Not sure if everyone here attended the post-acquisiton call by management held on 6th October 2025, the meeting included new CFO Rohan Mittal, Founder Bhanu Chopra and investor relation, Divik Anand.

Here are some keytakeway notes from my end, I might have missed out some stuff and haven’t verified it that thoroughly, the flow of it might be here and there as well. Leaving this here for future readers to fit the timeline better if the call transcript is not readily available.

# Management Call details

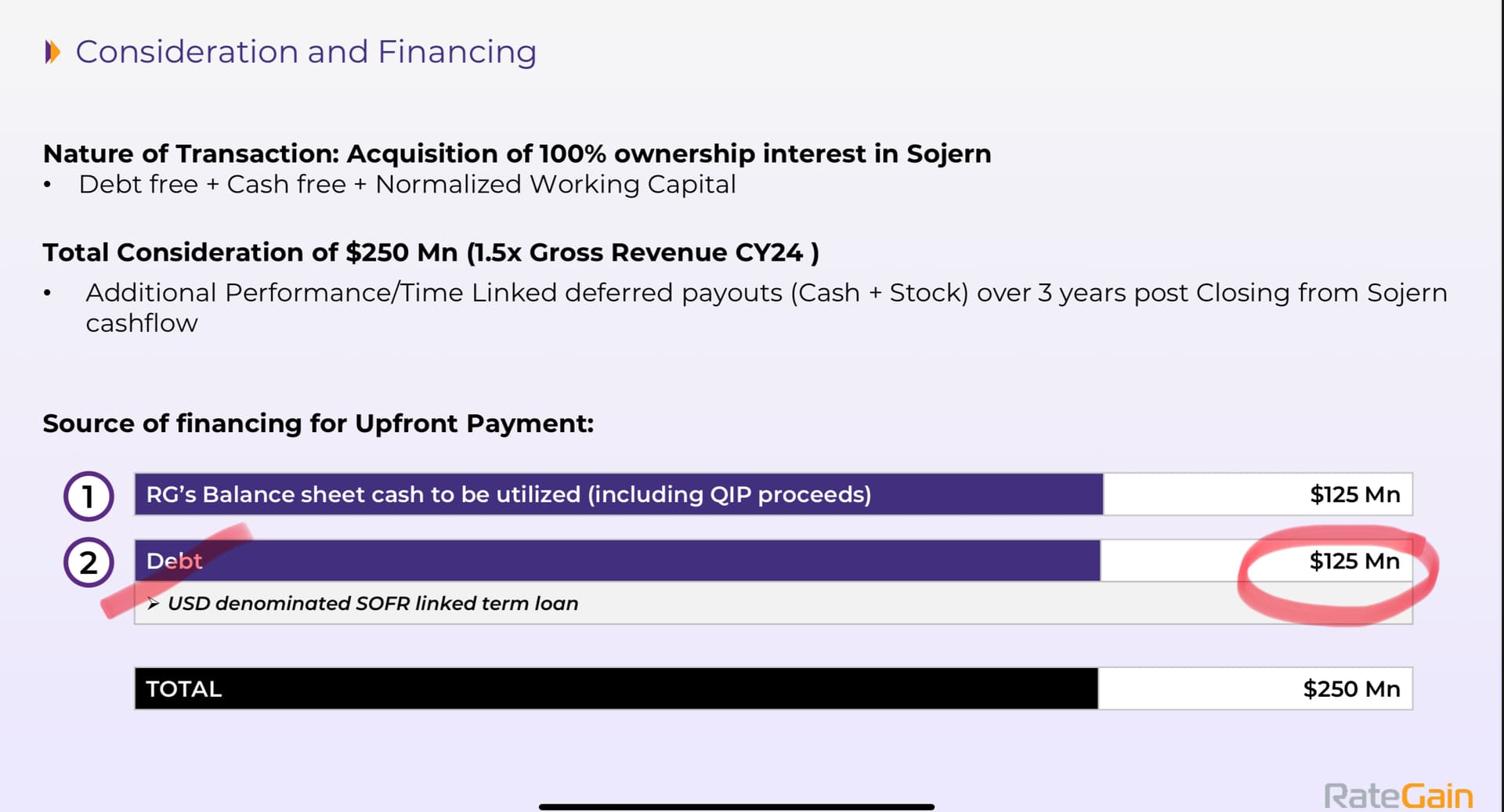

The Company currently has $152 Mn of Cash for this acquisition, of which it will use $125Mn and have the balance as surplus. The Debt of $125 Mn will be SOFR linked + 250BPs. Net debt to EBITDA will be a little under 2x on a run-rate basis at ~50 million EBITDA, before synergies. We expect the debt to come down substantially in 12-24 months. We typically convert 70-90% of EBITDA to operating cash flow. Debt cost expected at SOFR + ~250 bps. With recent Fed moves, that implies roughly 6.6–6.7% currently, give or take.

There are no direct competitors at RateGain’s scale in Mar-Tech post acquisition, they still face competition from agencies but its more of a corporation-competitor relationship where sometimes rategains has to give them access to their own data for their benefit. On a larger scale, they face competition from Meta and Google. Some names in the broader space include Criteo and Tripscody, while in the large-platform ecosystem customers can also allocate to Google and Meta. We are building a differentiated B2B proposition for hospitality within that larger landscape.

