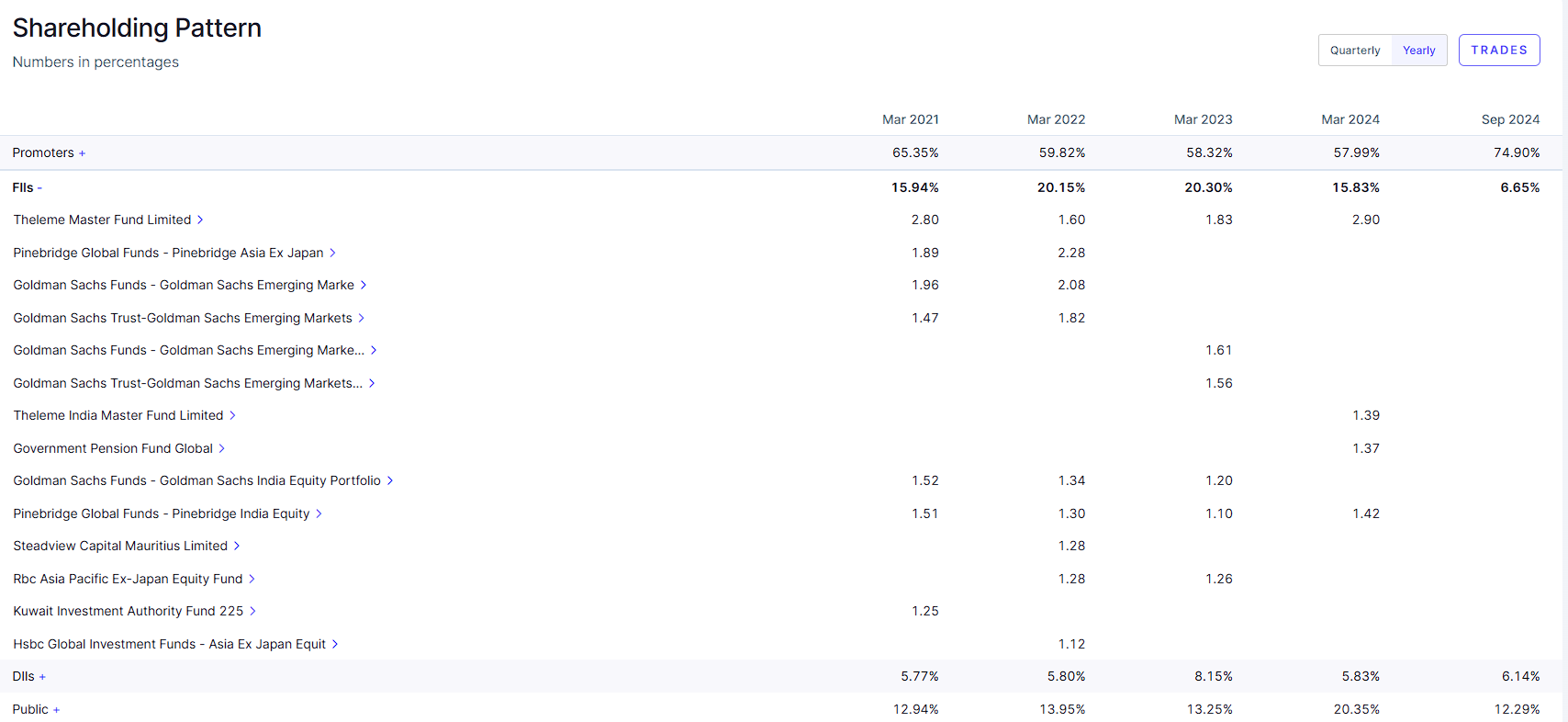

FII’s are the major sellers for this stock; do they see any triggers or are they just moving to better opportunities available in the market?

FII sold and Promoters added.

1 Like

Tailwinds and opportunity in cPaaS sector

3 Likes

The answer may lie in Free Cash flows. The company has generated very little fcf over the past many years inspite of good profits growth. In the long run, markets reward only companies with high FCF

Yes completely aligned with @milan_j_shah about the cashflow issue.

Current FCF Yield is 0.4% and current CFO to EBITA is -17.6%

I believe in this sector, that this is going to be a huge opportunity for this company if done well

1 Like

Significant reduction in PAT YoY .Along with tepid Tanla results,CPAAS sector seems to be having challenges

2 Likes

Hello,

I’ve been invested in onmobile and I came across a new product on their website(no other details found so it’s perhaps yet to be launched)

This sounds like a CPaaS white label aimed at telcos.

I proceeded to read the posts in this forum and saw that the industry has been subject to immense competition + telcos also wanting to do CPaaS

My knowledge of this industry is confined to whatever I read on this forum/outside since yesterday evening when I learned of this new product.

It’s unclear if buzzmo is a CPaaS offering by onmobile or if it’s some sort of white label to be used by telcos

Either way, given the 25 year presence in telco space and integrated with 100+ telcos globally, I wanted to understand if buzzmo possesses a legitimate opportunity in a space that’s increasingly competitive.

Their current president and COO was hired in July 2024 who was ex comviva and seems to be related to the CPaaS industry

Any direction from the forum members regarding the opportunity for onmobile’s product or atleast the details of what the product could be/current industry dynamics would be greatly appreciated.

Thank you

Nothing scaled!!

Its clear seeing numbers of most of the Cpaas players that A2P sms market is declining rapidly and since it forms majority of the revenue of most of them there is no visible growth since last many qtrs. But whats interesting to see is almost all are reporting 20-30% growth in newer forms of communication like whatsapp RCS etc.

RCS seems to be kind of blowing off with 850% yoy growth, though small base.

RCS Interactions in India Skyrocket by 850% in 2024: Infobip Report - The Tribune

RCS: The Next Big Customer Engagement Opportunity in India

Route too is seeing good growth in this newer segement with 20%+ yoy growth with ARR reaching 10% of total revenues. Mgmt does expect it to grw to 25-30% in nxt 3 yrs..

4 Likes

After the BOD change where proximus ceo has become chairman of BOD the stock is falling a lot. Anyone with any thoughts regarding this

Route Mobile

- Revenue down 3.7% YoY but gross margin jumped to 22.9% (from 20.8%). Less volume, better business.

- Debt fully repaid. Sitting on ₹1,389 Cr cash — 42% of market cap.

- Top 10 client concentration improved from 48% to 43%. Customer base broadening.

- FY27 guidance: 5–9% revenue growth, ~12% margin, dividend hiked 50% to ₹16.5/share

Result seems better looking at Valuations

Invested- 3% PF at 500 levels

2 Likes