https://www.bseindia.com/xml-data/corpfiling/AttachLive/6eae5bcf-efb7-425a-a414-3500891b61ed.pdf

1 Like

Being their CC partner Bajaj Holding can be interested in having a stake.

Clarification from RBL Bank

RBL bank approves fund raising via private placement of equity shares worth 826 cr to five investors at 340.70 per share

https://www.bseindia.com/xml-data/corpfiling/AttachLive/98f0b116-ab8a-453f-a723-5bde6311ff3c.pdf

Rbl Bank launches QIP today to raise 2000 Cr.

RBL Bank successfully closes QIP, raises Rs. 2,025 Crore

4 Likes

Latest Results

- Net Profit reduced by 69% YoY in Q3 FY20 due to accelerated provision on advances (9M FY20 reduced by 37 YOY%)

- NII growth of 41% YoY in Q3 FY20 (9M FY20 growth of 45% YOY); Other Income growth of 30% YoY in Q3 FY20 (9M FY20 growth of 36% YOY)

- NIM continues upward trajectory, 4.57% in Q3 FY20 vs. 4.12% in Q3 FY19 (4.35% in Q2 FY20)

- GNPA at 3.33% vs. 1.38% in Q3 FY19, NNPA at 2.07% vs. 0.72% in Q3 FY19

- Total customer base of 7.82 million; addition of 0.5 million in the quarter

1 Like

Guys, till when do they have partnership with Bajaj finance on CC? if I remember its 2022.

Did RBL management comment on the watch list? At Q2 end, it was 1800 Cr.

The current market crash will give good opportunities to invest in good companies. Drop in RBL bank got accelerated due to YES Bank fiasco. I believe private banks will continue to gain more market share from public sector banks in a faster space. Also few business/Clients of Yes Bank and Govt banks should migrate to HDFC/Kotak/SBI/RBL/ICICI/IDFC First etc leading to more business.

I recently purchased more of RBL after selling 90% at 550-600 levels. Though NPAs recently hiked to 2.5/3% level, I feel the bank will tide over this in the next 1 year. It constitutes 2nd largest holding in my portfolio. Hoping to see no spike in NPAs beyond 3.5%, fingers crossed.

1 Like

You have stated that drop in RBL bank accelerated after fiasco of yes bank. If it is so, the customers would move either to PSU banks or strong private banks (which are very few).It is stated that Mr market knows muh more than an investor,what could be the reason your opinion in continuous fall of RBL share price and assumption that NPAs of RBL would get managed better from now on.

2 Likes

The bank was commending premium due to 30% plus growth YOY, however it did come at a small price leading to a hike in NPA. The management acknowledges it mistake and have already taken corrective steps on the future steps to manage its loan book. The management is good, HDFC too has quite a decent stake in it. I believe the bank might show subdued results in the next 2 quarters, however 2-3 years down the line the scope of growth is immense. Based on current valuations, i feel the bank is attractively priced. Closer look on its NPA level is the key.

I believe the fall is more due to Yes bank concerns over small private banks financial conditions. RBL today came over with a circular yest that they lost 3% in deposits in the last one week, however post RBI update yesterday over banking sector, I wont be surprised if RBL wins back 75% of them back in 1-2 months at max. Whatever the trouble, at current price fears are over done. I dont bother with 1-2 quarters results, good business are made over continuous hardwork over the years. I wont bother with the price for the next 6-12 months, either be it 100 or 300.

Disclosure - I added 50% more to my current holding in RBL bank yesterday at 160.

2 Likes

Yes, remains same at the end of Q3 too.

Updates-

According to a regulatory filing by Coffee day Enterprises, it has received the first tranche of Rs. 2000cr out of Rs 2700cr for the sale of Global Village Tech Park.

Link- https://www.bseindia.com/xml-data/corpfiling/AttachLive/f0c9d5f9-63e5-4e7b-b293-19b592be28b5.pdf

According to bloombergquint, RBL bank has been repaid the full amount.

Link- https://www.bloombergquint.com/business/coffee-day-repays-rs-1-644-cr-to-lenders-after-getting-sales-proceeds-of-tech-park

And as per Livemint, Rbl bank has received Rs 81 cr

Link- https://www.livemint.com/companies/news/coffee-day-gets-rs-1800-crore-from-blackstone-for-it-park-deal-11585319349415.html

2 Likes

What most people do not realize about financials - Loss of confidence in the lender’s stock price can eventually translate into loss of confidence about the business itself

Imagine someone is running an IT company - the stock price falls 40%. Do the customers really care? Maybe but mostly not. An IT company can continue to grow revenue and profit even if the share price falls lower since their core service does not have any linkage to how the financial markets perceive the company. As long as products/services are up to the mark, customers are fine with doing business with the company. Deals are signed, money keeps hitting the account.

