Sorry, I don’t fully agree with the above assumption of Raymond tagged as wedding/occasion brand. Yes they are the largest in that segment, but they do have shirts and trousers for formal and casual wear and now they are also stepping into home furnishing, sleepwear, inner wear. Link

2 Likes

True. They kind of want to be niche with their own (and limited number of) brands.

Also, Raymond brands caters mostly to Men. Not catering to Women is a big loss of business opportunities in this segment.

2 Likes

Let us look at what the companies have delivered so far.

- Sales for TRENT has grown by 46 % in the last 1 financial year (FY23 to FY24) and 36% CAGR in the last 5 years (FY-19 TO FY24). PAT has gone up by 15 times in the last 5 years.

The segments that are now with RLL has grown its sales by 6.9% in the last FY and 2.3% CAGR in the last 5 years under the same Chairman . It is aiming to grow its sales by about 15% and profits by about 18% annually in the next three years.

Management can underestimate growth and the company can probably grow above this. But as of now I do not see any reason to bet on something like that. The best I would hope is for the business to do as well as the management is telling it would and use its new found freedom to pursue a path of double digit growth consistently.

Surely as mentioned earlier RLL has to earn its multiple.

-

There is no comparison on governance and management quality of both the companies. The multiple for TRENT obviously includes the ownership by TATAs and the management oversight that brings with it. One should pay a premium for TRENT on this factor alone.

-

The number of stores may not be a good metric as the size and the format of the stores vary. But if a crude comparison is required then TRENT is doing close to 14 crore plus sales per store while RLL is only doing just above 4 crores sales per store across its 1590 outlets, many of which I would assume as mature stores.

-

More importantly TRENT is a young company with a fresh idea and after several years of iteration their business-model & store model especially Zudio clicked at the store level . They have found the playbook and is ready to be scaled up further which the market should be pricing in. I also believe that the market is enthusiastically pricing in the possible success of its other ventures such as supermarket. Raymond on the other hand has a promise of delivering 15% cagr sales growth and hopefully they do that. One can only hope that things turn out positive for RLL after the bad quarters post demerger.

Personally for me Raymond is about suits or at best textiles. I do not understand how a single brand Raymond can be associated with a price range of 300 Rs to 15000 Rs as he is saying in one of the video.The legacy the brands carry can also be a limiting factor. One has to spent money on building the new brand in new categories if they are going to do it under a new brand name.

My guess is that TRENT would trade at a lower multiples in the coming years and my hope is that Raymond would recover from the last couple of quarters and atleast trade at a better multiples in the coming years.

Disclosure: I am invested in Raymond Lifestyle and I would obviously like to get a good return on the bet. Also invested in Trent but at a very small level compared to that in Raymond Lifestyle.

7 Likes

I agree with the views on the comparison being made between Trent & RLL as in they are somewhat different.

Having said that, RLL’s closest peer will be Vedant Faishons at least when it comes to Ethnix’s competition with Manyavar. Even here, RLL is much more than only Ethnix. Now if we compare RLL and Vedant, RLL is extremely cheap.

Other competition could be between RLL and Aditya Birla fashion when it comes to men formal and semi formal wear segment. Here as well, RLL is much better in my view. ABFRL is still making losses every quarter. Again, RLL is much beyond what ABFRL is.

They are now entering into sleepwear segment where I think Page has dominance but it’s extremely fragmented market.

I think Q3 results will be extremely important. If they give very poor or stagnant results in this quarter, I will need to think for exit.

3 Likes

As much as I like this forum, sometimes the core real-life products of companies get overlooked. The reason Zudio (Trent) or WestSide (Trent) are famous (I say this as a 21 year old) is that they refresh their entire offering within a month according to latest trends and appeal to the real spenders - the teenagers of this decade. I have been shopping for 90% of my needs at these two stores. During the oversized clothes trend, they capitalized on it. Now during the “quiet luxury” trend they seem to be doing pretty good too. And lets not even get into the female side of it. The design of their stores with the music are also great appeals to repeated footfall. Experience of Zara/Armani with the price of the GST you would pay on a Zara/Armani purchase.

