Rategain

RateGain Travel Technologies Ltd is a leading distribution technology company globally and the largest Software as a Service (SaaS) provider which works in the shadows of travel and hospitality industry in both domestic and international travel markets. The firm offers specialised services across different verticals like hotels, airlines, online travel agents, meta-search companies, package providers, car rentals, cruises, and ferries.

What does it do? - It has three major verticals:

1. Data as a Service (DaaS) (33% of Revenues) - Here, RateGain analysis a massive 24bn data pack of millions of customers to find consumption and decision making patterns and helps the companies (hotels, airlines, etc.) with dynamic pricing that may help them maximise their revenues and profits

2. Marketing Technology (MarTech) (43% of Revenues) – Helping the hotel and travel companies with their digital presence by feeding real-time consumer insights into its software, packaging it and selling it as a subscription to the airlines, hotels, and online travel agents. Helping optimise bookings, monitor engagement and travel intent data

3. Distribution (24% of Revenues) – Helping hotels with availability, rates and digital content across multiple online travel agencies (OTA) and global distribution systems

These are more details of the revenue streams of the company:

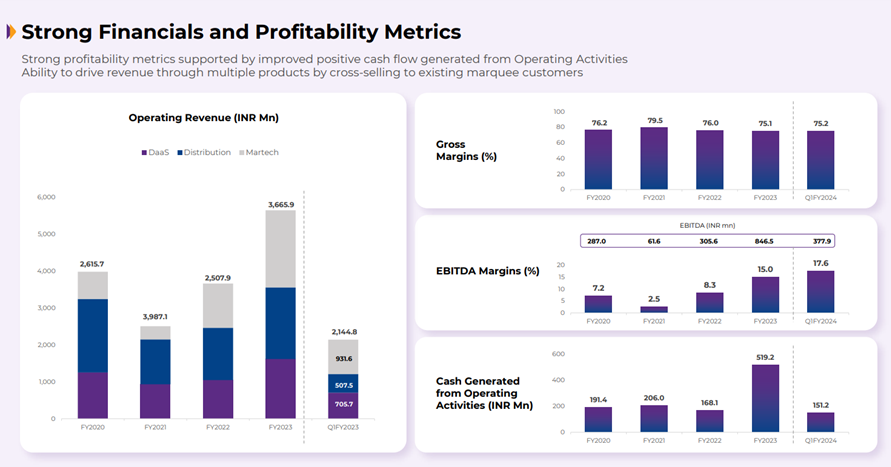

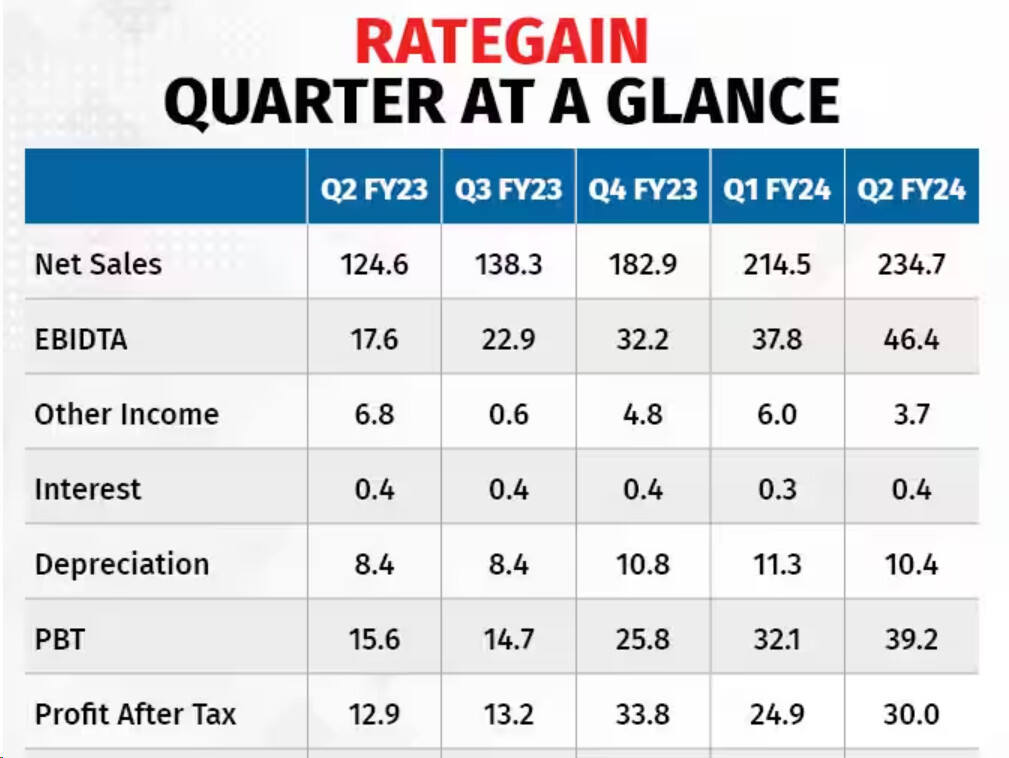

As far as the profitability is concerned, here is a snippet from their latest Q1FY24 presentation:

Key points to note:

- DaaS Segment is growing the fastest – it grew at a massive 139% YoY in Q1FY24

- MarTech grew at 88% YoY

- Distribution grew at 27% YoY

- Added 115 new customers in Q1FY24 – now they have over 3000 customers globally

