Hello everyone

I have been following the major road construction players for some time since Project Bharatmala was announced last year. As this project is for 5 years duration till 2022, I think this can be a major investment theme going forward.

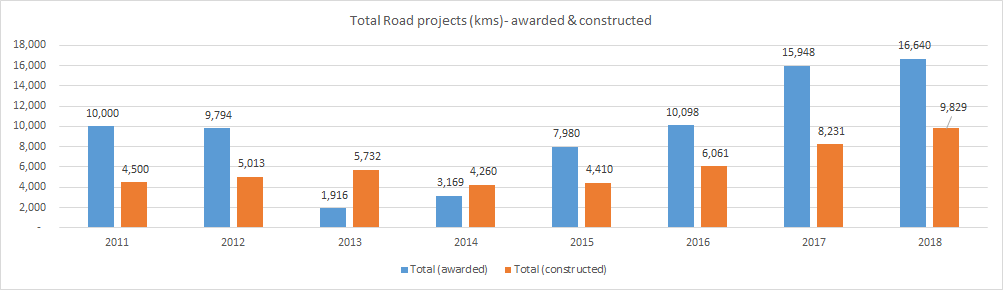

I have done some work on the performance of 6 major players in this space over the past 7 years i.e. from FY 2011 till FY 2017. I have chosen this period because it will cover the entire cycle of construction activity - 2011 and 2012 which can be considered good years in terms of road projects awarded and completed and then 2013 and 2014 which were pretty slow, followed by an uptick in activity again. Following chart will help visualize (data taken from MoRTH & NHAI annual reports.)

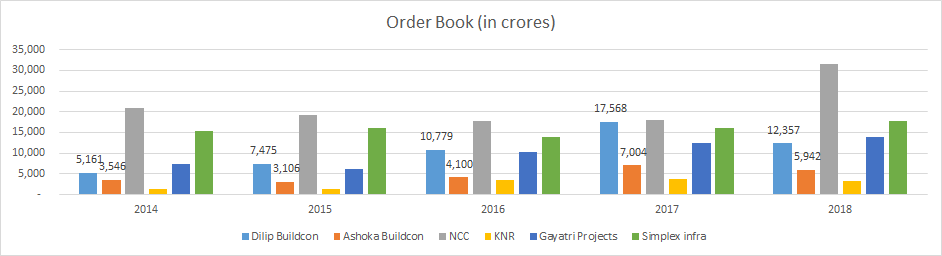

Now the fortune of road construction players is mainly dependent on this contracts awarding and construction activity. See chart below for last 5 year order books of these 6 players (data compiled from ARs)

With the targets set forth in Bharatmala Pariyojana - 35000 Kms of roads & highways across the country with an estimated expenditure of Rs. 5.35 trillion in Phase 1 (with more to come) - I am sure the good players in this space can make a hefty bounty!

Companies forming a part of my current research focus are:

- Dilip Buildcon - DBL

- NCC

- Ashoka Buildcon - ABL

- KNR Constructions - KNR

- Gayatri Projects - GPL

- Simplex Infra - SIL

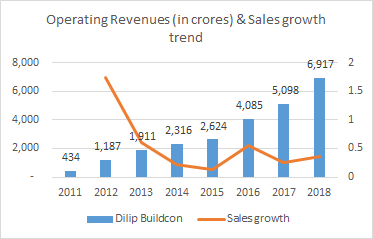

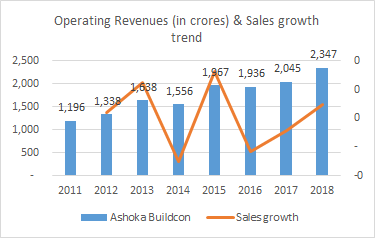

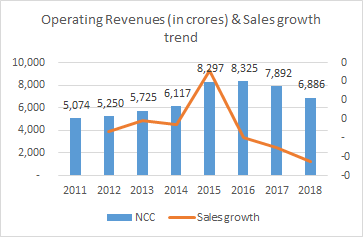

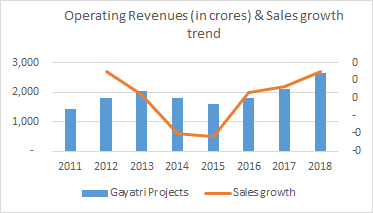

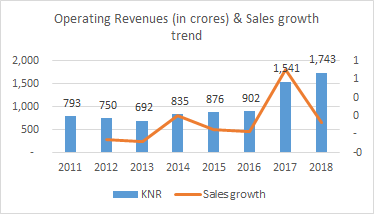

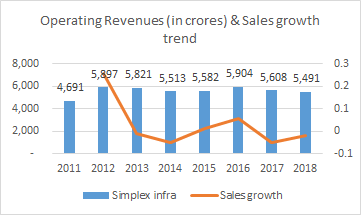

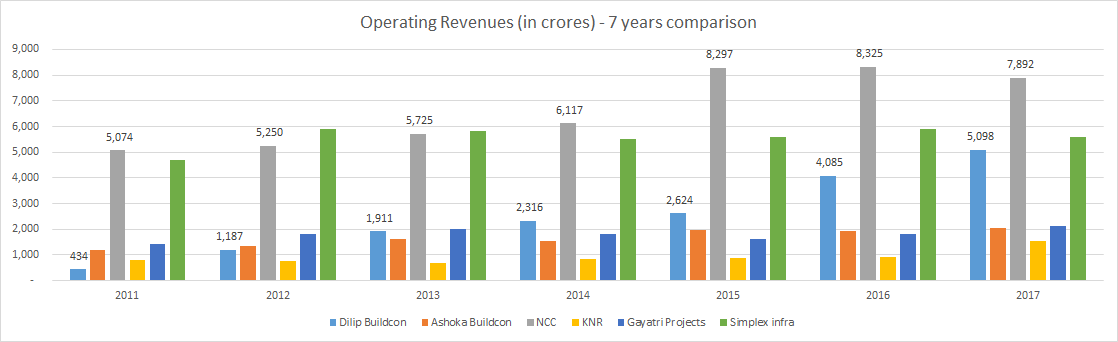

Key Parameter 1 : Operating Revenues - Q4FY18 has been estimated on the basis of 3 Quarter results.

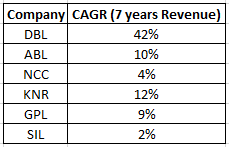

Some observations on the Operating Revenues over the last 7 years:

- DBL has grown topline at a very high growth rate.

- NCC - Bad topline growth even though it has the biggest order book of all the players.

- KNR is second. Its topline is flat in average years but has shown good growth in years when order activity has picked up.

- SIL - Relatively flat topline. Even declining in good years of 2017 and 2018.

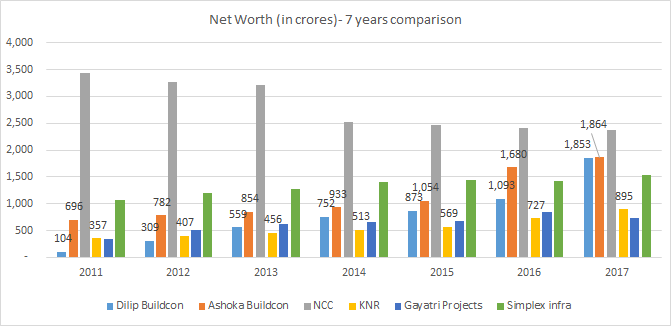

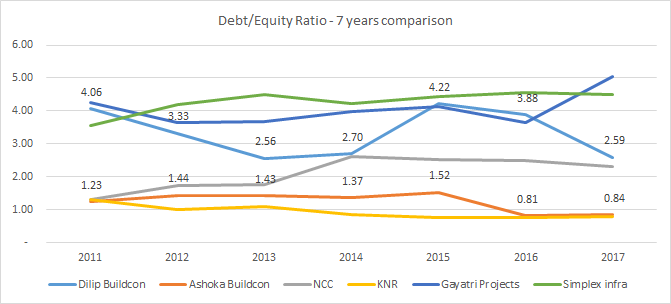

Key Parameter 2 : Networth & Debt/Equity (Here Debt/Equity takes into account Current + Non-Current Liabilities and Networth is shareholders’ funds - Capital + Reserves & Surplus)

Some observations on the above:

-

KNR and ABL have low debt compared to other four.

-

DBL has consistently reduced its debt/equity ratio while also growing the topline and bottomline.

