The Company has completed the process of acquisition of above said assets / plant & machinery on 26 September 2019.The same will help the Company in diversification of its existing product line by adding new products like Magnesia Carbon Bricks etc.

Orient reportedly paid around Rs.40-45 crore for the Manishri acquisition. A recycling plant will be set up and production will begin in November this year. Interestingly, magnesia carbon bricks have no domestic source and are currently entirely imported.

Besides this, Orient acquired Intermetal for Rs.10.5 crore earlier this year. Here too, the target company specializes in import substitution and has blue chip clientele. Intermetal has a manufacturing facility on a 4-acre land in Wada and an office in Kandivali. It has 35% PBT margins and Orient got a good deal. Apparently, the business was sold as the owner was getting old and his only son working in the I.T. sector had no interest in continuing with a boring old economy business like metallurgy.

The interim order from NCLT for group company mergers is expected any moment now and the merger process will be complete by November.

Steel sector is currently going through a down turn, but low energy costs continue to support production. This is especially good news for small steel mills whose production is very sensitive to energy costs. Orient is a large player in the small steel mill segment with more than 600 clients and a market share upwards of 50%. This is also a very profitable segment since small mills pay with very short credit cycles or sometimes even in advance compared to large steel mills.

Overall, pessimism seems to be overdone for the Orient stock. The company is consolidating & positioning itself well in the current downturn.

(Disc: Invested)

10 Likes

Cuttack plant was acquired by RHIM in August, 2019 from Manishri Refractories and Ceramics Pvt. Ltd. (Manishri). “The public listed Indian subsidiary of RHIM, Orient Refractories Ltd., entered into an Asset Purchase Agreement with Manishri to purchase the plant along with the land, machines and equipment at a value of Rs 45 crore. Commercial production at the plant is expected to start soon after completion of the trials,” Borgas added.

1 Like

Interview of Mr.Parmod Sagar:

3 Likes

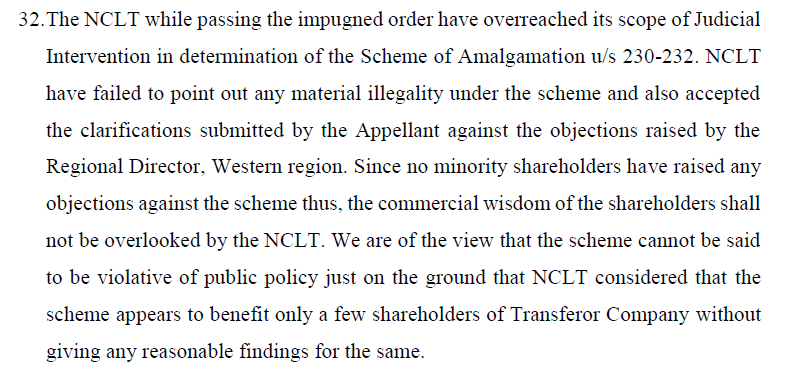

The judge has taken the market value of Orient shares and face value of the other two unlisted company shares and held that the valuation ratio is unfair & unreasonable !

I think it is a settled principle that valuation is a complex and technical exercise, and judges are not supposed to get into it, especially when there are no objections filed by any aggrieved persons for the merger.

I hope this order is challenged successfully in a higher court.

5 Likes

(a) The Petitioners under provisions of section 230(5) of the

Companies Act, 2013 have to serve notices to concerned

authorities which are likely to be affected by Amalgamation.

Further, the approval of the scheme by this Hon’ble Tribunal

may not deter such authorities to deal with any of the issues

arising after giving effect to the scheme. The decision of such

Authorities is binding on the Petitioner Company(s).

(b)It is observed that the Petitioner companies have not

submitted a Chairman’s Report, admitted copy of the Petition,

and Minutes of Order for admission of the Petition. In this

regard, the Petitioner has to submit the same for the record of

Regional Director.

