Channels and Frequency:

End user industry wise

Here comes the major answer for your question in my opinion

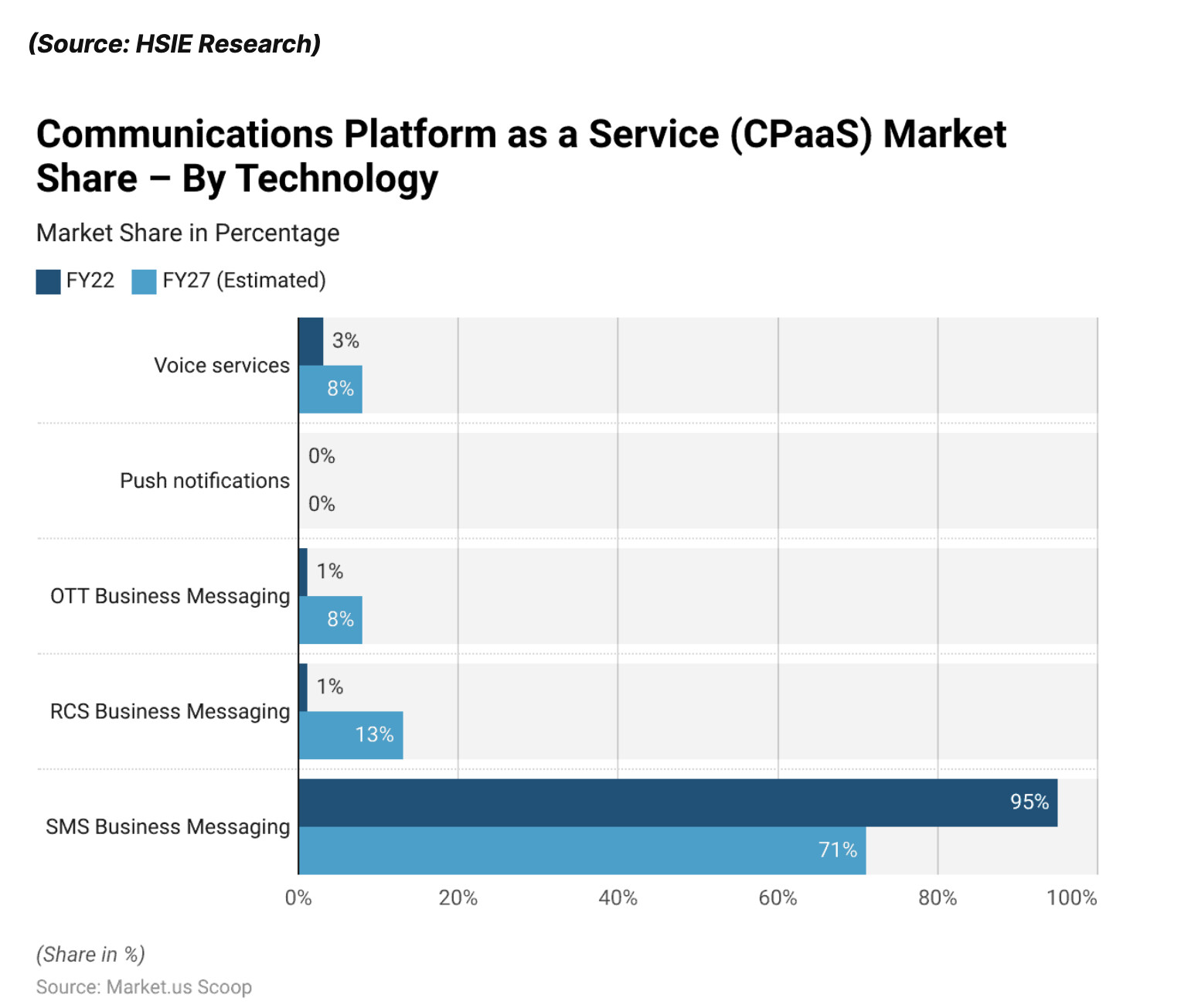

Technology Segregation:

