https://twitter.com/Rajesh_FC/status/1701605661774397872?t=slUiYB9ZWaOLjHS81W3Sjw&s=19

I have benefited especially in cleaning up through this forum and finding out nuances so sharing my portfolio and philosophy both.

आ नो भद्राः क्रतवो यन्तु विश्वतः May auspicious thoughts come to us from all over the world – Rig Veda

Cleaned up many laggards in the last quarter and will continue to water the flowers and cut the weeds. What better day to write this today when most of companies in portfolio ended in deep red.

Key points- Temperament for concentration and to bear fluctuations or drawdown of 50% or more also calmly when conviction is there, Foresight to identify small to nanocap with long run ahead, Patience from min 5 year to decades to forever also (beyond my life)

Process of building perspective on investment will continue life long. Investment was gift from covid and what a blunder to start so late in mid 40s but better late than never.

Education – reading annual reports, analysts reports, investor presentation, mega trend, pod casts, youtube videos, management commentary forums such as valuepickr. Reading / listening to more than 1000 hours of wisdom of Buffet, Munger, Mohish Pabrai, Vijay Kedia and many more , last but not the least late Big bull indomitable, unfiltered and inimitable Rakesh Jhujhunwala. I learnt from him that investment portfolio and trading portfolio can be separate. Exposure of a few whom I admire on twitter or superstar investors’ pick as bulk deal or above 1% is known publicly. There are many who don’t know that they don’t know ![]() as Buffet said vividly. Some have strong opinions or may be incentive driven to earn anyhow, so we have to be very choosy also whom we interact with. Sharing a few examples – Brightcom or BCG- there was concerted push by many and when I looked at linkedin just saw 100 odd employees that too in countries which are hardly known to be talent hub, how can I company with around billion dollar revenue have 100 odd employees. Does the business even exist? Another one after acquisition of Tejas by Tatas and later management guidance that they are aiming for top 5 telecom OEMs in the world still many influencers goading to book profit on 30 to 50% gain or quick to jump on poor quarterly results. Mostly great investments take many years or even decades of conviction. Investing is probabilistic but all we need are a few big winners as Peter Lynch says. Good governance and sustained earning growth are vital for creating value and yet very few companies are able to pull it off. Making mistakes and learning from them will continue lifelong too.

as Buffet said vividly. Some have strong opinions or may be incentive driven to earn anyhow, so we have to be very choosy also whom we interact with. Sharing a few examples – Brightcom or BCG- there was concerted push by many and when I looked at linkedin just saw 100 odd employees that too in countries which are hardly known to be talent hub, how can I company with around billion dollar revenue have 100 odd employees. Does the business even exist? Another one after acquisition of Tejas by Tatas and later management guidance that they are aiming for top 5 telecom OEMs in the world still many influencers goading to book profit on 30 to 50% gain or quick to jump on poor quarterly results. Mostly great investments take many years or even decades of conviction. Investing is probabilistic but all we need are a few big winners as Peter Lynch says. Good governance and sustained earning growth are vital for creating value and yet very few companies are able to pull it off. Making mistakes and learning from them will continue lifelong too.

