This thread offers many valuable lessons. While I haven’t invested in or tracked Raymond Lifestyle, my curiosity was piqued when I saw it was the 6th biggest loser.

One key takeaway is that we often put too much emphasis on conviction. Many VP friends in our group have invested heavily in RL, believing strongly in its potential. However, the lesson here is that conviction is important, but as the saying goes, “No one knows beyond a certain point.”

Instead of endlessly averaging down, it’s wiser to let the market decide once a significant amount has already been allocated to a stock. Thanks for valuable lession in my investment journey.

Valuation seems compelling but where the growth will come from?

As highlighted in the earlier post, young don’t associate with the brand. Relying solely on Garmenting for growth won’t move the needle much.

Comparatively,

Arvind fashions has good brands.

ABFRL has a very vast portfolio of brands, retails chains, and big in ethnic.

Wouldn’t it be prudent to invest in these stocks in the market downturn as compared to the Raymond Lifestyle?

The reason share price got beaten up was that management promised great Q3, delivered a poor one, leaving question marks on execution, brand affinity (too many choices and does raymond appeal to young?) and transparency.

While they are adding stores, most of the times when I drove past the Raymod stores in Bengaluru, they have been empty. These investments are expected to pay over long term, however I wonder if the current generation finds Raymond appealing at all.

With change in management I would monitor business performance over next few quarters.

disc - no holdings right now, booked loss after Q3.

Same argument could be made for Bata, Relaxo, Blackberrys etc.

The point is they don’t have to cater to the milenials, as milenials move up the age group, portion of that brands like above mentioned will find its audience in them.

Plus think tanks in a company have to address the gaps in terms of target audience if any and they will have to make a catagory to cater to them( as is what bata atleast tried to do in 2018-19, campaign with sushant singh and Kriti senon) I don’t assume over the years raymonds management would not expand the product portfolio for milenials, atleast they will try, that’s my sense.

Execution for all retail apparel brands have been negative to flatish Q3, unless it’s a disrupter in the market like the likes of trent, and v2R in value retail and zara & H&Ms in aspirational catagory.

I don’t expect the company to be a disrupter or give a tearaway topline and bottomline, but they will grow in line with GDP , I hope they do slightly better.

Valuations don’t give comfort in going into dirupters at the moment coz market is discounting their growth for 3-4 years in advance.

They can’t grow at 50%s for next 3 years is my sense there will be saturation, and when that does their multiples will crash.

That’s a slight comfort here, expectations been low, so are the valuations, if it slightly grown better than the GDP in case of raymonds you might see multiple expansions.

One thing that doesn’t meet the eye, is why do they have 9k cr as reserves in their balance sheet. That’s 1.4 times their marketcap.

And yet debt of almost 1.5k cr.

If they have such cash surplus, why debt then?

If anyone has better understanding or details about that would appreciate the inputs

The reserves and surplus in the balance sheet simply reflect the profits earned and retained by the company till date. It does not mean the company has 9,000 cr. of cash in the bank. This is the profit that has been earned in the past and already plowed back into the business.

Yesterday, I completely exited my position from Raymond Lifestyle Ltd (RLL) with a ~48%loss. RLL was a high conviction bet which in the end caused the highest damage.

I describe high conviction bets as one with potentially large upsides and low downsides. A halving investment humbled that description. My last update on 17th Feb’24 concluded with me buying more of the stock. So what changed in little over a month?

Quite a bit, actually. Some external stuff which I couldn’t anticipate/ control:

Resignation of Top Mgt: The CEO and CBO both resigned in early February. Restructurings like internal elevation of few personnels to key positions and roping in a new CBO felt like plugging gaps. An attrition in management (especially when they are tendering resignations themselves) doesn’t bode well and leaves an uncertain strategy forward.

Encumberances of shares: Promoter co,J K Investors recently pledged upto ~8.3% of RLL shares. A creation of pledge by the promoter does not necessarily mean financial distress or a lack of confidence in the company’s prospects. However, the market views this negatively.

The Textile sector: has been beaten blue & black, left, right and center. Quality names like Vedant Fashions, Arvind Ltd, Trent and Page Industries has seen massive declines since Jan’25. The sentiment was evident when last weeks’ long market rally could hardly lift their prices or my spirit.

