Communications Platform as a Service industry market size was estimated at $12.5bn in 2022 and projected to reach $45.3 bn over next 5 year at a CAGR of 29.4% as per a report by MarketsAndMarkets

Messaging (SMS, Whatsapp, other OTT, RCS), email, Voice, Video, Chatbots etc all form a part of services which gets rolled into this industry. The driving force is to offer Omni-channel messaging services to enterprise customer, ideally from a single API.

Digitization in general and transactions (Banking, UPI, E-commerce, Travel etc) in particular are driving the heady growth number of messages being sent out daily. Initially starting as a one way communication (A2P), now two way communication is becoming mature and diverse use cases are being driven on them. Whatsapp messaging is positioning itself as a workflow driven, rich media, two way communication enabler - something akin to what the chatbots do. Chatbots are now graduating to Natural language processing and using AI to be able to provide users an opportunity to interact in their natural way of “speaking”.

Other than Whatsapp, Truecaller is another app, which is trying to monetize its presence as a SMS client to drive OTT messaging. Presently starting as an SMS alternate, but likely to go the Whatsapp way as it develops its solutions.

India as a country is today in many ways a leader in the fintech space, with humongous volumes being processed. Messaging tags along with transactions - whenever a transaction happens, user has to be informed that a transaction has occurred - be it SMS or email or message on whatsapp and sometimes more than one channel. As an example, 30Crore+ (300mn) UPI transactions are being processed daily in India. There are two parties (sender and receiver). Assuming even 25% of these users have subscribed to / enabled SMS alerts - one can start appreciating the sheer volumes that are happing. And UPI is just one case, albeit the largest one.

UPI is growing at more than 40% CAGR (RBI expected it go grow at ~50% in 2022). Other digital transactions are also seeing high growth. With these kind of numbers it is perhaps, quite feasible that industry could conservatively grow at 20%+ rates on volume (and much more on value as higher value added products including 2 way communications and rich media are coming in).

When an industry grows volumes at 20% CAGR, it is big by most yardsticks, particularly when it is already on an extremely large base (50bn/5000Crore+ A2P messages are sent monthly). With continuous evolution and making the messaging richer, 2 way/interactive, value wise the figure could be potentially much higher. Further, in case of NLD messaging - forming the bulk of the volume, India has among the lowest rates in the world and there could be triggers for rate increase by Telco (ILD messaging has seen 3 years of continuous price increases). Basically, the industry has taken off big-time over last 3 years and is continuing its orbit lifting manoeuvres.

How should a market value such heady growths? Few of the key considerations that could go into valuing could be:

-

Ease of Entry - There is literally no barrier to entry in this industry. 100’s of small companies dot the landscape, in addition to few large one. This is a perceived -ve, but practically it means nothing.

-

Ease to Scale - This is where it gets interesting. While entry into the industry, putting together a platform is reasonably doable, getting into the enterprise market is a different ball game altogether. A lot of domain knowledge is required, high levels of customer support, customized reporting requirements and mid level of integration timelines (few months to few quarters) - suddenly change the pitch. Added to this a very low margins business, as far as top end customers are concerned (10-20% gross margin) and suddenly this is not a commodity market anymore (even though SMS is a commodity). There are effective short to medium terms barrier to enter and grow into a large enterprise account. There is significant short to medium term stickiness in large enterprise accounts.

-

Competitiveness - the level of competition is high in this industry and at a base level there is little or no differentiation at product levels (A2P SMS is A2P SMS after all), and given low margins the game is played on a very narrow range. This is perceived to be a very significant risk factor and one cannot wish it away. As a theoretical argument, a price war between players, can take out margins and render players unprofitable, even with huge growth in the industry. Interestingly, however, scaling beyond a point requires resources and capabilities largely beyond much of the mid level players. Hence, while theoretically players can compete crazily, it really does not happen that way. We have seen consolidation happen. Mid size players are typically getting acquired by larger players (more often than not international players wanting to make an entry). And differentiation exist to some extent in service delivery and platform capabilities and not in the end-product per se as players create certain attributes important to an industry or a process (campaign management for example)

-

Scalability - Industry has shown extreme levels of scalability and it can scale further and very rapidly. Movement to cloud based computing, has made scaling a matter of hours and not even days and literally a zero-capex game. Hence, growth is possible almost on demand. An exteme plus point (as with most platform related business).