Portfolio-

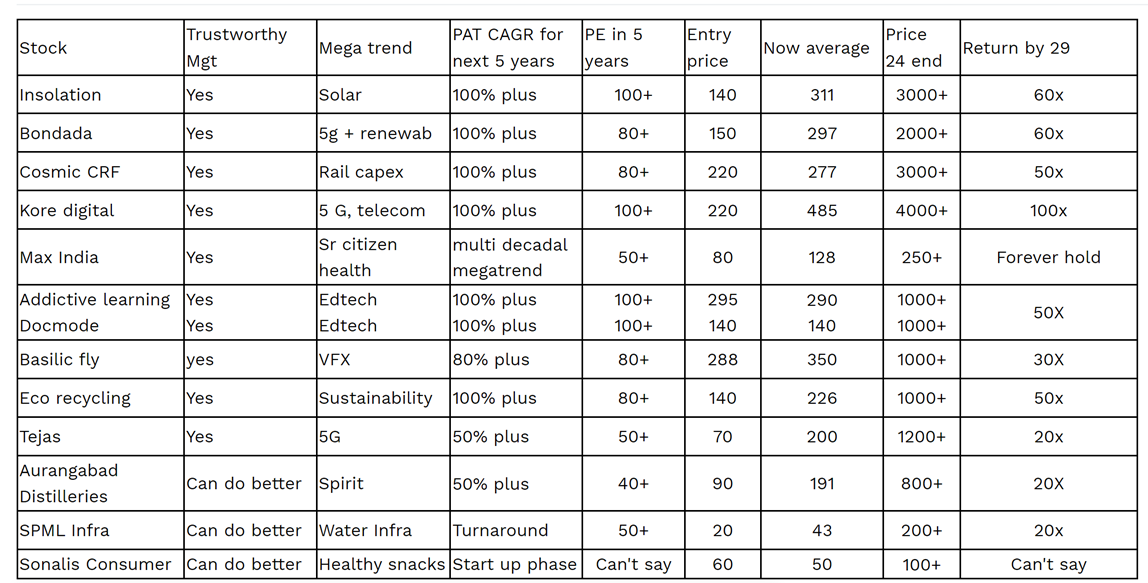

Long term 75% of portfolio - As long as thesis remains intact (holding since 3 years KPIT, Tejas & Optimums) others are Max India, RIR, Frog cellsat, Kore digital, Cosmic CRF, Ecoreco, SEML, Timescan, Affordable robotic, Insolation energy, Aurangabad distilleries, Reliance Industries

Second high risk not more than 10% of Portfolio to review by Dec 23 and if hypothesis is wrong then exit - Coffee day, Sonalisconsumer,

Review by next Sept 15% of portfolio and if hypothesis is right then move to long term - Waa solar, Silicon rental, Patel Engineering, Kamat hotels, Bondada, Hazoor, SPML infra, Ind swift, Mercury EV

DYODD (do your own due diligence)

Questions:

1.Why do you hold partially failed company like CCD?

2. Sonalis Consumer is a pump and dump as far as I know. What thesis to invest?

3. Waa Solar has CG issues. Why to invest?

Major companies are in good sector/valuations and good to see SMEs in your long term view.

Regarding Silicon, I was bullish on there business and still am. On VP, there is a thread showcasing high parameters compared to industry players; to play on safer side I booked my half holdings on nominal profit.

Thank you for feedback.

- CCD AGM I had partcipated last year and they had clear plans of debt reduction and strategic investor. In the current AGM they reiterated the same. ARC has taken two loans and bulk should be settled in two quarter. They said that once bank loan is settled then strategic investor will come in. In Growing phase QSR category is valued at 10 x revenue so that is hypothesis. Let us see how it unfolds

- Sonalis consumer I got impressed by passion of management in interaction as they have plans of increasing capacity to 5x this year doubling revenue every year in the mid term. Have to see execution.

- Looked undervalued in megatrend let me find out more. Yesterday was AGM which looked eyewash to me so will exit by next year if price doesnt move up. At this price looks very less downside.

Mercury EV-Tech has formed an in-house assembly line for the 2W & 3W products where production of 2W has been started with brand name of “EZ” and “Smart”. The Company has introduced this model in market with 130+ dealers network PAN India. Company owns an 18-acre land where it has started setting up in-house facility for manufacturing key components like battery, chassis, motor controller, brake shoe, CED paint and already operational assembly line. The company’s mission is to continue towards a responsible and green transportation journey with innovative and advanced Make-in-India electric mobility solutions. It aspires to provide all-inclusive service and charging stations across the nation to push the market towards a clean energy alternative.

As per Annual Report FY2023: The Company already have land bank of Rs 30 Cr.

RIR is RIR Power Electronics Ltd ? What is your rationale behind investing in this company. The have just secured proposal to ivest 500 Cr+ in Odisha.

Being from this industry this announcement gives me a headache. Fabrication and packaging are very different parts of the value chain. You wouldn’t even be able to buy half a lithography machine for 500 crores lol or put up a decent economies of scale packaging or ATMP (as its called) facility.

