Hi Deepak,

Thank you for the detailed response.Much appreciated. From the looks of it, we stand to face disruption from Watsapp pay then? Considering reliance is now involved, i think other players will be significantly impacted.(Hope my comment doesn’t get flagged, still figuring out what works in this forum and what doesn’t!)

From what i am reading on the subject, i don’t think payment gateway platform companies will be impacted much though.I am still trying to understand their business model and seeing where all the individual components fit in the value chain.So wondering if payment gateway companies might face disruption in the future. Thoughts?

Regards,

Shweta

Well said!

In a recent interview to a TV channel, HDFC CEO Keki Mistry explained why financials is optically an easy yet a very tricky business. He quoted “It is very easy to increase market share in the finance industry by compromising lending norms and HDFC doesn’t believe in this philosophy”. Needless to say that lending standards are the backbone of financials.

Coming to your point on importance of confidence in lending business, case study on Money Matters Ltd explains best its relevance.

Money Matters CEO in 2010 was accused of bribing Banks to get money. The development led to a massive fall in stock price and ultimately the business. Despite solid return ratios, confidence crisis never allowed the NBFC to reboot to its normal state. The company was eventually merged and renamed as Capri Global Capital.

This NBFC fallout played a pivotal role in my understanding about the importance of reputation in lending businesses.

Chiefly, NPA ratios - end product of lending standards - gives a better indication of how lenders are managing their reputation risk.

1 Like

@deevee in you blog post you had mentioned that you made your decision of exiting RBL bank one year ago after discussion with one senior investor. Can you highlight which points he mentioned so that it will help us understand RBL bank in better way.

Disc: exited with loss few months back.

2QFY21 Result and con-call highlights:

Asset Quality:

Slippages: As NPA recognition stood still, RBL Bank’s reported slippages (₹1.45bn v/s 0.5bn in the

previous quarter) around one fifth of FY20’s run rate. The up-gradation & recoveries stood ₹2.3bn

against ₹1.5bn in 1QFY21.

Headline NPA: Reported GNPA/NNPA/PCR: 3.34%/1.38%/74.8% against 3.45%/1.65%/70.5% in the

previous quarter. Calculated PCR stood at 59.4%. The bank’s Pro-forma GNPA and NNPA ratio would

be 3.49% and 1.49% respectively.

The “BB + and below” book stood at 7.5% of the total book. The “BB & below pool (calculated)” stood

at ~6.3% of the net advances.

Provision expenses: In 2QFY21, the bank’s provisioning expenses stood at ₹5.2bn v/s ₹5.0bn in the

previous quarter. It included COVID provisioning of ₹3.1bn. Additional ₹3.54bn COVID provisioning

was done in the previous two quarter. The total COVID provisioning stood at ₹6.64bn (120bps of

advances). The COVID provision includes mandatory provision of overdue accounts as on 29th Feb

2020.

Balance Sheet:

Advances: The bank’s advances stood at ₹561bn; declined 4% YoY and 0.9% QoQ. Loan Mix carries:

Retail: 43%, Corporate: 43% and DB & FI: 14%. Retail loan grew at a healthy pace of 7% QoQ and

wholesale de-grew by 5% QoQ.

Deposits: The bank’s deposit stood at ₹645bn and grew healthy sequentially at 4.5%. CASA inched

up 100bps sequentially to 31.1%

CRAR stood at 16.1% with Tier 1 of 15.1% and a LCR of 171%. The bank got approval for fund raise of ₹15.7bn through QIP. The post – money CET: 1 would be 17.4%.

Income statement:

NII/NIMs: The bank’s NII stood at ₹9.3bn; grew healthy by 7.7% YoY and de-grew by 11% QoQ. Bank’s

NIMs de-grew by 51bps sequentially to 4.34% because of proactive reversal of interest income on

Non-wholesale book. It is further expected to slip in next quarter. Non – interest income grew by

3.3% YoY and 37% QoQ.

Bottom line: A strong other income led to PPP growth of 4.4% QoQ to ₹7.1bn. A heavy and

sequentially flat provisioning expense (₹5.2bn v/s ₹5bn in 1QFY21) led to PAT growth of 2.1% QoQ

to ₹1.44bn.

I see hope for retail facing banks.

In recent RBL investor presentation, Ahuja sahab says:

"Given our business Traction and competitive strength in certain businesses, starting next quarter, we expect to return

to profitability and over the next nine months, make up for the loss of the quarter, and shall target

an ROA of 1% or so for exit Q4 of this year, thus setting us up well for the next fiscal year. "

So Eps is going to start looking good only after a few quarters.