After hearing some much awaited discussion on Raymond Lifestyle, I decided to actually visit their website to see for myself if they could entice me to buy something from their website.

Observation 1: Once you press the Categories drop-down, you won’t even be able to navigate to the categories before the drop-down disappears. (God knows how much sales must have been lost due to this).

Observation 2: Once I somehow made it to the exhibit of clothes in Park Avenue, all I see is out-dated 2015 colorful design polo t-shirt styles that even uncles do not choose to wear anymore. And in their sleep-wear segment, they just have the same Zudio offering for 4x the prices.

Observation 3: Visited their flagship store in South Mumbai on a weekend, I was just one of the ten customers in the 4 floor store. Seeing shirts for 2,999+ which I would get for 699 elsewhere.

Conclusion: Will continue holding and not accumulate more until real on-ground changes are shown, not just the blabbering of random expectations and numbers by the management.

Disc: Holding Raymond Lifestyle since delisting.

19 Likes

It is astonishing to me that someone would compare Trent and RLL. Trent is only EBO. It has three major brands: Westside, Zudio, and Star (leaving aside ZARA).

RLL should be compared to an ABFRL or Arvind. They are in the business of creating a brand and selling it to EBO and MBO. Also, let’s be frank: apart from Raymond, they don’t have a Tier-1 brand recall. And Raymond, no one under age 40 would buy except for a Suit.

Ethnix has to be seen in terms of execution. The only positive I see is the garment story.

6 Likes

Agree with the discussion, will watch out for the Q3 and Q4 numbers. Lets see if they are able to make some real progress.

2 Likes

Once the genie is out of the bottle, it’s very hard to put it back. I am guilty of comparing the sales per store of the two companies, but that was only to convey that there’s little point in comparing the valuation of two companies based solely on the number of stores.

I would like to add two more points

-

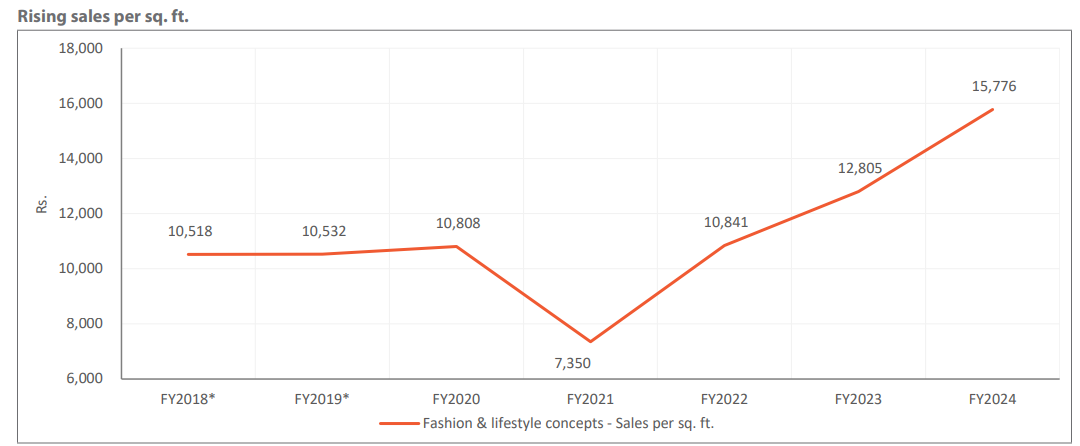

Sales per square foot would have been a good measure. The only catch is that there are additional 4,200+ multibrand outlets, which I assume, would have significantly contributed to RLL’s actual sales. It would be great if sales per sq ft figures are figured out separately for each format.