PL read the above on page 5, which means that petitioner companies HV not complied with 230(5).

These (point no. 8) are observations of the Regional Director and all of them have been responded to in the very next points (points 9 to 14). In point 15, the judge says “the clarifications and undertakings given by the petitioner companies are hereby accepted”. So this is not a problem.

Orient has arranged an analyst call tomorrow to discuss the merger. If anyone has the timings and dial-in details, please share here as there is no intimation to the stock exchange.

It is strange that the company arranges a con-call for investors and does not inform the stock exchanges nor displays the information on its website.

Anyway, given to understand that the call is scheduled at 2:00 pm today.

Dial in: 1800 266 1221.

All those interested may take note and attend.

Thank you @vh1, that was helpful.

I am summarizing the call below whatever I could capture for the benefit of all. There may be some errors or mistakes in my understanding, so please take your precautions before investing:

The management said they plan to appeal the judgment in NCLAT. They believe that they have a strong case and are confident of a favourable decision. They are hiring a new law firm and Senior Counsel. The appeal will be filed in 8-10 days and the NCLAT judgment will take around 6 months. Parent company RHI is very serious about the merger and is fully behind them in this. So there is no going back. They don’t have a Plan B at the moment i.e. what happens if they lose the appeal in NCLAT.

Regarding the reasons for rejection, the management said the judge has challenged the valuation on the ground of effective date of the merger (1-Jan-19) not being the date of the valuation (31-Jul-18) as the share price has changed between the two dates, making the swap ratio redundant. But in our application, we have already stated that the effective date could be this date or any other date as decided by the court. The judge has ignored that.

At the moment, nothing changes due to the rejection. They are working in close co-ordination with the two companies operationally already.

Besides the above, there were several other questions on regular business.

-

Q1CY20 was turning out to be better than Q4CY19. Things were improving until the corona issue. So far there have been no RM problems or imports from China, shipments are moving. Don’t see any issue going ahead. RM prices have not gone up due to the Corona issue, but we are facing some delays & minor cost increases with shipping companies.

-

The two previous takeovers viz., Manishri and Intermetal are proceeding well. We plan to ramp up the Manishri plant. Manishri has Rs.100 crore potential. With Intermetal also, we are planning to increase the production this year. Intermetal is very small but we plan to double production, it fits very well into our scheme of things.

-

The two merging companies RHI Clasil and RHI India are complementary to Orient. RHI Clasil is into non-steel industries. RHI India does not have manufacturing, it is a trading company. It is into bricks. The pro-forma sales of the 3 companies jointly are Rs.1400 crores in 9M. (Said something here I did not hear clearly).

-

Capacity is not a constraint, we are adding more in each of the companies. There is ample opportunity to grow in industries like ceramics, cement, glass, petrochemicals etc. We want to increase business in non-steel business. We can do new capex, but we don’t believe in huge capex. (Here something about tapping Magnesita business which I did not hear clearly). Technology will be Brazilian and equipment will be Indian. We also plan to enter foundry business in India.

-

Europe steel market is shrinking but China market is growing, cancelling out each other.

-

Consolidation has happened in the domestic Steel industry. Margins are under stress for everybody as steel companies have grown larger and have higher bargaining power. So we cannot command premium. But the advantage is also that bigger customers need stronger vendors, so it benefits us. With JSPL, we have made an Asia Pacific record. With Arcelor Mittal (former Essar Steel) we have business Rs. 8-10 crore per month, plan to increase it. We are also looking at PSU business closely; we will grow in that segment future.

(Disc.: Invested)

13 Likes

Disclaimer:

Not invested, but interested once valuations are in my range. Sharing the notes prepared from the MOSAIC research (VP, ARs, Screener, Company’s Website, Competitors Presentations, Internet etc) for discussion/feedback ONLY. Long post, but was unavoidable. I appreciate anyone who can share their thoughts/notes about the competitive advantages of this business that make it earn industry leading NPM, OPM, ROE and ROIC.

