I forget to mention about debt. But I looked at it. I think cash should be able to cover most of the debt part. Also company has got loan at low rate of interest(i think 5-7%).

1 Like

ANNUAL REPORT 2019

1 Like

One thing I would like to add is that as per investing.com charts: Aluminium Price - Investing.com India

aluminium prices seem to be near the bottom of the cycle. Although having said that no one can predict what will happen in the future (they could go lower of course).

Another good thread to track the aluminium industry and its intricacies is the nalco thread: NALCO - lowest cost producer of alumina and bauxite. the TL;DR (as per my understanding) seems to be that we are somewhat oversupplied and hence aluminium prices will remain soft unless china shuts down some of its smelters. Also, the demand from some sectors like Aviation, Automobiles would take a hit due to capex being cancelled / postponed by companies.

Adding this since the company’s output is directly used in aluminium industry and hence the health of the clients would impact Rain’s own health to some extent.

3 Likes

Rain industries conference call on 31st july 2020 at 16.00hrs.

1 Like

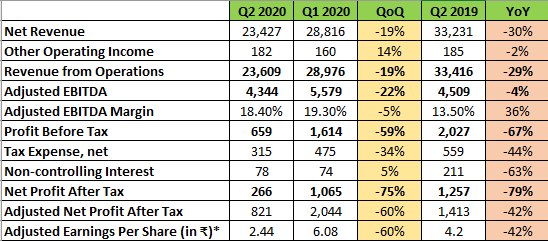

Q2 Cy2020 Earnings presentation:

Results:

My summary from the results and presentations are. If somebody can share the notes from the conf call, that will be great, to be held today…

Snapshot:

Net Revenue down ~30% YoY for the company as whole.

Carbon:

- Carbon Sales volumes decrease by ~18% YoY

- Realizations decreases by ~13% YoY ( weak demand n supply due to Covid)

- Carbon Sales Revenue decrease by ~29% YoY

Advanced Material:

- Adv. Material volumes decrease by ~20% YoY ( customer facilities shut down - partial reason)

- Realizations decreases by ~13% YoY ( weak demand n supply due to Covid)

- Adv. Material Revenue decrease by ~31% YoY

Cement - mainly due to lockdown/shutdown in india

- Cement volumes decrease by ~34% YoY

- Realizations increased by ~6% YoY

- Cement Revenue decrease by ~30% YoY

Unfortunately with Covid (& permitting) - ACP production is now probable only in Q1 2021

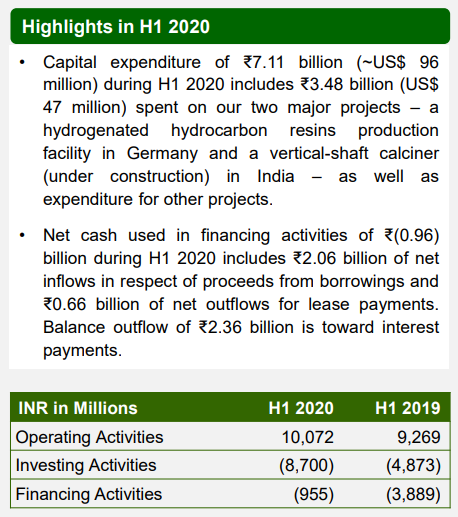

Highlights from the presentation (aggregated for quick reference):

-

Despite fall in Carbon segment EBITDA margins due to lower volumes and realisations, EBITDA for the quarter improved as a result of appreciation of USD and EURO against INR

-

Advanced Materials segment severely impacted due to decrease in commodity prices and lower demand as a result of temporary shutdowns of customer facilities on account of COVID-19

-

Cement segment performance impacted due to lower volumes resulting from COVID-19

-

CPC revenue decreased primarily on account of price decreases due to price pressure across all the regions, coupled with lower volumes as result of sluggish demand and timing of shipments

-

Pitch revenue decrease driven by lower prices due to reduced demand from aluminium and graphite industries

-

Adjusted EBITDA increased by ₹257 million due to appreciation of USD and EURO against INR

-

Revenue decrease primarily driven by lower prices due to fall in related commodity prices and sluggish demand; decrease was further driven by lower volumes due to the closure of our unprofitable Uithoorn facility

-

Adjusted EBITDA decreased by approximately ₹246 million as a result of margin pressure and lower volumes due to temporary shutdown of customer facilities and significant drop in demand by automotive, rubber and adhesives industries in response to COVID impact

-

Revenue from Cement business decreased by 30.2% due to lower volumes on account of COVID-19

-

Adjusted EBITDA from Cement business in Q2 of 2020 decreased by ₹176 million due to decline in volumes

7 Likes

they seems super impacted this time as well …earlier US sanctions, environment concerns and this time covid …

Points taken from todays conference call

- Vertical shaft calciner plant is almost ready, waiting for equipment (missed the name of the equipment) from China.

