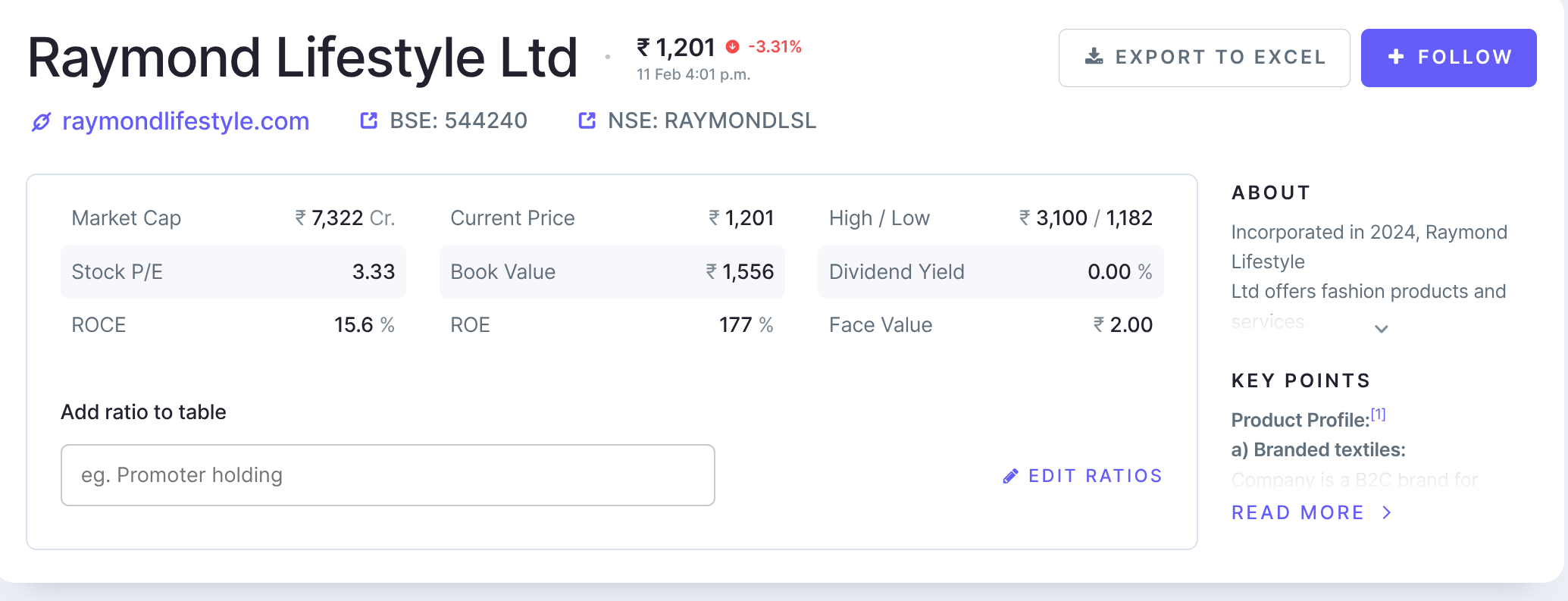

Hopefully, those worried about why Raymond Lifestyle was trading at such dismal multiple got their answers, now it’s trading on the higher end with EVEBIDTA of 51.x. Value might emerge now as it has started trading below Book value.

2 Likes

Cheap can always get cheaper. I have paid my tuition fees to the market for this learning. Management that doesn’t walk the talk is also not a good sign. Thankfully I had kept my allocation small waiting for the earnings trigger.

3 Likes

Are any reasons specified for the weak performance?

Concall is scheduled for today 4pm

.

One thing I noticed is that the stock is now trading below the book value. Any more downside doesnt look logically feasible though you never know.

The book value is close to 10,000 Crores. Does anyone know details of this calculation?

On Screener Book Value Per share at todays closing is 1556 and CMP was 1478.

And as you said total book value was close to 10,000Cr whereas the Current Market Cap is 9010 Crs.

Management has extended the FY28 EBITDA guidance of ₹2,200 Cr. by 12-18 months.

What to me is surprising is this interview 2.5 months into Q3 (December 16th) - very positive commentary and no hints of slowdown/demand weakness ![]()

2 Likes

It is due to 5300 crores of assets created which is mainly goodwill and intangible assets like brand value created at the time of demerger. It is not totally due to physical assets. This year’s annual report will provide more details.

Check this video at 50:00 min where it is explained.

5 Likes

That explains why the stock price dipped below the shown book value. If 5300Cr worth of intangibles created due to the demerger is excluded, the book value should come down to a little over 4000Cr while the company trades at a market Cap of 9000Cr. So the actual ratio should be around 1.5.

