Yes, they won’t be the same. I don’t know how the share capital amount adjustment will happen (perhaps any knowledgeable person can share the details). But the number of equity shares will be done as mentioned in my post above.

1 Like

In demerger, the company’s worth or market capitalization before and after the demerger matches. Equity or number of shares pre and post does not match.

Presentation from today’s investor meet, highlighting different segments and future strategy in all three verticals.

Covers some new initiatives in lifestyle like Sleepwear by launching SleepZ By Raymond and Innerwear in Park Avenue, and more insights about MPPL business on the engineering side.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/dbe36c70-d3e5-461b-85b6-a2d45781506f.pdf

Out of these three businesses, which has higher growth potential going forward and available at reasonable valuation?

When the new demerged business will be listed on exchanges for retail investor buy/sell?

Because of decrease the FV, no of share is increase but equity share capital will be same. EPS will decrease. ESC only change when fresh issue will happens.

This should be a good sign, if a proper succession plan is in place and even better if they disclose it…

There is already a succession plan in place for the Raymond group which is yet to be disclosed publicly. While specifics are confidential, rest assured, a well-considered and robust process is in place, maintains Raymond Chairman and MD.

1 Like

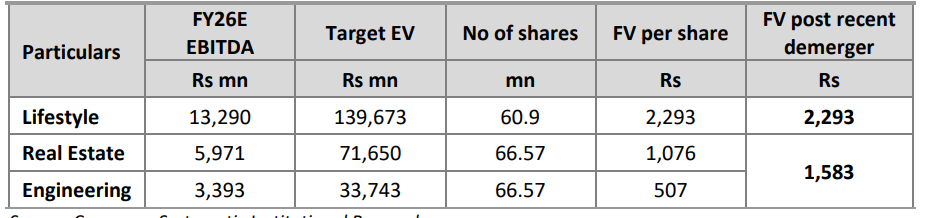

Systematix assign fair value of ₹1583 per share for Raymond Ltd (Ex-Lifestyle) which includes ₹1076 and ₹506 for real estate and engineering respectively. They value Raymond Lifestyle Limited (RLL) at ₹2293 per share of RLL.

Full Report: https://intra.systematixgroup.in/Institutional/IPOMail/Raymond%20-%20CU%20-%2006-07-2024%20-%20Systematix.pdf

This seems quite low multiples.

For example - Page Industries has an EV/EBITDA multiple of ~40+. Raymond in shirting is as big a brand as jockey in underwear. Both have premium positioning.

Similarly, DLF and Godrej Properties has an EV/EBITDA multiple of ~60+ - similar asset-light business model

Shouldn’t that dictate the potential value?

1 Like

Price discovery - Raymond Ltd (ex Lifestyle) is trading at Rs. 2000 today

what a great value unlock story this has been… been holding since Rs 440 for entire company…

now the RE + engg alone quoting at 2k… insane…

2 Likes

Depending on what the Lifestyle shares are listed at there could be some selling pressure on the original shares by DIIs and FIIs.

