1 Like

OFS coming soon

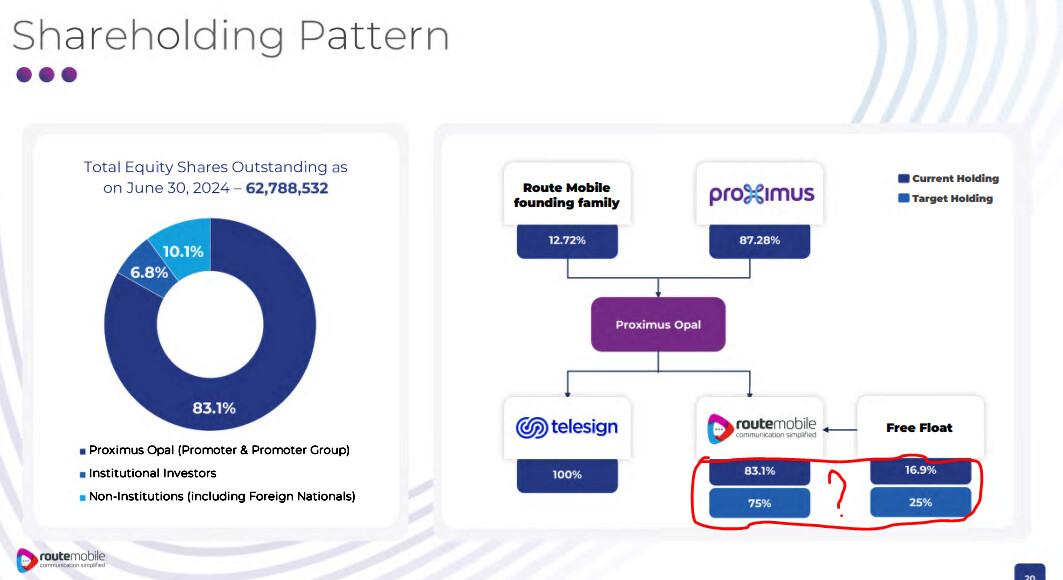

Promoter holding should be reduced to 75% as per regulations

2 Likes

last week, saw some off-loading by promoters and Abakkus is completely out in June qtr. So both DIIs & Promoter free float shares are in market.

Seems for now, limited upside and there’s no traction in the company. CPaaS as a space is here to grow, esp with WhatsApp business & Google’s RCS getting into more thick of things while businesses are looking to find new engaging ways to keep a connect with their customers and also be instantly available, without a human need. Recently, Route also got Metro ticket booking contract and has been expanding the services tie-ups. Airtel already shared the intent to get into CPaaS and that’s off course has very great synergy to them.

But for now, the upside seems limited seeing Route’s valuations, more free float & offloading from promoters to happen (i expect they will complete by Mar’25 or least come to 77-78%). Tanla is there on lower deck of valuations but with Proximus buy-out, the leverage exists more with Route.

Coming months to see how this pans out and if looking to buy into a CPaaS growth story, Route can be considered as it should give good window for slow accumulation, fair valuations wrt growth runway and a strong promoter group with global reach & associations with big firms.