-

I believe the reinvestment needs are irrelevant on a per sq. ft basis. RLL, as mentioned in the forum, follows a FOFO model, and once RLL figures out what works in the franchise arrangement, it is the franchise owner who has to make the investment. Again, as far as I understand, Zudio operates on a FOCO model, where the investment is made by the franchise owner, not the company. This means once you have established the right model or playbook in place, the reinvestment needs for scaling up cannot be that high.

For me, the raw individual observations, shared here in a context, are the most interesting part. If we left all the scuttlebutt to the professionals, I would have just read some of the analyst reports, taken them at face value, and stopped at that. At least here we are clear that these are anecdotal observations.

1 Like

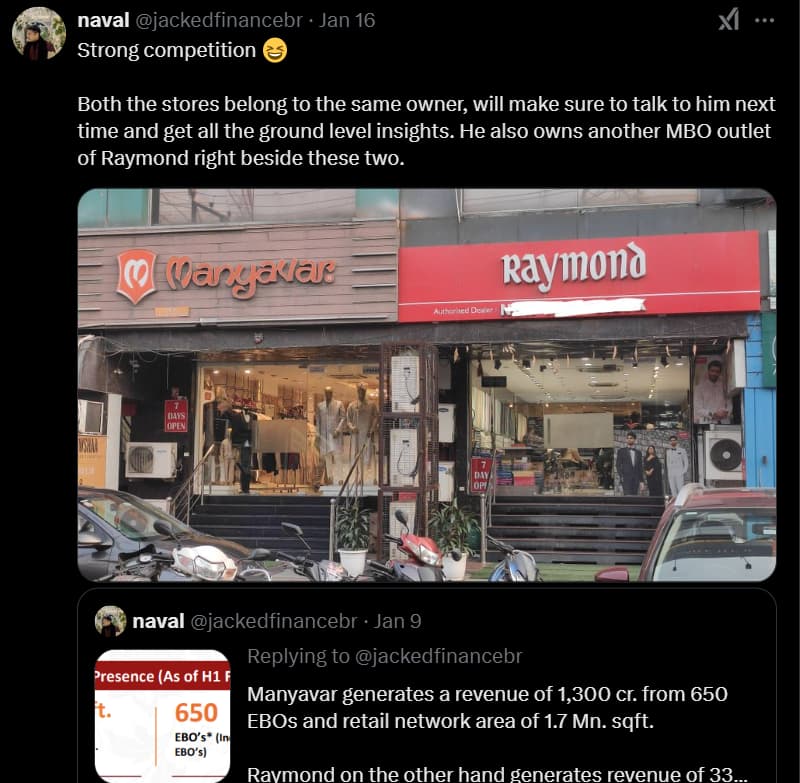

Shared an interesting insight around EBO store counts and their revenue comparison b/w Raymond, Manyavar and Trent.

“For a brand to get pan India noticed a brand must have atleast 200-300 stores.”

Ethnix’ revenue/sqft. is low as I had already mentioned earlier that 80% of the sales for Ethnix happen during wedding season peak and many of the Ethnix stores opened in the last one year did not experience peak wedding season until Oct. 2024.

Considering capex/sqft. is almost half of Trent stores, revenue/sqft. of Raymond EBOs is actually good.

Trent’s consol. revenue/sqft. was a breakthrough was a result of expansion even during covid and consumer spending spree post covid.