- Revenue per employee increased by 53% YoY

- Pipeline of 36Cr revenue (which is over 40% of the annual recurring revenue)

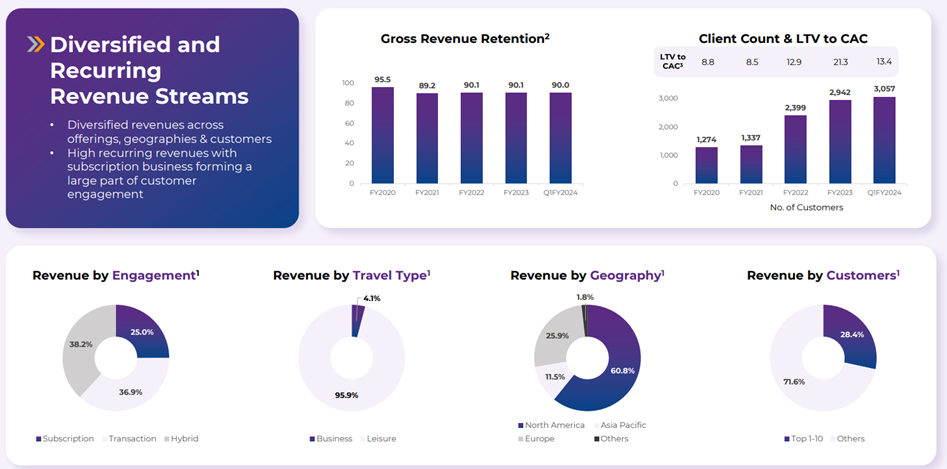

- 63% of the revenue is predictable in nature (Subscription based)

- Sticky customers with 90% Gross and 110% Net Revenue Retention

- 7 of the Top 7 customers have been with them for more than 10 years, which makes one believe that they might be doing something right there

- Margins expanding – 17.6% OPM as of now, expected to reach 25% in the next few years as there is high operating leverage in the business

- Actively acquiring companies for synergies and more revenue streams

- Acquired Adara at a very attractive valuation of 0.6x revenues (Adara finds ways to measure the actual travel intent of a customer and helps RateGain to further strengthen its dynamic pricing

- As per a report, it apparently has 185 companies on its target acquisition list

- Cash rich company with Net Cash & Cash Equivalents of 34Cr

- Tailwinds in the travel industry - 17 out of 22 key global destinations have fully recovered over 2019 levels.

- Aims to double revenues in the next three years

- Important to note that RateGain does not have a single direct competitor, globally

- 25 of the top 30 OTAs and 23 of the top 30 hotel chains in the world are its customers

- Some international carriers like Lufthansa and Singapore Airlines are its clients too

- Moreover, India’s newest low-cost carrier Akasa Air tied up with RateGain even before its launch. Just because it wanted to ensure that it was getting its pricing right from the start

Risks:

- Since the company is highly correlated with the travel and hospitality industry, its performance is largely dependent on how these industries perform.