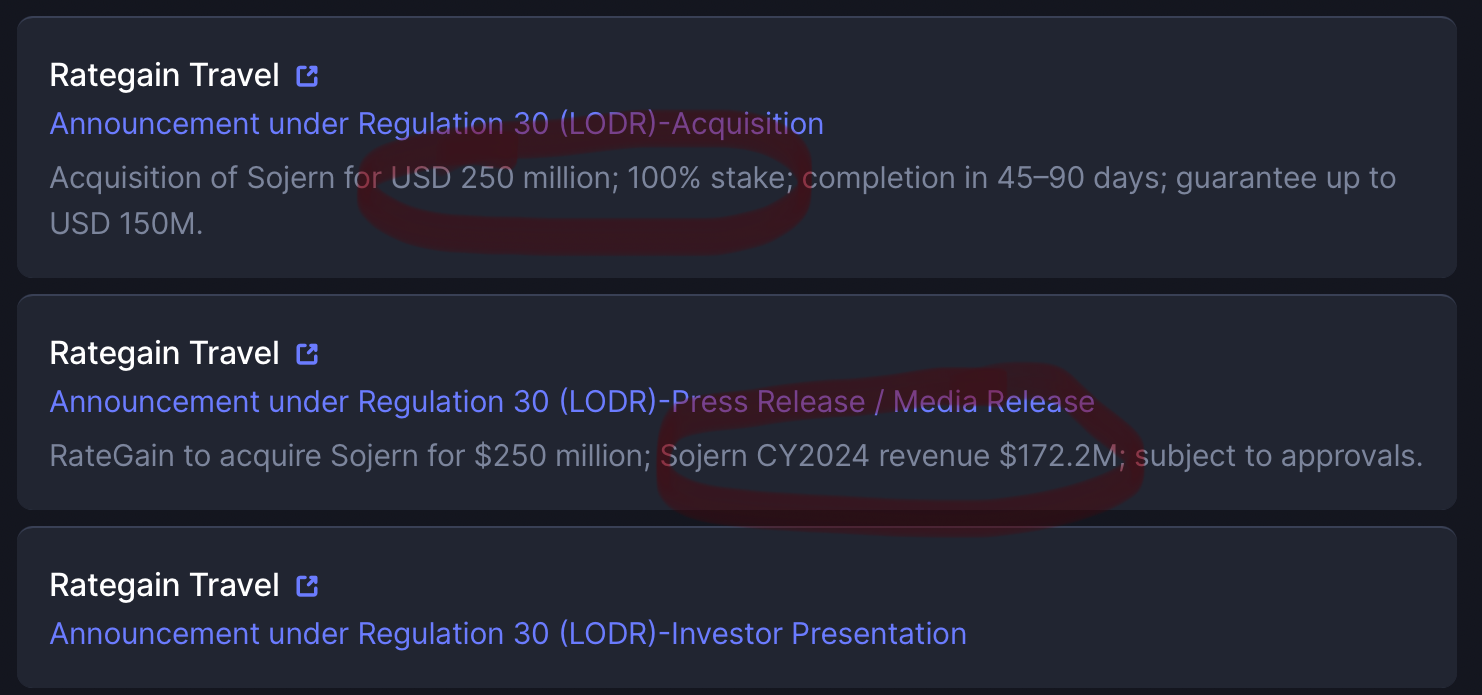

The Acquisition has been in talks since 2022 but the Company’s M&A straetgy has been disciplined, one of the reason why Sojern agreed to P/S of 1.5x is due to backing of TCV which is a PE firm who wanted an exit from Sojern as it had surpassed its investment duration.

The Basic Synergies will be to reduce cost of SG&A and other expenses and shift them to India, unsubscribe from redundant services subscribed.

Sojern’s current ebitda margins of 11-12% will be taken to 17-18% in FY27 from these cost reductions, other synergies such as cross selling will benefit even more. Sojern has been growing at 4% topline in the past year. Major cost reductions will be from Primarily SG&A: office consolidation, procurement leverage on software, removing redundant tools, and centres of excellence in finance, HR, legal, and other teams. These levers take EBITDA from ~11–12% to 17–19% exit-run by FY27(just for sojern). Additional levers exist but are not in guidance yet.

The Senior Management personnel will stay at Sojern and it will work as its own entity as with Adara which operates as itself. There will low layoff at Sojern post acquisiton and they will be based on performance based layoffs.