Whereas if you are a bank, there is a very direct business linkage to how the market perceives the stock price. Over the past few weeks a lot of corporate customers have been pulling out deposits and reducing dependence on the banking systems of a few banks (we all know which banks). A bank has to get money from either deposits or from the debt markets, this gets impacted when the financial market perception of a company’s stock changes for the worse. The question that starts plaguing everyone is - If everything is all right, why is the stock price falling everyday? Does the market know something that I do not know? Is my money safe? Let me move my money to some other bank till things stabilize

A bank/lender creates value through the prudent use of leverage, borrow multiple times compared to net worth and deploy that money into areas where one can make a good spread. When the cycle gets punctured (reason maybe genuine or silly), this can affect the actual operating prospects of the business itself. Then leverage works in the negative cycle and takes away value from the business.

Does not mean that one should not invest in lenders (though I personally haven’t so far), it just means that one needs to think of these possibilities in a more nuanced fashion for lenders compared to any other business. Some businesses are inherently riskier than the others, banking any day carries more risk than a consumer business that sells soap. There is a very good reason why banks are regulated so closely while most other businesses don’t have even 5% of the regulatory oversight.

Always understand the game you are playing. If I ever invest in a lender, I would spend more time tracking how the debt markets are pricing their fixed income offerings than track what the equity markets are saying. Everything gets linked, a 6 month liquidity problem (whatever be the trigger) can bring down a lender even if the rest of the business is solid.

25 Likes

A unique perspective indeed: ITs and FMCGs may not be affected by a tumble in the stock price, but banks get affected as depositors’ confidence reduces.

I see Lending as one of the most lucrative sector for investment, even more than banks, FMCG, Pharma and definitely IT; and your perspective gives me an added reason to be watchful.

Could you please elaborate. Or better if you could demonstrate with a specific example of this very bank. It’d be golden.

Thank You.

I have always been enamored by these newly listed banks (the likes of IDFC, RBL, AUF etc.) as I strongly felt that one can safely ride the wealth creation journey over a 4-5 year period, provided you get the entry point right. But almost all these IPOs were obscenely overpriced and didnt provide too much comfort to invest.

Today, RBL at 0.6 times book (vs the crazy 4-5 times few months ago) seems to provide as much valuation comfort as one can reasonably expect. In this regard, to sharpen my knowledge- i started browsing thru the VP thread from 2016 IPO days.

I just cant wonder at the prescience of @Yogesh_s and @8sarveshg in highlighting the risks a good 2/3 years prior to such events unfolding…I had a surreal feel when i went thru their pointed observations around the following concerns

- mgmt intentions - way too many analyst meetings for a small bank!

- masssive ESOP led dilution

- juicy corporate loan & fee income growth

- recency of their loan book- and predictions as to how the NPA indigestion to haunt them later

- Equity dilution to pump up the overall Book (and not necessarily the per share metrics like EPS, BVPS etc.)

- obsession over “fastest growing” bank tag

No amount of excel jugglery & Warren Charlie quotations can stand in front of common sense / risk mgmt approach these 2 gentlemen have articulated in less than 200 words! Hats off to you folks! . Its such a sad feel that @Yogesh_is isnt active on the forum

17 Likes

Hi Deepak,

Brilliant explanation. I am currently researching Infibeam and trying to understand how payment apps work, risks they face, moats and other things. Going through the diagram you have put up, are so many intermediaries required? Is there a possibility of big players integrating these intermediaries into one big solution and thus wiping the small players out?

Is there any resource that explains these details in a more basic fashion. Or any point of view you have on Infibeam? Surprisingly there is no thread on this company in Valuepickr.

Any feedback much appreciated.

Thanks,

Regards,

Shweta

1 Like

Hi @shwetukk

Nice to note that you found it useful.

Retail B2C payments have changed quite substantially since I wrote that post actually. The business models have also been tweaked. It is a long topic but I will try to summarize a few models which are there now.

Wallet issuers: These pre paid instruments imho will be out of vogue. RBI had mandated KYC by Feb 2020 which they luckily had waived off in a way in Dec 19. I don’t think standalone wallet businesses stand any chance of survival unless they pivot or get acquired else shut shop.