- Being in a constantly evolving space, RateGain also faces the risk of competition in developing better tech products and keeping up with the changing dynamics of the industry

- Valuations are on the expensive side but that may be less of a concern if it keeps growing at this pace and is able to expand its margins

Disc: Invested

22 Likes

Thanks for the detailed analysis. A few questions:

-

How does it get consumers data? Any views if the recent data protection act which got passed in parliament will adversely affect their SaaS business model?

-

Who’s the competitor globally that you mentioned?

2 Likes

Sir, in this company non executive independent directors are not hold any shares what is advantage or disadvantage of it?

2-Girish Paman vanvari sir taking big salary but they have experience in pharma and chemical company.it is benign for company?

Provides good insights in company’s business model

6 Likes

One comprehensive provider that does all doesn’t really exist. Individual segments have few competitors like Codi, Sabre, Amadeus that handle meta and Google. And as agencies like WPP and psPublicis that do social.

2 Likes

Few points I want to highlight about Rategain:

-

TAM by FY25 - 70,125cr (Huge Opportunity)

-

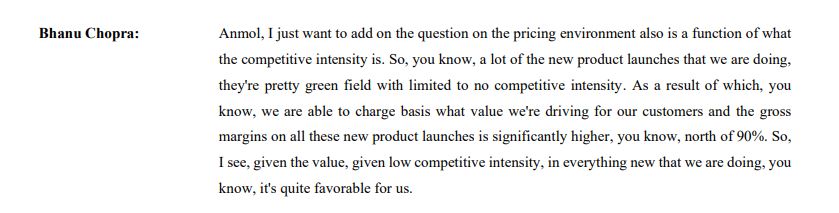

Many of their new product launches are higher in value chain and have limited to no competitive intensity. Gross margins are north of 90%. Good lever for margin expansion along with operating leverage on matured products.

-

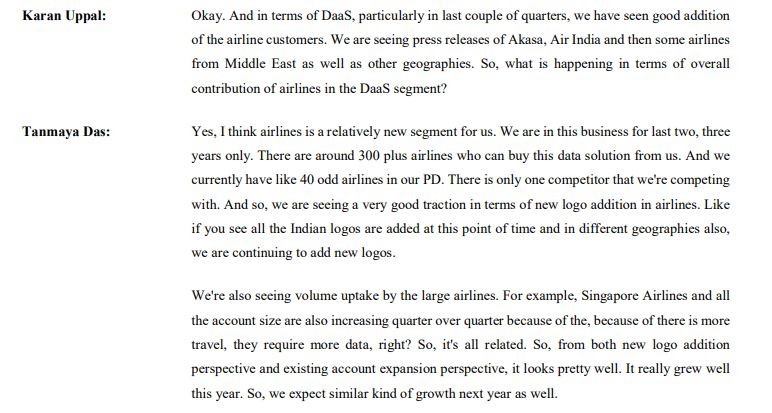

Airlines is a relatively new segment and they are competing with only one player in this.

-

Cyclicality of the travel and hospitality industry is definitely a risk. Cycle is in favor now and just reaching pre-covid levels.

-

Management guiding to double the revenues on FY24 base by FY27. FY24 revenue should be around 875cr. So FY27 revenue comes around 1750cr. You can model with PAT margin expectation.

If mgmt walks the talk, PAT margin can be 20%, which comes to around 350cr.

In base case scenario, giving 40x PE multiple comes to 14000cr Mcap (around 21% CAGR)

Disclosure: Invested, Not a reco.

8 Likes

Almost all companies of startup circle are loss making and ultimately survival chances for long terms are very low

Q2 results out today, net profit up 130% YoY basis(13 crores Vs 30 crores)

Q2 Sales up 88% on YoY basis i.e 125 Vs 235 crores.

2 Likes

Rate gain has posted a very strong set of numbers .

In the concall management guided doubling the revenue with 25% margins in 3 years. The only concern was that the bulk of the growth in this quarter came inorganically from Adara, which showed exponential growth. The management guided strong growth vis-a-vis flattish performance in Distribution vertical for H2 . They also have a strong war chest ready for future acquisition opportunities .

