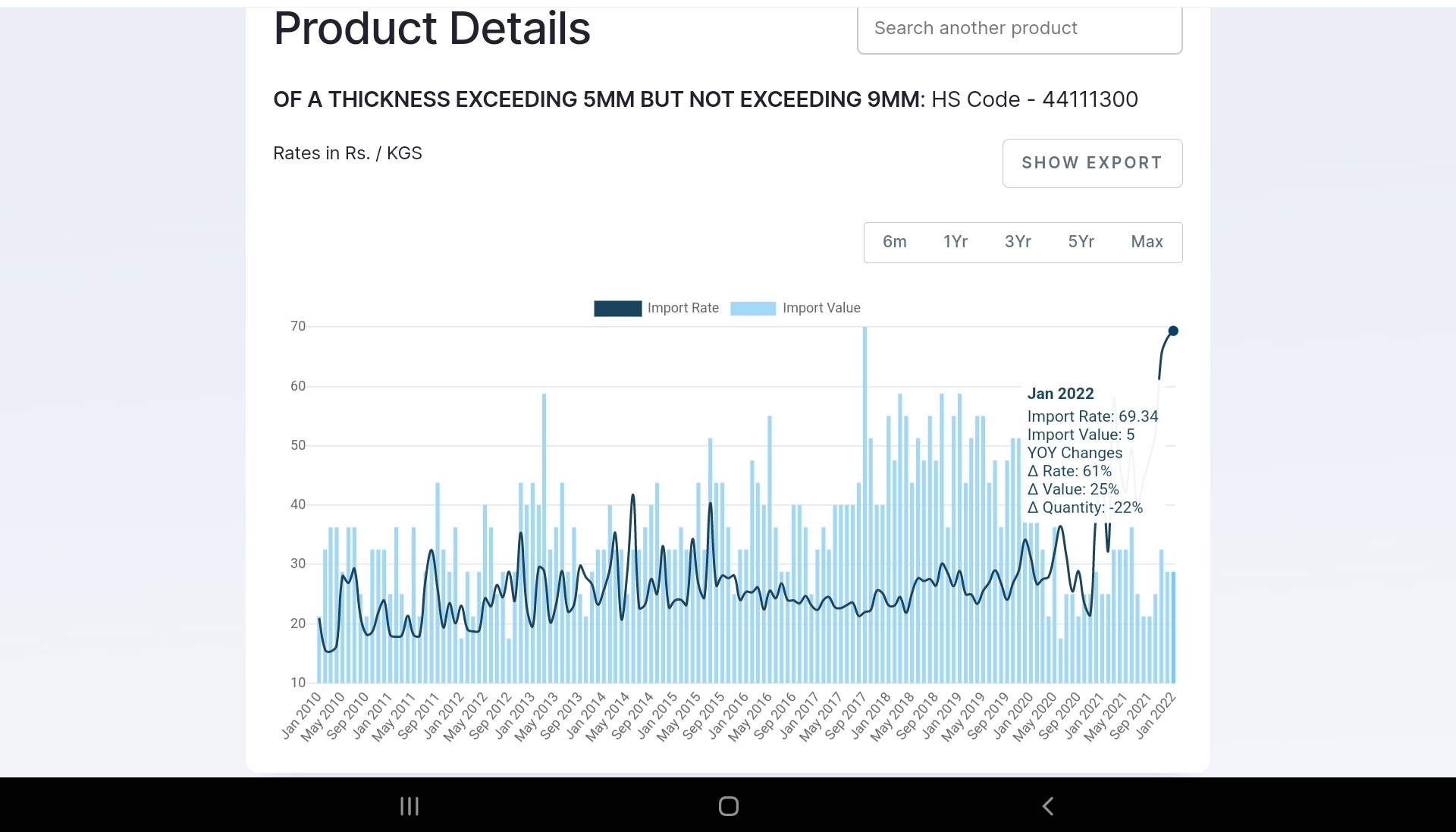

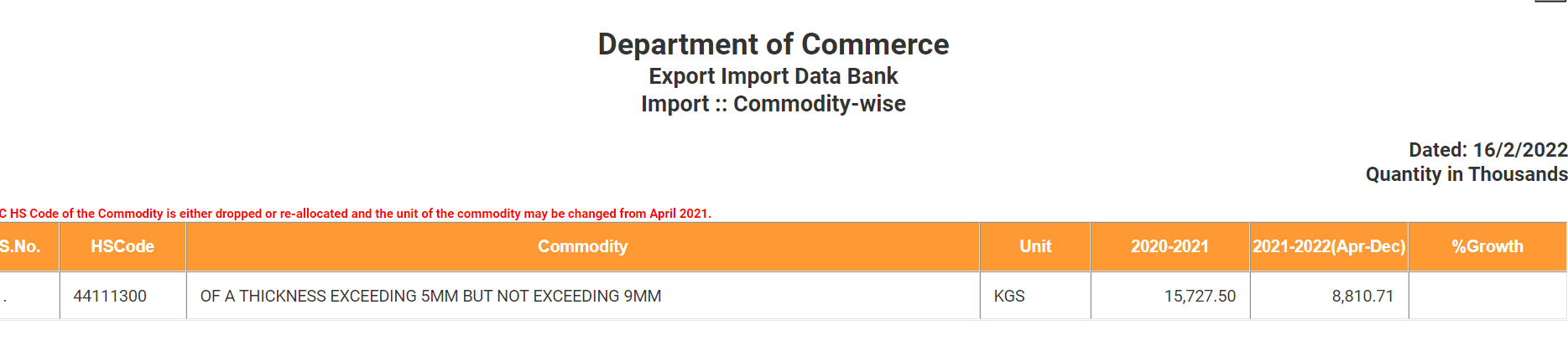

4. Imports from China and SE Asia - Whenever we talk of any commodity, our biggest risk factor is dumping of cheaper material from China and SE Asia. Fortunately, going by the commentary from the leading MDF players in India, it seems that imports are not likely to be a threat at least for the coming 4 quarters. This is on account of increased usage of MDF in home countries and increased share of furniture exports to Western markets from China and SE Asia. Therefore, their capacities aren’t free for less remunerative volumes in India. As you can see below, imports of MDF (HSN codes : 44111300 and 44111400) are down by 30-35% on a yearly run rate basis. Imports are a key risk for this kind of an industry and the present situations seems to protect the MDF industry from this particular threat for the foreseeable future.