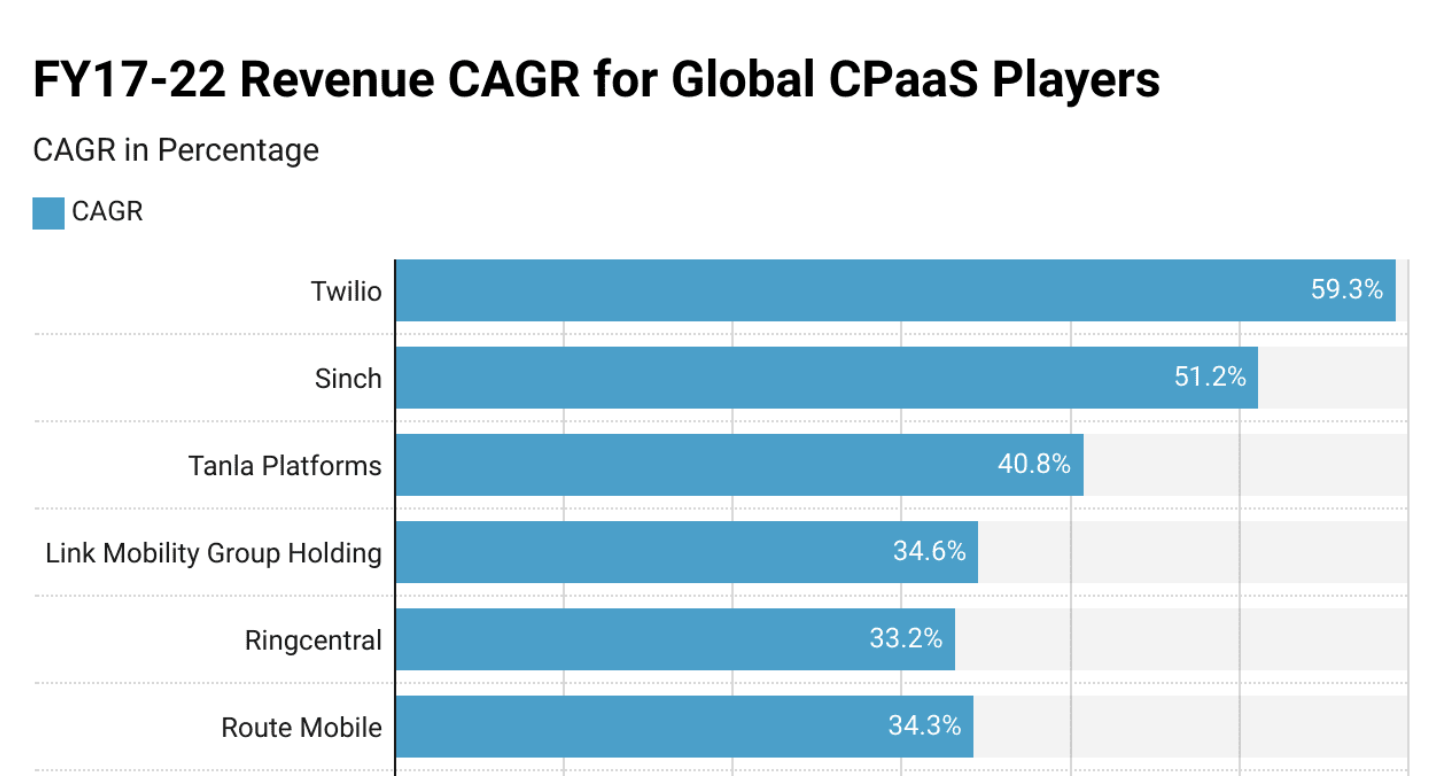

See Tanla and Route Combined made almost 8000crores of revenue which almost a $1 Billion, so that’s inline with the current market size of CPaas in India $0.89B , however the slowdown was attributed to the technology graph, if you see the SMS is on downward trending, both are now Focussing on High growth sections such as OTT, and RCS, however they are bit slow in adoption, tanla has better edge over ROUTE in this facet, they are going through product innovation route

Twilillo the largest global player recent acquired data analytics platform for next lever of growth, Tanla is focusing on in-house products in this catg, ROUTE choose to go via integration route of these tools built by other players.

TLDR;

The growth muted due to SMS trend is declining and the revenue are kinda inline with market size, however the newer segments are not right to win, they need to execute well in other segment such RCS (Google’s largest global RCS (Rich Communication Services) platform partner and has been recognized as Meta’s Growth Partner of the Year for the second consecutive year),

My thoughts:

I think tanla must be working on a propieratory product where communicating it in concall might affect their growth chances or they might struggle with product market fit.

Definitley there seems to competitive intensity in this sector now from smaller player it seems, however both tanla n ROUTE has lot of cash in their books for inorganic growth if needed,

All in all, we should get more clarity in which direct this company gonna in one or 2 quarters but by then if things are positive , we wont be getting it cheap. so in my opinion if there is no issues in terms of corporate governance both Tanla and Route Poised for growth to become multi baggers

Route has been optimistic in their growth outlook and given the new promoters Proximus group give me more confident on them

Tanla refused to share any future outlook, this could be due to launch of new product which they don’t wanna give away before getting first mover advantage since they work closely with TRAI (regulator), However they could be burning cash or genuine concerns on scalability or some other internal issue that may hamper them , i am not sure what it is, but i think the CMP factored those too. Still i can fall further too until they start showcasing for growth for few quarters, (Historically, thy had traded at 8-12 PE for almost an year so i m cautious on position sizing)

Disclaimer: invested in both companies less than 1.5%, as the market is now wobbly, I am looking to increase the allocation heavily to 8-10%(given the tailwinds and cash, debt free) as i build further conviction on the management and clarity on current hesitation by management