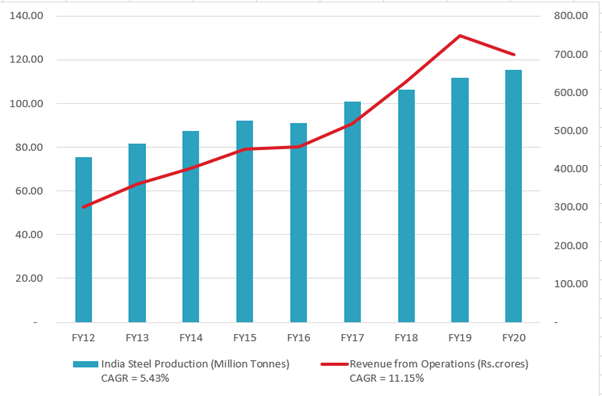

Between FY12 and FY20, steel production in India increased at a CAGR of 5.43% p.a., from 75.70 MT in FY12 to 115.53 MT in FY20. In the same period, Orient Refractories’ revenue from operations increased from Rs.300 crores to Rs.700 crores, a CAGR of 11.15% p.a. By contrast, competitor Vesuvius India grew at 6.33% CAGR in the same period, and IFGL Refractories’ India operations grew 8.67% (from FY17-20, for which numbers are available). ORL thus has grown at double the rate of India’s steel industry, and increased its market share by a significant margin. In 2019, ORL’s market share was estimated at 20%.

When revenues grew 11%, PAT increased faster at 14% and cash flows increased even faster at around 15%. Dividends tripled during this period.

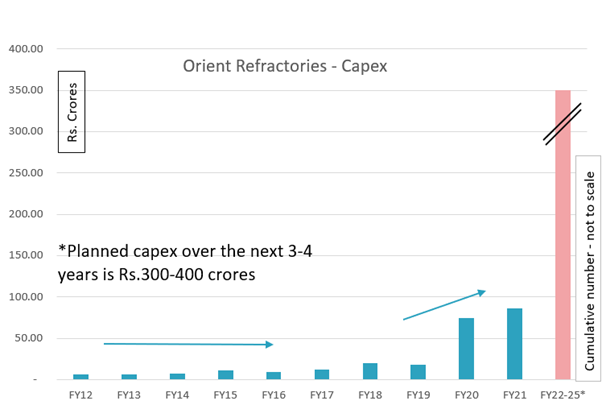

More importantly, all this growth came with minimal capex. Between FY11 and FY19, ORL’s cumulative capex added up to just Rs.90 crores in 9 years. This is much lower than the capex incurred by Vesuvius and IFGL, both of whom have delivered lower growth with higher capex. At the start of FY20, ORL’s Gross Block stood at Rs.189 crore.

And ever since the merger with group companies was announced, ORL has stepped on the accelerator even further.

In FY20, ORL did a capex of Rs.74 crores. It acquired assets of Manishri Refractories for Rs.44 crore and announced Manishri’s capacity would be increased from 10,000 tons to 18,000 tons. Manishri produces magnesia carbon bricks for which there is no other Indian source and is entirely imported. ORL also acquired Intermetal for Rs.10 crores, a small company but which has 300 customers in the steel industry.

In FY21, the merger with group companies finally cleared all hurdles and got consummated. The merged entity RHI Magnesita India (RHIM) is double by revenues, has 75% higher operating profits and 57% higher PAT. An equity dilution to the extent of 34% has also taken place.

For RHIM, the Balance Sheet shows capex of Rs.85 crore for FY21. The management says going ahead, a further capex of Rs.300-400 crore is planned in the next 3-4 years. Even by standards of the merged entity’s size, this capex plan is quite large.

Post the merger, the company’s addressable target market has expanded beyond steel to other sectors like cement, glass, non-ferrous metals etc. An R&D Center is coming up in Rajasthan which will be integrated with the RHI’s global R&D. Some high end products are being introduced in the Indian market which were not produced here until now.

In a recent TV interview in June, the management made several promising points.

By chance or by design, all this is happening at a time when the steel, cement and other consuming sectors are seeing a sharp upswing. Strong growth, far better than what past trends indicate can be expected going ahead.

(Disc.: Invested)