Given a lot has been already shared about the Co’s profile and recent prospects, I’d like to share on three things: Competition, Risks & Valuations

Competition

Before talking about competition, I would insist the reader to spend 5 mins on the Co’s website to understand their various products. If you don’t want to that’s fine; do check it out later.

Rategain competes in a robust marketplace with several key players such as OTA Insight, Fornova, TravelClick, SiteMinder, and DerbySoft. Each of these competitors operates in various segments like Data as a Service (DaaS), Distribution, and Marketing Technology (MarTech).

As seen from the above chart, what sets Rategain apart is its integrated coverage of all the segments combined with trust and scale. This enables Rategain to leverage vast amounts of data from different touchpoints in various parts of the value chain in two ways:

- First, this extensive data collection enables more informed and effective decision-making, enhancing product development and customer service.

- Second, this wide-ranging presence facilitates cross-selling opportunities, allowing Rategain to offer bundled solutions that are not possible for competitors who specialize in narrower fields.

All of this sounds good on paper!

Given Rategain competes globally with other providers we snooped around a bit to compare how does it fare against its competitors. We came across a report by Hotel Tech. Hotel Tech ranks each product within categories with a proprietary ranking algorithm, the HT Score. The linked article details their robust rating system which we understood to be highly indicative of best-in-class experience and user appeal. (The links for these reports are attached in the article below, I am getting an error in linking it here.)

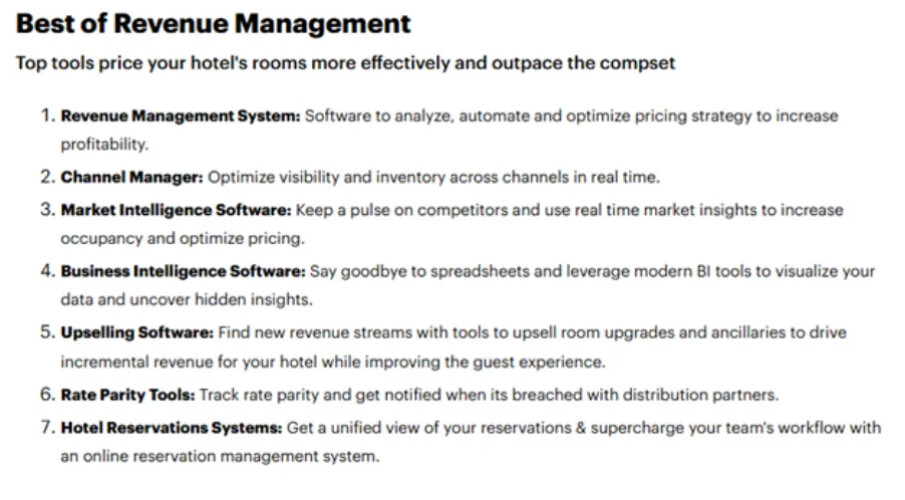

Hotel Tech ranks each product in categories such as: Operations, Revenue Management, Guest Experience, Marketing, Meetings & Events, Vacation Rentals, Food & Beverage, HR & Staffing etc.

Within which Rategain’s category include Revenue Management and Marketing.

Revenue Management itself is sub-divided into various functions which are given in the below screenshot:

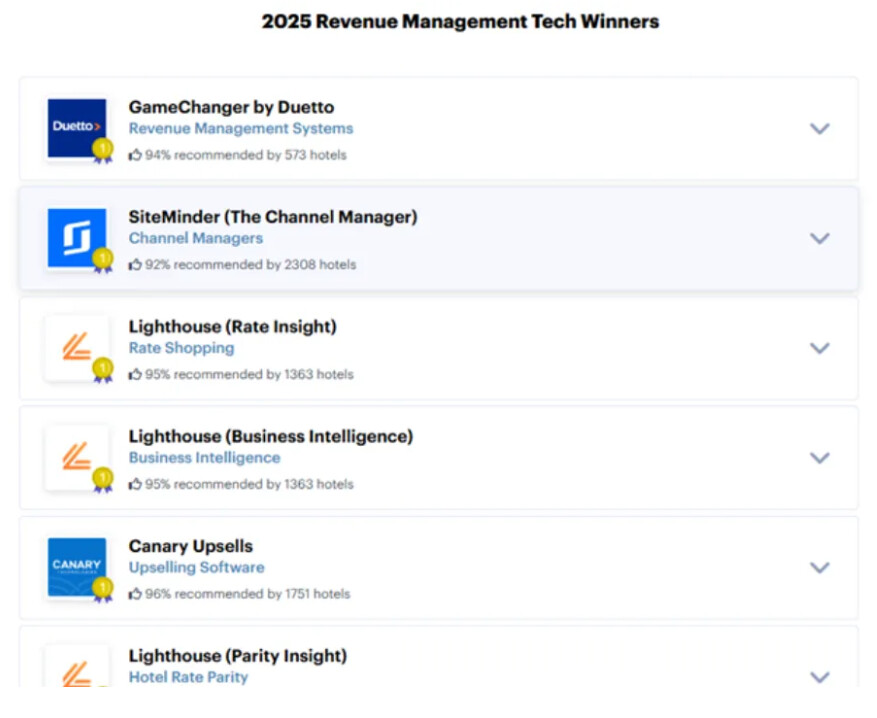

The winners for 2025 within each sub-category is as below (Rategain doesn’t feature in any):

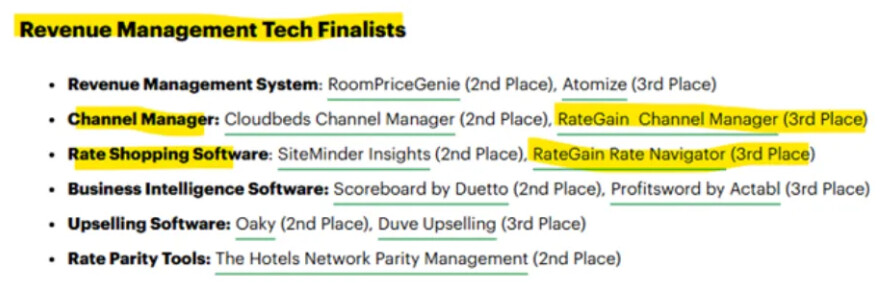

However, it does grab 3rd place amongst the best Channel Manager and Rate Shopping Software category.

In 2024, the Co had a similar rating finishing runners up in the Channel Manager and Rate Shopping segment within the Revenue Management category, with no representation in the marketing segment as winner or finalist. Help yourself with the 2024 rankings.

However, the Co ranked amongst the top 10 companies (10th and 9th) in the 2024 and 2025 respectively Hotelier’s Choice Award.

In short, this means Rategain faces excessive competition from global players like Light House and SiteMinder among others in both the revenue management and marketing segments. They are quite far from the top players, and this should be indicative of keeping tempered expectations in the Co’s revenue growth.

In India, a notable competitor within this segment is STAAH Tech. Find the Co’s website here .

The Risks

While sectoral tailwinds, less cyclicality compared to other travel businesses, geographic diversification, integrated platform, the travel industry’s push towards data and digitization & scope for a strong acquisition etc. make a good case for Rategain, we are more inclined towards the risks.

The Co’s share price has seen a stark decline in share price in last 6 months with price falling from ₹750-ish levels to CMP of ₹430.

This recent fall in price is due to quite a few reasons:

- Single digit revenue growth to the tune of 6-8% expected for FY26.

- Huge investments in sales and marketing can keep pressure on the margin in the near term

- A falling LTV to CAC ratio since 2023 attributed to lack of winning any big clients in the last year.

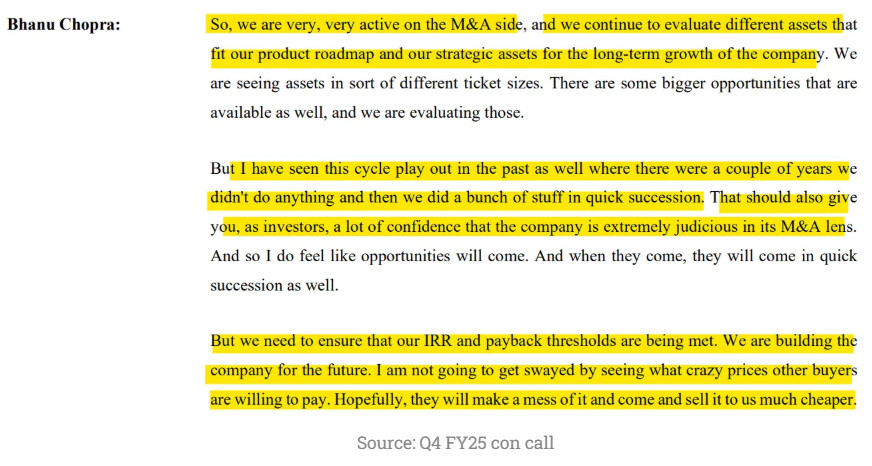

- Since its QIP in Nov 2023, the Co hasn’t been able to materialize any acquisition targets stating its reluctance to overpay for any acquisitions.