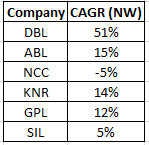

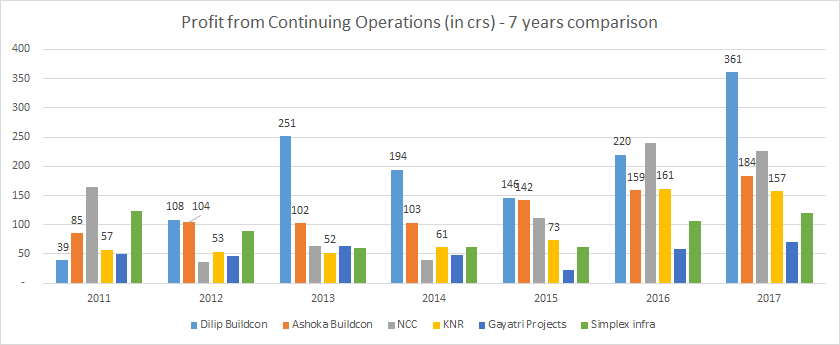

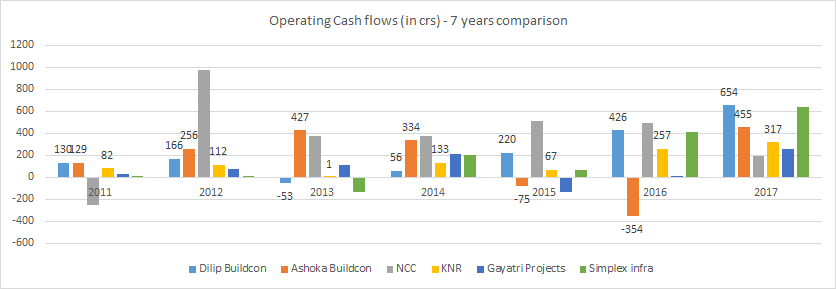

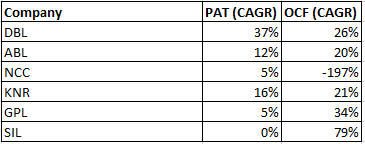

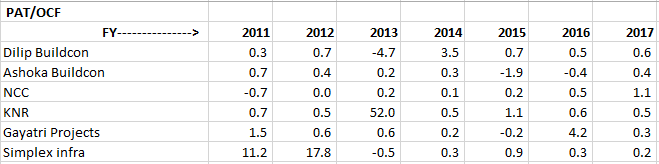

Key Parameter 3 : PAT and Operating Cash flow

Some observations on PAT and OCF trends:

-

KNR is the only company which has had positive operating cash flows all throughout the 7 years.

-

DBL emerges as the quickest in terms of PAT CAGR growth.

-

PAT/OCF - The closer this ratio is to 1, the better it is since it means that there is no major difference between PAT and OCF. But in the road construction sector, payments can get stuck with the govt for multiple quarters before flowing to cash flow via reduction in receivables. So wherever you see a negative PAT/OCF, it could be because of stuck payments as a result of which you can see a negative PAT/OCF in one period buy a bump in PAT/OCF in the succeeding period. With the onset of Hybrid Annuity model, cash flow position of all the players should benefit since 40% payment is made by the govt upfront.

I will be uploading some key profitability metrics, geographic presence of each player, type of projects and valuations in this post itself soon. That will enable more informed decision making.

IMO, the best analysis for investment purpose should be kept simple to understand. Past performance can in no way guarantee future performance. But it can certainly give some confidence to take investment decisions. All of the above companies are well established businesses with a strong track record in execution.

KNR is a bit conservative in bidding while Dilip Buildcon is the most aggressive which is apparent from their Order book and PAT growth as well. ABL sits somewhere in the middle of these 2. On the flip side, DBL has high, albeit reducing, debt.

I am not too keen on NCC and SIL because of poor topline growth and GPL because of very high debt. (others may disagree on the basis of separate parameters)

Key risks to this theme:

- Govt isn’t able to find the money for investment with oil price (and subsidy burden) rising and populist pressures mounting in an election year.

- Projects get delayed due to land acquisition issues.

- NDA govt is not re-elected in 2019 and the new govt stalls the program.

- Cyclicality of business.

Some important links:

- What is Bharatmala project: All you need to know about Modi govt's massive infrastructure push through ambitious roadways plan | Business News – India TV

- 2018-19 target: Centre aims to build highways at 45 km per day | The Financial Express

- Highway construction grew 20 pct in 2017-18 | The Financial Express

I invite esteemed VP members to share their opinion on the potential of road construction players over the coming 5 years.

Disclosure: Invested in KNR and looking to enter ABL with a 5 year outlook. All financial data taken from Moneycontrol