The main positive points of Orient Refractories Limited (ORL) are:

The parent RHI is the second biggest player in refractory materials. They are planning to increase exports from Indian subsidiary gradually over the years. In a recent announcement ORL has sought shareholder approval to increase Related Party Transaction limit from Rs. 90 Cr to Rs. 126 Cr for year 2017 - 18 and 40% increase every year thereafter. Here we take this increase in RPT limit as a positive sign for the company.

The company is increasing it’s production capacity from 9300 T to 11500 T by 2019 for Isostatic Pressed products over next two years. It is claimed to be the most profitable product category for the company.

The increase of market share of Electric Arc Furnace (EAF) route of steel production is beneficial for ORL as their revenue share and production capacity is more suited towards that. For records, in India 57% of steel is produced by EAF route compared to world average of 27%.

In China only 5% of steel is produced by EAF route and since environmental concerns and high fixed cost are limiting growth of steel production through BOF (Basic Oxygen Furnace), we feel price of Refractory materials would remain firm in growing production environment.

The worldwide steel production is up by 5.6% in Q1 17 (Jan - Mar) and in India it increased by almost 11%. As ORL revenue is function of total steel produced, it is a good proxy to steel upcycle.

Even though the Refractory material needed per tonne of steel production has gradually reduced from 30 Kg per ton to present 10 Kg per ton, the profitability of ORL has never been dented. And as the companies are moving from just suppliers to Total Refractory Management solution provider for EAF, going ahead we are hopeful of their protecting profitability and edge in the financial ratios.

Glass and non ferrous industry also consume about 20% of world demand of refractories. These sectors are also in an upward trajectory, boding well for ORL

Oligopolistic structure with 4 key players in the Indian market ensures discipline in pricing environment.

The points of uncertainty in case of ORL are

Availability and price stability of main raw materials Magnesite and Dolomite. These are mostly imported from China to India. We don’t foresee any major hindrance in this as RHI globally is a large purchaser.

It’s dependency on steel cycle and it’s not a kind of Buy and Hold company. The unpredictability of steel cycle is not easy to gauge and exit is needed ahead of the cycle turns otherway. Even though the ORL track record says if did reasonably well in downcycle too and protected most of its profitability and return metrics.

Although the return ratios are best in class among competition for ORL, it’s main competitors like Vesuvius and TRL Krosaki and to some extent IFGL Refractories are also formidable players in the Indian market.

Overall it’s a company where investors may seek steady and safe return still the cycle turns.

Disc: This is not a recommendation to Buy / Hold / Sell and it’s main intention is discussion among members and visitors of the forum. Author has a position in the stock from lower level. No Buy or Sell made by him in past 30 days in this stock. The author recommended this stock to his advisory client at https://aveksatequity.com at a lower level and also discussed it in public forum in a recent ET Now TV appearance.

Overall, the whole refractory industry seems to be looking up.

OCL (refractory division), Dalmia Bharat (refractory division) and IFGL have shown improved FY18 Q3 results.

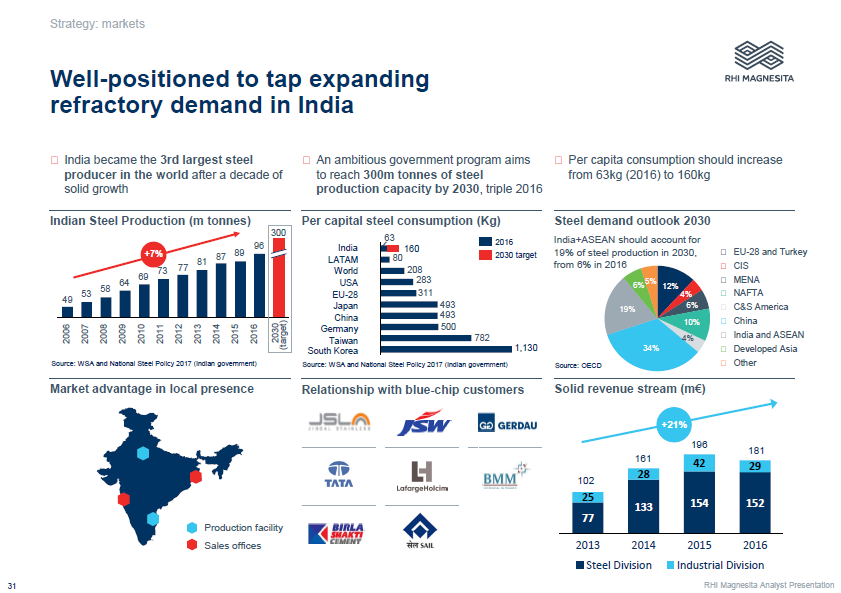

Further, for the benefit of all, would like to draw attention to RHI Magnesita’s analyst presentation.