5 Likes

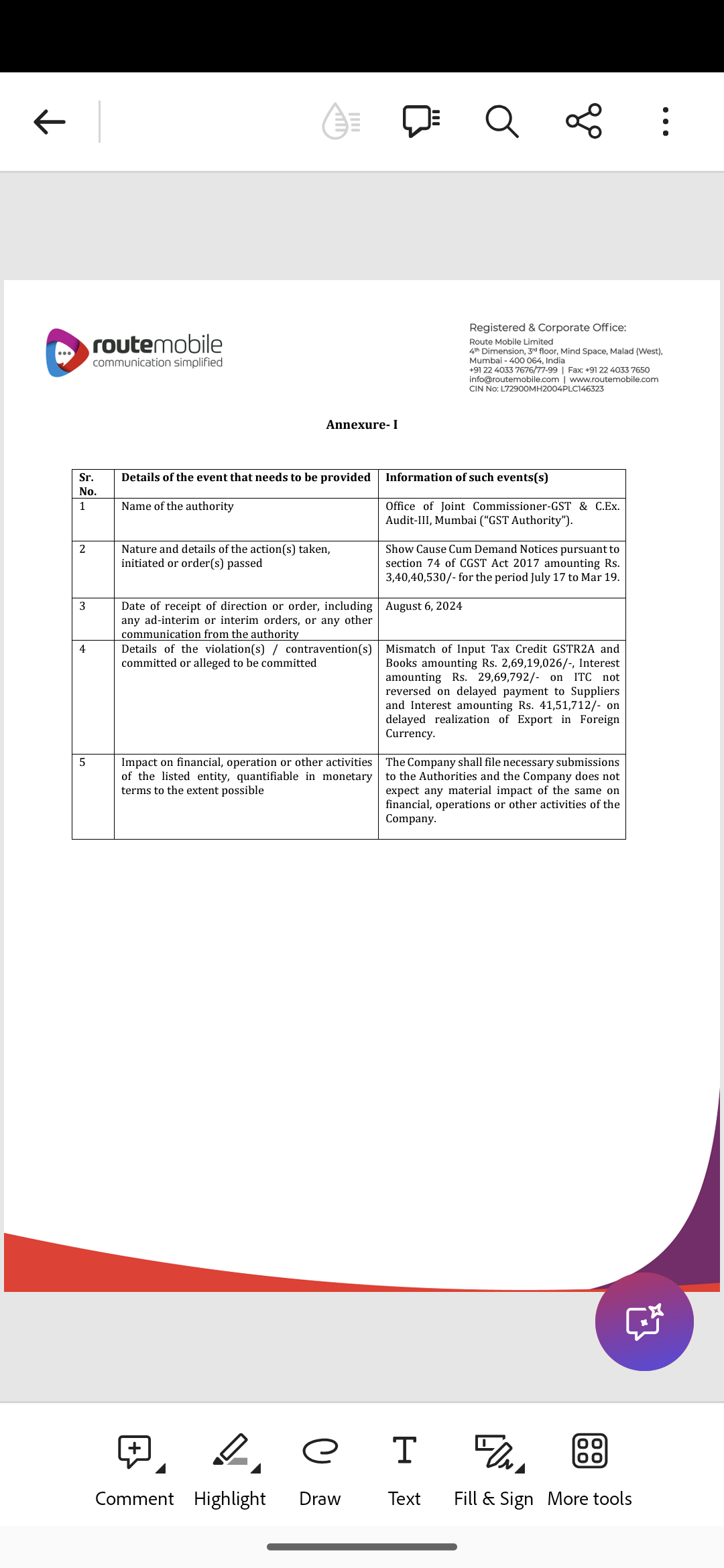

Route Mobile faces significant GST tax demand.

The company has received a notice from the GST authorities demanding a hefty sum of Rs. 34 crore for the period July 2017 to March 2019. The tax department claims discrepancies between the company’s GST returns and its financial records, along with penalties for delayed payments to suppliers and export-related issues.

I just gone through the Q1FY25 Concall of Route Mobile.

- New promoters have came in.

- Expecting revenue growth of 18-22% growth in FY25

- Expecting margin expansion in coming years

- Aiming to achieve 8300cr sales in next 2-3 years (tha’ts 26% CAGR growth)

My simple take(no complex calculations) -

CMP - 1530

Current Sales 4000cr roughly

PAT - 390cr, Net Margins at 9.8%

We can expect 8300cr Sales by FY27 with Margin Expansion of 3%

then FY27 PAT will be of 1080cr

ATH is at 2223 with P/E of 91

Current P/E - 27.7

If management do walk the talk then we can see P/E expansion + Margin Expansion + PAT growth

We can see these levels in 3 years -

- 4765 at current P/E

- 6025 at 35 P/E

- 6880 at 40 P/E

In last 5 year, sales is almost 5x and PAT is 7x.

Note - I have read 3 concalls of mid cap IT companies but Route looks cheapest. Another 2 co has also given guidance for sales growth of 20% but they are already trading of 40 times of earnings.

I may be wrong in my analysis.

Disc- Invested with proper allocation and risk management.

5 Likes

Please have a look at the Free Cash flows of this company over the last many years. They are nowhere near their PAT levels. For all top performing stocks worldwide (outside new age companies), the common feature has been consistent growth in FCF. This is the reason that the stock is not moving in spite of big CAGR in profits etc

2 Likes

yes, this may be the reason.

i want to add one more point.

when company got listed in 2020. It got listed at 66 times of earnings and within 6 months P/E was around 130.

