Hi @Rajesh_Singh sir! May I learn about your thesis behind Sun Retail Ltd? Because from what I see is, the company is currently loss making and was doing reasonably well until FY 19 but then had been on a constant decline (that too massive decline) and is again gaining momentum (FY 24). Is it a turnaround story or what?

There is no sun retail in my portfolio so cant comment , you may be talking about Sonalis consumer , its quarterly update, preferential and bigger goals ahead are game changer can study that.

3 Likes

Thank you @Rajesh_Singh Sir for sharing your knowledge and insights with us. Sir, have you looked into Nirman Agri Genetics? Management is very ambitious and they are looking at 100% CAGR. There’s a lot of buzz regarding it amongst SME investors as well.

1 Like

Not invested in that but looks like multibagger if mgt is able to execute its plan .

2 Likes

Sir, some sceptics have raised the issue of regulatory non-compliance by Sonalis consumer such as late publication of results etc. Is the management of the company honest and trustworthy?

I full trust them and have invested since the last one year even when price dipped to 30 Rs . There were issues but management was transparent with us in our discussion and in AGM too.

1 Like

Sir @Rajesh_Singh did you check Kamat Hotels Q1 result? Is it on expected line?

Result is below expectations and management explained the reason. This will unfold fully by Q4 when their capacity is built fully.

2 Likes

@Rajesh_Singh : Any views on Transteel Seating technologies ?

@Rajesh_Singh : Do you track Canarys Automations ?

Thanks alot for such valuable information.

This is old propaganda and dated too mgt clarified a few quarters back post preferential u can read the transcript that they work with subcons. Order book copynis uploaded. Guidance of 1000 crore topline with similar pat percentage by FY 26, already a multibagger and mega multibagger in making.

Regards

1 Like

hello sir ,

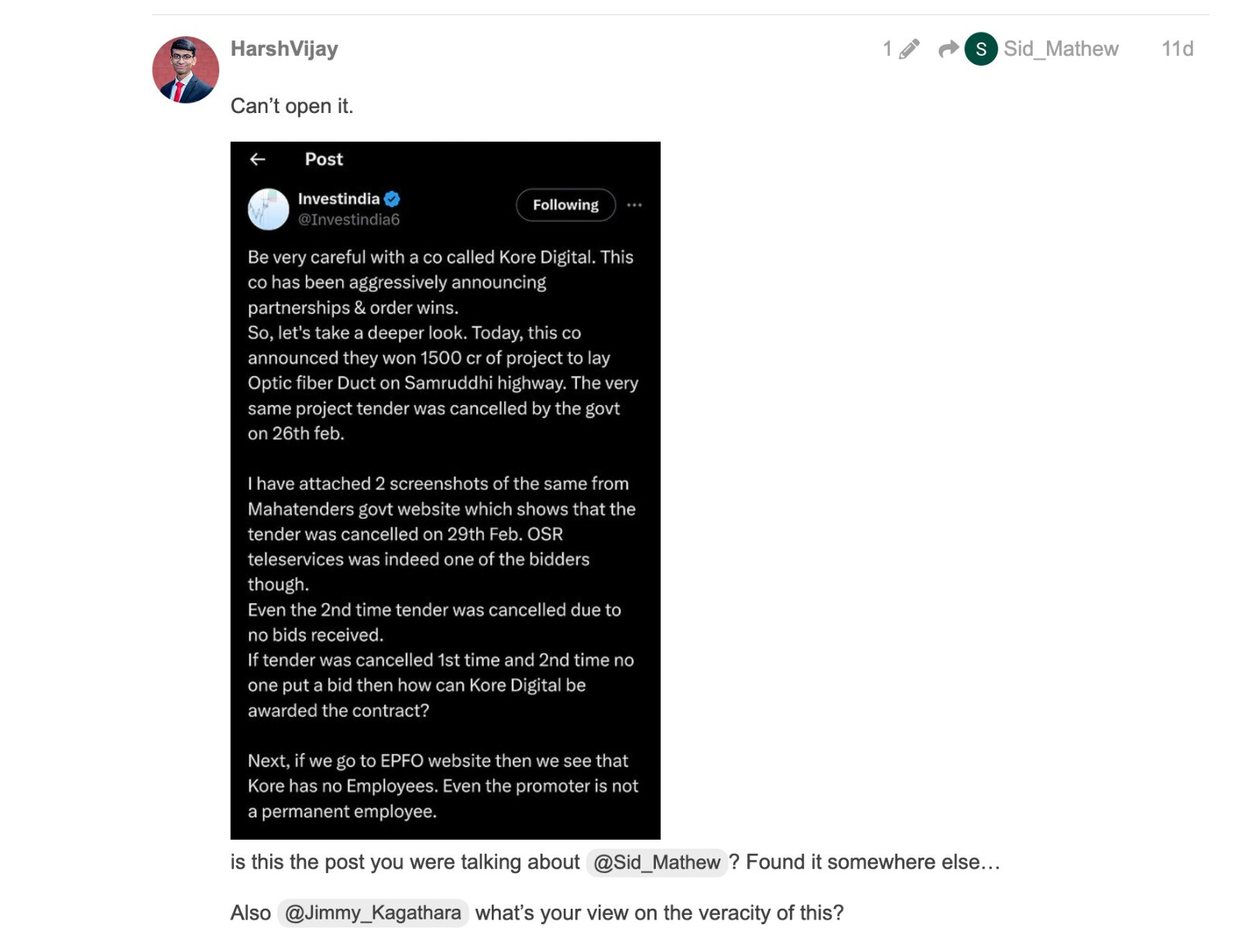

is it right time to enter kore digital or i missed the bus!

i am new here on this thread as well in markets.

Key is to enter stocks before they run, may like to study K2 infragen and cellecor gadgets both have guidance of 100% CAGR and have not run much

1 Like

Sir - what about TRANSTEEL SEATING Technologies and Canarys Automations

As per my analysis of cellecor gadgets

Negative

- Companies porfolio main product is feature phone(old nokia brick type) , As per market/industry of feature phone is on decline buy -15 to 20% every year.

- They have entered into Cluttered market of smart tv and tws and smart watches(low marging and highly competitive margin).

- There is no usp in this type of bussiness lets say moat or competetive edge.

Positives

1)There distribution network(offline sales) are in tier 2 and tier 3 cities wich consist of 80% sales as of now.

2) If i may not be wrong beat xp ecommerce head is being hired by them just few days ago as per there update… beat xp is kinda experieced in online/ecommerce market. This hiring may help them boost there online sales.

Sir please ,

with your Experience and knowledge what do you think about this company ? am i missing something ?

I have not studied so wont be proper for me to comment

Rajesh Sir is very bullish on Cellecor gadgets.

-

I don’t think there is segment wise rev data available but feature phones must be a small part of their total rev, which is only going to reuce in the times ahead thanks to the new gadgets they are launching.

-

Distribution will be the key while targeting tier 2 and tier 3 cities. there’s huge potential and the rural incomes have been already rising and is expected to rise in the times ahead (look at some of the proxy data like tractor and 2-wheeler sales). Brand building will be the key which I think cellecor has.

-

A great distribution network and a good brand image is the EDGE/MOAT.