Hi, Baltic Dry Index is an index for shipping freight for dry bulk materials such as steel, grains, coal etc. This is not the right index for tracking containerized freight which is used to transport MDF/HDF.

Ocean freight is classified into dry bulk vs containers vs tankers (liquids) as far as I know.

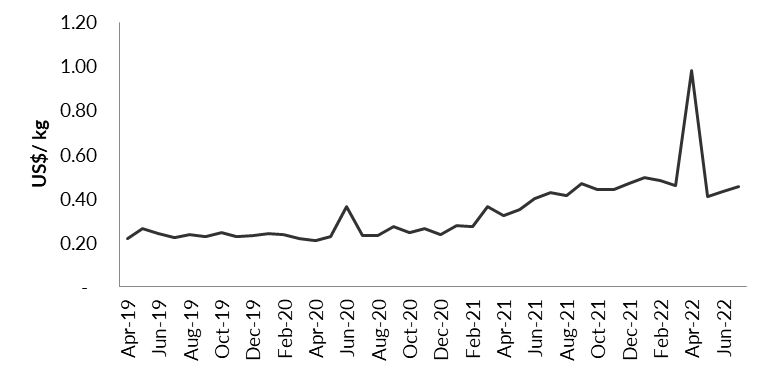

While container freights are also coming down MoM, they are still 4X the freights that persisted during Q1FY20-Q1FY21, the last annual period with significant import values.

I expect dry bulk freights to capitulate much faster than container freights going forward. This is because China RE Sector is slowing down alarmingly and China RE is the world’s largest consumer of dry bulk commodities.

Thank you @nirvana_laha, the actual pricing data is behind paywall… but you’ve mentioned the current prices are still 4X pre-covid levels, it’s reassuring

I’m still wondering if dry bulk and container shipping are water tight compartments, which can’t service the other sub-segments… maybe when the price differential exceeds a threshold, repurposing may kick in… (just a loud thought)… knowledgeable boarders may correct

Thank you @nirvana_laha, the actual pricing data is behind paywall… but you’ve mentioned the current prices are still 4X pre-covid levels, it’s reassuring :blush:

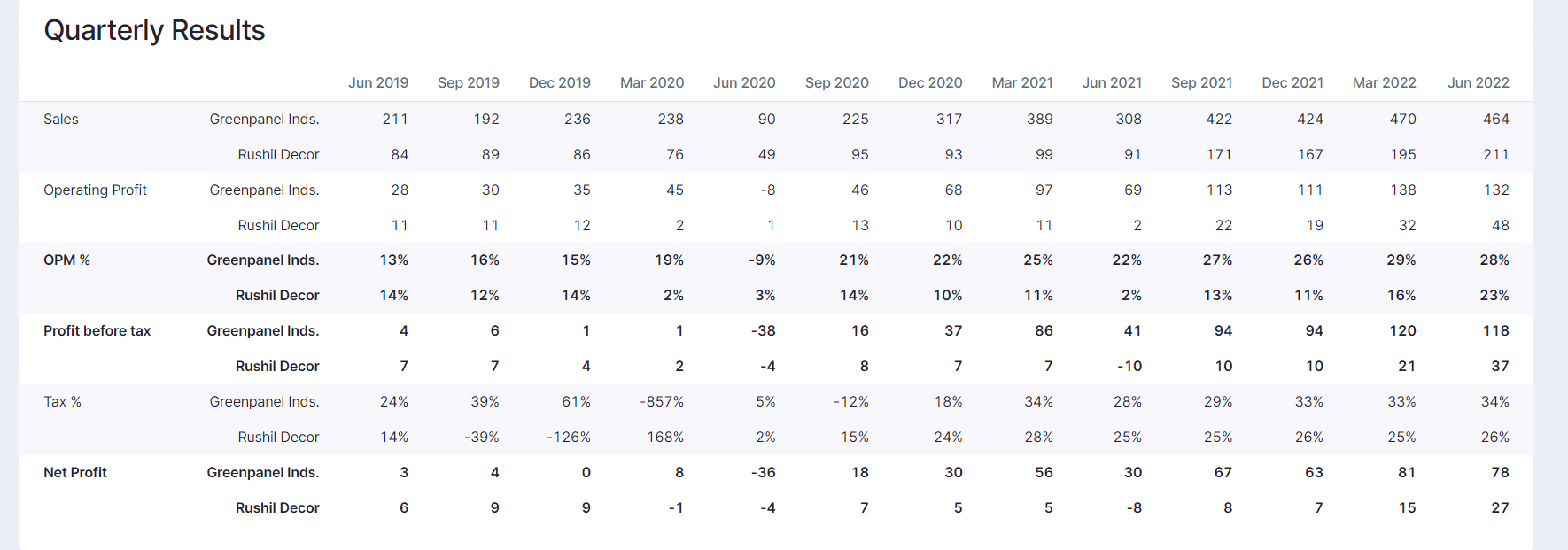

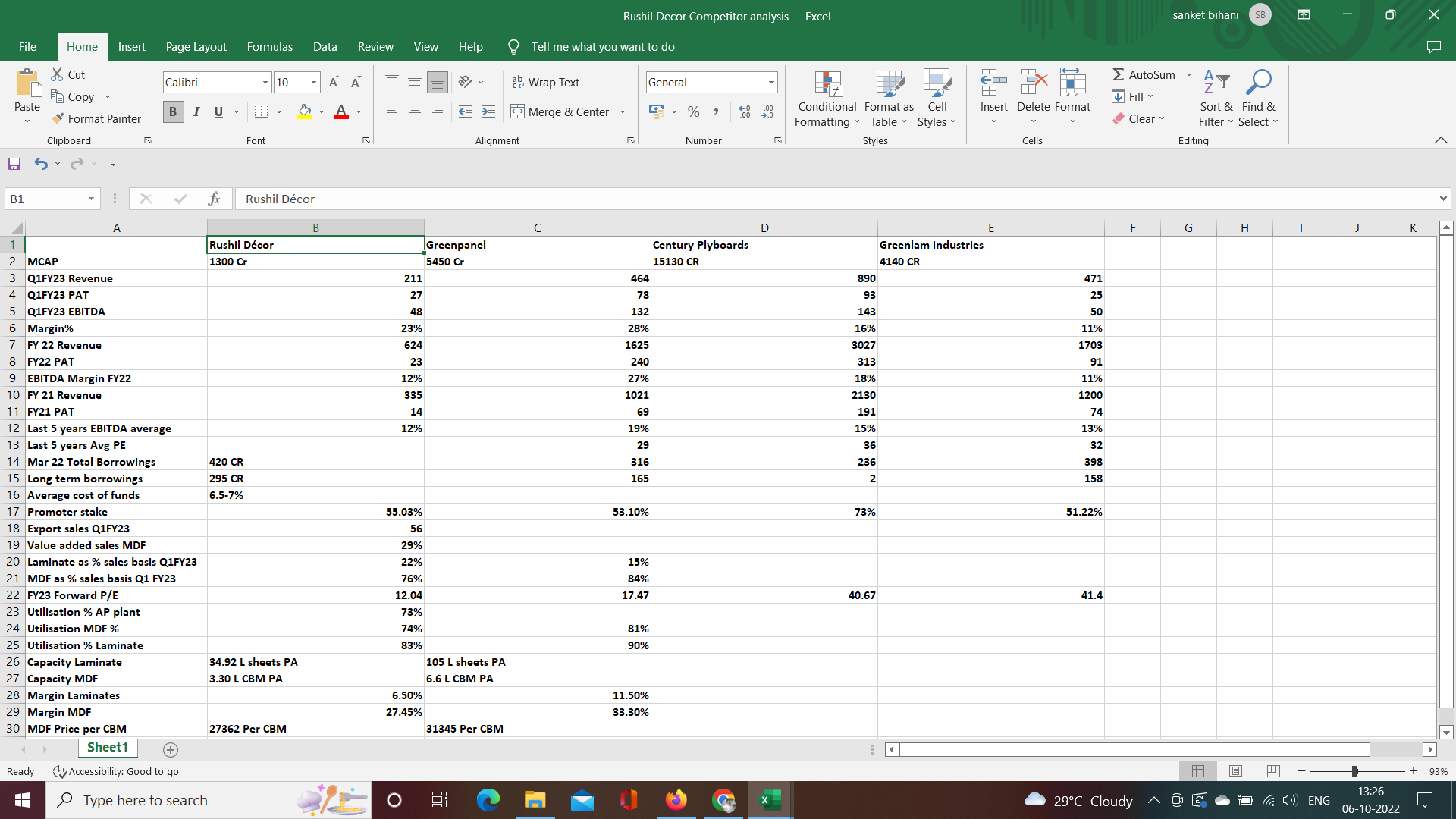

From an MDF perspective - Greenpanel seems to be a much better play - Better Numbers + Better Valuation + Dominant Market Share? Any data points in favor of Rushil?

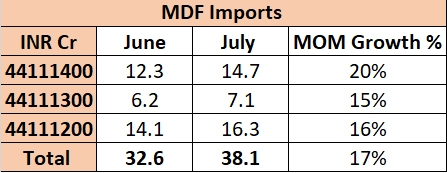

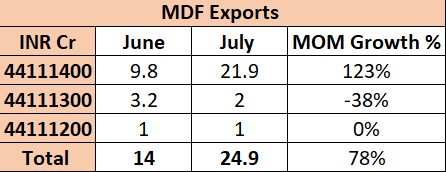

MDF imports have grown by 17% MoM but exports have increased by a whopping 78% MoM. June export numbers were low, so this MoM export growth is a little misleading. However, average monthly exports in Q1 FY23 were 25.5Cr, so the July numbers of 25Cr remain on trend and strong.

My interpretation : Freights are cooling off slowly but are still much higher than they were 2 years ago when imports were really strong. Export market remains healthy going by export revenues in July (Export realization data is needed to confirm this but that will only be available in Oct when Greenpanel releases its data).

Of course this data is with a lag of 1.5 months, so intervening changes in freights and import/export will affect real time data. Global freights seem to have come down by ~7% MoM from July to Aug, so this will have some incremental impact in Aug and Sep numbers.

Tracking freight remains a key for this stock. Going by the trend so far I am not expecting any significant dent in realizations in Q2. If freights keep coming down secularly in Q3 and Q4 then we might start seeing some moderation in realizations in late Q3-Q4. Shall wait for Q2 results to evaluate further.