Apparently, RBL has learned well, and they are now setting their strategy right.

Bank has plans to expand books in rural finance, home Finance, increase CASA and most importantly they are credit card focussed.

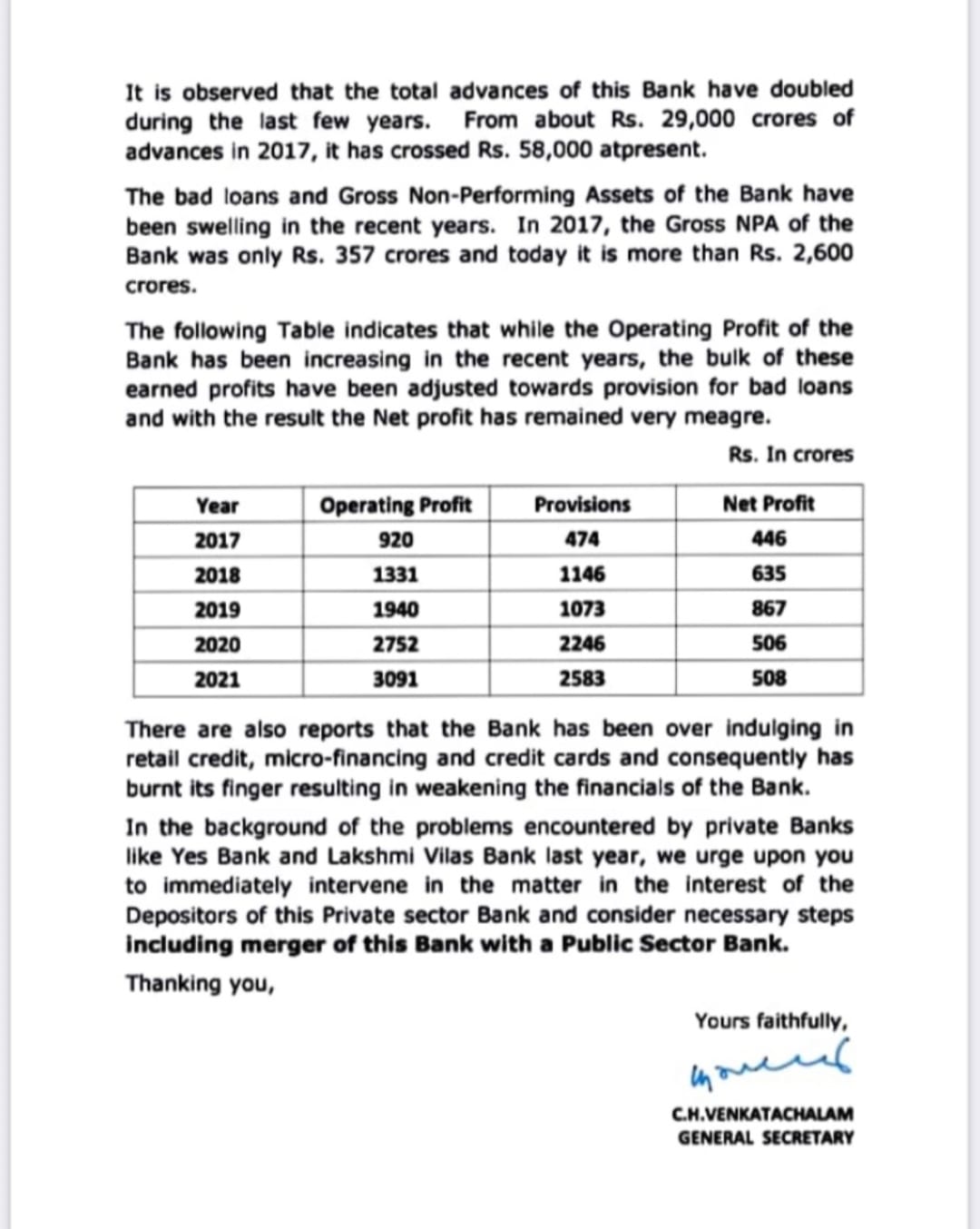

All in all, I feel the way RBL is attractively priced at

10K Cr Mcap for 3114 Cr (FY21) of PPOP

compared to say idfcfirst which is priced at:

30K Cr Mcap for 3113 Cr (FY21)

Compared with Au Small finance:

34k Cr Mcap for 2158 Cr

(AU, Bandhan are probably not a right comparison RoAs are different)

In short, idfcfirst is priced 3x of RBL. Furthermore, RBL has plans in action to increase the Loan book, whereas idfcfirst is riddled with legacy issues and have not shared any plans to expand their loan book.