Where I could have done better:

Optically low valuations: I invested in RLL in late Nov’24, anticipating a demerger play where there is indiscrimanate selling by major institutions in the beginning, only for the stock to rise up within a few months. This didn’t play out. I should have exited then but I figured the stock was trading too cheap.

I attributed the FY25 earnings to a few depressed quarters and calculated earnings multiples with FY24 figures, thinking I was being conservative. Little did I know then, that FY24 was a period when the company enjoyed the best EBITDA margins in its recent history and such margins were unlikely to sustain. This high margins made the valuations appear a little cheaper than they actually were.

Lack of Primary Research: I was too fixated on the numbers and the financials and overlooked the product research. I recently revisited that. Raymond is a legacy brand with old designs and printed shirts priced at premium prices (₹2000 and above). Very few people wear tailored shirts and mostly people stitch suits for weddings and all which Ire in the range of ₹18k to ₹20k. Branding which is the bread & butter of such cos is clearly not there. Most of the times when I drove past the TRS stores in Hyderabad or visited in malls, they have been empty. Same with Ethnix. Also, speaking to young adults it seems they simply don’t associate or even heard of brands like Color Plus, Parx & Park Avenue.

The brand really some fresh breath of life, some refreshing to make it appealing to Gen Z, otherwise they’ll end up writing off those intangibles in Balance sheet and investors will be left holding the bag.

Disc: 7% of portfolio. Holding and hoping for some sign of turnaround

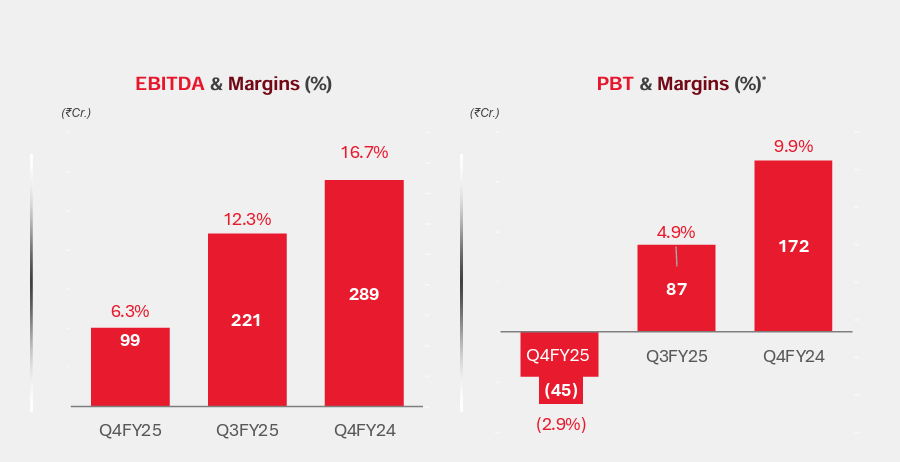

Company’s fixed costs seem to be high, hence profitability is proportionate to revenue. The results are not good obviously but I think it’s still to do with the lull in the market / sector. Last week, Vedant Fashions too reported a (slightly) negative YoY growth. Once / whenever, the sector as a whole gets better, results would reflect the same I guess

(Blaming ransomware attack on IT systems for revenue shortfall is funny though)

A disastrous set but not surprising given how other fashion retailers leave aside value retail have been doing. Plus add to that so many senior management exits & this was never going to take off.

I might have a biased view but these legacy retail companies need to come up with sharper strategies to have meaningful share that’s also supposed to be profitable.

Everyone has followed the same template of Ethincs, innerwear, sleepwear, activewear as the next big bets for their groups with their core business/ brands no longer commanding same growth & market share they used to.

There’s hardly any call to action for loyalty, except the old world loyalty points & exclusive preview sales.

The full price business rests on same levers as wedding dates, winter wear demand etc.

All in all brand salience has gone for a toss. It’s almost like similar stores, similar merchandise & to top it similar service levels in stores.

Overall, footfalls & final buy becomes a combination of exciting store windows, overall discounts offline & exclusively discounts online.

Until & unless, the big players come up with a new playbook apart from category extensions & acquiring brands, this would be a story of trying to grow topline at cost of bottom line because of new categories & brands & discounting or a stagnating topline to manage bottom line via lesser discounts & more full price sale

Disc: Do not hold any company from ABFRL, Raymond, Arvind, etc set of lifestyle retail companies.