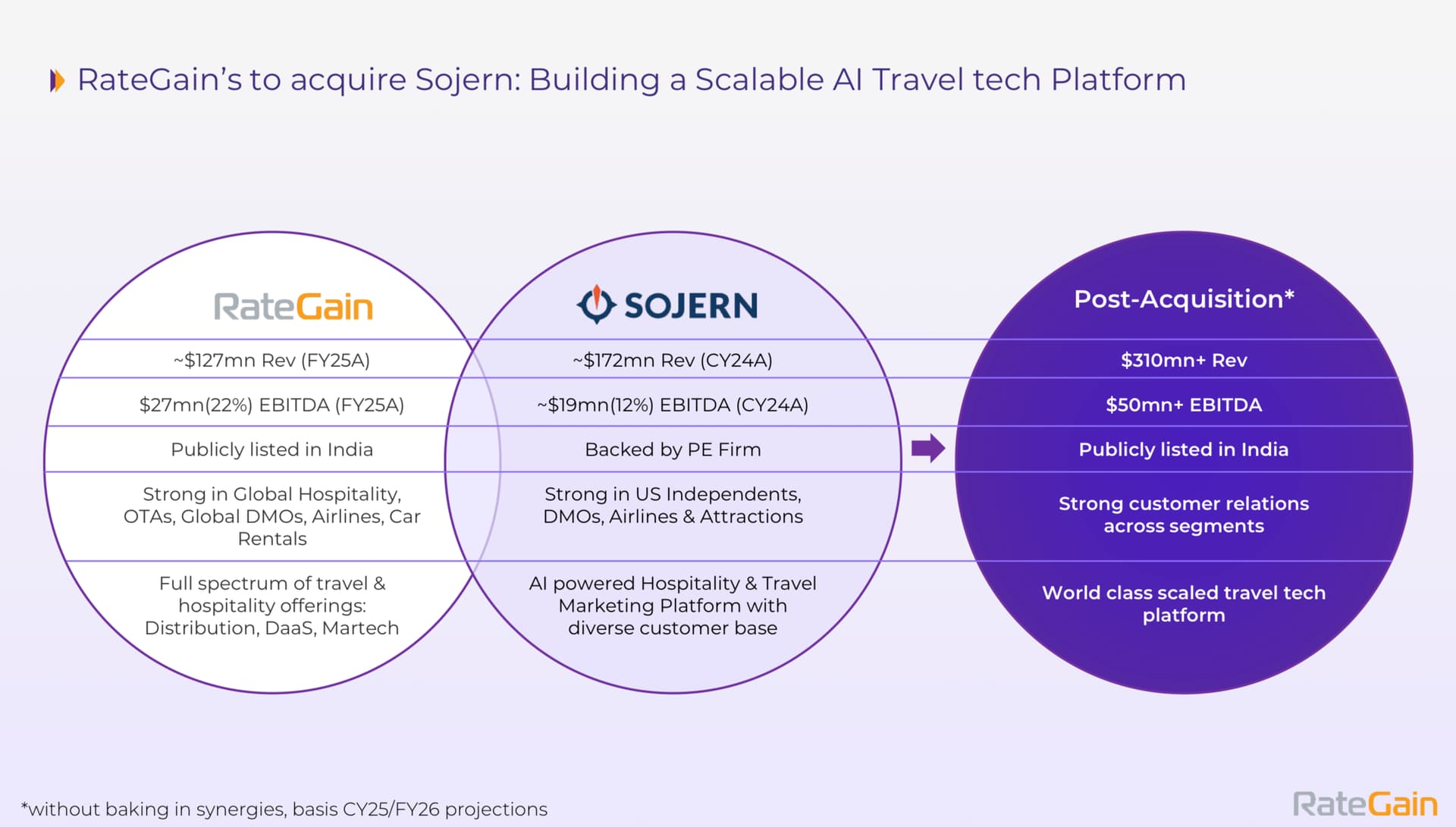

Post Acquisition Guidance : Rate Gain to grow 6-8% and Sojern is growing at 3-4% currently, Combined unit expected growth in expected to be 15% for FY27. Ebitda margins, rategain is epxected to do 15-18% in FY26 and did 18% in Q1 FY26, for sojern standalone ebitda margins were 12% in CY24 and the goal is to get combined business margins of 18-19% in next 12 months.

