agree @Venkat_Rakesh. The company has once again lowered its FY25 guidance, now expecting 12-13% YoY growth—down from 15% in Q2 and over 20% in Q1.

I feel the story isn’t matching the numbers. The company has captured a significant portion of its TAM, yet it seems to be struggling with revenue growth.

Disclosure: I have been invested for a long time but trimmed my position today.

With the 12-13% guidance for FY25, estimated Q4 revenues are 256-265 Cr.

Computed the segment wise revenue based off past quarters commentaries (used NotebookLM) to arrive at the below. Distribution segment has been flattish last 7 quarters

While the management under promised on guidance and over delivered on results in FY23 & FY24; they have been lowering their guidance each quarter in FY25. (20% → 15% → 12-13%)

Is a pipeline of 507 Cr, ~2x sales good enough? I was reading online that a good SaaS pipeline should be >3x sales. Maybe this explains the additional investment in an SDR team for lead generation.

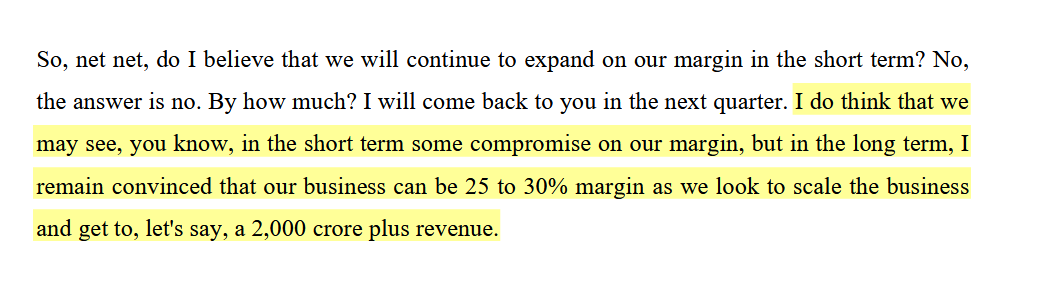

In the past, this stock had very high valuations because of 1) High growth (>60%) on low base and 2) FY 27 long term guidance of 2000 Cr which implied future growth at 26% CAGR

Because both aren’t happening currently, that may explain the correction.

What I am looking forward to in Q4 concall:

guidance on FY 26 revenue and EBITDA margins (they mentioned about an ongoing budgeting excercise)

2000 CR revenue by FY 27 still holds true or does it get revised?

additional details on this large deal signed up with a big software company

Disc: Invested a small amount for tracking purposes.

Can someone please help why the company’s ROE is low? Usually SaaS companies have high margins & ROE. Is it because that large chunk of money in cash or investment (1200cr) which might not be yielding great returns? or something else too

This is mathematical - they generate profits, which are being put into reserves (and hence add to the equity base- the denominator in RoE). Currently the profits (and cash) are being retained in the Balance Sheet as the mgmt scouts for acquisition options. The equity base is not generating return, hence numerator is not growing commensurate to the denominator.

The stock has corrected significantly and has around 1200Cr of cash on the balance sheet. EV/EBIDTA is at its lowest. Do you have any thoughts about investing here. Planning to add this as tracking position.

Markets tend to react strongly to downward revisions in guidance, and we’re seeing that play out with RateGain. Over the last year, the company has continuously lowered its guidance; 20% in Q1FY25, 15% in Q2FY25, and now 12-13% in Q3FY25. These frequent downward adjustments often lead to heightened market volatility, as investors typically reassess the company’s growth prospects and profitability.

As for valuation, it’s important to remember that a significant stock correction may not always signal a clear ‘buy’ opportunity. The price at which you find value is subjective and depends on your individual risk tolerance and investment horizon. While the stock might look attractive at lower levels, it’s crucial to evaluate whether the reduced guidance reflects a temporary setback or a more fundamental shift in the company’s trajectory.

One assuring fact is that RateGain is at quite a favorable multiple. Yes, revenue has slowed down, but they are not into just some IT services. I believe they should be able to come out of this with revenue picking up. Guidance is for March 2025 only, but Management did indicate that they struck some new contracts that will take time to reflect. I believe revenue should pick up with time, and this will reflect in the better premiums.

What I like is that company is slowly transforming from distribution company to a technology company. More revenue is coming from data services and tech services, this should translate to higher PAT as they are high margin business. While revenue growth might be around 12-13% I feel PAT growth will be higher. Assuming a conservative PAT growth of 15% for next 3 years, and its available a PE multiple of 25 it looks attractive. Also their revenue retention is around 90% which I feel is quite good, they are also spending on creating AI agents for hotel which can add a lot of value.