What are Refractories?

Inorganic non-metallic material that can withstand high temperature without undergoing physical or chemical changes as they have high melting points, making them a suitable barrier between high and low-temperature zones. Principal raw materials used in the production of refractories are oxides of silicon, aluminum, magnesium, calcium and zirconium, and some non-oxide refractories like alumina, carbides, nitrides, borides, silicates, and graphite.

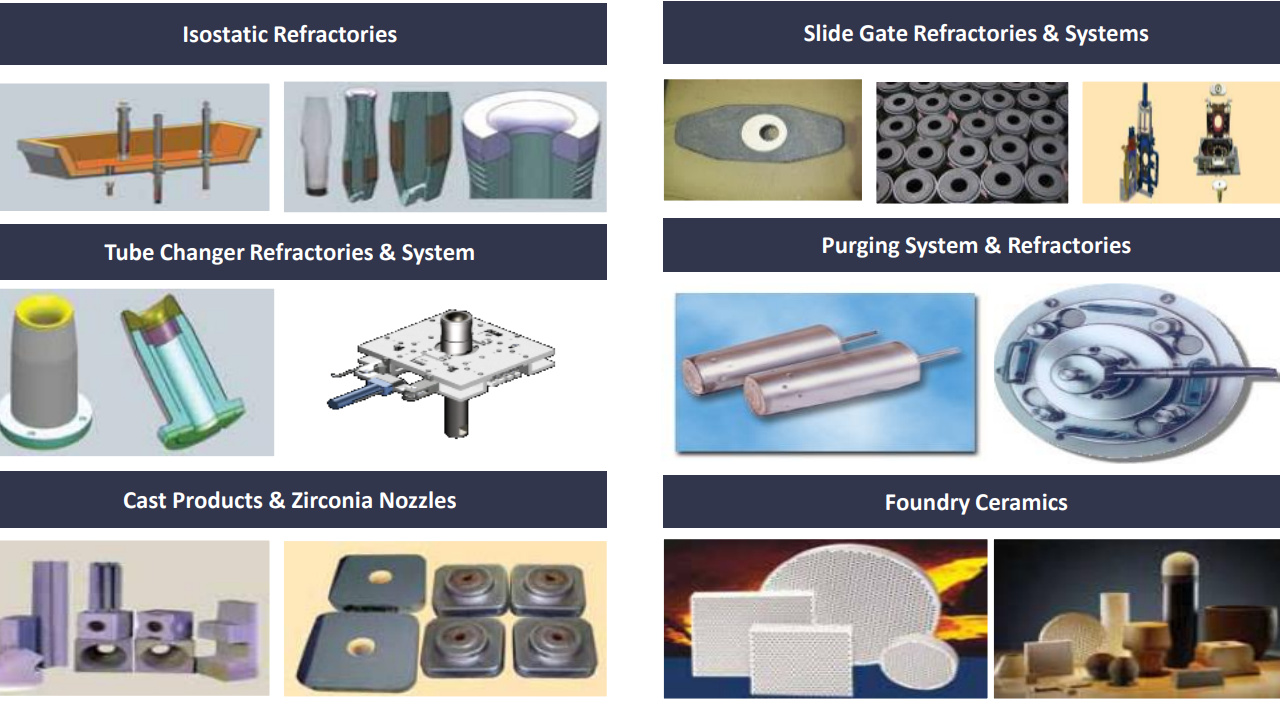

Types of Refractories: ( Source- Presentation of IFGL Refractories Ltd)

Usage of Refractories:

The refractory products are mainly used in high-temperature manufacturing processes in iron and steel industry, metal smelters, cement, glass industry and for other industrial products. Demand for the refractory is primarily dependent on the consumption of steel, which accounts for about 75% of the total value and the remaining is used for glass, cement, non-ferrous, petrochemicals etc. Steel industry, which is cyclic in nature, comprises the biggest customers.