- ACP product is being tested by an independent lab and by also a couple of smelters, the testing by the independent lab is predominantly to show case that ACP is better than GCP.

- Q2 the demand has been subdued due to Covid and also China is now back, they did mention that Q1 was relatively better as they got some spot orders due to China not operational (please note Rain follows calendar year reporting - Jan to Dec)

- HHCR plant is still underway and expecting it to be commercially by Q3, this is a good margin business, did not reveal the exact range.

- In terms of the sector trend, Gerrad mentioned that the sustainability of LME Aluminium price (which is in the range of 1700USD/T) largely depends on the Inventory

- All plants are currently operational and almost at Pre-covid levels, but the management did highlight the risk on the business if the second wave spread happens.

- Their PETROS product got some good traction due to the usage on Lithium-Ion batteries

Please note these are some of the key points I made a note of, please add or correct if i may have missed or mentioned anything incorrectly.

Disclaimer : Invested and please note this is not a recommendation from my end (Not a SEBI registered member)

10 Likes

-

Vertical shaft calciner plant is almost ready, waiting for equipment (missed the name of the equipment) from China. --> FGD related equipment was pending from China.

-

HHCR plant is still underway and expecting it to be commercially by Q3, this is a good margin business, did not reveal the exact range. --> Jagan in one of the earlier concalls mentioned EBITDA range of 30-35% at full capacity utilisation for HHCR plant.

3 Likes

Thanks @anks_v10 for the update.

My two cents on Rain Industries.

Have been invested in Rain for quite some time now when I was pretty naive in terms of my exposure to the stock market (that doesnt mean I am now an expert, still learning)

These are some of the thoughts that I think if plays out could be in favor of Rain industries

- Advanced carbon segment - This holds a bunch of products which cater to various industries and are relatively high margin in comparison to the traditional carbon products - CPC and CTP, to be more specific the HHCR which could bring in additional streams of revenues and the PETRONAS (correct if I have misspelled) on the usage of Lithium-Ion batteries.

- Rain basically caters to the cyclical industries such as Aluminium and Steel (Graphite industry to be more specific), off late I have been keeping an eye on the LME prices to see the trend of the underlying commodity price which will have a meaningful impact on Rain industries, currently LME-Aluminium is around the 1700 USD/T range and if this price is sustainable then from a logical standpoint it makes sense for the Aluminium smelters to produce and in-turn favoring Rain Industries

- Their in-house ACP product can replace the GPC hurdle which they currently have can be a great game changer along with the verdict from the court on the sulphur emission norm for which they are anyway ready to meet the norms.

My investment hypothesis is slowly getting tilted towards the hope of Rain becoming a specialty chemical player instead of just a commodity player, when this transition is going to happen, I dont know, but as I go back in time and start connecting the dots, the probability of this happening is quite certain but as Investors we need to have abundant patience.

I have just put across my thoughts and no way a recommendation on this stock.

Fellow members please feel free to add.

Disclaimer : Invested not a SEBI registered member

14 Likes

Call Transcript

3 Likes

Hi Yourraj,

Reserve are generally non cash items , so they cant really use this money to pay interest ?

In Cash flow statement i cant see anywhere there is a entry called transfer to reserve.