Ofc there are parameters in which IDFCfirst wins, like a high CASA ratio, which it achieved quickly. So I feel RBL can do it as well, as it appears to be a function of interest rates.

3 Likes

Is there a way to find the outstanding esops and the exercise price ?

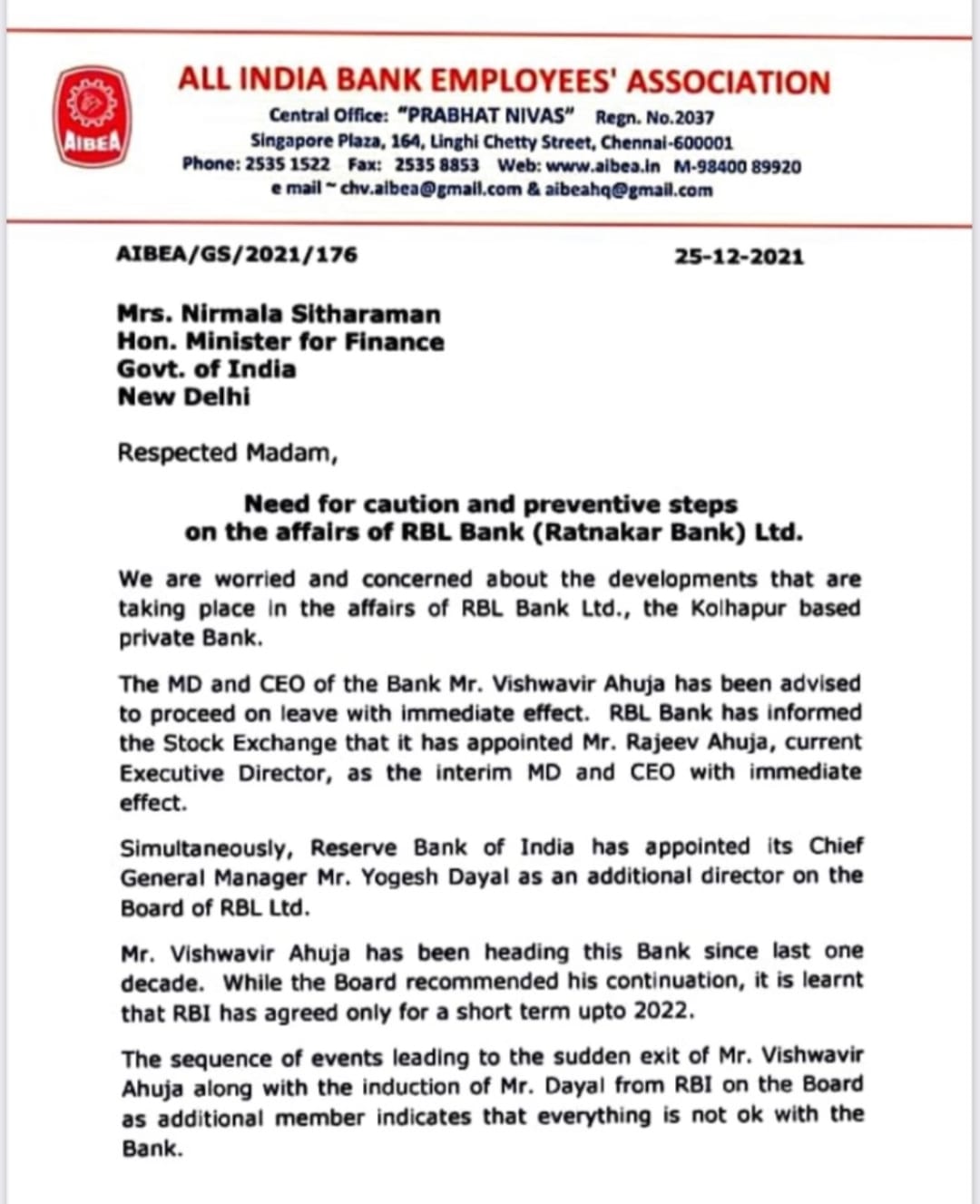

RBI knows something more than what is disclosed.Expecting in the next 15 days based on RBI appointed director,moratorium on withdrawals and disbursement of loans.Hopefully the bank will survive but will cause pain to shareholders.

One part of me says that everything was fine even in the last AGM call, they had enough tier 1 and a good enough PCR. The stock was already really cheap at 0.8x PB so it’s not really comparable to yes bank

But on the other hand, i dont see any good reason for the RBL to appoint a director over the weekend and the MD to abruptly leave with no explanation.