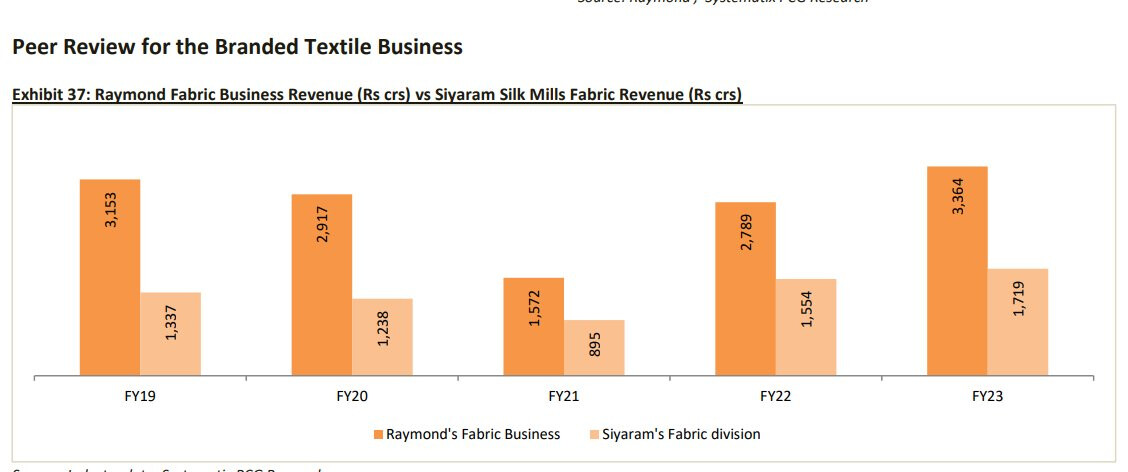

Also for comparison of Branded Textile segment, Raymond’s revenue is twice of its peer Siyaram Silk.

Disc. - invested.

3 Likes

Who bought after demerger are not getting benefitted. Looks like its tough time Inspite of tailwinds in this Q3.

Even Vedant Fashions (YOY) growth is not good!

Bottom line remain stressed as company is planning for more stores opening. New stores opening might not be EBIT positive initially.

2 Likes

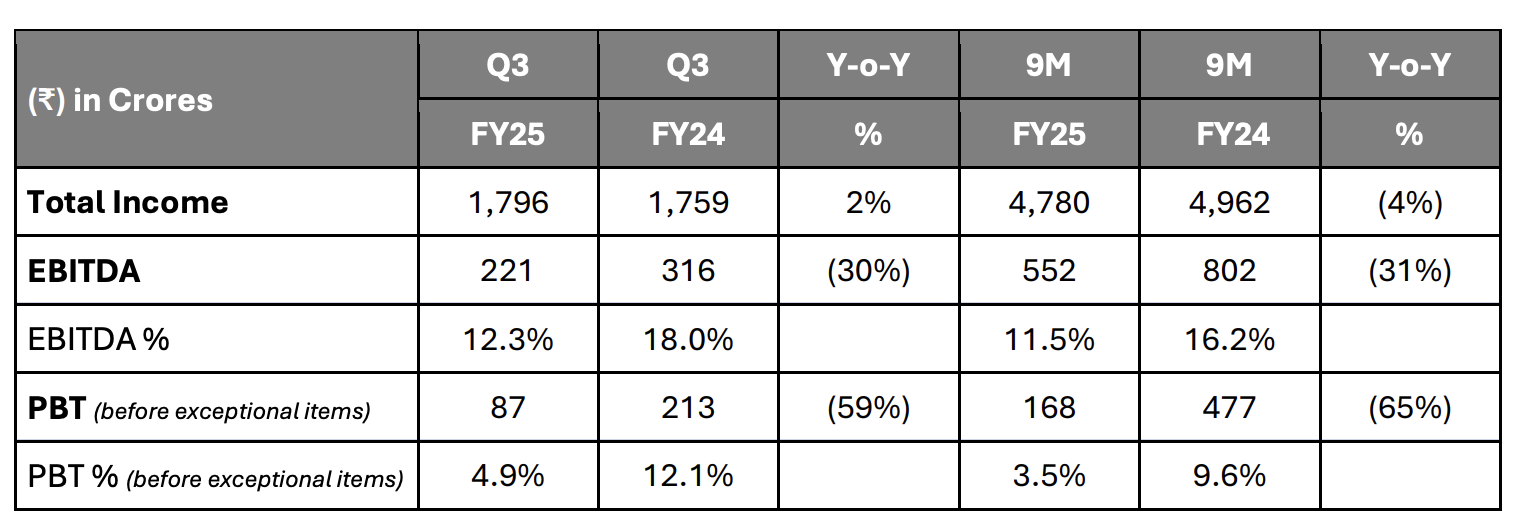

What a poor set of earnings despite Q3 being the peak wedding season. I wonder what excuse management will give this time? EBITDA fell 30% YoY.