- Management also indicated that their distribution business will witness decline in revenues for the coming quarters. This partly due to wind up of one of the sub-brands of a large OTA and also due to repricing of legacy contracts in DHISCO.

Apart from the above, the Co also faces other significant risks such as:

-

Economic Slowdowns: Rategain’s revenue is closely tied to the health of the global economy, particularly the travel and hospitality sectors. An economic downturn can lead to decreased consumer spending on travel, reduced hotel stays, and overall lower demand for travel services.This is unavoidable as economic downturns are neither predictable nor avoidable.

-

Geographical concentration: While Rategain caters to customer’s globally, more than half of its revenues are from North America. Any economic slowdown, geo-political tension or internal political crisis can lead to reduced demand for the Co’s services.All that said, we do find it encouraging that the Co’s concentration in North America has been steadily coming down from 65% of revenues in FY21 to 54% in FY25.

-

Competition: As outlined earlier, the Co faces strong competition against various global players across many categories. Clients changing ships from Rategain to its rivals or competitors coming up with innovative products can derail Rategain’s future revenues.While Rategain faces a deluge of rivals, its products still stand out given its integrated platform and ability to process and analyze large volumes and data in real time continues to be a key differentiator.

-

The AI-angle: We are currently in the 1960’s of the AI revolution. In the years and decades to come we will likely see seismic shifts in various industries of the world. The travel sector won’t be an exception. The Co’s adaptability and edge to constantly innovate and launch new products would be a key monitorable.Amongst the many interviews and con calls, we skimmed through a recurrent theme was a commitment to being an AI-first company. In such spirits, the Co recently launched VIVA, an AI voice agent designed to help hotels convert more bookings by engaging guests in over 18+ languages, answering common and complex queries, processing reservations and confirming bookings.The Co also launched Smart ARI which uses AI to solve for overbookings and rate parity violations. While this is less than the tip of the AI iceberg and does not carry any future guarantee, Mr. Chopra’s forward-looking vision provides comfort.

-

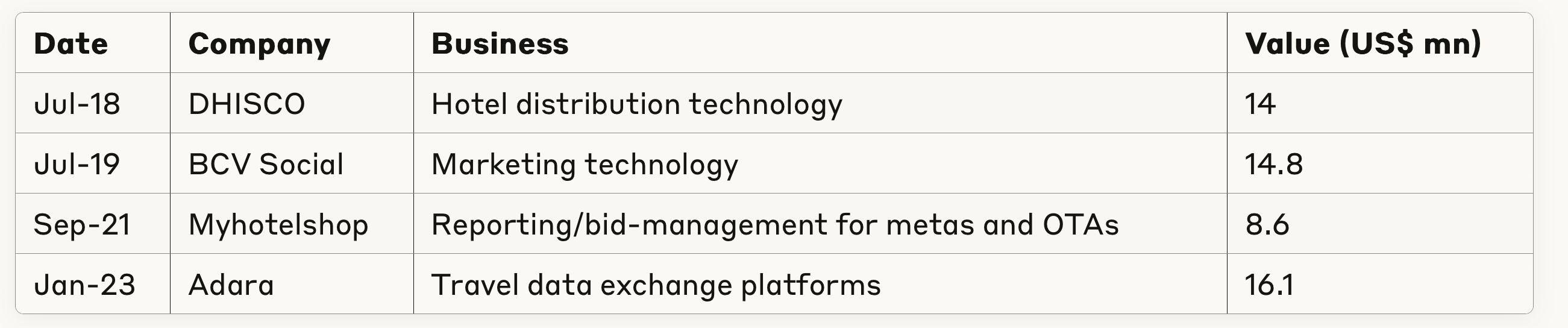

Wrong/Weak acquisitions: An important driver of Rategain’s growth strategy is to acquire other companies to enhance its own products and market reach. M&As are tricky and often turn out to be unsuccessful. Misjudging the value of a business, overpaying for it or even poorly integrating it can lead to financial disruptions and operational strain for the Co.However, we find ease in Rategain’s approach to acquisitions. Mr. Chopra has been repetitive in stating that they are not willing to overpay for acquisitions. And that they will only agree to valuations that comply with the group’s required IRR of over 20% and a payback period of five to seven years. DHISCO’s turnaround to profitability post-acquisition or acquiring Adara at 0.7 times sales to significantly augment’s Rategain’s Martech solutions, offers testament to the company’s disciplined approach.