Unfortunately with no information it’s hard to take any decision and the stock is going to be in the lower circuit on monday anyway so it’ll he hard to take a decision.

If it was a normal think the the RBI could have just released a divergence report and allowed the existing shareholders or new ones to pump in capital, this kind of behaviour from the RBI makes it impossible to invest in any small bank

disc: recently invested, planning to exit

2 Likes

In hindsight maybe but only upon a time Bajaj finance was a tiny no name capitive finance arm of Bajaj. All the big banks like icici, axis, hdfc were tiny compared to the psu’s in the 2000’s

It is laughable that a country as massive as India will end up with only 3-5 lenders. There are a lot of banks that each service lots of niches in the economy. There is a very high risk associated with smaller banks compared to larger banks but just saying stick to leaders is lazy

3 Likes

I spoke about current situation… And by leader’s i didn’t mean the size of bank/nbfc …

If going by mere size , it’s SBI . Which is 3x bigger than HDFC …

What i emphasised was quality … as they will be the last one to fall…I never mentioned banks , it can b any financial institutions like

In banks - hdfc, kotak now even ICICI

SFB - AU

Gold financing - muthoot

Nbfc - bajaj finance , chola

Psu - SBI, canara ,bob

Home loan - Hdfc , Aavas

These stocks trade at premium, for a reason…

But lot of people i know go for bargain and burn their fingers…

Yes bank , dcb , suryodaya, ujjvan now RBL and lot of examples on nbfc side

At present for me it’s rationality. Or as like u mentioned even if it’s laziness , I’m happy it saved me.

Here RBI is absolutely right , their first job is to protect the interests of customers , not investors.

2 Likes

I have avoided investment in banks be it private or public after loosing fortune in yes bank, it was a major shock of my investment journey, by gods grace could recover losses and alos made huge money in last 18 months, selling yes bank at 10 rupees, i still remember so that this blunder never happens. Yes bank, Dhanlakshmi, RBL, Ujjivan, Suroyadaya, are examples. Even for long term portfolios i dont want to hold and bank as banks are most leveraged business and highest risk.

Stock market is not for small investors, regulations doesn’t favor small investors here, see equity portion of DHFL, Yes bank, videocon, equity is valued last when liquidation or takeover is finalized. Always looks for strong corporate governance and large companies to avoid loss of capital.

the jhunjhunwala story seems planted, they don’t need premission to go up to 4.99% and logically, they would reach that first during the panic at a much lower price before getting permission for 9.99% which they can go via a QIP incase the bank needed money

6 Likes

initial question: 0:00

Somnath Ghosh (insightful): 10:00

DSP, what are the issues and succession plan: 13:20

Succession plan: 18:20

Why did the RBI take this decision: 32:30

Kotak sec: 40:45

Previous stress tests : 45:10

Succession again: 48:40

Any divergences? (not yet): 54:00

MFI (provisions taken upfront, see some more stress in q3): 56:00

Is vishvavhir still part of the board? (no answer): 57:20

Any more RBI appointees likely? (insightful): 1:01:30

Wholesale: 1:14:00

Liabilities: 1:20:30

Fund raising (most likely 2023): 1:21:30

They didn’t mention anything about raising capital immediately, only mentioned tier 2, @Aniesh7 you share a (now deleted) post that claimed that they were in talks with a US fund, would love to know where you got that info from

lots of rumours spreading and out of context quotes floating around on both the buy and sell side, better to actually listen to the management. Believing them is another things but everything should be heard in context and take an informed decision

2 Likes

https://m.rbi.org.in/Scripts/BS_PressReleaseDisplay.aspx?prid=52928

There has been speculation relating to the RBL Bank Ltd. in certain quarters which appears to be arising from recent events surrounding the bank.

The Reserve Bank would like to state that the bank is well capitalised and the financial position of the bank remains satisfactory. As per half yearly audited results as on September 30, 2021, the bank has maintained a comfortable Capital Adequacy Ratio of 16.33 per cent and Provision Coverage Ratio of 76.6 per cent. The Liquidity Coverage Ratio (LCR) of the bank is 153 per cent as on December 24, 2021 as against regulatory requirement of 100 per cent.

Further, it is clarified that appointment of Additional Director/s in private banks is undertaken under Section 36AB of the Banking Regulation Act, 1949 as and when it is felt that the board needs closer support in regulatory / supervisory matters.

As such, there is no need for depositors and other stakeholders to react to the speculative reports. The bank’s financial health remains stable.

Ajit Prasad

Director (Communications)

4 Likes