Disl: I took a position in RBL bank yesterday.

The current situation with RBL bank is quite interesting. Let us look at facts as they happened chronologically:

Saturday 25th Dec

a) RBI appoints additional director on board.

b) VV Ahuja goes on indefinite leave. Rajeev Ahuja become interim MD/CEO.

Sunday 26th Dec

c) The board issues a presser reiterating their guidance.

d) The board conducts a conf. call attended by Rajeev Ahuja.

Key Points:

No additional info on why VV was removed. Reiterated the Q2 guidance of below 2% net NPA and Q4 exit RoA of 1%, difficulty in MFI book.

Some conjecture that can be made, there were differences between RBI and VV on his succession planning, RBI likely had issues on large variance in credit cost during VV’s tenure.

e) CNBC-TV18 reports RJ and RKD are looking to acquire 10% in the bank.

Monday 27th Dec

f) CNBC-TV18 reports RJ has no interest in the bank before the markets opened.

g) The stocks tanks 25%.

h) RBI issues a clarification about the financial position of the bank.

i) Bajaj fin renews the Credit card arrangement with RBL bank.

What has changed?

a) VV Ahuja is out.

b) RBI has intervened.

c) Bajaj Finance has renewed the partnership.

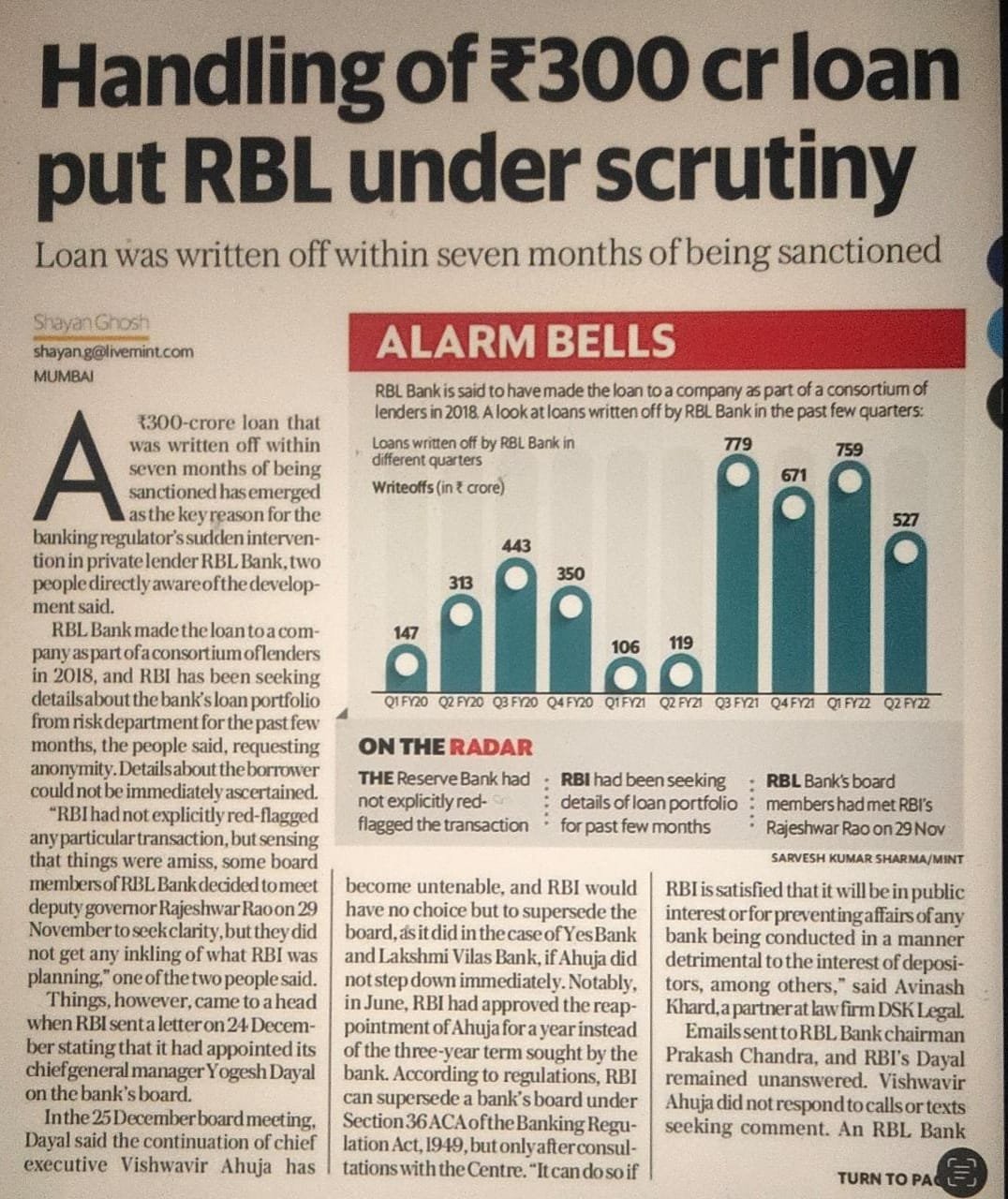

d) We know that Q3 results are in line with expectations as mentioned in the conf call. The book is more or less kosher because of RBI’s clarification on the fianancial health of the bank

Moving on to VV’s tenure at RBL:

VV Ahuja became MD of the bank in 2010. From then on the bank started to accelarate growth. The entire idea was to continuously raise capital, lend to corporates, focus on MFI, bring in high quality management by incentivising them with ESOPs. The goal was to achieve scale and all the advantages that comes with scale like op. leverage, low cost of borrowing. Corporate lending will keep opex in check and MFI will keep the NIMs high. The bank’s advances grew from 1170 cr in 2010 to 54000 cr in 2019 a 50x growth, this resulted in an optical reduction in NPA’s since the relative balance sheet growth was way higher. The bank raised capital every alternate year and at higher P/B multiples. The end goal was to reach the coveted 1.5% RoA no. The branch addition was kept to minimal to keep a check on opex. In 2019-20 corporate portfolio problems started to emerge and this was also the time when Yes bank and other FIs started failing. Severe stress started emerging in RBL’s corporate books. VV Ahuja to his credit came out in middle of a quarter and accepted issues with their corporate book. What followed was a period of significant provisioning/write offs in the corporate book starting from Sep2019 to Dec2020. Meanwhile the other large retail portfolio of MFI started getting multiple hits due to demonetization followed by Covid Wave 1, Covid Wave 2. By this time VV Ahuja and the rest of the mgmt. at RBL had realized that they were on a slippery slope and had to have more solid business verticles. They started cleaning up their books very fast and started growing the third line of business in Credit Cards and started focusing in home loan portfolio.

In summary VV Ahuja created a sizable balance sheet expanding on the corporate side and MFI and just when everything was going great the bank hit multiple roadblocks.

How does it look now?

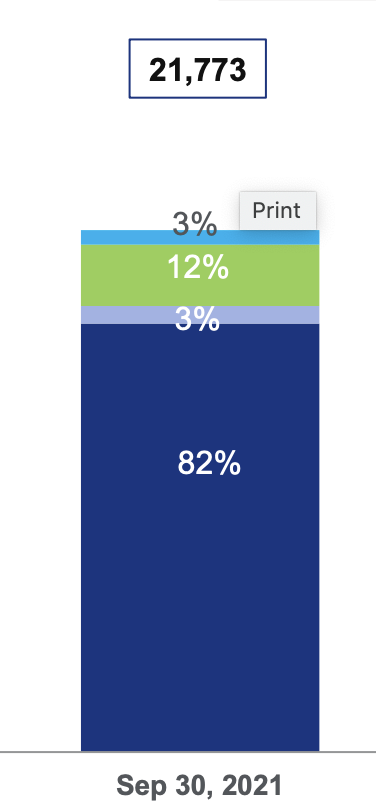

The bank’s advances haven’t grown since last 2.5 years, corporate book is down from 33000 to 25000, MFI is limited to 10%, Credit card portfolio is around 20% of the asset book, MFI PF is down from 7000 cr to 5000 cr. Bank has added large no. of retail branches and will continue to do so. The corporate book has low yield and higher rated portfolio has gone up. The retail wholesale mix now is 55:45 and the bank intends to bring it down to 65:35 in favor of retail.

The idea of having MFI at 10% imo is to have a high yielding priority sector portfolio and avoid buying it from third parties and avoid agri loans. Structurally the bank is in a much better shape now IMO. What is also celar from the past conf calls is the bank is also more focused on Housing sector. The housing PF today is 3%.

How is the macro environment now?

A lot of corporate defaults have happened between 2015 to 2020. Some of them were frauds and some of them were geniune defaults. The troubled coporate sector areas a few years back, today are in a much healthier state. One doesn’t see Power/Infra/NBFCs/Metal companies in any sort of distress. The retail distress does exist due to Covid and is a key monitorable.

Is the situation similar to Yes Bank?

I dont think so. The situation is similar to Yes in the manner in which RBI has intervened but otherwise not so much.

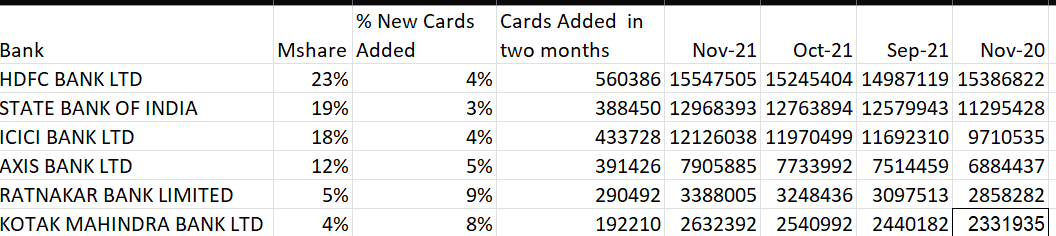

The dominoes are not falling in the corporate world. The corporate macro environment today is much better than it was in the case of Yes bank. RBL over a period of last two years has written off significant bad debts from coporates, the book too has shrunk significantly. The corporate book today is much granular for RBL. Micro loans PF has also shrunk with significant write offs and the bank intends to keep it at 10%. Bank is well capitalized. Credit Card PF despite being unsecured is much safer and bank has started growing its coporate book again. The bank did not issue Credit cards in 2 of 3 months last quarter due to Visa localization issues and despite that Bajaj fin continued its relationship. Credit Card customers are mostly salaried. October Credit card data released on RBI site shows significant growth.

The Key risks:

Investment in banks is about trust. Having observed the evolution of the bank I dont see a possibility of frauds involving management (if I am wrong here the entire thesis goes for a toss). RBI clarification on the fianancial health of the bank is another indicator of the asset book. At a personal level my position is less than 5% and if I see more issues with my thesis I will exit the stock.