Revenue Performance:

- Overall revenue grew by 2% YoY.

- The 9-month revenue declined by 4% (₹4,780 Cr vs. ₹4,962 Cr in 9M FY24).

- Only growth from Garmenting (+18% YoY), rest all categories were either flat or showed degrowth.

Segment Performance:

- Branded Textile (-6% YoY revenue): ₹856 Cr; margins impacted due to lower demand.

- Branded Apparel (+5% YoY revenue): ₹458 Cr; margins impacted by store expansion costs.

- Garmenting (+18% YoY revenue): ₹309 Cr; margin hit due to adverse sales mix and higher costs.

- Shirting (-6% YoY revenue): ₹201 Cr; demand slowdown affected performance.

Q3 FY2025 earnings result -

fb605445-33a2-4d57-8d42-7f018c264d21.pdf (5.8 MB)

2 Likes

Inspite of Q3 being a wedding season, the general market conditions are still not very good as also can be seen from Vedant Fashion’s results. Manyavar is exclusively for marriage occasions and they have grown below 10% YoY. Raymond Lifestyle has has major impact in Q3 on textile business, which is not dependent on festivities much.

We need to see when the general market conditions improve. If topline grows, margins will be much better.

1 Like

Arvind Ltd textile segment (woven) grew 6% YoY but mostly it is B2C business and largely exports. Vedant Fashions has grown only 7.8% in this wedding heavy quarter and 1.5% for the 9M FY25.

Need to wait for results of competitors like Arvind Fashions and ABFRL to really see how was the relative performance on the apparel side.

I think retail as a business is a very tough space to crack. Had shared a few of my thoughts on ABFRL thread also. Now I don’t track these companies primarily because I’ve a few biases against them from the eyes of a shareholder:

The customer loyalty isn’t the same as it used to be

Same store growth for all these companies is very underwhelming

Heavy dependence on wedding season & festive. Markdowns have become a normal scenario. Customer is spoilt for choice

Emergence of so many brands both offline & D2C

Expansion might become a challenge through franchisee route. I can be wrong but don’t think franchisee profitability is as lucrative now again because of business getting shared

A capital intensive business with store capex & inventory a big chunk & fluctuating consumer demand a big threat

Having said that value retailers have given stellar returns & might continue to do so basis performance primarily banking on the trend moving from unorganised to organised & scope of markets wherein they can operate with low rentals & the growing customer base vis a vis income group & geography

Now, these are some of the things that come to my mind towards these business & I could be really wrong & biased but these questions need to be asked of management or built into thesis as to if something differentiates these companies.

6 Likes

I exited today in huge loss. Pathetic results. Marriage season was flooded in Q3 & despite that muted growth YoY & QoQ also.

Will shift to better stocks available as reasonable valuation to cover my loss.

I also exited with loss today. Apart from bad results (which could be because of overall economic situation), what I particularly did not like was management wasn’t very transparent. They were fairly positive about H2 in Q2 con call, while they would have already seen the trend for more than a month in Q3 by then. Though the wedding season hadn’t started when they held Q2 con call, they mentioned October has seen good growth - with this kind of result, it is hard to believe.

The lesson learnt is to do some ground level checks (especially in consumer space where it is easier to do) to get some sense, regardless of what the management says. Raymond shops always seemed empty in Bengaluru all through Q3.

5 Likes

You’re very much right that the management was being very optimistic about growth prospects. I should have definitely done some ground level checks when I had the chance ![]()

3 Likes

This is what I conveyed last month. Result turns out the same.

1 Like

Hopefully, those worried about why Raymond Lifestyle was trading at such dismal multiple got their answers, now it’s trading on the higher end with EVEBIDTA of 51.x. Value might emerge now as it has started trading below Book value.

2 Likes