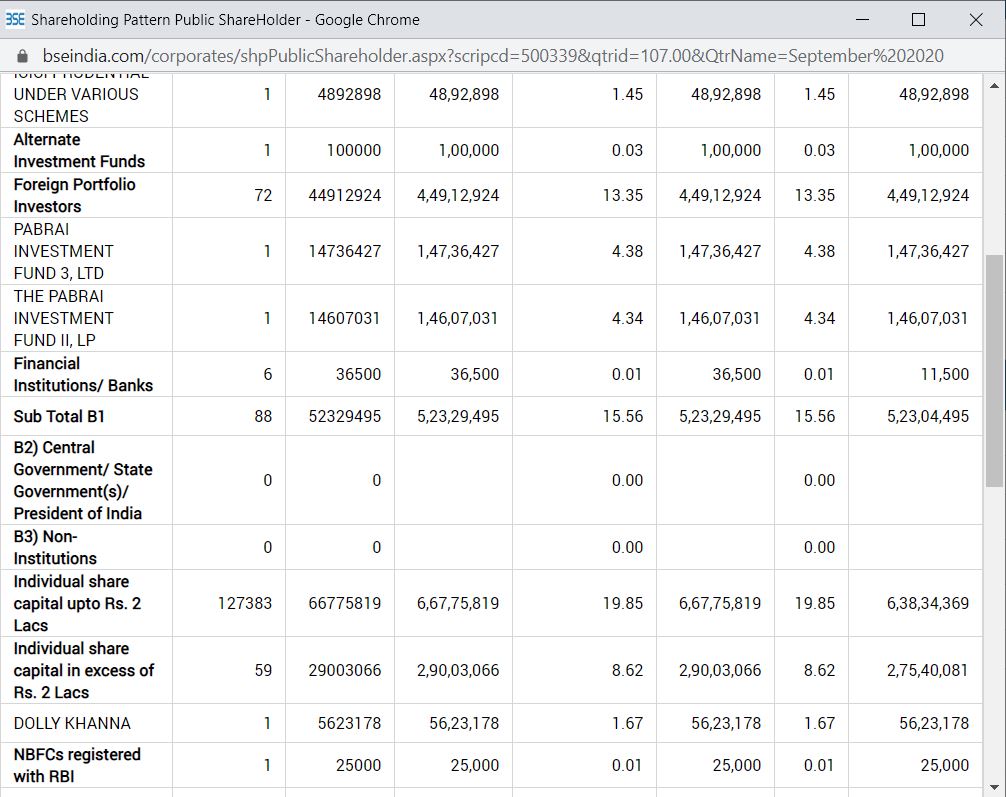

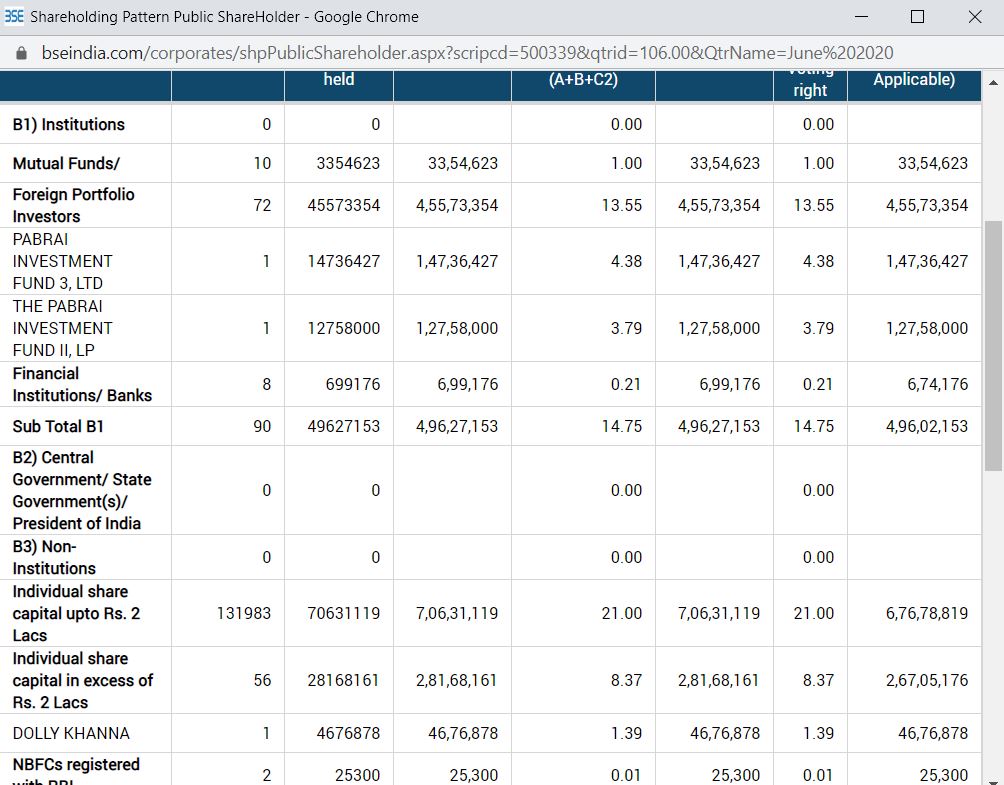

In the Sep 30th shareholding ace investors like Mohnish and Dolly Khanna increased their stakes on Rain, well, just wanted to highlight their conviction on the company.

5 Likes

Please could you verify the source of this information

Feel free to check BSE.

analyst investor call letter

1 Like