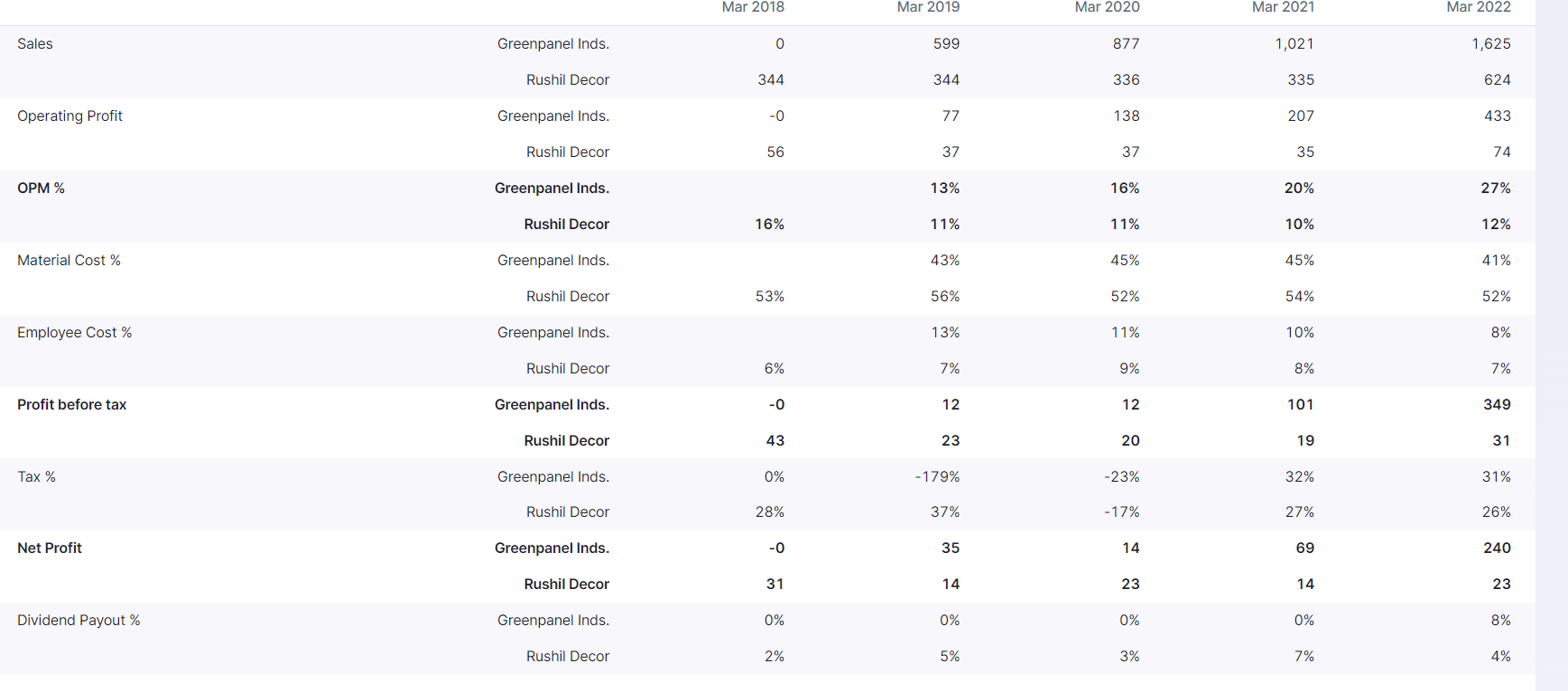

Investors make the most money when bad/worse numbers become good/better numbers. You need to study the 2 companies to understand in the near term, whose financial are going from not-so-good to good and whose are remaining stable.

Assuming Rs900crs revenues and 22% margins we get to Rs198crs EBITDA. Assuming no reduction in interest costs of Rs20crs and depreciation is 25crs PBT would be Rs173crs. PAT after 25% take would be Rs130crs.

Current market cap is Rs1281crs. Rights issue is 1:3 so new market cap = 4/3*1281 = Rs1708crs.

So at current price stock is trading at Rs1708crs/130crs = 13.1x P/E post dilution.

On the argument that RoE of company is too low, lets calculate FY23 RoE and see. FY23 PAT estimate is Rs130crs. FY22 Networth was Rs287crs. So FY23 networth = Rs287crs + Rs130crs + Rs200crs (assuming peak rights issue) = Rs617crs.

So RoE = Rs130crs/Rs617crs = 21% which is more or less inline with the all the good companies in the industry.

BTW 3.38% of Rushil Decor is owned by Sajjan Bhajanka who is the Chairman of Century Plyboard

I wonder if the Rushil Decor - rights entitlement trading is impacting the stock price of Rushil Decor? But when I look at NSE the rights entitlement is hardly trading. So why is the stock so weak over last 3 to 4 days even though its so cheap. Any insight?