As per my analysis, Any company which is growing at 40-45% growth rate should be given 60 times to earning in bull case and in base case 50 times is good. But route is at 130 times of earnings.

So, P/E contraction started.

1 Like

Management has guided this in Q1FY25 ‘The free cash generation for the business should improve

meaningfully during the year and we expect the cash conversion from EBITDA to be within

the 50% to 75% band’

2 Likes

Not a good idea to compare it with other IT companies. Its CPaaS, competitive sector. I feel there’s always the threat of telcos stepping up their capabilities and offering in-house services. Margin erosion clearly indicates some form of pricing pressure.

1 Like

Hey, I’m not a IT guy. Honestly I don’t understand CPaaS much. I bet on this stock with purely on management guidance and I’m closely monitoring that Is management doing walk the talk or not.

I have allocated 4.3% of my portfolio to Route and will increase till 8% if management achieve 20% yoy sales growth in FY25.

That’s my strategy in Route.

3 Likes

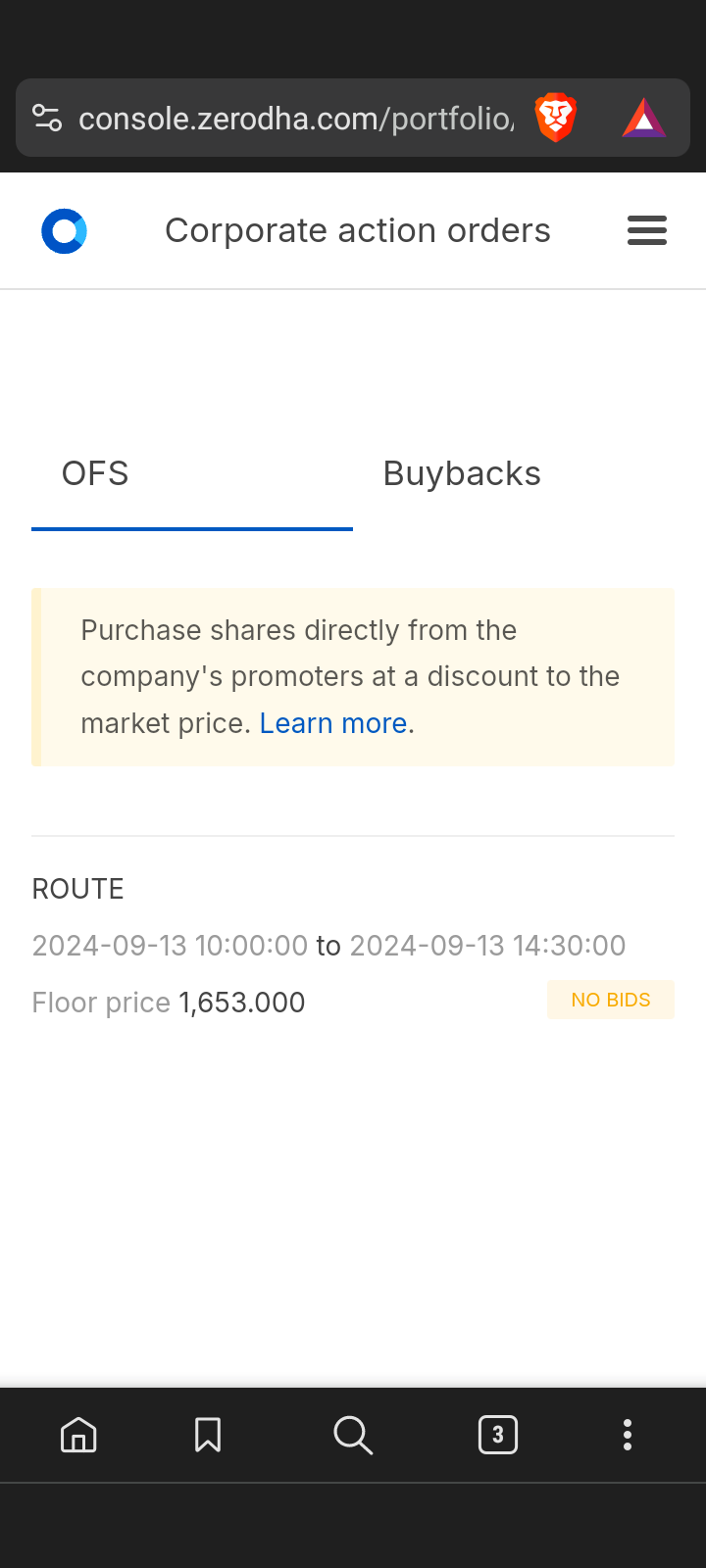

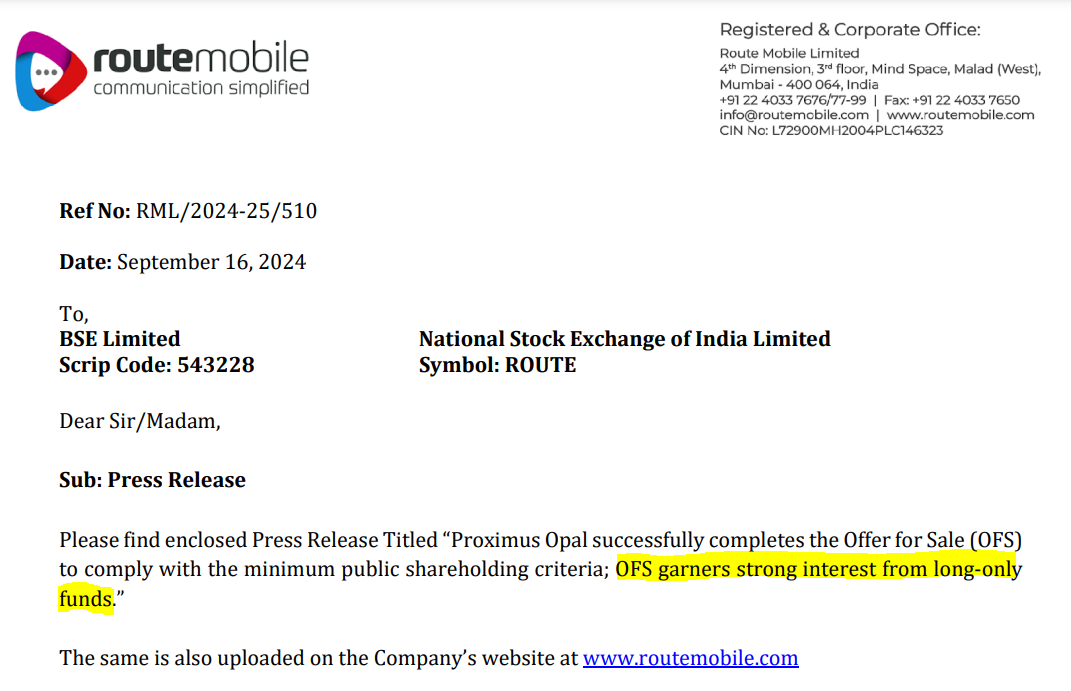

And here it is, the much awaited OFS on Sept 13 for Retail investors.

The floor price for the Offer shall be INR 1,635 per Equity Share

2 Likes

How to apply for OFS as share holder

CMP is 1700. OFS is 1635. Discount is less than 4%. Why would anyone subscribe for this OFS ?

I was just browsing this company. Any reason it has not performed in the last 2-3 years whereas their fundamentals have improve during the same time frame?

company went 4x post listing, it is okay to cool down and then rise again. Their profit is more than doubled from the time it was at ATH last time. Company will create value again for its stakeholder. We just need to hold for good returns ![]()

2 Likes

co has listed at 60-70 P/E and pe has went to 130 in not time.

co’s pat is growing at 30-40% p.a. so 130 pe is not justified so price remains constant for 2-3 years and when earnings came, P/E contracts and its at 28 now

For me, Route mobile should have 35-40 P/E because co. is giving 30% growth guidance for next 3 years and new promoters has came.

Disclaimer - Invested and biased. Not a rec. to buy or sell

3 Likes

Hello

Route isnt an IT company … it uses technology and provides services more on a responsibility basis and have metrics which add value to customer …

So customers will tend to rely on them and will continue to do business . There is also technology disruption… which is very imprtant … So companies who do not keep up with technology disruption ( which is difficult) will fall by the wayside…

Malolan

2 Likes