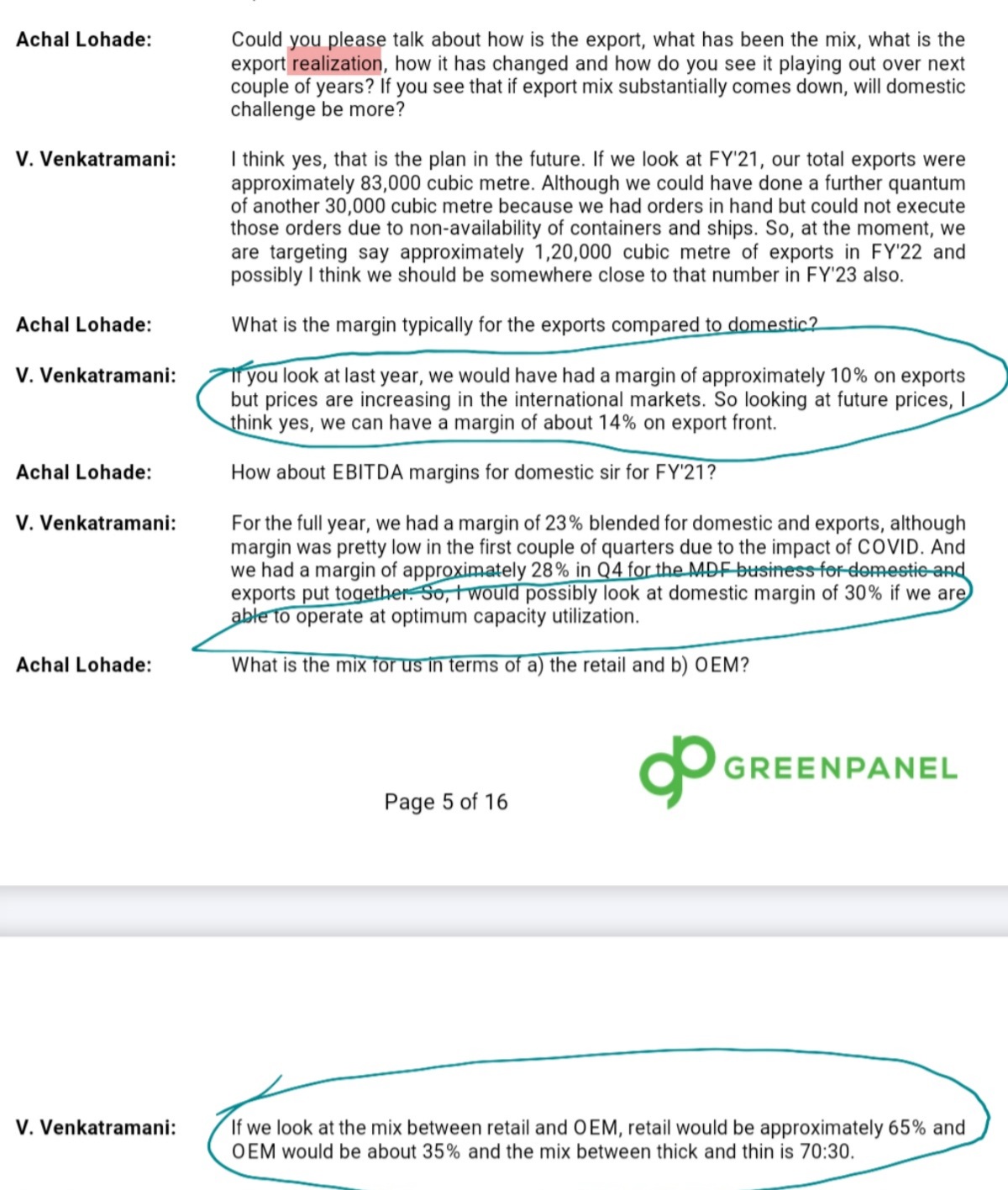

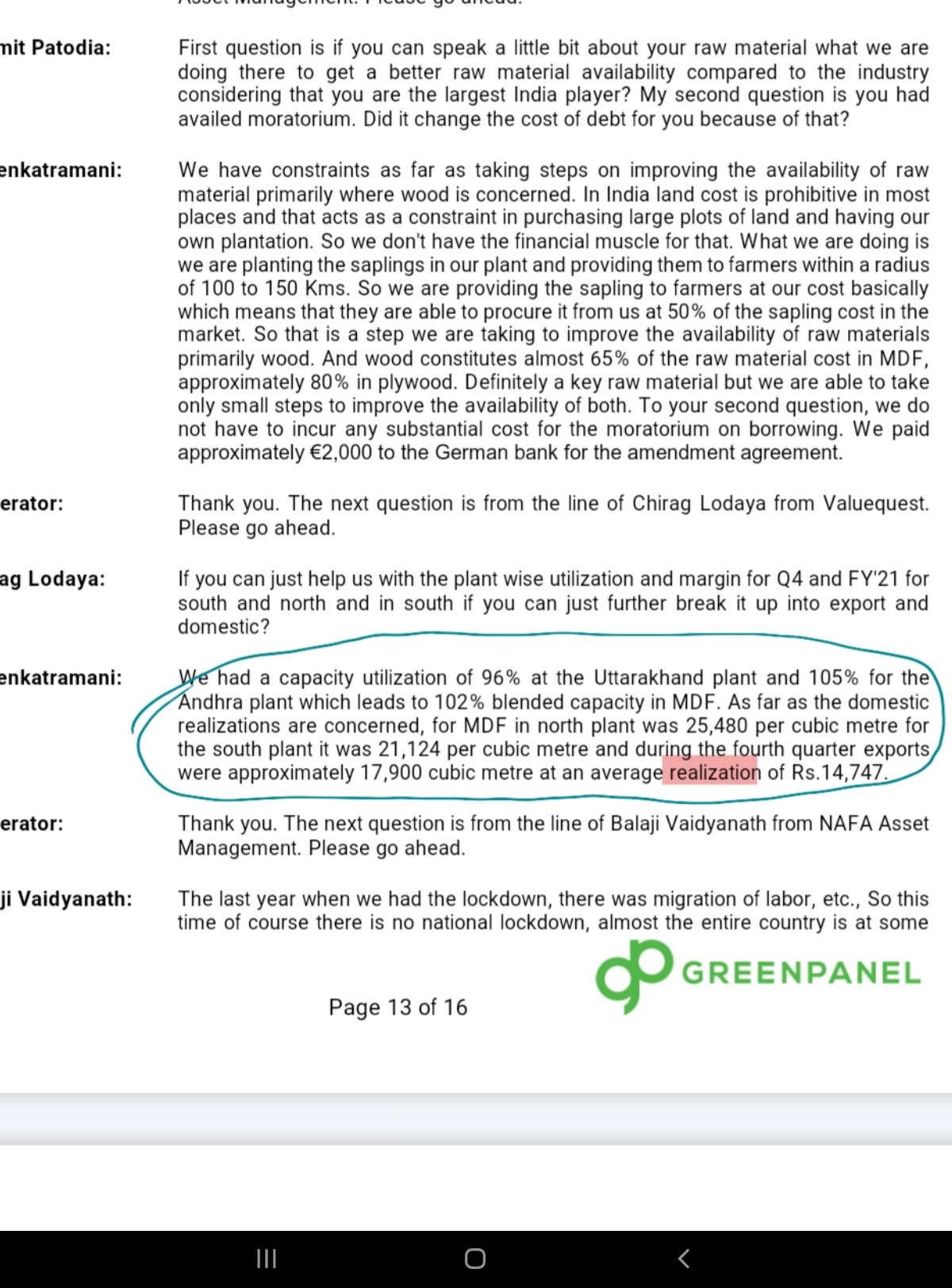

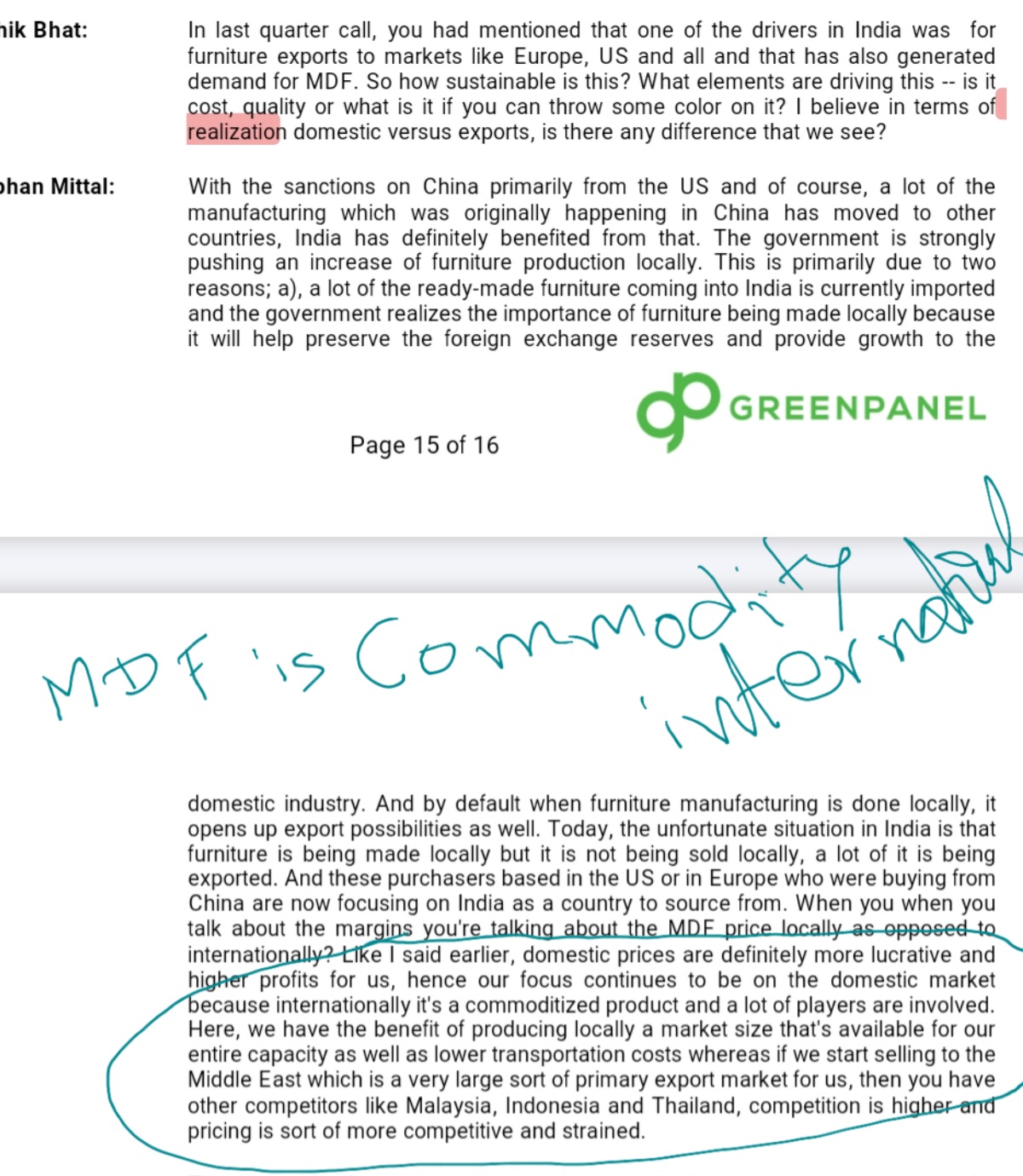

5. Exports - Due to Covid there has been a global shortage of MDF availability. This gave an opportunity for leading Indian players to increase their share of exports at good realizations (Generally export realizations are lower than domestic realizations). This opportunity of higher export realizations is also likely to continue for a few more quarters.

6. Demand - All industry participants expect demand to grow robustly in the medium to long term with growth CAGRs of 15-20%. Real estate revival and increased substitution of plywood by MDF are the two key triggers driving demand growth. Present demand is at a yearly run-rate of ~14-15L CBM and at a CAGR of 15-20% is likely to be at 21-25L CBM by end of FY25.