Hoever on other side I am still not able to understand the reason behind such a decline in stock price? Is it mostly due to lower guidance? Also anyone know what is the reason behind promoters decline in shareholding in last 2 years?

I somehow believe that fair multiple is about 20x because they have about 1200Crs in B/S. Removing this amount will bring the Market Cap to about 4000 Crs with about FY25E PAT to be about 200Crs. The company does seem cheap but I am not sure if one should consider my above valuation approach. But the fact remains that company is willing to wait out to find proper company for acquisition should be appreciated.

The reason for the Falling Promoter shareholding is that they did a QIP last year.

But I want clarity on a matter is the management sticking with the guidance to double the revenue from FY24 in three years?

PAT growth is more due to huge reserve company is carrying, leading to increase in Other incomes

Company need to take some action with huge surplus of money sitting ideal in the reseve else it will lead to more pain for Stakeholders.

This Quaterly revenue will be in single digit as per the yearly guidance of 12-13% , leading to down-rating in PE

200 cr of profit in FY25 will include around 75 cr of other income, mostly from interest on 1200 cr. So operating part will be around 125. So valuation should be 125*20 + 1200 = 3700 cr

Their TTM Operating profit is 226, post depreciation it will make it to 190 Cr, which translates to a PAT of 152 assuming a tax of around 20%. The current valuation is 5200 cr and cash of 1200 Cr. So this makes 4000Cr valuation of the business and translates to a PE of around 26.

Yes, I think your math is correct and I did miss out one the interest component of the income statement in my previous statement when I mentioned it is currently at 20x

But Coming back to the Current PE 25, it does slightly seems attractive to me as the management has reaffirmed 2000 Crs Revenue Guidance in the previous con-call. Snippet below.

While I don’t believe they can achieve this target in 3 years time from FY24 being previously stated, however I do believe that they can do in 5 years time at a Sales Growth of 16% by the year FY29 with Margin of 25% yielding 500Crs as PAT.

I think they will have impact on the PAT margin next FY once they acquire company

FY24

FY25

FY26

FY27

FY28

FY29

Revenue

957

1100

1280

1480

1730

2000

PAT Margin

15%

20%

20%

22%

25%

25%

PAT

144

220

256

326

433

500

Mcap

5200

5200

5200

5200

5200

P/E

25

20

16

12

10

PEG

0.5

1.2

0.6

0.4

0.7

This is an highly ideal situation if all things go well.

Disclosure: Not Invested, tracking.

I hope they remain prudent and patient. Given how things stand, good chance US and world in general goes through a slow down. This will potentially offer lucrative acquisition opprtunities - something they have been deferring due to too.many suitors chasing too few a targets driving insane valuations.

Long story short, good chance revenue targets are met, albeit inorganically

In the Feb 2025 con-call where they did a downward revision in their guidance, there were two encouraging points that have gone unnoticed, which will help them reach 2000cr annual revenue target by FY27.

They have two big deals in the pipeline -

Upselling to an existing big customer - “there is one existing big customer that we are negotiating a very, very large deal on just continuing to serve them large volumes of data.”

New big customer acquisition - “we signed a very large deal with one of the biggest software companies on the planet”

The main risk is a slowdown/recession in the US especially after the tariff scene. But this might come as another opportunity to buy distressed companies cheaper valuations for a turnaround (like Adara which couldn’t withstand covid). Are there any other risks that I am missing?

Disc: Not invested. Looking to make fresh positions.

The management has not explained specifically why the jump was 3x. But if you look at their commentary in earnings calls, they have repeatedly focused on increasing sales and digital advertising expense. For example the below excerpt from Page 9 of Q1FY24 earnings call:

Yes, so it’s going to be a combination of really three things, right? So, like I said, within the existing product set as well, we are seeing quite an acceleration. And we are continuing to invest more in the sales and marketing there. We added more people in Latin America. We’re bringing back Ex-Adara folks. We’ve really taken on digital marketing also in a big, big way. And we see a very, very good return on ad-spend there.

Also, I suspect they are putting more and more advertising efforts behind their marketing tech division. As a result you see their marketing tech division revenues grew by 111% in FY24.

Moving on to your next question

Please note that in the DRHP, the company explained on Page 283

Demand partner fees that decreased by 53.01% from ₹ 195.94 million in Fiscal 2020 to ₹ 92.08 million in Fiscal 2021, owing to a reduction in revenue as demand partners are paid revenue share from revenues obtained from customers.

But yes, why would this fee go up 4x? Actually, it has gone up from 1.89 paise per rupee of revenue in FY23 vs 4.15 paise in FY24. The only explanation I can think of is that it was due to ‘Adara’ in the marketing tech division. They acquired this business at the end of FY23 and therefore may be the revenue share arrangements of Adara with demand partners is what led to this growth.