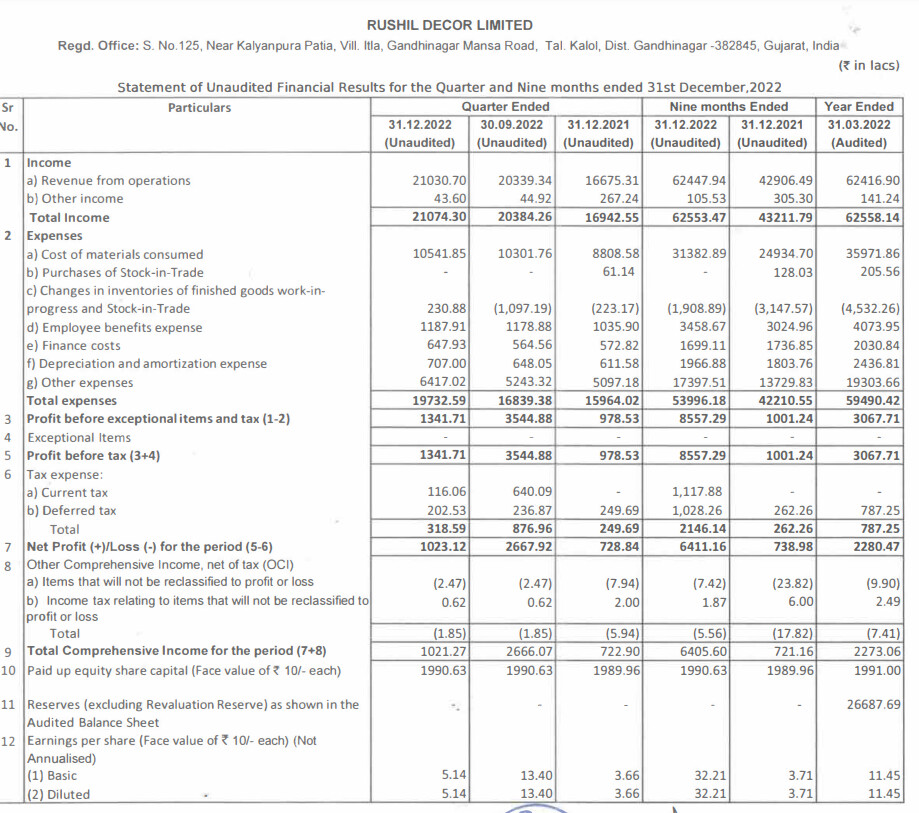

Q3 results are poor. Margins collapse - EBITDA down QoQ from 23% to 12.6%. MDF segmental EBIT down from 26% last Q to a measly 9% this Q. Shows the amount of margin pressure in MDF due to increasing imports.

The margin situation was abnormal for the industry for the last 2 years due to Covid related logistics cost hikes and Asian imports being diverted to Europe & USA. Both of these seem to have reversed now. I expect margins to remain challenged while the upcoming new capacities get absorbed over the next 1-2 years. Unless there is another global supply chain issue, imports are likely to remain steady, thus keeping pressure on domestic margins.