7. Supply - Present per annum installed capacities and upcoming capacities are as follows:

Greenpanel - 6L CBM

Action Tesa - 4.2L CBM

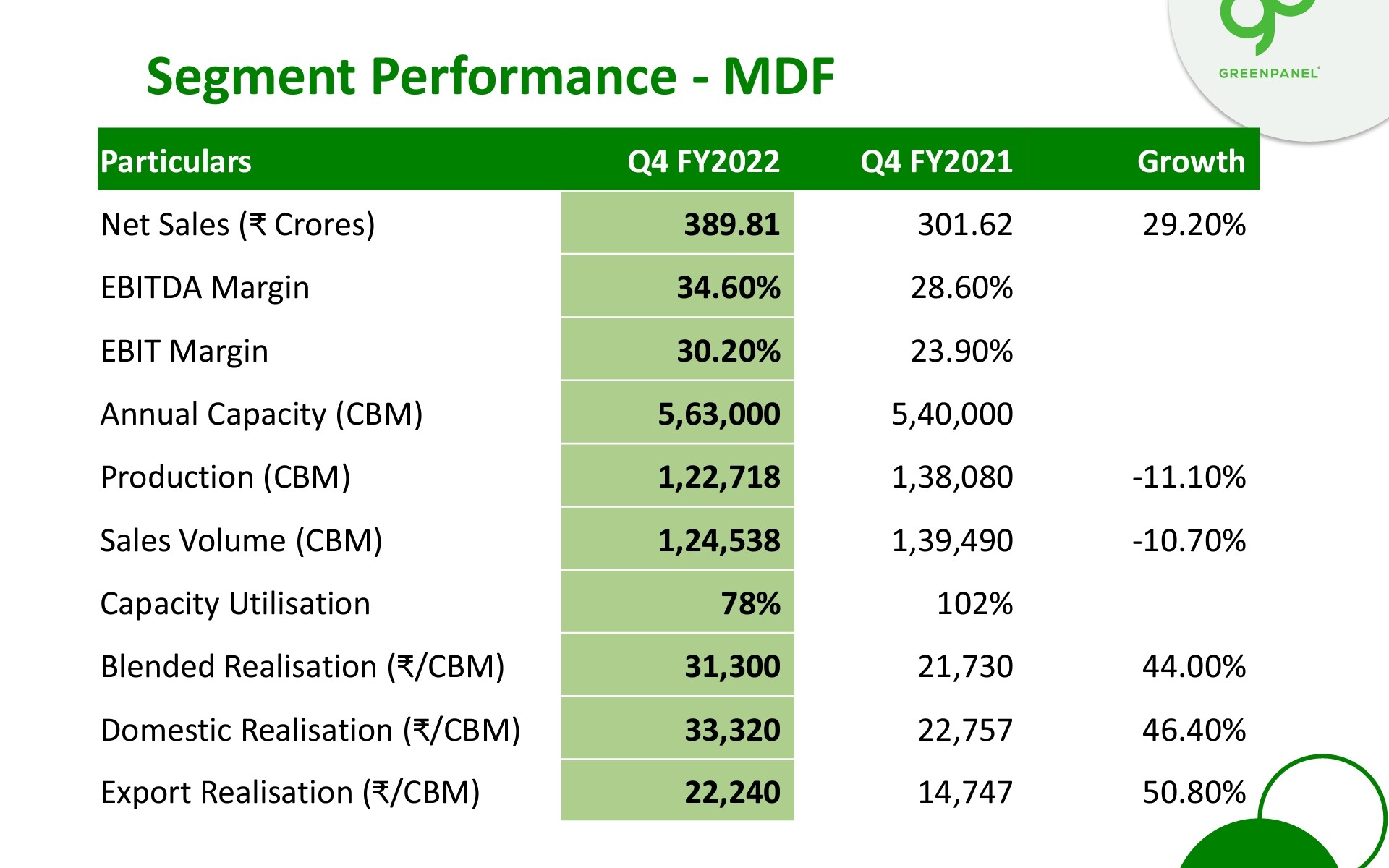

Rushil Decor - 3.6L CBM (New capacity. FY22 utilization will be ~60%; full utilization from Q4 FY22 onwards)

Century Ply - 2.2L CBM

Century Ply - 4L CBM (Upcoming capacity - Greenfield plant in AP - Q3 FY24 and brownfield in Hoshiarpur, Punjab - Q2 FY23)

Greenply - 3L CBM (Upcoming capacity in Gujarat - Q1 FY24)

Other players - 1.3L

Total visible capacity by FY24 end - 24-25L CBM. Its likely that capacity in FY25 will be around 28-30L CBM (Greenpanel is expected to announce new capex in coming quarters). At a projected demand of 21-25L CBM, this will mean an overall capacity utilization of 75-85% which is high enough to ensure margin stability. In summary, there is no over capacity problem anticipated in the medium term (provided import situation remains as described)