The entire semiconductor hype in India is unfounded IMO - we are 5-10 years away from doing anything even on leading edge nodes right now. Investors should pay a close attention to the value chain, technology node and product segments RIR Power is catering to - you will find that its mostly commodity (look at their website). The only project that is worth anything is the Tata Micron ATMP JV and the proposed Foxconn STMicro JV for 40nm Fabrication. If you buy RIR power - buy it not for Semi but maybe an EMS play?

Exits - Optiemus at 3x , management not credible, participated in AGM - they planted a few yes sir type shareholders , even CEO was not invited and peformance has been average too. Same reason for exit of Waa solar - Management comes reads voting instruction and AGM is over - cant trust such promoters. Frog missed guideline and lowered guidance - again crediblity issue exited , timescan - another laggard since the last one year exited , SEML - another laggard exited, Reliance exited full position it is 10x here in a decade with demergers and all but my goal is 100x not 10x , RIR not conviced with narrative exited, Affordable buy price was high hence may test patience exited , Coffee day trimeed exposure - debt resoluton taking time. Ind swift lab exited - doesnt seem attractive with main business gone. Bondada moves to long term portfolio. Basilic Fly new entry (management guidance of 50 to 80% CAGR for next couple of years).

Criteria to stay or exit - Management not transparent or not delivering (surprise is a big no no), Explosive growth with large TAM is a must to have 10x terminal value at least in 5 years, High ROCE,

Long term 75% of portfolio - As long as thesis remains intact (holding since 3 years KPIT, Tejas ) others are Max India, Kore digital, Cosmic CRF, Ecoreco, Insolation energy, Aurangabad distilleries, Bondada, Basilic fly

Second high risk not more than 5% of Portfolio to review by Dec 23 and if hypothesis is wrong then exit - Coffee day (trimmed), Sonalisconsumer,

Review by next Sept 20% of portfolio and if hypothesis is right then move to long term - Kamat hotels, Patel Engineering, Silicon Rental, Hazoor, SPML infra, Mercury EV

Tracking position - Shelter Pharma, Auro impex

Booked profit in Mercury EV at 3x as needed money for preferential of Kore digital. Exited Hazoor at 3x as mangaement is not trustworthy

exited coffee day at 2x too as better opportunities available. Exited Patel engineering, Silcon rental as many companies with 50% plus CAGR available and dont want to get stuck in 20% plus CAGR.

will Hold Kamat as I feel at 100 crore PAT with 40 PE, it will reach 1000 min this year. Sonalis conusmer is only risky bet now and will wait for H2 result and if not good then will book loss. New entries are Addictive learning and Docmode

Key learnings :-

Large allocation in the early phase when high conviction in management, value, patience to let the winners run, foresight to see megatrends and future ahead in years and decades not in a quarter or year and ignore all the noise be it macro factors or fluctuations. India itself is a megatrend now as we aim to cross 30 trillion dollars and beyond in the coming decades.

As late Big bull Rakesh used to share that he does three things in equities something may be only he could pull off hence the greatest of all time (futures and options, trading upto one year then investing) – don’t want to try future and options as Vijay Kedia says – Rome was not built in a day but Hiroshima was destroyed in a day. The framework for investment – explosive growth for years ahead with reasonable valuation (50% plus CAGR with large opportunity and runaway ahead with tailwinds).

Insight from rewowned investors like Peter lynch, Rakesh Jhunjhunwala, Warren Buffet, Charlie Munger, Vijay Kedia, Bharat Shah, Madhusudan Kela, Utpal Seth, Howard Marks, Gunavanth Vaid, Mohnish Pabrai, Ridham Desai, Ramesh Damani, Ashwath Damodaran, Porinjy Veliath, Raamdeo Agrawal, Basant Maheshwari, Nilesh Shah, Ruchir Sharma, Ashish Kacholia and many other stalwarts. Almost all of them are so generous in sharing their framework, thinking process and overall experience, triumphs and failures- youtube videos of their perspective is an excellent source. More importantly anyone can see their allocation as in most the holding is above 1% so their entry and exits are in public domain. This is one of the easiest way to learn from the masters.