1 Like

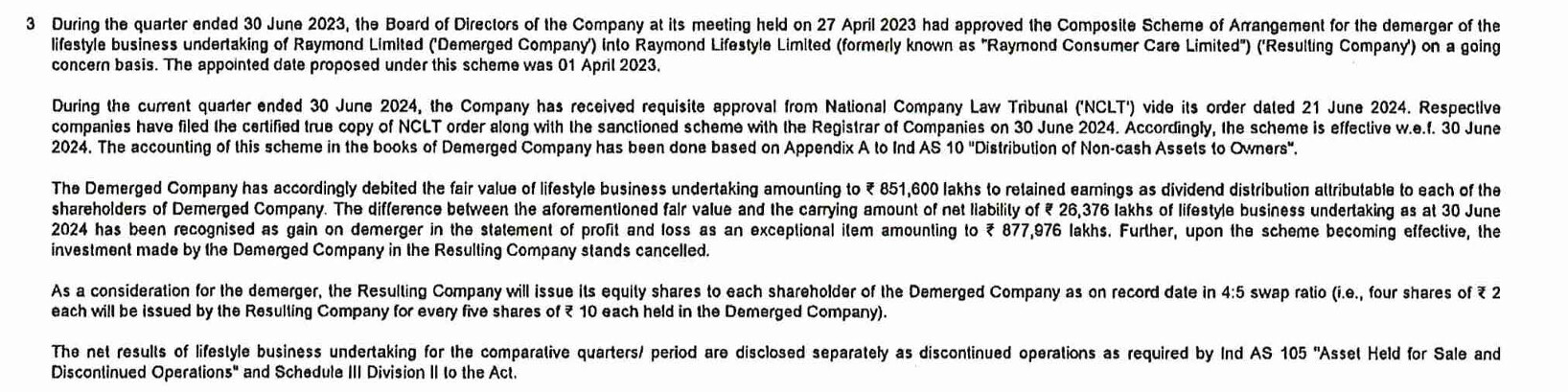

Has anyone analyzed today’s result, there is an exceptional gain of around 7000cr, which actually spiked the profit. However, following notes in the statements creates confusion that, Is it a notional adjustment or a real gain of 7000cr on the books. Excerpts from today’s result

Even after including the MPPL revenue this quarter there is only a marginal increment in the Q1FY25 revenue compared to the last quarter Q4FY24 (excluding MPPL).

Raymond Lifestyle Limited website is up.

Raymond Lifestyle Limited

2 Likes

Few new members in Raymond Lifestyle board

https://raymondlifestyle.com/uploads/Composition%20of%20Board%20of%20Directors.pdf

1 Like

Few of my takeaways from Q1 FY25 of Raymond

Raymond seems to be navigating a complex business environment with mixed results across segments. The real estate business is showing strong momentum, while the lifestyle segment faced headwinds. The engineering business performance was bolstered by the Maini Precision acquisition but saw some margin pressure. Overall, management appears confident about growth prospects in the latter half of FY25, banking on a robust wedding season and festive demand.

𝐒𝐭𝐫𝐚𝐭𝐞𝐠𝐢𝐜 𝐁𝐥𝐮𝐞𝐩𝐫𝐢𝐧𝐭:

The company is in the midst of significant restructuring, having completed the demerger of its lifestyle business and initiating the vertical demerger of its real estate arm. This signals a clear intent to create focused, independent entities that can chart their own growth trajectories. The acquisition of Maini Precision also indicates Raymond’s push into high-potential sectors like aerospace and defense.

𝐌𝐚𝐫𝐤𝐞𝐭 𝐃𝐲𝐧𝐚𝐦𝐢𝐜𝐬:

A key trend is Raymond’s shift towards an asset-light model, especially evident in its real estate business where it’s pursuing joint development agreements (JDAs). In the lifestyle segment, there’s a clear focus on expanding retail footprint and distribution reach. The company is also betting big on the ethnicwear market with its Ethnix brand.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐓𝐚𝐢𝐥𝐰𝐢𝐧𝐝𝐬:

The residential real estate market continues to show strong demand, particularly in the affordable luxury segment. In engineering, the auto ancillary and aerospace sectors are showing promising growth. The potential shift of garment manufacturing from Bangladesh to India could be a significant opportunity for Raymond’s garmenting business.

𝐈𝐧𝐝𝐮𝐬𝐭𝐫𝐲 𝐇𝐞𝐚𝐝𝐰𝐢𝐧𝐝𝐬:

The lifestyle business faced challenges due to inflationary pressures, unseasonable weather, and a muted wedding season in Q1. The engineering consumables segment is grappling with weak demand both domestically and in export markets.

𝐈𝐧𝐯𝐞𝐬𝐭𝐨𝐫/𝐀𝐧𝐚𝐥𝐲𝐬𝐭 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬:

There were questions about the sharp margin decline in the garmenting business despite revenue growth. Management attributed this to capacity ramp-up costs and adverse product mix but expressed confidence in margin recovery. Concerns about channel inventory in the lifestyle business were addressed, with management stating that secondary sales exceeded primary sales.

𝐂𝐨𝐦𝐩𝐞𝐭𝐢𝐭𝐢𝐯𝐞 𝐋𝐚𝐧𝐝𝐬𝐜𝐚𝐩𝐞:

Raymond’s integrated play from fabric to garments positions it uniquely in the textile and apparel space. In real estate, its brand equity and execution capabilities are helping it compete effectively in a crowded market.