Rushil Decor Opportunity

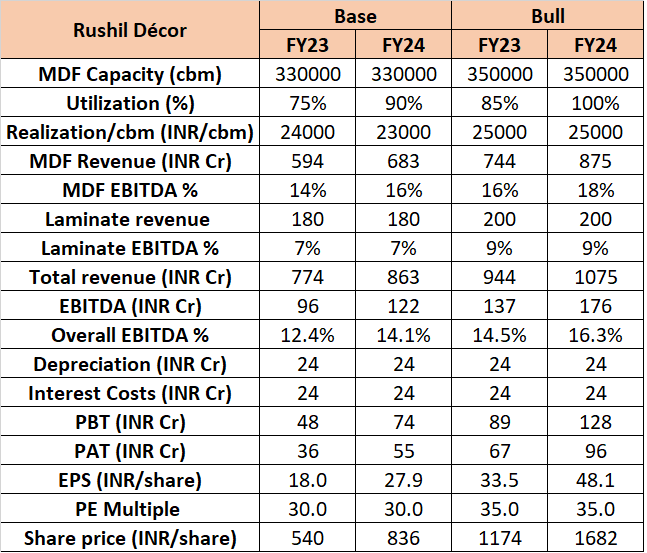

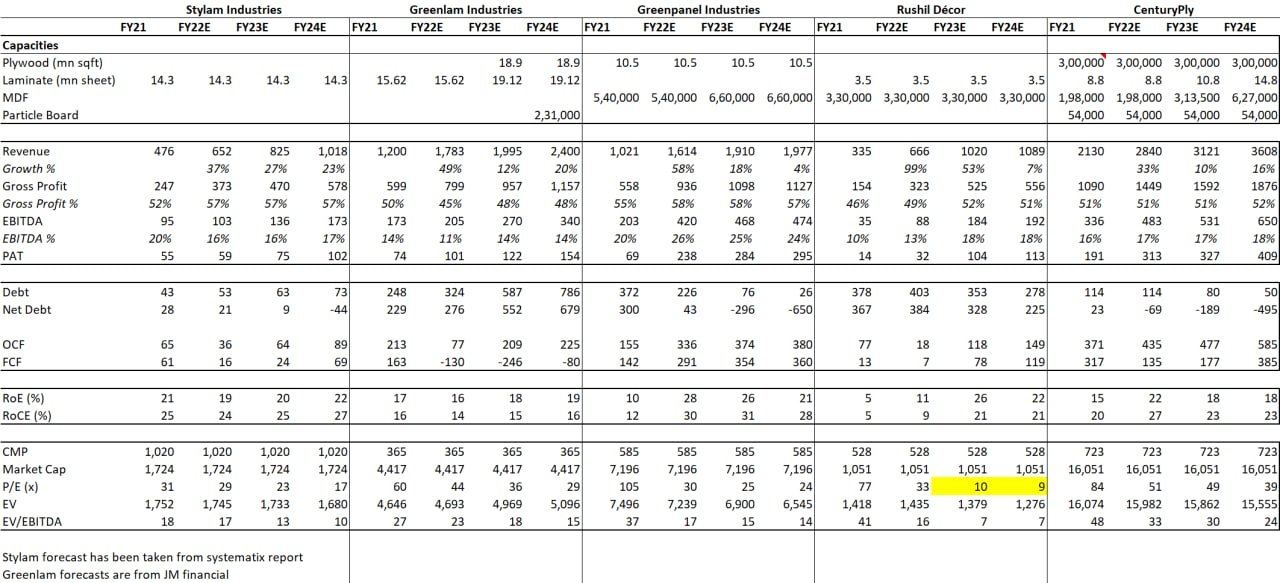

While the MDF industry as a whole is a great investment opportunity in the long term (5+ year horizon) Rushil Decor is best placed to provide outsized returns to investors in 1-2 year horizon I believe. Reason for that is they have recently commissioned their 2.5L capacity AP Plant in Q1 FY22. After overcoming initial hiccoughs in running the plant at higher capacities, this Quarter Management has come out with very bullish commentary regarding the Plant and has said that they have been able to operate the plant at 80% capacity in December. Going forward they expect to run both their plants at 75% capacity (Demand is not a problem). Realizations have also increased 15% Q-o-Q and a further 5-10% increase is expected in Q4. Realizations are still some way away from market leaders Greenpanel (less by 7-10%) but this gap will go away as ramp up of value added MDF production happens in the newly commissioned AP Plant. Given the bullish commentary by management on demand environment and new plant capacity ramp-up, quarterly EPS is likely to jump to and sustain at INR 6/share from Q4. This would mean the company is currently valued at 17x FY23 EPS (CMP 415). This seems cheap for a company with long term growth prospects such as Rushil.