Hence anything that affects the steel industry will have effect on the refractory business.

What are the tailwinds for the Refractory Industry in India?

As of FY2020, Indian Steel production capacity is 145 MT. Indian Steel Ministry has a target of erecting steel capacity of 300 MT per annum by the end of 2030 which bodes well for Indian refractory industry. The Indian steel industry is undergoing consolidation primarily due to ongoing Insolvency and Bankruptcy Code, which is expected to build up its strength but also to provide a higher market share for industry leaders in refractory industry since their products act as the basic need to manufacture steel.

What’s the market opportunity for Refractory Industry in India?

Indian refractory industry is around Rs 9,000+ crores, which is 3% of the global refractory market. Indian market is expected to grow at 5-6% as steel production heats up.

About the Company:

Orient Refractories Ltd (ORL) was demerged from the ‘Orient Abrasives Limited’ with effect from April 01, 2011. The equity shares of the Company were listed and admitted for trading on Bombay Stock Exchange (BSE) w.e.f. March 09, 2012 and National Stock Exchange of India Limited (NSE) w.e.f. March 12, 2012.ORL is in the business of manufacturing, plant at Bhiwadi, Rajasthan, and marketing special refractory products, systems and services to the steel industry in India and Globally.

ORL’s PARENT COMPANY RHI MAGNESITA N.V, whose shares are listed on the London Stock Exchange, is the leading global supplier of high-grade refractory products, systems and solutions which are indispensable for industrial high-temperature processes exceeding 1,200°C in a wide range of industries, including steel, cement, non-ferrous metals and glass. With a vertically integrated value chain, from raw materials to refractory products and full performance-based solutions, RHI Magnesita serves customers in nearly all countries around the world. The Company has a high level of geographic diversification with more than 14,000 employees in 35 main production sites and more than 70 sales offices around the world.

What’s interesting?

In the last few years, company’s financial strength has improved. As of Sep 2019 , company has Investments & Cash worth of 100+Cr. Company’s initiatives to use the financial assets to grow the breadth and depth of its products and offerings seems interesting considering their current ROE. In the recent past, company has taken up following initiatives ( some of these might be repetitive in case one reads the entire thread, do skip if so):

- The existing capacity of isotopic products of 9,300 tons per annum was increased to 11,700 tons per annum in 2018. The other project includes installation of hydraulic press for slide gate refractory, which is expected to be completed in third quarter of FY 2019-20.

- In April 2019, ORL acquired INTERMETAL ENGINEERING INDIA PRIVATE LIMITED(IEIPL)- which does marketing and manufacturing of steel plant equipment (viz., slide gate system for flow control of liquid steel, oxygen lancing and CCM assemblies such as mould jacket assembly, dummy bar assembly) specially used during the flow of liquid steel for continuous casting, ingot casting which are exported to various countries and caters to about 300 to 400 regular steel plant customers in India - by paying an amount of ~10 Cr. IEIPL had an average revenue of ~5 Cr. in last 4 years and company plans to double the production.

- In Aug 2019, ORL did an investment of 45 Cr. to purchase PPE assets from Manishri. The plant, which is located near Cuttack, Orissa, is identified to produce Magnesia Carbon bricks-which have had to be imported till date- and has a capacity of 18,000MTPA. As per recent concall, the plant has potential to add 100 Cr. to the revenue.

- Company is building an R&D Center at Bhiwadi.

- As per recent concall, Company plans to enter the foundry business in India.