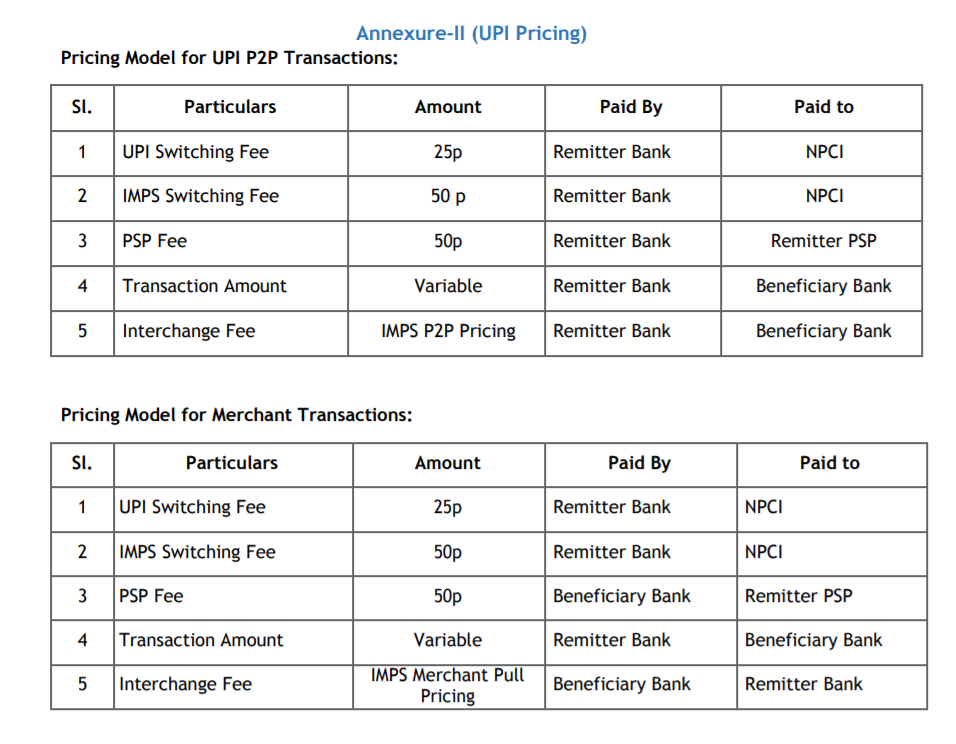

UPI: The biggest uptake has happened here. This has completely changed the industry. More importantly the financial considerations in a UPI txn is quite different to what I have explained above. In summary this is what it looks like

There is a 80 page document called NPCI UPI Procedural Guidelines. I have an old version of it. Google for the latest version you will get it.

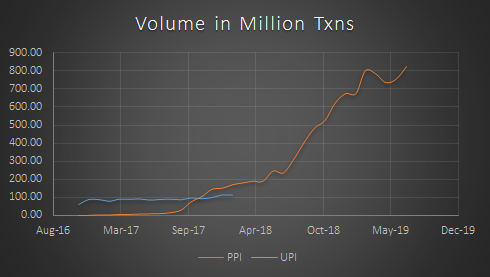

UPI has swelled from ~0 txns in April 2016 to over a billion txns in Oct 2019. I haven’t updated my data after that yet but the trend will be upwards.

Imagine the power of sending money on whatsapp. It is convenient & quick. A payment use case is a subsidiary use case to chatting and that is how we have seen a lot of success in say WeChat pay in China.

Credit: I used to joke that pitch a small ticket credit line idea to a VC and he will give you more money than you need. Not sure if that is happening now. But RBI has put regulations around this now. My basic disconnect is most of the products say they are getting new users but it is the same user who is credit worthy and getting these lines. Models of risk scoring might be effective but I do not know. Anyways small B2C credit line businesses are minuscule actually.

Traditional Credit/Debit/NetBanking: These will no go away so easily. Cards have survived 70 years or so with archaic mechanisms. Infact they are still written in Fortran! All payment processes have evolved from this in terms of authorization, authentication, clearing and settlement.

I dont think customer facing businesses are looking at building a standalone payment business either it will be there to assist another business or will act as an enabler.

Big players are always acquiring intermediaries across the verticals. Check up say a Visa and MasterCard they always tend to acquire processors or get a stake. Infact they even get stakes in B2C companies in payments.

How will say the end state look like. I have my own views on who will be the leader in this. But refrain from that discussion in public as I am working in this domain. Excuse me on that.

I do not track infibeam either.

Rgds

Deepak

4 Likes