I will provide my perspective of investing in this sector and choosing KNR:

1/ I believe that to reach the target of $5T economy government has to spend money on building infrastructure. Therefore, even though there is huge debt on NHAI, government will find a way to keep the spending going. This thesis makes this sector attractive for me for investment. As there is big overhang of NHAI debt, so I m limiting my allocation to 5% of portfolio

2/ Now coming to choosing the companies in the infrastructure space, I prefer a company with strong balance sheet (lower D/E) so that it can withstand the tough environment/cycle and also able to capture the opportunities when other players are struggling. I found KNR to be having the best B/S hence invested in the company.

Disclosure: I am not an expert. This is not a recommendation. I am invested in KNR

Simplex Infrastructures Ltd. had bagged two construction projects of Bangalore Metro Rail (BMRCL) worth a total of Rs. 877 crores. The progress made by the Company is very poor compared to other contaractors including its competitor ITD Cementation.

Big infrastructure spending push announced by Govt (Link)

So my thesis that government has to spend on infrastructure to become 5 trillion GDP is panning out but execution and fund allocation is the key as govt finances are pretty much stretched.

I wonder whats the source of funds… Tax collections so far indicates that there will be fiscal stress… Requesting boarders please provide some inputs in this regard.

Discl: Not invested in any road construction players… but following the sector closely for investment.

informed exchanges that it has bagged a highway project worth Rs 522 crore in Haryana from the National Highways Authority of India

Earlier this week, HDFC Securities had recommended a buy rating on the company with a target price of Rs 441 after attending the company’s analysts meet.

I don’t track road sectors, however found this report by HDFC securities thought it might be of help to the forum - can any senior members share some light on the below report?

Execution improvement to be seen by 2QFY21-end. Performance of the company

remained impacted during 1QFY21 too on labor unavailability. Labor availability has

improved to 50-60% for SEL from June onwards. From a current run-rate of daily

execution of Rs45 mn, it expects to improve it to Rs100 mn by September on improving

pace of work on Mumbai-Nagpur expressway, Kim-Ankleshwar and Gadag Hanalli

projects.

Order inflow scenario is gradually improving. NHAI has called for bids worth Rs177

bn for 24 EPC projects and Rs280 bn for 27 HAM projects to be submitted by August

2020. Bids for metro projects worth Rs20 bn are also expected to be finalized in 2-3

months. Sadbhav Engineering has submitted bids worth Rs34 bn for road EPC and Rs4.7

bn for metro projects in July, 2020. The company expects an order inflow of Rs30-40 bn

in FY2021 across roads and other segments.

Receivables remained high during FY2020. Receivables jumped to Rs19.3 bn on

delays in release of payments for four projects – Kim Ankleshwar (Rs1.4 bn), Jodhpur ring

road (Rs2.5 bn), and two packages of Rampur-Kathgodam (Rs1 bn). However, since these

are for certified works, the company expects the payment to come through in next 2-3

months.

Conciliation process is on for Rohtak Panipat project. The company had already

initiated the process of conciliation for Rohtak Panipat project and has filed for claims

worth Rs11 bn for the loss of revenues owing to alternate stretch, erosion in equity

investments and loss funding done by the parent for SPV. It expects a positive resolution

on the same during FY2021. It has also initiated loan refinancing discussion with banks

for Rohtak Hisar project. For both projects, loss funding during FY2020 was Rs750 mn

and is expected to come down to Rs600 mn in FY2021. Till any outcome from NHAI, it

expects cash flows from Maharashtra border check post to take care of interest and debt

repayment for both the projects. Maharashtra border check post had revenues of nearly

Rs22 bn during FY2020 and commissioning of additional check posts by October and toll

revision of 18% from FY2022 is expected to improve its cash flows further. Combined

debt of three SPVs together is Rs30 bn. We also expect further support from dividend

income from InVIT units to take care of loss funding till the NHAI outcome gets finalized.

Road assets are 10000+ 2000 (recently acquired)= 12000 cr.

Amaravati project completion aimed to have in this calendar year.

Anta simaria in Bihari, bridge project, insignificant progress in Q2 due to rising ganga levels.

Tamilnadu project, 5 oct as appointed with reduced scope, land acquisition will be finished (80% on Jan 20121). Booking revenues after Q4, preparation started, mobilized. taking over land.

Water infra: Bid for UP in 2000 cr for water project in Nal se Jal theme. Other states are also considering. In this FY additional bid of 5000cr is planned.

Oil & gas: 4 relevant blocks in different situation with partners. Total investment 500cr. 250cr written off. 100cr. to be invested. It will be peak for investment. Long gestation cycle. Once results are proven, selling it to long term player. FY22 will have clarity. Start to engage with players. Intend to exit this business line .