-

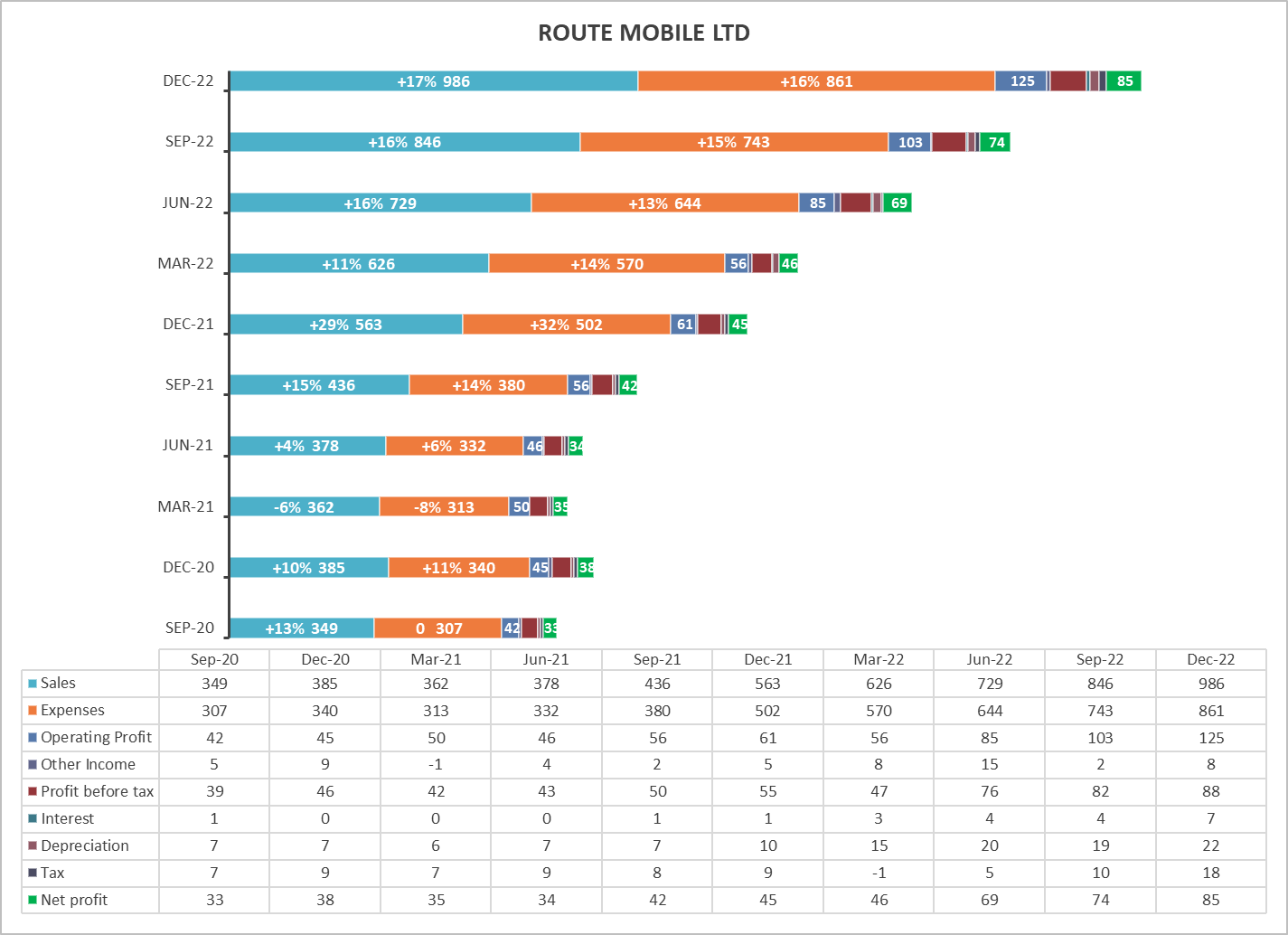

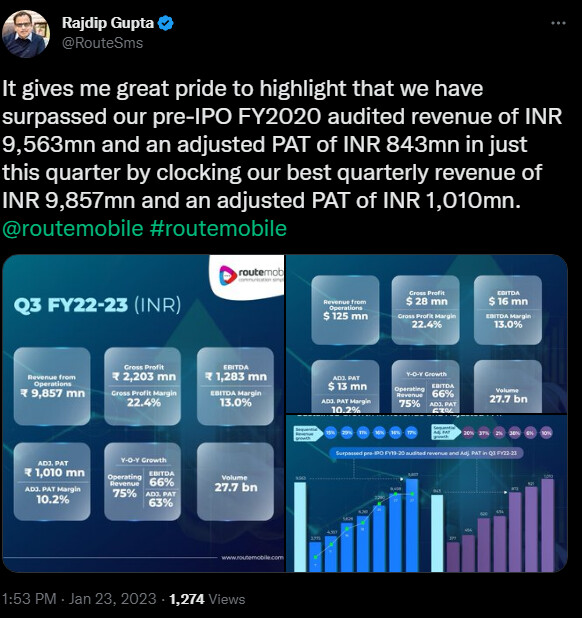

Expansion - these solutions are usable globally with little amount of localization / adaption to regulatory requirement (if any). Therefore, it is both an opportunity an challenge. Challenge as foreign players can come in and they have indeed come in, albeit mostly thru acquisition route - Valuefirst got acquired by Twilio, ACL got acquired by Synch and as on. The result so far is not clear and they have not really eaten away the market. On the other hand it provided opportunity to Indian companies to grow abroad - Route Mobile has done exactly that, while growing its Indian business by leaps and bounds (FY23 is likely to be a 70% top-line growth year for them!!). Given the experience of low cost operating and immense volume - Indian companies should be able play this game well.

Somewhat related to this is the aspect of platform business

-

Legacy platforms - SMSC, Firewalls, hubs etc.

-

New platforms (mostly enabling some regulatory aspect) - DLT, anti sms phishing and some value enhancing platforms - which are yet to be proven. Add to this the conversational AI platforms.

With the platforms in play there is a much higher margin, high stickiness (often multi year deals), but lower value business. It helps improve the business profile as it grows to a certain threshold of the gross margins contribution, helps de-risk the companies from the competitive threat in enterprise business to a decent extent.

All in some plus and some -ve factors. A potential of high growth with likely hood of a stable or growing margins (value addition going up - rich media/interactivity etc), can change the perception of the valuation of the key listed Indian players - Tanla and Route, incidentally both of which are profitable (Against some of the leading global players, who are still in the red) and are delivering good operating cash flows and FCF too.

I believe there are exciting days ahead for this industry and the two listed companies which have followed a divergent strategy.

Tanla - market leader in the Indian Enterprise business, has focused almost exclusively in India and wants to drive value creation thru the platform business and grow organically.

Route - key challenger in the Indian Enterprise business, growing rapidly through acquisitions particularly outside of India. While it does have its platforms, its more a wannabe, an imitator in this area.

Between them, they control nearly half of Indian Enterprise business and many experts believe this industry despite lower barriers to entry, low product differentiation etc, is actually headed for consolidation and between two of these players, they are likely to grow market share. Both these companies are exciting and have their strength areas (and weaknesses) and are likely to grow in tandem or ahead of market.

Invite nuanced discussion, for better understanding of the industry and its trends and development, both India and globally, including regulatory interventions. The Forum has separate threads for both the companies and that should be the right area for company specific discussion.