Also it is worth noting that these Intangibles will be amortized over subsequent periods which will have its own set of consequences on the Income Statement.

Any opinion on the valuation of the stock at current levels?

1 Like

I feel retail is a difficult business. Company is trying out lot of new things. They are expanding Ethix very fast. They are starting with Sleepz and Park Avenue Innerwears etc.

In retail though one can grow the overall topline by opening new stores, but important metrics to track are the - Ebitda margin at company level and store level, Inventory Management, Same store sale growth, Attractiveness of Business for Franchisee etc etc. For these the jury is still out, and not too convinced about the Company’s performance.

So we should wait and watch and track the performance before entering the stock.

4 Likes

+1 I think it’s still early days especially with the company expanding into a lot of new segments.

They have a good brand so that’s a plus point.

The main question is now on the Jockey can that walk the talk, do smart allocation and grow the business over the next few years?

Has anyone done any background research of the management based on their past experience and performance?

3 Likes

MOSF report on Raymond Life Style after Q3FY25 result.

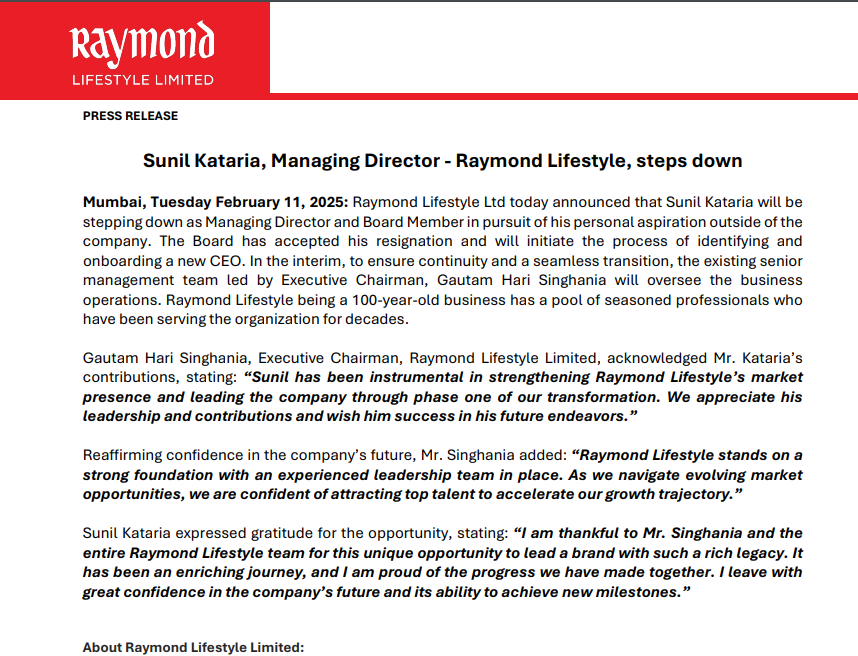

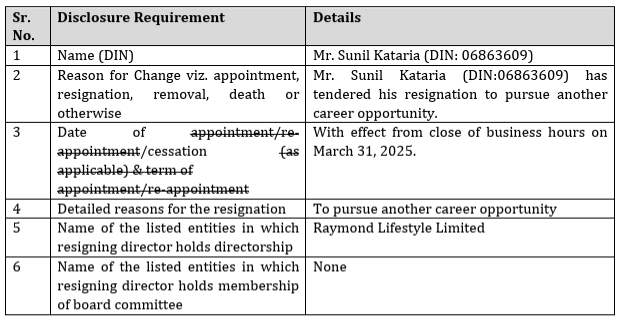

Sunil Kataria has resigned from the Board; in the interim, the senior management will be led by Gautam Singhania.

1 Like

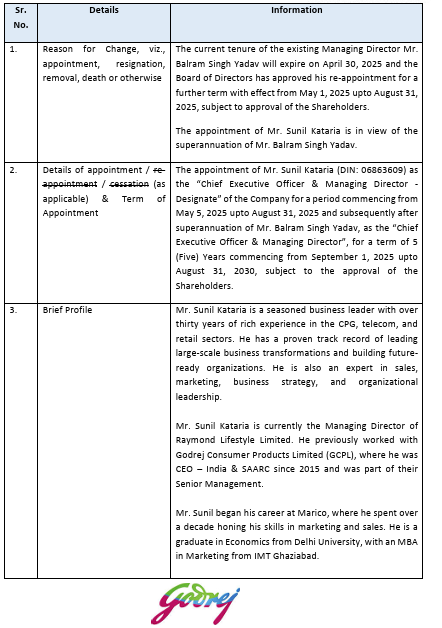

The outgoing MD sounded very positive about future prospects of Raymond Lifestyle and the strategy they had put in place in the Q3 results con call but is moving to Godrej Agrovet now within days. Has his views on RLL business changed so suddenly?