The present debt/equity ratio is high at 1.5x. But this isn’t a major concern in my opinion for the following reasons:

- The nature of the beast is such that high capex is needed to setup a plant. Given that Rushil was in a lower EBITDA business of laminates before, it was natural it had to take on a large debt burden to do the capex of INR 450 Cr. Players like Greenpanel have gone through the same high debt cycle but now they are paying back debt at a rapid rate thanks to full capacity utilizations and good cash flow.

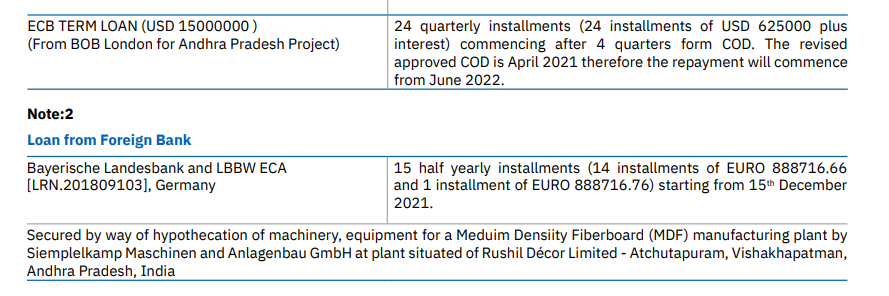

- A large part of the debt is German debt financed at 3.2% p.a. and the forex risk of the loan is more than 100% hedged by its exports. Blended interest cost p.a. for the company is low at 5.9%. Given that Rushil will operate at full capacity from Q4 onwards, cash flows and EBITDA will improve and therefore I don’t expect the debt to be an overhang on company performance.

The laminates business is a stable business with ~200Cr yearly run-rate and EBITDA ranging from 8-10%. PVC boards business is very new and is EBITDA negative. Therefore, not much to analyze in the other 2 segments.

I see the MDF industry and Rushil Decor especially as a great play on real estate revival in the medium term and secular MDF adoption as a replacement of plywood in the long term.

Disclosure: Invested in both Greenpanel and Rushil Decor with transactions in Rushil Decor in last 7 days.