𝐅𝐮𝐭𝐮𝐫𝐞 𝐏𝐫𝐨𝐣𝐞𝐜𝐭𝐢𝐨𝐧𝐬:

Management maintains a positive outlook for H2 FY25, expecting a strong wedding season to boost the lifestyle business. They’re targeting 20-25% year-on-year growth in booking value for the real estate segment. For the engineering business, mid to high-teens growth is projected.

𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐃𝐞𝐩𝐥𝐨𝐲𝐦𝐞𝐧𝐭:

Raymond is investing in capacity expansion for its garmenting business, having spent INR 200 crores. In real estate, the focus is on an asset-light model through JDAs. The company is also investing in marketing and branding, particularly for new store launches and the Ethnix brand.

𝐎𝐩𝐩𝐨𝐫𝐭𝐮𝐧𝐢𝐭𝐢𝐞𝐬 & 𝐑𝐢𝐬𝐤𝐬:

The Bangladesh situation presents a significant opportunity for the garmenting business. However, execution will be key. The real estate business has substantial growth potential but faces risks typical to the sector like regulatory changes and economic cycles. The lifestyle business needs to navigate changing consumer preferences and increasing competition.

𝐂𝐨𝐧𝐬𝐮𝐦𝐞𝐫 𝐏𝐮𝐥𝐬𝐞:

While Q1 saw muted consumer sentiment in the lifestyle segment due to various factors, management expects a revival in the latter half of the year driven by the wedding and festive seasons. In real estate, customer sentiment remains positive, especially for affordable luxury offerings.

Disclaimer: This is a general analysis and does not constitute financial advice.

7 Likes

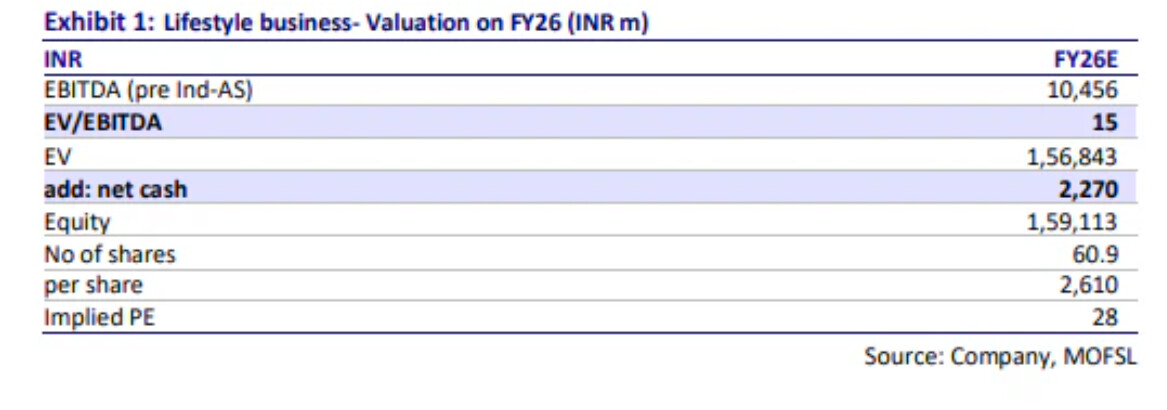

Raymond Lifestyle is expected to list in 2-3 weeks time. This division had an EBITDA of ~1150 crores last fiscal. While the margins are expected to improve as Ethinix brand grows, the overall revenue growth is nominal and not comparable with the likes of Trent, Aditya Birla Fashion etc (that sell multiple non-owned brands). We never know for sure as they seem to be focussing a lot in growth by increasing the garmenting capacity and adding some industry veterans to the board etc, the combined efforts of which might result in better topline growth.

Given this context, what is a reasonable valuation for Raymond Lifestyle in terms of EBITDA multiple?

Pls note that they are cash surplus but still may have working capital loans that might result in interest payments

3 Likes

on a lighter note, the rush you see in the pic is outside the shop, not inside ![]()

Analyst presentation for plant visit held at Vapi on 26th August.