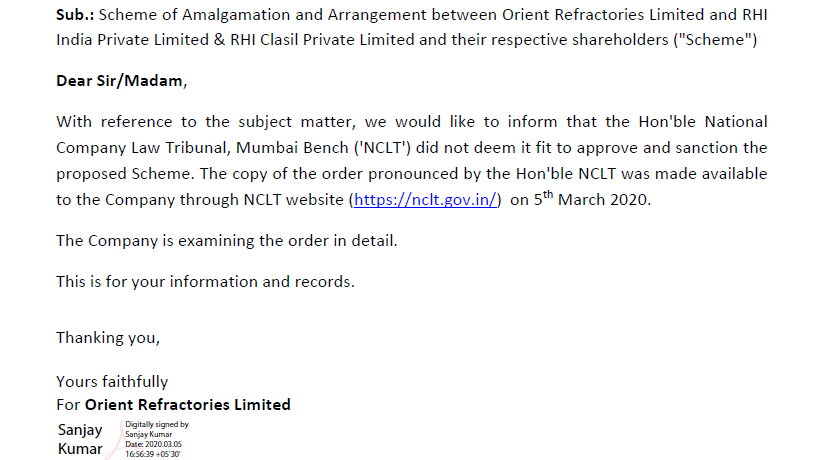

- In 2018, RHI Magnesita group commenced the reorganization of its Indian operations by merging its two other Indian subsidiaries – RHI Clasil Pvt. Ltd. and RHI India Pvt. Ltd., with Orient Refractories Ltd., in order to enhance the business and operational synergies. The combined business will create a larger asset base in India, and importantly will provide customers with one single refractory solutions platform offering the industry’s most comprehensive product portfolio, including, among others, Magnesia and Alumina based bricks and mixes for large industrial clients as well as specialty refractory products, with proven supply and sales capabilities. The Company, along with the Merging Entities, had filed a joint company scheme petition with the NCLT on [27 May 2019] for sanction of the scheme of amalgamation but the same has been rejected by NCLT and company intends to challenge the same.

A comprehensive presentation by ORL about the pursued merger, and products Demand opportunity:

ORL-Presentation

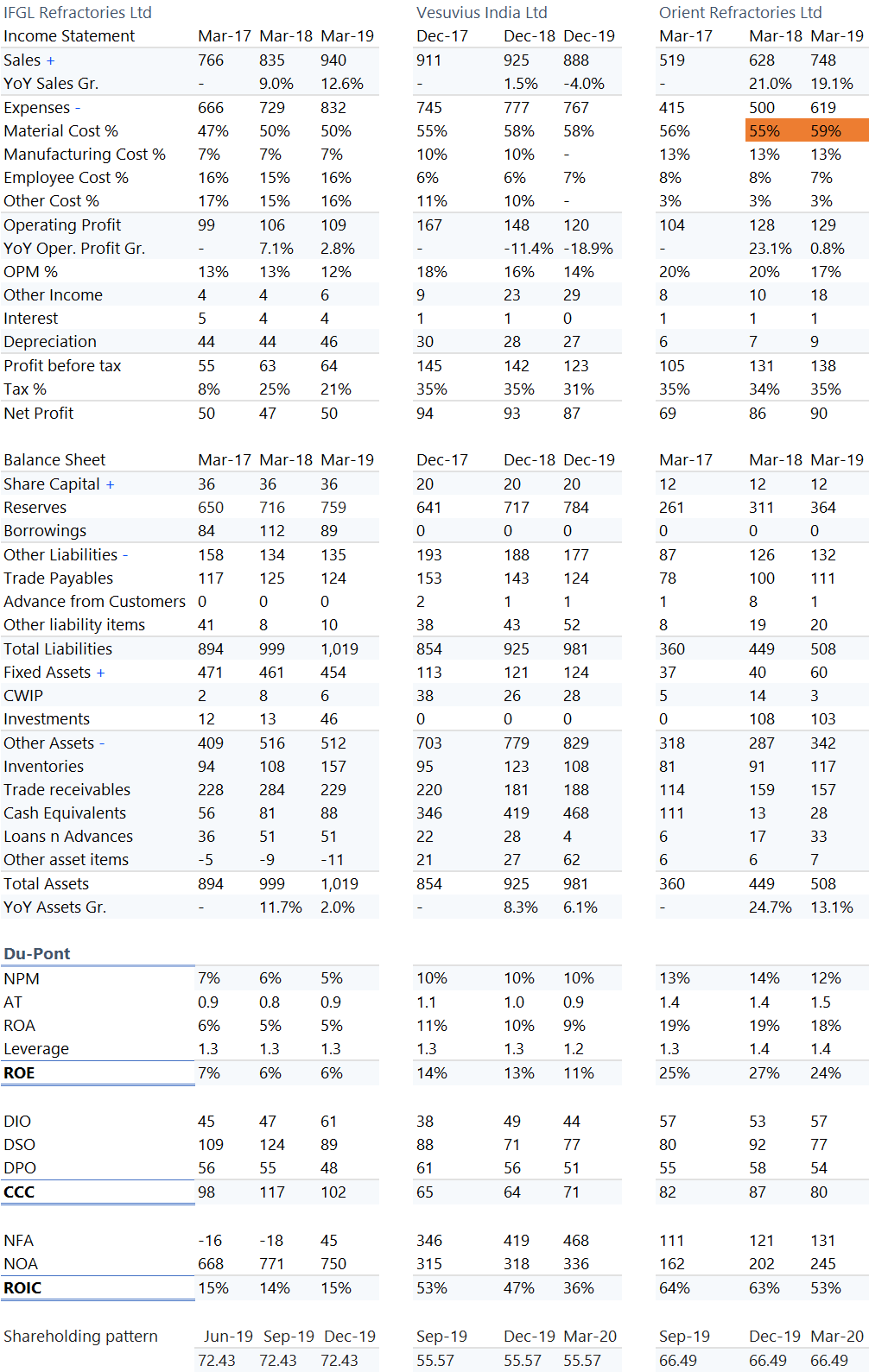

Peer Analysis: (Data Source: Screener.in, Author’s Analysis)

Data spreadsheet for your reference:

PeerAnalysis.xlsx (17.0 KB)

8 Likes

Hi @Chandragupta…

can we get the concall transcripts on ORL website …

else can you please let me know any other place where we can get it

Thanks

Concall audio is there on Research Bytes.

1 Like

This is where companies like ORL who have a strong parent and worldwide presence will have an advantage, can source Raw Materials from elsewhere:

4 Likes

Its there in Research Bytes, go to Orient Refractories page, Analyst Calls / Meets section. Date is 18-March-20 If Chrome doesn’t work, use Microsoft Edge, you can even download the .mp4 file and listen offline.

https://www.researchbytes.com/Orient-Refractories-Ltd-O0192.htm

You need to login of course, which is free.

So this might be the reason the stock shot up suddenly yesterday. Very strongly positive news:

8 Likes

please find link below for web cast of AGM

10TH AGM held on 28 August 2020

2 Likes

CARE Ratings webinar on the state of Indian Steel Industry.

https://youtu.be/v8oRX0UsJ6U?t=2165

First half an hour is on Iron Ore and Coking Coal (two key inputs in steel making). From 35 minutes onwards, there is an insightful talk by Mr. V. R. Sharma, Managing Director, Jindal Steel & Power.

Some highlights:

- Strong demand from Europe and U.S., seeing prices seen never before in a long time. This will remain so in the current quarter and at least till Jan - Feb

- Industry will see 5-6 % growth in current quarter and 10% growth in Jan-Mar 21 quarter

- Pent up demand & government infra spending driving steel demand

- Steel industry will wipe off old losses and balance sheets will become healthy

Discusses many other issues as well, on government policy, technology etc.

Hopefully, this will translate into promising outlook for Refractories sector as well.

5 Likes

NCLAT strikes down NCLT Order, allows merger to go ahead as per the original proposal.

In striking down the order, NCLAT says exactly what I had said earlier here:

https://forum.valuepickr.com/t/orient-refractories-speculation-cum-special-situation/51/49?u=chandragupta

6 Likes