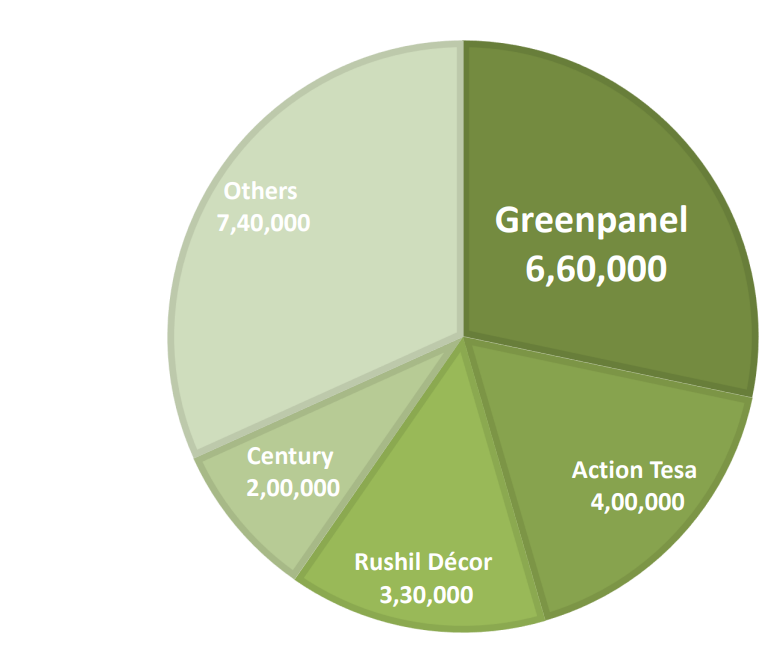

Promoters of competitors (Century and Action Tesa) of Rushil Decor bullish on the company

Greenpanel is operating at almost full capacity. New capacity coming up in FY25 and management is guiding down margins for FY24 which implies where limited PAT growth. That might be the reason why the stock is consolidating

Have been trying to use some chart patterns and price-volume action in Rushil. Rushil closed below the first key support level of 579 today. The next strong support is at 520 where the stock opened with a huge gap up over the previous day with very high volumes right after Q1 results were announced. Price dropping below 520 is a leading exit indicator for me.

I had read that the MDF companies are trading at highest margins which is expected to weaken in next few quarters…thats the reason why companies like Greenpanel and Rushil Decor are correcting…

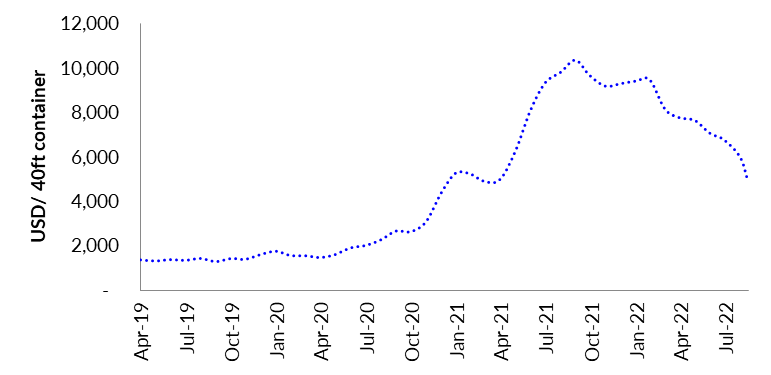

One of the reasons why MDF players like Greenpanel and Rushil was doing well was very high container freight rates and no local supply. At the end of the day , MDF is a commodity and they had to compete with cheap imports in Pre-Covid era. Container freight rate is coming down at an accelerated pace and there is a fear that it may come down to a level where imports of MDF to India will again become competitive. This may be the reason why there is a pressure on both the counters (Green Panel, Rushil). It may be worthwhile to check with the management in next conference call about the level of container freight rate at which MDF imports will become competitive. Here is the chart of container freight rate.

Though container freight costs have come down meaningfully, it is still 3.5x pre Covid levels and MDF import realizations are holding up. Stock is trading at a P/E of 10.9x after recent fall which is super cheap