1 Like

Can anyone share more on how to interpret the data, keeping into consideration excluding goodwill, intangible assets and exceptional items one time profit of 2,059.

Screener shows book value at 1,556, the P/E looks depressed at 3.33 (I believe this is due to the one time exceptional item in profit of 2,059).

Anyone who’s good at reviewing the accounting, can you please help with reviewing the balance sheet and share your perspective on what’s the true value of the business ?

I think the market is still in price discovery for this stock.

It’s a retail chain, I think the best way to compare it would be with the likes of bata or even to vedant fashion to some extend .

Why I’d compare it more with bata :

-

The presence across country matches almost with bata.

-

Bata has been stagnant on topline front for last. 4 years , yet if we look at valuations it trades, that gives me alot of hope for this counter.

-

Both the brands are known for their product quality, and not popular amongst millennials but have a decent acceptance among old school guys.

On whichever parameter be PE or market cap to sales u compare it with likes of bata it’s at a significant discount.

2 Likes

Hi All,

If nothing else, RLL will soon be the poster child of ‘buying the dip’ memes. As of Valentine’s day 2025, I am standing at a ~40% unrealized loss. Haven’t sold a share till date. In fact, I am thinking of buying more the coming week. Here’s why:

-

The chance of a further 20-25% correction seems relatively low at this level for RLL.Valuations are depressed across the textile sectors with strong Cos like Vedant Fashions, Arvind etc. beaten blue and black. Seem to be the downcycle of this cyclical sector. Muted consumer spending is in the design of any economic cycle so no suprises

-

Talking of opportunity cost, I personally held decent cash since the last 3 months as I expected correction. Even If I didn’t, booking 40% loss on RLL and investing the rest 60% in a new stock (which I would naturally know less about) in a down market and expecting to make a profit is not something I am capable of.

-

Averaging at these levels seem prudent to me as probably when consumer spending improves in the next 3-4 quarters, I maybe able to book a small loss and get out. Or if prospects/fundamentals improve will be happy that I chose to stay the course.

-

@rahulbhardwaj19 mentioned about the one time gain of 2200 Cr which likely seem to be a combination of adjustments due to the demerger and a 100% dividend that was announced post the slump sale of the FMCG biz for ~2800 Cr. As part of the dividends, RLL also got a pie which came in as other income. I can only say for certain once the annual reports are announced.

-

Regarding the company trading at less than its book value that’s just optics. During the demerger, the company was valued higher than its net asset value; the difference of which was taken on the balance sheet as goodwill and intangibles. Goodwill = Purchase Consideration − Fair Value of Identifiable Net Assets. It was done probably to inflate the paper value of the business as it would get listed at a higher market cap and so that the Singhania’s could be a few 1000 Crs richer.

-

As of the latest available BS ending Sept. 30 2024, value of the goodwill & intangibles (G&I) was roughly 5200 Cr against a total asset side value 13600 Crs. Adjusting the asset side for the G&I, we get a value of 8400 Cr. If you remove the current and non-current liabilities of ~4100 Cr, you get 4300 crores of equity or book value. At current market cap of ~7000 cr, that’s roughly 1.7x P/BV.

-

With all that out of the way, lets revisit valuations. I look at valuations not just by PE but through a trinity of PE, ROCE (capital efficiency) and Growth. Here we go:

-

PE: Assuming full year sales of ₹6400 crores for FY25 (8.5% down vs. FY24) and assuming a stressed PAT margin of 4% (₹250 Crs); RLL will trade at a expected FY25 PE of 28. This is inclined towards attractive as we are assigning PE based on a bad year of sales and margins. In FY26 if the Co is able to clock 7000 Crs worth of revenue (same as FY 24) and slightly improved PAT of 5% then also, it would trade a forward FY26 PE of 20 which is very decent.

-

ROCE: We compute the ratio by using the following formula: EBIT/Invested Capital where Invested Capital = Total Assets - Current Liabilities. Note we are using the latest available BS as of 30th Sept’24 (Q2) where receivables and inventory are seasonally high to cater to the upcoming festive and wedding season. The same figure has come down as of Q3.

-

EBIT of ₹429 crore compared to invested capital of ₹5350 (adj. for G&I) Cr gives us a ROCE of 8%. Again, the EBIT figure has been taken as of current year of stressed margins.

-

Is there any scope of improving ROCE? The company plans to expand via opening 600+ EBO stores. EBO stores are primarily company owned and would thus require more capex which would hurt ROCE. However one off costs such as employee training, freight costs and store expansions are likely to moderate. The management also mentioned that they are seeing better signs from in ground retailers with healthy orders.