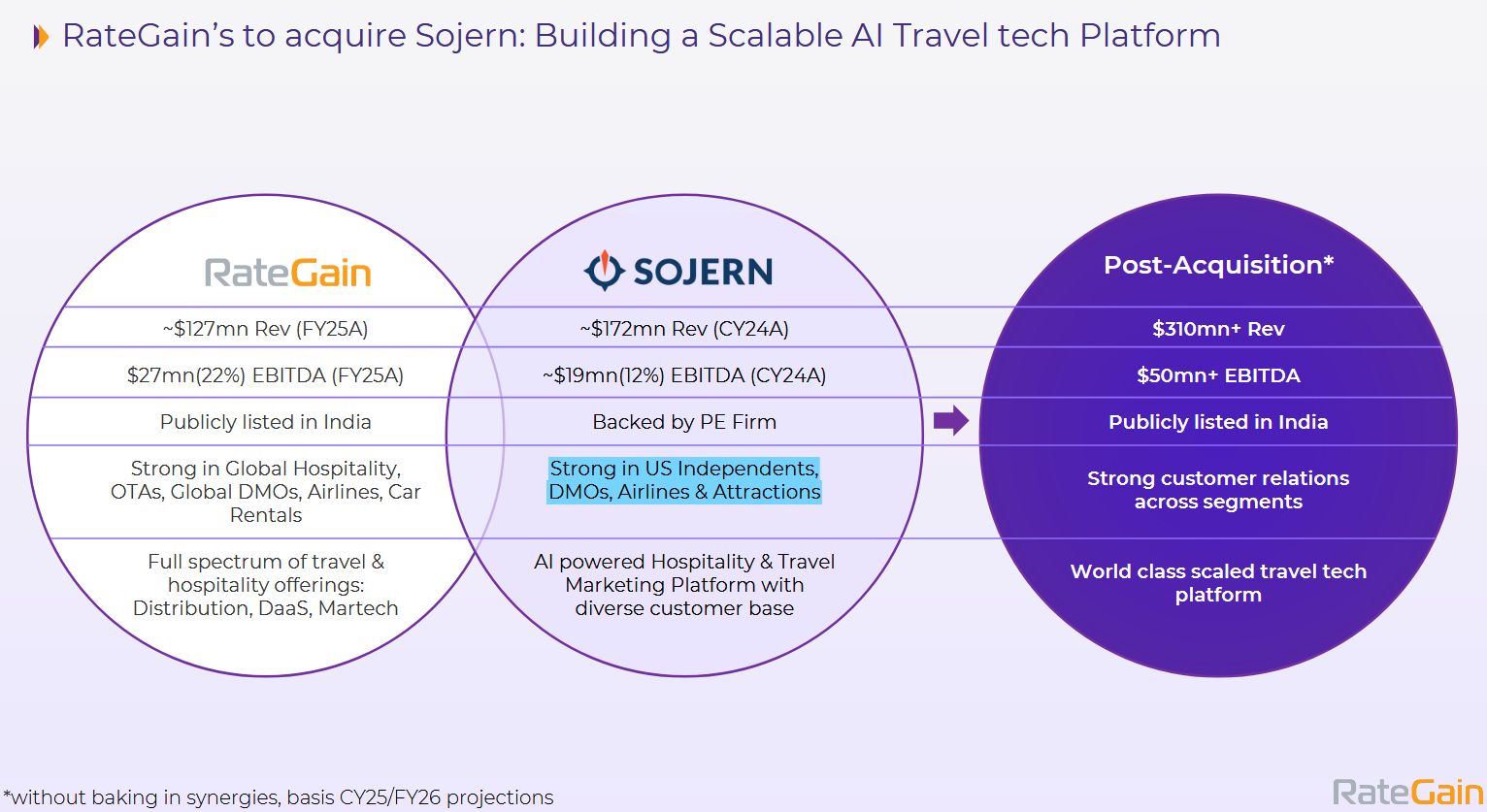

Why 4% growth for Sojern?

Sojern’s properties business grew double-digit, while DMOs/corporates declined, which is comparable to Adara’s competitive space where we have grown north of 20%. We see scope to revive growth in the DMO/corporate segment and further accelerate the properties business via our combined multi-channel offering and expanded GTM in APAC and the Middle East. Beyond cost synergies to reach 18–19% margins, we also expect operating leverage from revenue acceleration.

There is overlap with Sojern’s customer in enterprise, however, for smaller and independent properties there is less overlap which makes about 50% of sojern’s revenue. Sojern brings demand to the hotel website; with UNO, our personalised booking engine and guest-engagement solutions can help convert and grow share of wallet across acquisition, retention, engagement, and wallet share. Sojern also already has a guest-engagement and retention platform acquired in 2023, which we can roll out to our base.

Sojern’s main differentiation is their guest engagement platform which rategain always wanted to do. This platform takes data from guests after their stay and then uses it to drive more bookings for hotels. For DMOs and corporates, Sojern’s capability set is very similar to Adara, and they have often been a key competitor. On the property side, Sojern’s offering is similar to our Demand Booster

Post Acquisition : They(sojern) historically leaned into display/programmatic, while we focused more on metasearch and search. Combined, we become strong across display, programmatic, search, metasearch, and social. In addition, Sojern’s guest-engagement platform fills a capability gap we had post-booking.

This deal will be EPS accretive, “Looking at FY27 (full year of merged operations), we expect $63–65 million EBITDA given our growth and margin guidance. That should translate to $36–39 million PBT, which implies a 30–35% year-on-year PBT increase versus Q1 annualised PBT. Interest costs will be highest in year one and then decline as debt reduces, which naturally supports EPS growth even before further synergies.” - CFO

Moreover, blended tax rate should be 22.5% for forecasting purposes*

Out of $250Mn, 50-60% will be goodwill, and balance will be amortised over time.

On a 10 year horizon, no goal to become something like a GDS, they will focus more on front office, the TAM on it is $7B vs the Company’s $310M after acquisition, leaving room to acquire in form of market and wallet share. They haven’t ruled out Mid-office/Back office opportunities but not in plans as of recently

There are no m&a deals in pipeline and focus is more on executing synergies for this Acquisitions.