The parent company seems quite positive on India business.

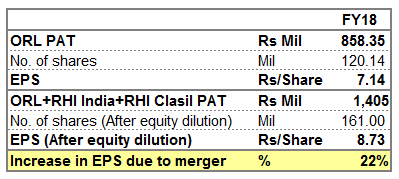

They are planning to merge RHI India with Orient refractories. Seems like for ~35% dilution of equity, the revenue is going to double. I believe this is good for existing minority share holders. RHI’s holding in the merged entity remains almost unaltered (69.6 to 70), might be because of SEBI regulations. Am I missing anything?

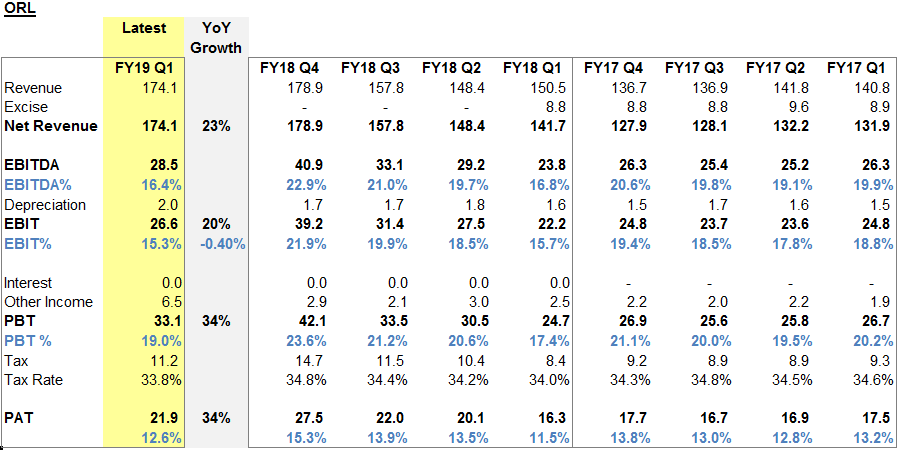

1.good results by the company, sales up 18 %, PAT up 34%

2.the two unlisted companies RHI india and RHI clasil being merged into orient, RHI india is a trading company, while RHI clasil is more into alumina based refractories, both have had a good ROE in Fy18.

3. post merger share count of orient goes up from 120 mln to 160mln while the revenue of combined entity being doubled and PAT goes up by 60% ( considering FY18 P & L).

Apart from the immediate arithmetic, I see two distinct advantages from this merger:

ORL was hitherto “allocated” to Steel, as per RHI’s corporate policy. Now a whole new world of opportunities in other sectors such as cement, glass etc. opens up for the company.

The presence of Wholly-owned Subsidiaries in similar business lines acted as an overhang for the stock, due to fears of a possible conflict of interest of the promoter. Those fears will now go away.

The stock should get permanently re-rated upwards with this development, I think.

RHI should hold less than 75% of the merged company as per SEBI rules. Since the remaining two companies which are being merged are almost fully owned by the parent company, they’ll have to dilute some stake in this before merging.

Also, what does the community think about the current valuations (~220)?

I think it is still undervalued even after the surge after Q1 results given that it is merging to become a bigger entity with 100% increase in revenues and 60% increase in PAT.

I believe their margins will improve further after the merger.

In 2013, RHI Magnesita group acquired Orient with an intention to scale its refractories business in India. Reading an article on its merger scheme. The change in shareholding and the merger should bring in more corporate governance for the companies.

ORIENT REFRACTORIES LTD has approved the acquisition of entire paid-up equity share capital of ‘Intermetal Engineers India Pvt Ltd’ (IEIPL) a Company comprising of 1,597 equity shares of Rs.100/- each to make it a Wholly Owned Subsidiary of the Company.