-

Growth: The takeoff in Ethnix does not look that optimistic. It has been 24 months since it has been launched and the Co expects to do 100 crores of annual sales (vs. total sales of ~7k crores). Sleep & innerwear are too small to contribute anything material. Management itself stated that branded Textile will be a slow growing segment.

-

Growth is likely to come from garmenting via new customer acquistions in UK in the premium segment from customers such as PVS & Tommy (Q3 FY25 concall). Continuous increase in retail stores plus enhanced marketing spends in brands such as Park Avenue, Colur Plus etc. can lead to incremental revenue. But honestly these things are hard to crack and put a number on so I will leave it at that.

Final conclusion: I’ll look to average downwards this week. This is NOT an investment advice, just perspective from a fellow VP er. My opinions might change anytime and I would not be obliged to update the same here. So please do your research.

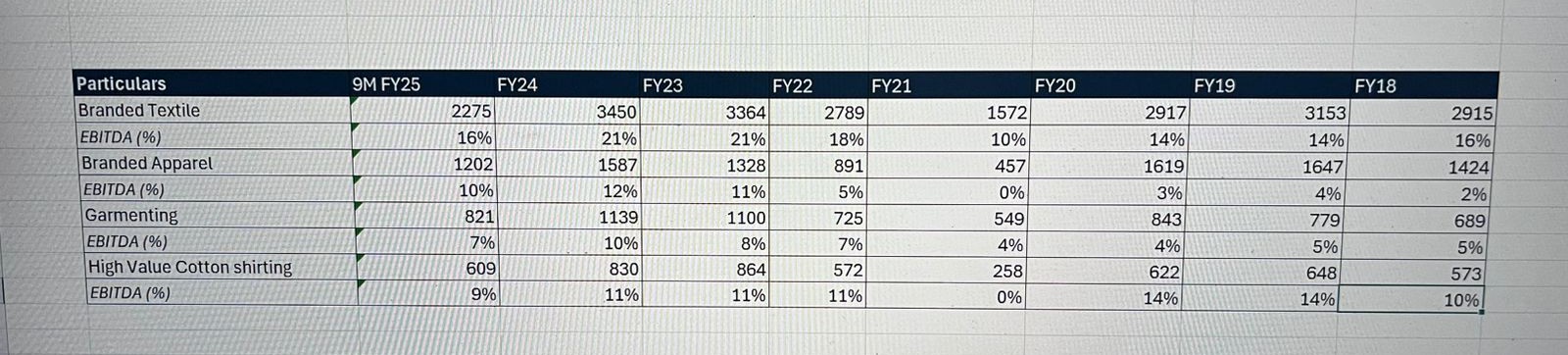

In closing here’s a snapshot of the historical revenue & EBITDA margins of the company just for check:

3 Likes

Q3 numbers for some competitors

- ABFRL Lifestyle Brands segment (Van Heusen, Louis Philippe, Allen Solly, Peter England) grew 0% yoy in Q3. Retail LTL at 12%. EBITDA margin grew by 40bps to 19.6%.

Total proposed ABLFL (lifestyle brands + innerwear + Reebok + American Eagle) grew 1% in Q3 and EBITDA margin increased by 90bps to 16.5%.

Tasva (comparable ethnic brand, slightly more premium) grew 50% yoy in Q3 and has achieved positive EBITDA. It has 67 stores currently. Retail LTL at 18%. - Arvind Fashions (USPA, Flying Machine, Arrow, Calvin Klein and Tommy Hilfiger) grew 7% yoy in Q3. They mentioned adjacent categories like womenswear driving growth (womenswear doubled yoy). Retail LTL of 11%. EBITDA margin increased by 110bps to 14.5%.

- Credo Brands Marketing (Mufti) grew 3.6% yoy in Q3. EBITDA margin increased by 230 bps to 30.6%.

These are the only listed competitors which are in similar ASP in mens apparel sector (Many different value retailers have performed much better).

Raymond Branded Apparel segment grew by 4.8% yoy in Q3. LTL at mid single digits. EBITDA margins dropped by 430bps to 9.6%.

So, on the revenue front every brand has struggled and talks about urban demand slowdown but they are able to improve their margins while Raymond is investing into ethnix and new segments which is hurting margins currently.

All three competitor’s market caps have also corrected quite significantly.

5 Likes

While poor consumer demand, operating leverage not kicking in etc are said to be some common reasons for the lacklustre performance, what could be the reason for decline in yoy gross margin . The COGS has increased by about 19% while the revenue remains flat. I checked for ABFRL and there is no such phenomenon.

1 Like