Current bids by NHAI: 58 bids, 58000 cr. HAM+ EPC. Bid only for which allows for their thresold returns.

Company will continue to pursue asset light model.

Company will be able to hold revenue and EBIDTA margin.

Asset monetization: Portfolio approach.

Panipat mubara chowk: PCOD to be achieved by this FY. If traffic will be measured for 3 years and if it falls, contractual provision to extend terms.

Returns for acquired project will be higher than HAM and water project will be have same returns as HAM though it is EPC bid.

Passenger train operation: could be stable business line, as it may give first movers advantage.

15% revenue growth guidance.

current collect for haryana section for tolling is 55 lac per day.

Order inflow expectation is 3000 cr. this financial year.

Do not reduce returns, change models to achieve that returns.

Conference call takeaways

COVID 19 Impact – Labour is back to pre-COVID levels. However execution is expected

to reach 100% levels (of pre-covid) only in Q4.

Margins: The company took provisions to capture the cost/time overruns it has faced,

on many of its projects, due to the pandemic – which it feels will not be reimbursed by

the client – leading to loss at EBITDA level. While some of these provisions might be

reversed later, we see little chances of that happening.

Interestingly, none of ITDC’s peers have taken any such – despite working on the same

projects, with the same clients, under the same terms and conditions.

Net Debt at Rs 3.9bn has increased significantly in this quarter due to delay in receipt of

mobilization advances on few projects, execution on same started.

Status on various projects –

o Mumbai Metro – 86% executed, tunneling to be completed by Dec-20.

o Kolkata metro – UG Phase 1 tunneling completed, work on elevated just started.

o Elevated metro Bangalore/Nagpur – 87%/90% completed respectively

o Bangalore UG metro – execution to pick up from Jan-21

o Myanmar project – construction to start from Feb-21

ITDC sees a healthy pipeline of Rs 200bn of projects – Rs100bn/Rs60bn/Rs30bn in

metro/marine/industrial segments. It is also keen on track laying projects for HSR.

Conference call takeaways

Covid-19 update: Currently, labour availability is back to pre-COVID levels and execution

stands at 90-100% of pre-covid levels, across all projects.

Payments: The Company does not see any liquidity problems in road sector, as most govt

bodies (state and center) along with NHAI are making timely payment. However power T&D

projects in Jharkhand & Bihar are witnessing delay in payments, leading to higher debtors.

Guidance: The management expects to achieve FY20 topline in FY21, and strong 15-20%

growth in FY22. Margins are expected to remain in 12-13% range. It expects additional

working capital loans of Rs 2.5bn by FY21 end. It also guided for additional Rs 40bn order

inflows in FY21, including 1/2 HAM projects in H2FY21.

Q1 & Q2FY21 margins were exceptionally high due to contingency provision being released

for projects recently completed. (Kharar Ludhiana, Anandapuram)

The equity requirement pending for 6 HAM projects is Rs 3.7bn – Rs2.1bn/Rs1.6bn to be

invested in FY21/FY22 respectively. The company has already invested Rs 6.7bn.

SBI-McQ exit: Talks are on advance stages with potential investors for stake sale. The

management expects few binding offers by Dec-20.

FC for Tumkur Shivamogga Pkg 3/4 is expected in Q3 and AD in Q4FY21. Bihar road EPC

projects are expected to receive AD in this month itself. The company received CoD for the

Anandapuram project, and the first annuity for the Kharar project in Sep-20.

The company is actively exploring opportunities in the water segment (it had bid for recent

projects in UP, but wasn’t successful in winning any) – and also power/railways segments

KEC International gets new orders worth Rs 1438 crore KEC International has been awarded the work orders worth Rs 1438cr across its various businesses. Company has secured orders of Rs 475cr in the urban infra/Rail segments in India. Company received orders worth Rs 383cr in Civil segment for infra works from private players in the Chemical, Cement & Residential segments and a Government order in the Water Pipeline segment in India. Transmission and Distribution business has got orders of Rs 362cr in Middle East and Americas. Cables segment has received orders worth Rs 218cr in India.