Overall this company seems to be on a roll .

Key risks would be impact on global travel and tourism due to present wars or some other black swan event , technology disruption etc. Stock has run up a bit , but I think it still has the potential to double from the current levels in 3years if management walks the talk.

Disc :Started Investing and looking to add on dips.

Rategain - Q2FY24

Source - https://www.youtube.com/live/GCvPd-PA2gQ?feature=shared

Updates from the above interview

- Was looking for expansion in the Middle east, but those plans have been paused due to the ongoing conflict.

- No impact of interest rates and the Ukraine and Russia conflicts.

- 35% organic growth.

-

Plan is to reach 1000crs revenue by FY24 and then double this revenue in 3 years (Approx 200cr gross profit even assuming 20% GM)

- The M&A plans are for all three verticals, Distribution, DaaS and MarTech. The ticket size is around $20m dollars, some could be more.

- Trying to fill in the whitespaces to form a fully integrated platform company with a lot of cross sell opportunities.

- Have a programmatic M&A plan and they have a database of 350 companies and at any point of time they are talking to a dozen of them and there are a couple of companies which are in the advanced stages of negotiations.

- Looking for companies that can give adjacent capabilities.

- Have around 435crs of cash in the balance sheet.

- Very judicious about what they pay and most of the acquisitions are around 1-2x the annual revenue.

- Geographically their revenue comes 60% from NA, 25% from EMEA, and the rest from the rest of the world.

- Penetration was small in middle east and latin america and now looking to expand there.

- The Middle East expanded dramatically but that has been put to pause.

- Revenue split by the verticals - 45%-Hotels,20%-destination management companies (Visit CA, Incredible India), 15% from OTAs, 5% - airlines and 5% from car rental companies.

- Deal wins 3x of last year, no slowdown seen.

Disc : Invested and increased holdings after the Q2 results.