Anyone with class four level arithmatic and common sense can become investor as Peter Lynch shared how class seven students consistently beat returns of professional of wallstreet. Will continue to stay away from cyclicals as am not smart enough to navigate it, overvalued, hyped , stressed assets. Investing is very forgiving as all we need is a few winners. It is similar to life as all we need is to be really good at a few things, a few good relations, a wide range of interests and friendly disposition.

When one of the greatest of all time Warren Buffet says that his capital allocation decisions have been really good in single digit percentage across lifespan then one can imagine what lesser mortals can do. One also needs to look at Berkshire’s investment in Paytm (where was MOAT, cashflow, pricing power or even value) which it exited with loss after five years. How difficult it is for the most renowned institutions to practice each time what they preach! To avoid stressed assets and also very rarely on turnarounds as going up from bottom is rare. To paraphrase even the best of leaders rarely develop their weak areas because self development itself is one of the toughest things. Turning around an organisation is extremely difficult so why bet on trouble.

Sharing most of the portfolio for the long term for the framework, the terminal value in the decade ahead can be much higher and not all will go as per the projection but all one needs are a few winners as Peter Lynch said and they will take care of the rest. The idea here is to share that have a long term horizon and if one is shuffling portfolio also by looking share price regularly but not on the basis of inherent strength of business and potential (future earnings) then returns are likely to be mediocre. Investing is like life in many ways- one gets what one is searching for. It is same ocean, what is that one is looking for salt, fish or pearls so all we need are a few pearls in form of relations and stocks for life. This is a simplified framework and projection for illustration. DO YOUR OWN DUE DILIGENCE

Sir anything you have added in this fall?

I am fully invested took new entry two lots in Presstonic, will assess after April result as expecting all SMEs to deliver min 50% earning growth

Sir any view on recent saga of KoreDigital on X and clarification by management?

I have discussed with chairman many times and find mgt trustworthy. They had a conference call with investors today

Yep. Got to know about management concall today but couldn’t join as maximum limit of 100 was there.

It would be great if you can share today’s management insight.

https://twitter.com/preet2419/status/1771442915887206739

He has posted on twitter

@chitreshlunawat Do not share your personal phone number in a public forum.

Hi @Rajesh_Singh sir,

Request your views and thoughts on the following-

- Took an entry in DocMode at 246 (1 lot, before the lot size reduction). Thoughts? Is the entry a bit late?

- Considering to enter Basilic Fly now at 353. Your views on whether its guidance has been baked in? Do you think it has the potential to perform better than Digikore Studios from here? You foresee any risks?

- Considering to enter Presstonic now at 121. Do you think it will be able to scale up? Understand the growth potential though.

- Your general view on Thaai Casting? I don’t see it in your PF. Any reason why?

Thanks

Ramanjan

I know question is asked to Thread creator still would like to clarify

- Basilic and Digikore both can give good returns, who will give more depends on deal wins. Size of Digikore is small and it seems float is too cornered, good result can zoom prices and vice versa. In Basilic there will be less volatility and Kacholia sir entering Basilic it is renowned among investors. Moreover , Basilic have guided for 60-70% growth whereas Digikore is looking to double the revenue in next FY

- Presstonic have good order book and can be a good bet. Recent correction have moderated valuations from higher side

- For recent listed IPOs if one needs more clarity than can wait for H2FY24 results to see the growth of pre-ipo was paper growth or real one.

Agree with Jimmy …

Any management not walking the talk or in case of SMEs not delivering 100 percent annualised growth in H2 is red flag… There are a few stocks like Tejas, Max India which are exceptions as mgt has given guidance also for longer term…i am expecting everyone else to deliver great numbers and portfolio to be multibagger this year also like last year… Rejection ratio has to be high to choose well.

Many thanks for the reply! Thoughts on DocMode at the CMP?

Will assess post H2 results all, management is aspirational and track record is great too… Let’s see