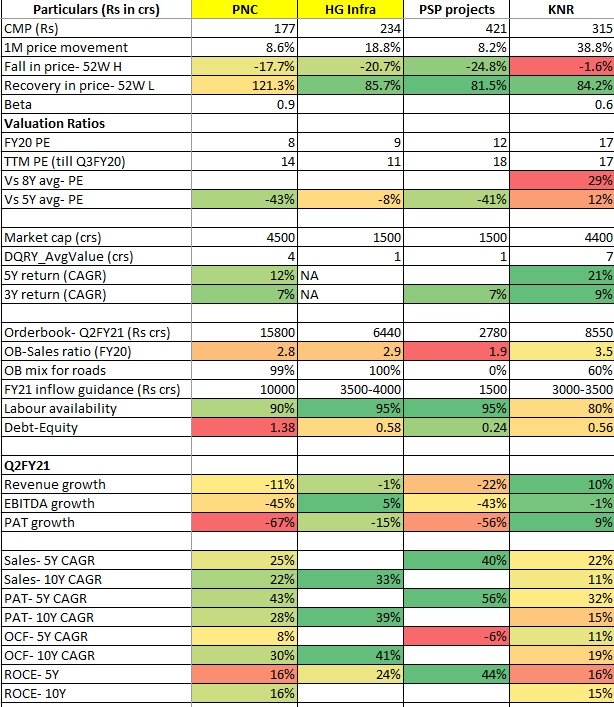

Here is a comparison I made between these 4 players. We can build on this.

Also, would like to know why HG is trading at a discount to KNR (or KNR is trading at a premium to HG infra)? Will HG might move towards KNR in terms of valuation if it keeps delivering going forward?

Ircon International gets Rs. 900 crore HAM project from NHAI

Ircon International (IRCON) has been awarded the work of upgradation of Gurgaon - Pataudi - Rewari section of NH352W in Haryana on Hybrid Annuity Mode (HAM) valuing Rs.900 Crore on competitive bidding basis by National Highways Authority of India (NHAI). This work will be undertaken & executed by a Special Purpose Vehicle (“Concessionaire” as a limited liability company) which shall be incorporated by IRCON as its Wholly-Owned SubsidiaryCompany.

Revenues were impacted due to Mubakara chowk - Panipat project no progress due to Farmer agitation. Company already communicated to NHAI for extension for time.

Amaravati land is available but waiting for clearance from forest department to enter for work.

Order inflows of Rs. 11,000 mn in EPC Water segment

4.Received PCOD of Gagalheri-Saharanpur-Yamunanagar (GSY)

5.Received Appointed date of Sattanathapuram-Nagapattinam

Invoked Force Majeure to ensure interest of the company is protected

One of few companies in infra sector with – LT credit rating ‘AA-‘

Qualified for 3 big senitation projects of mumbai for value between 1600 cr to 3000 cr. Each player will get only one project. Players are Shapoorji Paloonji, L & T and Adani.

Company will not purse revenue growth only without profitability.

Follow up order possible from UP government for " Jal Se Nal" scheme, they get order for 1100 cr (74% Welspun Enterprises and 26% Kaveri Infraprojects Ltd.) They get order for approx 1100 villages. possibility of 1700 villages if UP government decided. To be executed in next 21-24 months.

Oil and gas no revenues till next 3 years. will sell assets if suitable bidders arise.

Order book of approx 5500 cr give enough visibility for next 2-3 years.

One participant grill management about rosy outlook in 2018. Management comment yes they did not achieve and will not give any guidance further.

All in all company is facing head wind but valuation are rock bottom, positive change in road/water sector or large deal can turn stock prices upwards.

You can hear Concall

Disclosure: Invested

In Budget 2021, Infra get very good announcements. Welspun Enterprises can benefit from both verticals road and water. Water:

The Jal Jeevan Mission [Urban], will be launched. It aims at universal water supply in all 4,378 Urban Local Bodies with 2.86 crore household tap connections, as well as liquid waste management in 500 AMRUT cities,” she said. Newspaper Article

This mission would be implemented over five years with an expenditure of ₹2.87 lakh crore.

Road

Finance Minister pledged that the Centre will award national highway projects to the tune of 8,500 km by March 2022 and complete an additional 11,000 km of National Highway Corridor.

Decent nos. By KNR Constructions, both qoq and yoy. Good Scope of both topline growth & bottomline growth ahead boosted by sectoral tailwinds and policy

Recent run up in road construction companies indicate good times for this sector. Looks like smart investors loading up before orders flow in.

Though DBL always have most of orders, I have invested in Welspun Enterprises because of only one factor, they continue pursuing asset light model, means they do not buy equipment machinery etc.

They repeatedly told on previous concalls that they will not bid if profitability margins are not protected. That is why they do not have any new order since last 18 months. They have one harmonies substitution for mubaraka chowk panipat road asset. In addition they get their maiden water project, so another vertical is to add revenue, available at cheap valuation.

Sector tail winds are there, Let us see how story play out.

Competition is intense in sector.

Disclosure: Invested in Welspun Enterprise, Not invested in DBL.