Analyst Presentation

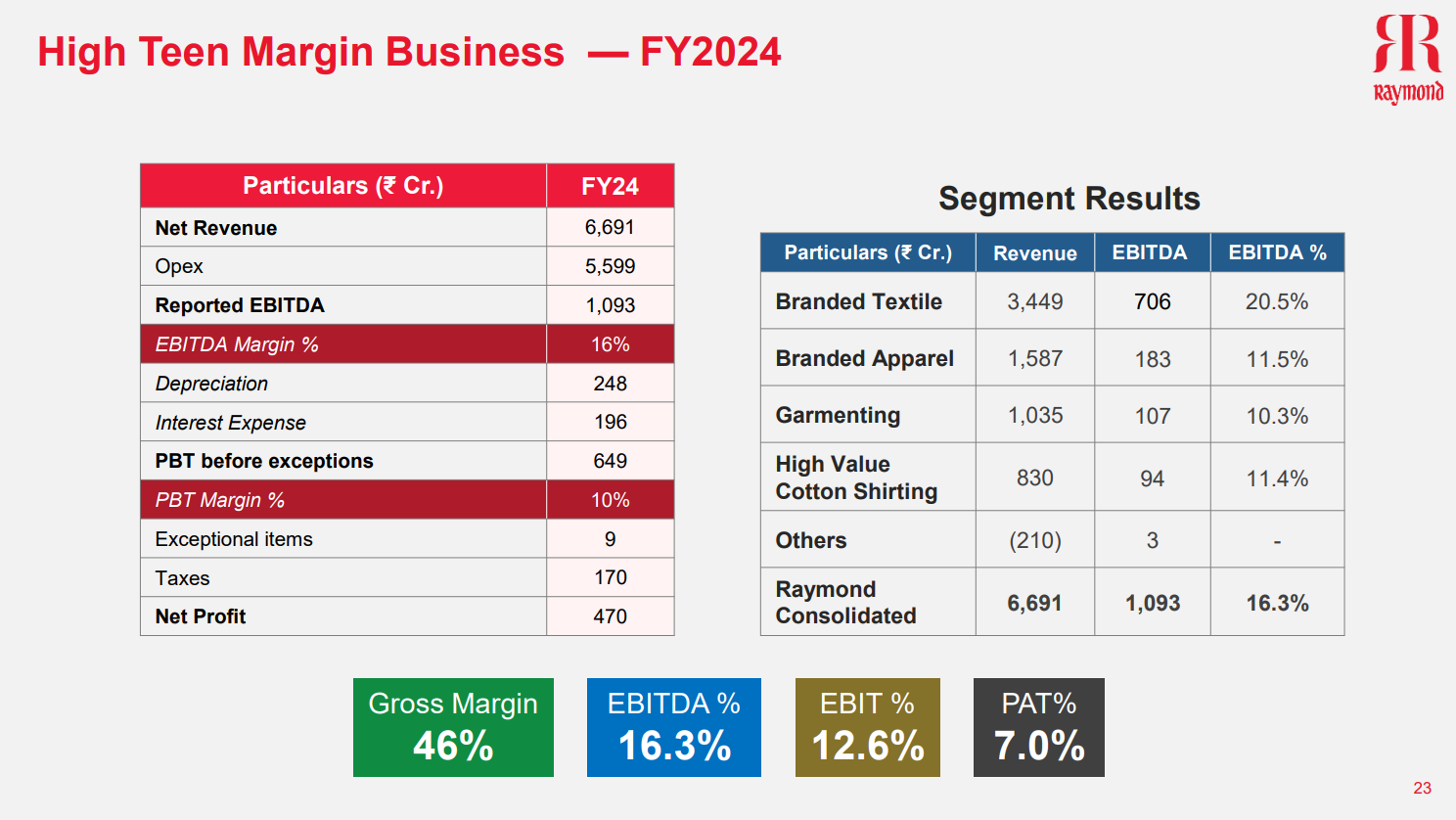

Financial Performance of Raymond Lifestyle for FY24

Net Cash Surplus at ₹227 Cr, Operational ROCE:31.7%, NWC Days:76 Days, Operational ROE:10.4%

- Explains the wedding and ceremonial part of the portfolio which is about 35-40% of revenue in detail, aims grow this part at 15% and to double ebitda by FY28

- Will add 650 stores mainly EBOs (300 for Ethnix) by FY27

- Details abouts Ethnix, SleepZ, Innerwear and Garmenting side of business

- Lists members of governance and senior management

1 Like