7 Likes

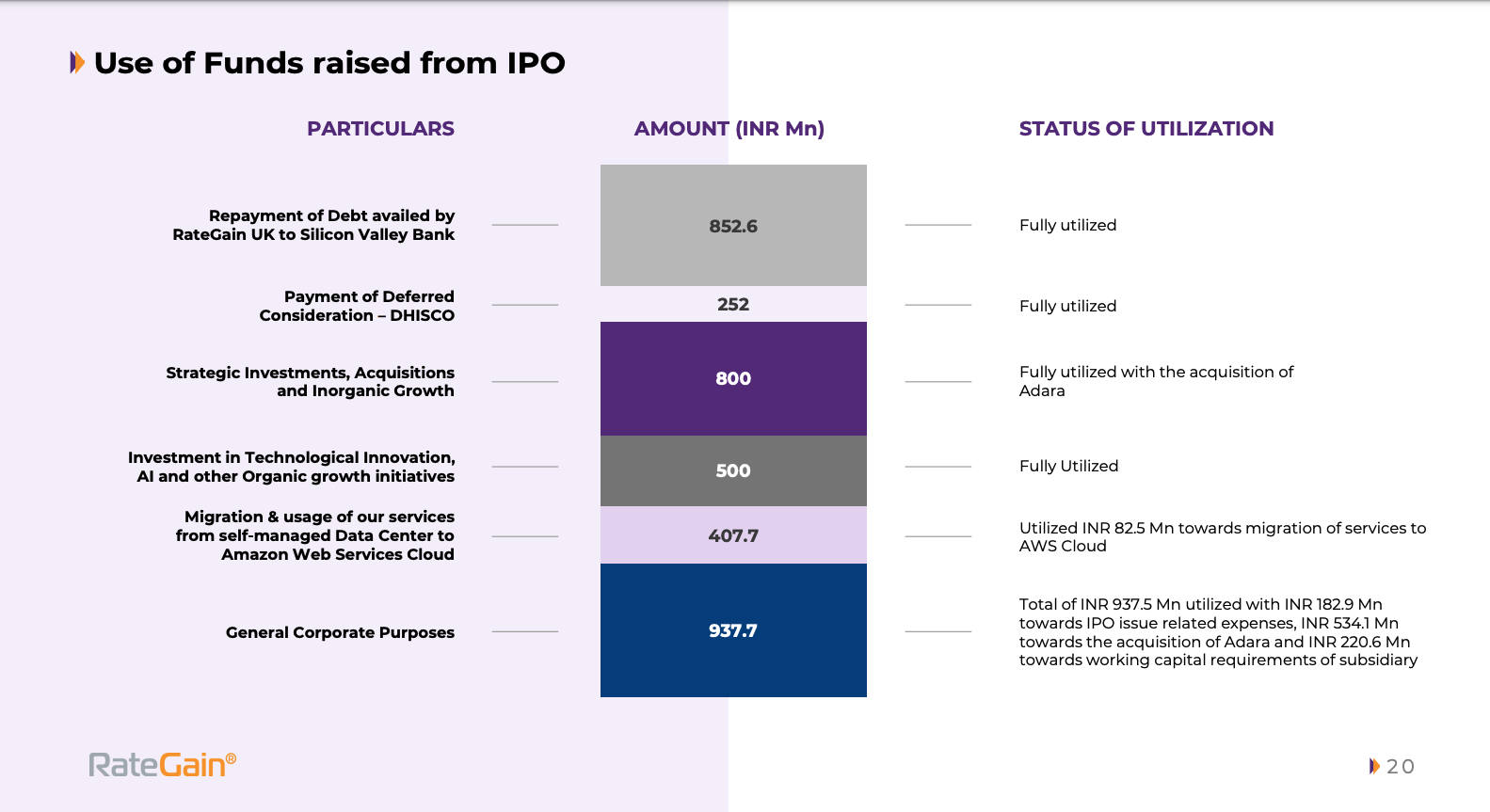

I would like to add one point here

The transparency with which they have mentioned, how they have utilized IPO money, that’s really show how management is serious and ethical about business. This gives me confidence to invest in them

9 Likes

Looks like there will be 5% discount on the floor price (Effective rate may be around 641/-). Good to see despite the news of EPS dilution the stock recovered from the day’s low to end only 1% down. Hopefully in the coming weeks/months rategain will announce some acquisition.

2 Likes

Here’s why I am excited about the fundraise and the road ahead.

Adara once had a pre-covid revenue of around $100m annually. Post-covid its revenue fell to $25m and was making losses of 15% at the EBITDA level and it was not able to recover until rategain came to the rescue and acquire it for mere $16m. Since the acquisition it has brought it a lot of synergies for rategain and has been generating cash from the very first quarter. Here’s the breakdown from the data I have analyzed based on the numbers given in the investor presentations and the concalls.

Adara has not yet reached the full potential and there is a huge runway for growth and the management has aspired to take it back its glory days (and reaching $100m revenue in the process) and even if they reach the halfway mark in year or two, it will still create a lot of value because of the operating leverage.

I don’t expect all their acquisitions to perform the same way, but they have turned around the businesses in the past (like myhotelshop) and I am waiting on their next announcement.

6 Likes

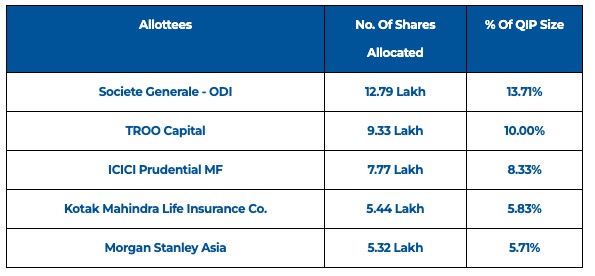

Looks like Societe Generale was allocated ~13% shares from the recently concluded QIP and have offloaded nearly half of their allocation on the first day of QIP listing (As shown in the image below).

Bulk Selling Deal

In my view decoding these actions from the firm might be an act of overthinking, hence we can wait and learn.

Disc. - Invested

1 Like

any potential names for acquisition?

It already had 9,11,095 shares of rate gain bought at Rs 375 since 01.06.2023 so might be some profit booking.

trendlyne bulk deal data.pdf (28.9 KB)