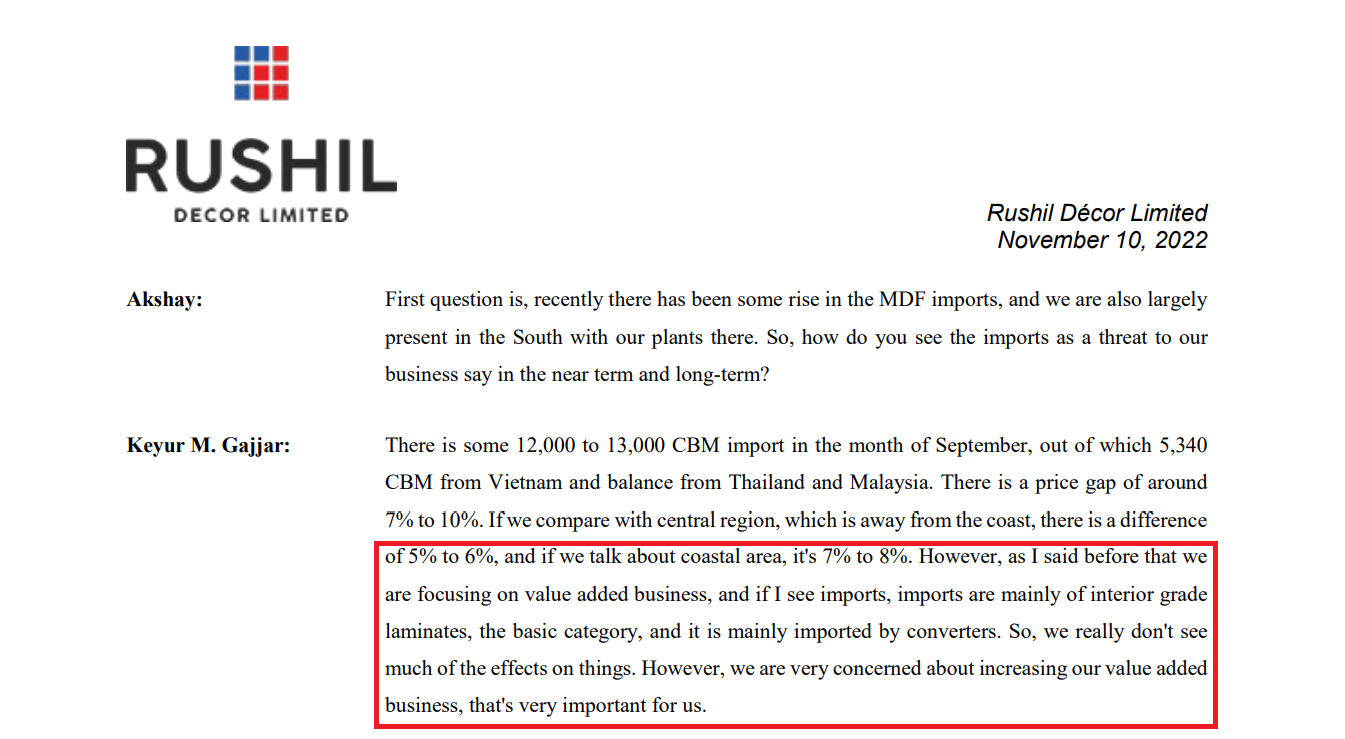

This is what Rushil management had to say about the threat of imports in Q2 concall.

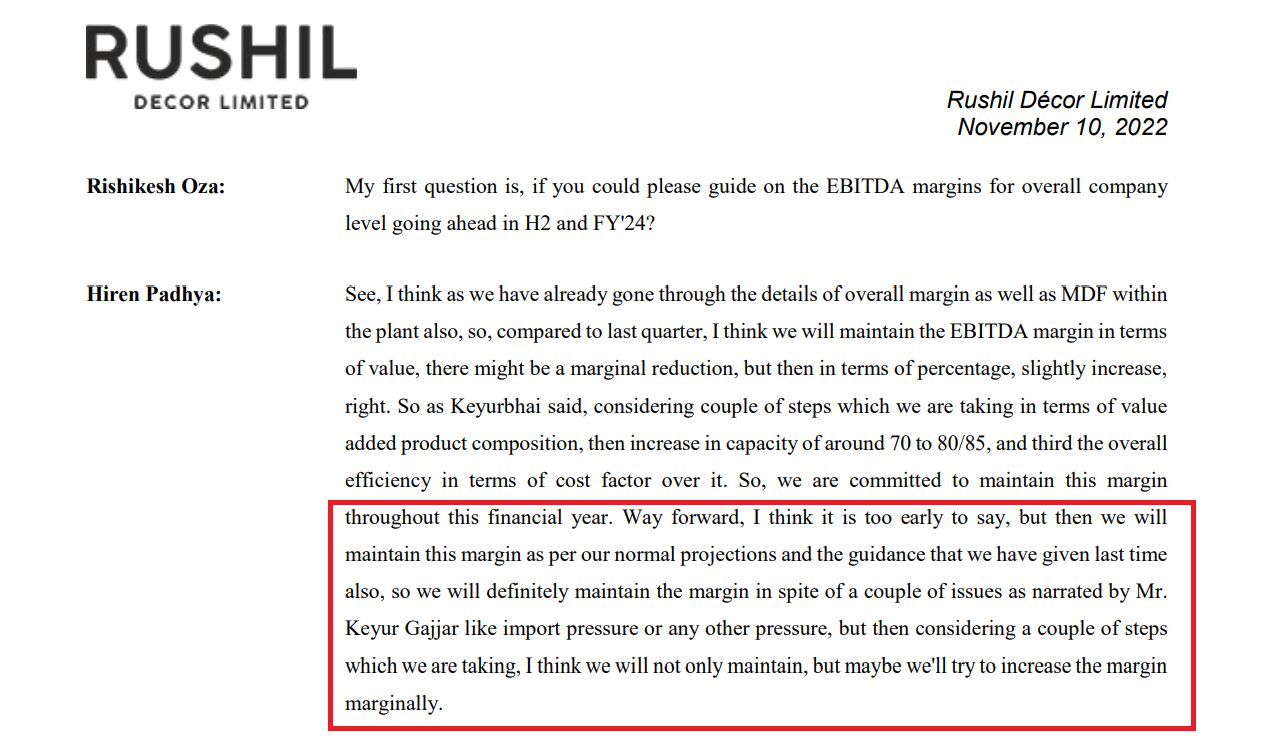

Forget margin compression, Rushil Management had guided for possibly slight margin expansion for Q3-Q4. After that guidance in Nov, EBIT margins in MDF have collapsed from 26% to 9% QoQ.

Disclosure : Was invested, exited in Oct basis price-volume action and import trends. Exit rationale was posted in detail here

Brutal drawdown in the stock in the month of October. I am trying to learn price-volume action for stocks. The price action for Rushil since October when it broke through the 520 support levels and closed the gap (474-520) and the volume action today, makes me think either results are quite poor or the resignation of the Secretarial Audit may have more to it than meets the eye.

Its also possible that Rushil has a good Q and price jumps back up (This happened recently in RACL Geartech, where the stock had started correcting in anticipation of Europe related slowdowns but results were strong and the stock is up 15% today), but the price volume action makes it look less likely to me. Greenpanel has also been consistently correcting.

Since I am trying to learn price-volume action and how to play commodity cycles via Rushil, I decided to exit my position today with minor profits. I was pretty torn about this decision and I am still not 100% sure about it. I don’t expect disastrous results from Rushil this Q, in fact results should be strong (Realizations may come down from Q1 but volumes should be strong). However, with freights coming down and imports resuming and exports coming under pressure sooner rather than later, peak margins are probably behind us. So its best to respect price action here in my opinion.

PS: None of the above is investment advise. I am a novice at technicals and commodity cycles. The above post is for shared learning and also to document my trades for future analysis.